A single-member LLC is the default vehicle for a non-resident who wants a US business without a US partner. It is cheap to form, gives you an EIN and a US banking identity, and — handled correctly — often produces no US federal income tax at all. But "handled correctly" hides two things that catch nearly every founder off guard: the LLC is a disregarded entity, which means the tax question is really a question about you, the foreign owner; and since 2017 a foreign-owned single-member LLC carries a mandatory annual filing whose penalty for being missed is $25,000. This guide explains what the disregarded-entity default actually means for a non-resident, when your LLC's income is US-taxable and when it is not, the Form 5472 obligation that applies even when you owe nothing, and how the single-member structure compares with a multi-member LLC and an electing C-corporation. It is written for US persons, EU residents, and readers outside both blocs.

Doola — US single-member LLC + EIN + the annual Form 5472 filing, built for non-residents

What "single-member LLC" means before you touch tax

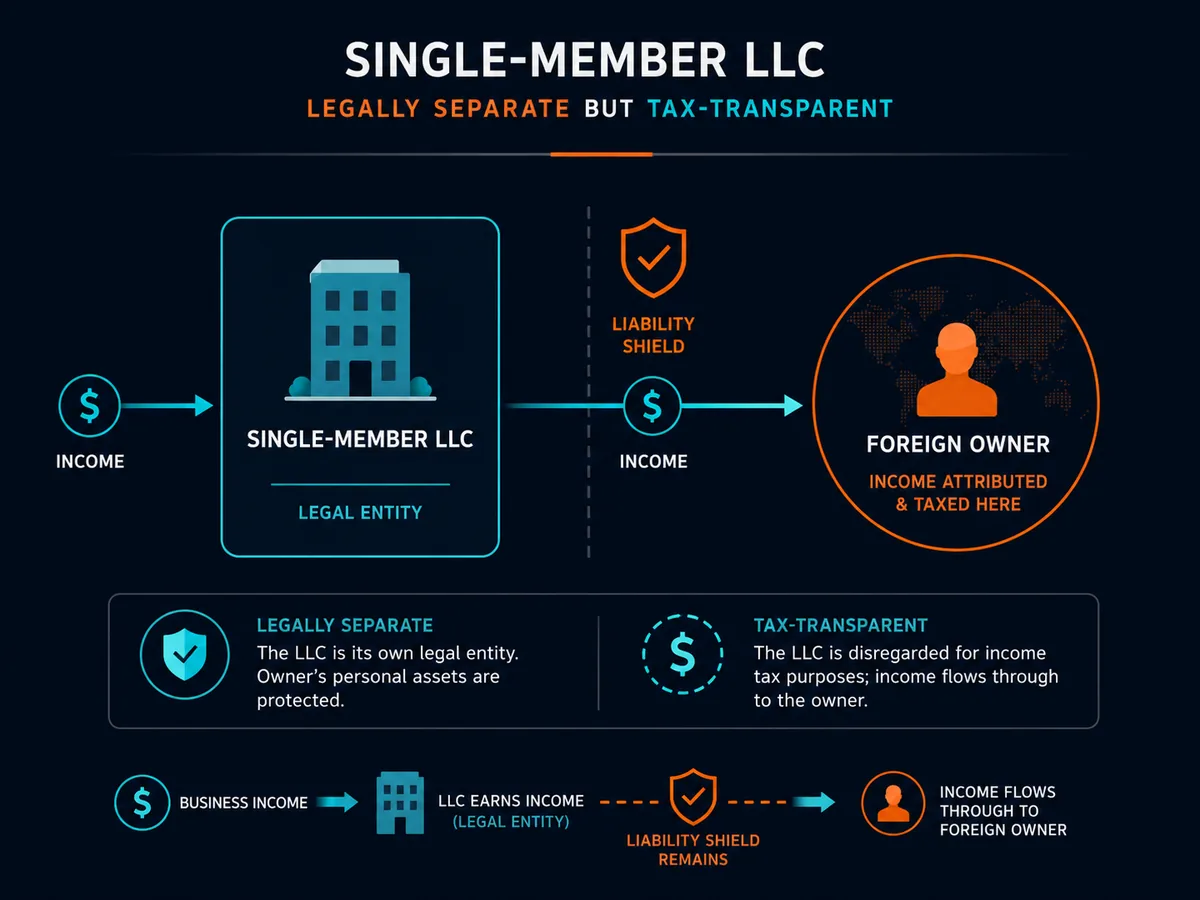

A limited liability company with exactly one owner is a single-member LLC (SMLLC). Legally, it is a distinct entity: it can sign contracts, hold a bank account, own intellectual property, and — most importantly — it interposes a liability shield between the business and your personal assets. That legal separateness is real and it does not change based on how the IRS taxes the entity. The people who sue your LLC sue the LLC, not you personally, provided you respect the formalities set out in your operating agreement and keep company and personal money apart.

Tax is where the single-member LLC does something surprising. By default the IRS does not tax it as a separate thing at all. Under the "check-the-box" regulations at 26 CFR §301.7701-3, a domestic LLC with a single owner is disregarded as an entity separate from its owner unless it affirmatively elects otherwise. This is the source of almost every misunderstanding non-residents have about the structure — so it is worth pinning down precisely.

The disregarded entity, explained for a non-resident

A disregarded entity is one the IRS looks through for federal income-tax purposes. It files no income-tax return in its own name. Its income, deductions, and assets are treated as belonging directly to its owner, as though the owner earned them personally. For a US-resident owner, that is simple: the LLC's profit lands on Schedule C of the owner's Form 1040, and the owner pays ordinary income tax and self-employment tax on it.

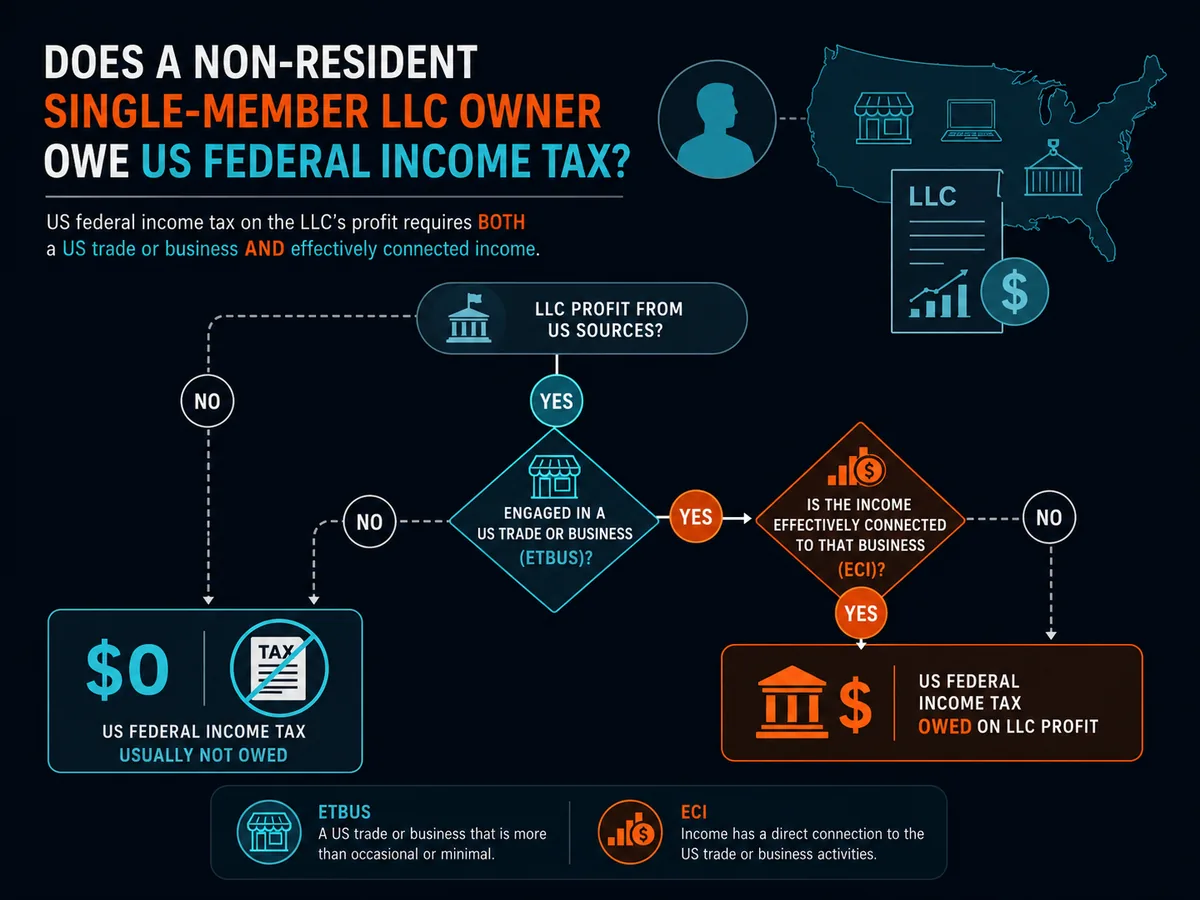

For a non-resident owner the same "look-through" happens, but what it looks through to is entirely different. The IRS does not tax non-residents on worldwide income. It taxes them under a narrow set of rules found in the international provisions of the Internal Revenue Code and summarised on the IRS Taxation of Nonresident Aliens page. So when your single-member LLC's profit is attributed to you, the question is not "how much US tax does the LLC owe" — the LLC owes none, because it is disregarded — but "does this foreign person owe US tax on this income?"

That question has two independent parts, and both must be true before US federal income tax attaches:

- Is the non-resident engaged in a US trade or business (ETBUS)?

- Is the income effectively connected income (ECI) — broadly, US-source income connected with that US trade or business?

If the answer to either is no, the profit generally escapes US federal income tax. This is why so many non-resident founders correctly pay $0 in US federal income tax on an SMLLC — and why the point is so easily overstated by marketers who present it as an automatic feature of the structure rather than a fact-specific outcome. If you are new to the term "non-resident" in the tax sense, read our explainer on what a nonresident alien is first — the definition drives everything below.

When your LLC's income is US-taxable (and when it isn't)

Engaged in a US trade or business (ETBUS). There is no bright-line statutory definition, but the concept, as the IRS describes it, turns on having activities in the United States that are considerable, continuous and regular. In practice a non-resident becomes ETBUS most clearly when the LLC has a US office or fixed place of business, US-based employees, or a dependent agent in the US who habitually acts on the business's behalf. Selling to US customers from abroad, holding a US bank account, using a US registered agent, and running payments through a US processor do not, on their own, make you ETBUS.

Effectively connected income (ECI). Once ETBUS exists, the income connected with that US business becomes ECI, and — after deductions — it is taxed at the same graduated rates that apply to US citizens, reported on Form 1040-NR. The IRS explains the mechanics on its Effectively Connected Income page. Both prongs matter: income can be US-source but not effectively connected, or connected but not enough to matter, and the sourcing rules for services generally look to where the work is performed, not where the client sits.

The archetypal $0-tax case: a developer resident in Germany owns a Wyoming single-member LLC, does all the work from Berlin, has no US office, no US staff and no US dependent agent, and invoices US and non-US clients. The service income is foreign-source (performed abroad) and there is no US trade or business, so there is no ECI and no US federal income tax on the profit — though she still has the filing duty covered in the next section, and she still owes tax in Germany. Change the facts — she hires a US-based salesperson working mainly for her, or opens a US fulfilment centre — and ECI can appear.

Two important caveats. First, US-source FDAP income (fixed, determinable, annual or periodical income such as US dividends, certain interest, royalties and rents) is taxed differently: a flat 30% withholding at source, reduced by treaty, whether or not you are ETBUS. Second, none of this is your only tax exposure — your home country almost certainly taxes the LLC's profit as your income, and a tax treaty may reallocate the rights. This article is about the US layer only, and none of it is advice for your specific facts.

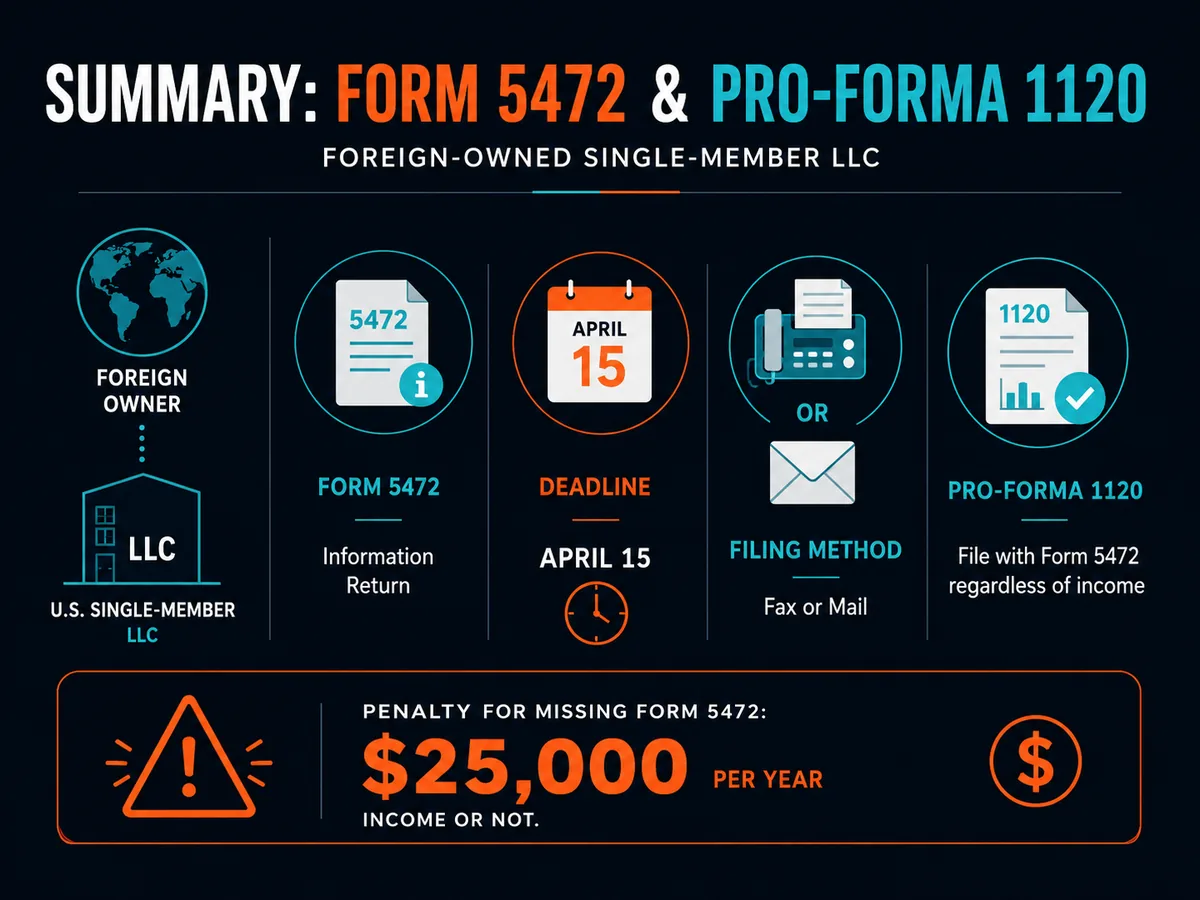

The filing you cannot skip: Form 5472 + pro-forma 1120

Here is the part that catches people. Being disregarded for income tax removed the LLC's income-tax return — but it did not remove all reporting. Since tax years beginning on or after 1 January 2017, a foreign-owned US disregarded entity is treated as a corporation for the limited purposes of IRC §6038A, under regulations at 26 CFR §301.7701-2. The practical effect: a foreign-owned single-member LLC must file Form 5472 ("Information Return of a 25% Foreign-Owned US Corporation") attached to a pro-forma Form 1120 every year it has a reportable transaction with a related party — most commonly, you.

"Pro-forma" means you complete only the identifying lines of the Form 1120 — the name and address of the LLC and boxes B and E on page one — not the full corporate income-tax return. The 1120 exists purely as a cover sheet so that Form 5472, which otherwise has no return to attach to, has somewhere to live. You are not filing a corporate income-tax return and you are not paying corporate tax; you are filing an information return. We cover the mechanics end to end in our pillar guide to IRS Form 5472.

What counts as a reportable transaction. For a disregarded entity the definition is deliberately broad. Per the Form 5472 instructions, it includes not just payments for goods and services between the LLC and its foreign owner or other related parties, but also amounts paid or received in connection with the formation, dissolution, acquisition and disposition of the entity, including contributions to, and distributions from, the entity. In plain terms: money you put into the LLC to capitalise it, and money you take out as the owner, are both reportable. That is why nearly every active foreign-owned SMLLC has at least one reportable transaction in year one and cannot argue its way out of filing.

How and when to file. The return is due by the 15th day of the fourth month after the LLC's tax year end — 15 April 2027 for a calendar-year 2026 LLC — with a six-month extension available on Form 7004. Critically, a foreign-owned DE cannot e-file this package. The IRS requires it to go by fax to 855-887-7737 or by mail to a special address: Internal Revenue Service, 1973 Rulon White Blvd, M/S 6112, Attn: PIN Unit, Ogden, UT 84201. Do not use the ordinary Form 1120 addresses.

The penalty. Under IRC §6038A(d), failure to file a substantially complete Form 5472 on time — or failure to keep the required records — is $25,000 per form, per year. If the failure continues more than 90 days after the IRS mails a notice, an additional $25,000 applies for each 30-day period (or fraction of one) it continues. The penalty is assessed automatically and does not scale to the size of the business: a dormant one-person LLC that forgot to file faces the same $25,000 as a company with real revenue. This single obligation is the reason many non-residents use a formation service that includes the annual filing rather than trusting themselves to remember it.

Single-member vs multi-member vs C-corp

The single-member LLC is one of three tax identities your US LLC can wear, and the difference is not cosmetic — each triggers a different federal regime.

Add a second member and you leave the disregarded world entirely. A multi-member LLC is, by default, a partnership. It files Form 1065, issues a Schedule K-1 to each member, and — the sharp edge for foreign owners — is subject to withholding under IRC §1446 on income effectively connected with a US trade or business that is allocated to a foreign partner, at rates up to 37% for individuals. Even with no ECI, a partnership is a full 1065 filer rather than a two-page information return. If you are genuinely the only owner, staying single-member avoids all of this; taking on even a spouse or a co-founder as a second member converts the entity into a partnership with a materially heavier compliance load.

Elect C-corporation treatment and you create a separate taxpayer. Filing Form 8832 turns the LLC into an association taxed as a C-corporation: a flat 21% federal corporate income tax on profits, plus a second layer of tax — 30% or a reduced treaty rate — when profits are paid out to the foreign owner as dividends. That double layer is a real cost, but the C-corp buys things the disregarded LLC cannot: eligibility to raise venture capital, a clean cap table, potential QSBS treatment, and the ability to retain earnings inside the US entity. It is the right structure for a fundraising startup and the wrong one for a solo consultant. Our guide to the US C-corporation for non-residents walks through when the trade-off pays off.

Note that a non-resident cannot use the S-corporation election at all: S-corps require all shareholders to be US persons, so a non-resident owner disqualifies the entity. If you have seen the S-corp discussed as a tax-saving move, it belongs to US residents — see LLC vs S-corp and the related LLC vs Inc comparison for where the line sits.

| Structure | Default for | US federal income tax | Annual federal filing | Foreign-owner note |

|---|---|---|---|---|

| Single-member LLC (disregarded) | One owner | None at entity level; owner taxed only on ECI / US-source income | Form 5472 + pro-forma 1120 (if reportable transaction) | Often $0 US tax with no US presence; $25k penalty if 5472 missed |

| Multi-member LLC (partnership) | Two+ owners | None at entity level; partners taxed on ECI | Form 1065 + K-1s | §1446 withholding up to 37% on ECI allocated to foreign partner |

| LLC electing C-corp (Form 8832) | Any (by election) | 21% corporate tax at entity level | Full Form 1120 | Plus 30% / treaty withholding on dividends to owner |

| S-corporation | US persons only | Pass-through | Form 1120-S | Not available to non-resident owners |

The EIN, banking and Stripe: why they still work

Nothing about being a disregarded entity stops a foreign-owned single-member LLC from functioning as a normal US business. To do almost anything the LLC first needs an EIN, the federal tax identifier issued under IRC §6109. Non-residents get one without an SSN or ITIN by filing Form SS-4 and writing "Foreign" in line 7b — the full procedure is in our guide to the EIN for non-US residents. The EIN is also what makes the Form 5472 filing possible, since the information return is keyed to it.

With an EIN and a US business address, the LLC can open accounts at non-resident-friendly banks and fintechs — Mercury, Relay, and Wise Business among them — and onboard to Stripe as the merchant of record. These institutions underwrite the LLC on its formation documents and EIN, not on its income-tax classification; the word "disregarded" never comes up in bank onboarding. Stripe will issue a Form 1099-K where reporting thresholds are met regardless of whether you ultimately owe US income tax, because information reporting and tax liability are separate systems. The takeaway: the disregarded status is invisible to the commercial infrastructure your business runs on. It matters only to the IRS, and only for the income-tax and 5472 analysis above.

Which state to form in

Because a single-member LLC pays no federal income tax at the entity level, the state you choose is mostly a question of state fees, privacy, and annual upkeep rather than income tax — provided the LLC has no physical nexus in any particular state. Non-residents overwhelmingly choose Wyoming, Delaware, or New Mexico, and the trade-offs among them (Wyoming's low fees and privacy, Delaware's court system and investor familiarity, New Mexico's no annual report) are covered in depth in our guide to which state is best for an LLC for a non-resident. The running cost of the structure — state fees, registered agent, mailing address, and the annual 5472 preparation — is broken down in LLC cost for non-residents.

One caution: choosing a "no income tax" state does not create a federal tax benefit that would not otherwise exist, and it does not override the ECI analysis. If the LLC is ETBUS through a fixed place of business in, say, California, then California can tax it regardless of where it was formed. State of formation and state of operation are different questions. For a non-resident with genuinely no US physical presence, the formation state is chosen for cost and privacy, and the federal outcome is driven by ECI, not by the state.

Getting it done without the $25,000 mistake

The single-member LLC is the correct default for a solo non-resident founder: it keeps the liability shield, avoids the partnership and corporate regimes, and frequently produces no US federal income tax when there is no US presence and no ECI. The failure mode is almost never the tax — it is forgetting the Form 5472 filing and walking into a $25,000 penalty on an LLC that earned little or nothing.

You can run the whole thing yourself: form the LLC with the state, get the EIN by phone or fax, and file the pro-forma 1120 + Form 5472 by the April deadline each year. Many non-residents do. But because the filing is annual, unforgiving, and cannot be e-filed, a formation-plus-compliance service earns its fee here more clearly than almost anywhere else. Doola and Firstbase both bundle formation, EIN and the annual 5472 filing for foreign-owned single-member LLCs; for the tax return itself, specialists such as Bright!Tax handle the international side. Whichever route you take, treat the 5472 as non-negotiable — it is the one deadline where forgetting is far more expensive than the LLC itself.

FAQ

Does a non-resident with a single-member LLC pay US federal income tax

It depends on two questions, not on the LLC itself. A single-member LLC is a disregarded entity, so its income is attributed to the foreign owner. That owner owes US federal income tax only if the income is effectively connected income (ECI) — broadly, US-source income connected with a US trade or business (ETBUS). A non-resident with no US office, no US dependent agent, no US employees and no US-source income generally has no ECI and therefore no US federal income tax on the LLC's profit. This is fact-specific: adding a US warehouse, US staff, or US-source services can create ECI. It is not advice — a US CPA should confirm your facts.

Do I still have to file anything if the LLC owes no US tax

Yes, and this is the trap. A foreign-owned single-member LLC that is a disregarded entity must file Form 5472 attached to a pro-forma Form 1120 every year it has a reportable transaction — even with zero income and zero tax due. Reportable transactions are defined broadly and include capital contributions into the LLC and distributions out of it, so almost every active foreign-owned LLC has at least one. The requirement comes from IRC §6038A and the 2017 regulations, not from whether you owe tax. Missing it carries a $25,000 penalty per year.

What is the penalty for not filing Form 5472

The base penalty is $25,000 per Form 5472 per taxable year for failing to file or failing to keep the required records, under IRC §6038A(d). If the failure continues more than 90 days after the IRS mails a notice, an additional $25,000 applies for each 30-day period (or part of one) the failure continues. The penalty is assessed automatically and is not scaled to the size of the LLC — a dormant one-person LLC faces the same $25,000 as a large company. This is the single most expensive mistake a foreign-owned single-member LLC can make.

What does 'disregarded entity' mean for a non-resident owner

A single-member LLC is 'disregarded as an entity separate from its owner' by default under 26 CFR §301.7701-3. For income-tax purposes the IRS looks through the LLC to the owner — the LLC files no income-tax return of its own and its profit is treated as the owner's. For a US owner that means Schedule C. For a non-resident owner it means the profit is analysed under the non-resident tax rules (ECI, US-source, treaties). Being disregarded for income tax does not remove the separate legal liability shield the LLC gives you, and — since 2017 — does not remove the Form 5472 information-reporting duty.

How is a single-member LLC different from a multi-member LLC for a non-resident

A single-member LLC is a disregarded entity by default; a multi-member LLC is a partnership by default. That changes everything downstream. A partnership files Form 1065, issues Schedule K-1s, and — critically — is subject to withholding under IRC §1446 on income effectively connected with a US trade or business allocated to foreign partners, often at 37% for individuals. A disregarded single-member LLC has no 1065 and no §1446 partnership withholding. If you are the only owner, keeping it single-member avoids the partnership regime entirely. Adding one more member converts it into a partnership.

Can a single-member LLC use Stripe and open a US bank account

Yes. Banks and payment processors care about the EIN and the formation documents, not the disregarded-entity classification. A foreign-owned single-member LLC with an EIN and a US business address can open Mercury, Relay or Wise Business accounts and onboard to Stripe. Stripe treats the LLC as the merchant of record and reports on Form 1099-K where thresholds apply, regardless of whether the owner ultimately owes US income tax. The disregarded status is an income-tax concept; the banking and payments world simply sees a US LLC with a valid EIN.

Should a non-resident elect C-corporation treatment instead

Usually not, unless you are raising venture capital or need US employees on payroll. Electing C-corp treatment via Form 8832 makes the LLC a separate taxpayer subject to the flat 21% federal corporate rate, with a second layer of tax (30% or a treaty rate) on dividends to the foreign owner. For a solo founder invoicing clients, the disregarded single-member LLC with no ECI is far cheaper — often $0 US federal income tax versus 21% plus withholding. The C-corp makes sense mainly for fundraising, QSBS eligibility, and retaining profits inside the US entity. Model both before choosing.

This guide is editorial. We hold affiliate relationships with Doola, Firstbase, Mercury, Relay, Wise and Bright!Tax, disclosed via our affiliate disclosure. Nothing here is tax or legal advice — see our disclaimer.

Ready to act on this?

Doola forms your US single-member LLC, gets the EIN, and files the annual Form 5472 — the one deadline where forgetting costs $25,000. Soveraine readers go to the front of the line through our partner link, and you fund independent editorial in the process.

Sources

- IRS — About Form 5472, Information Return of a 25% Foreign-Owned US Corporation or a Foreign Corporation Engaged in a US Trade or Business: https://www.irs.gov/forms-pubs/about-form-5472

- IRS — Instructions for Form 5472 (12/2024): https://www.irs.gov/instructions/i5472

- IRS — Taxation of Nonresident Aliens: https://www.irs.gov/individuals/international-taxpayers/taxation-of-nonresident-aliens

- IRS — Effectively Connected Income (ECI): https://www.irs.gov/individuals/international-taxpayers/effectively-connected-income-eci

- IRS — About Form 8832, Entity Classification Election: https://www.irs.gov/forms-pubs/about-form-8832

- IRS — About Form 1065, US Return of Partnership Income: https://www.irs.gov/forms-pubs/about-form-1065

- 26 U.S. Code § 6038A — Information with respect to certain foreign-owned corporations: https://www.law.cornell.edu/uscode/text/26/6038A

- 26 CFR § 301.7701-2 — Business entities; definitions: https://www.law.cornell.edu/cfr/text/26/301.7701-2

- 26 CFR § 301.7701-3 — Classification of certain business entities: https://www.law.cornell.edu/cfr/text/26/301.7701-3

- 26 CFR § 1.864-4 — US source income effectively connected with US business: https://www.law.cornell.edu/cfr/text/26/1.864-4