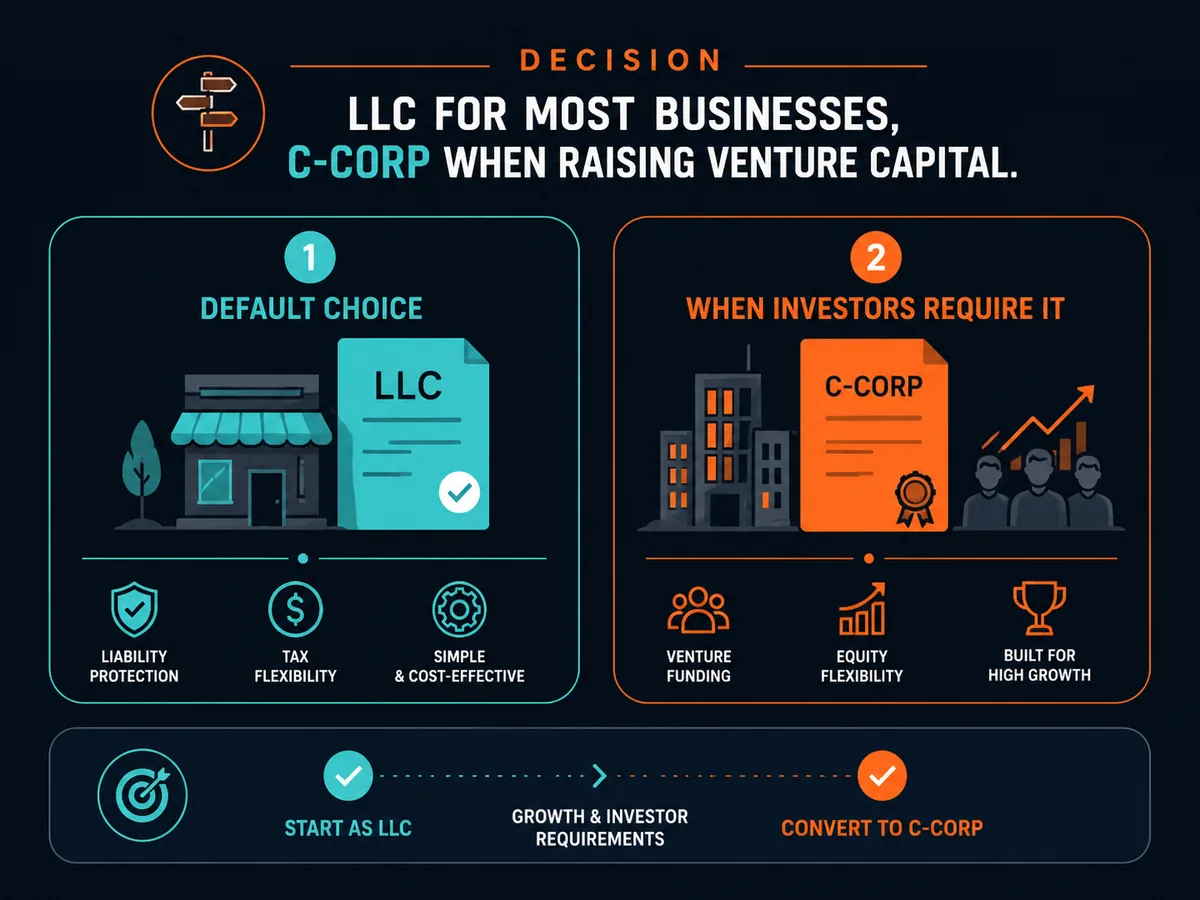

"LLC vs Inc" sounds like a single choice but is really two: a legal structure choice (LLC or corporation) and a tax choice that partly rides on top of it. Most small businesses are better off as an LLC — simpler, cheaper, taxed once. The main reason to incorporate as a C-corp is a specific one: raising venture capital. This guide draws the line clearly, covers the tax and paperwork differences, and explains the non-resident angle. Written for US founders and non-US founders using a US entity.

Firstbase.io — forms US LLCs and Delaware C-corps for global founders, with banking and compliance built in.

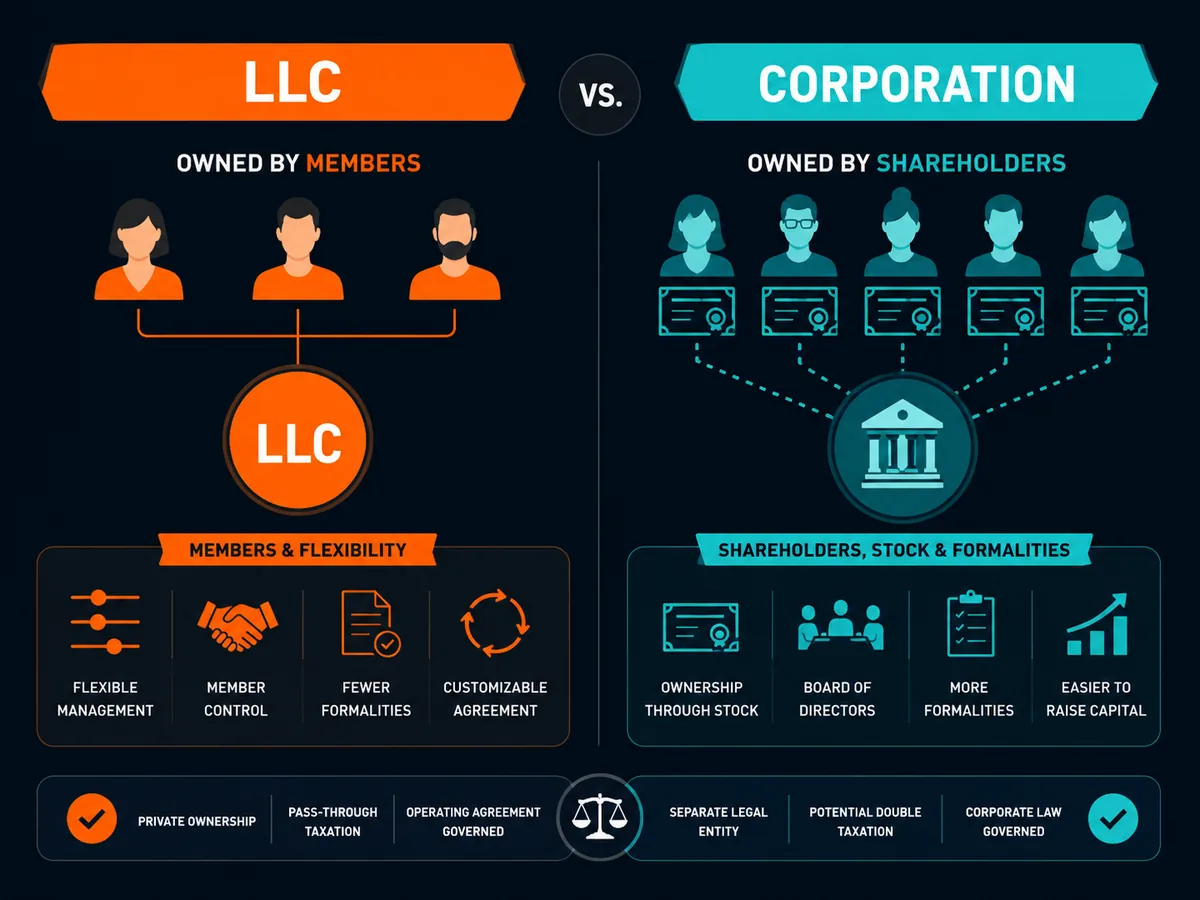

Same shield, different shape

Both an LLC and a corporation are separate legal entities that protect owners from business liabilities. The difference is in ownership and operation:

- An LLC is owned by members. It is flexible, has minimal required formalities, and is taxed as a pass-through by default.

- A corporation ("Inc") is owned by shareholders through stock. It must keep corporate formalities — bylaws, a board of directors, annual meetings, minutes — and is taxed either as a C-corp (entity-level tax) or, if it qualifies and elects, as an S-corp (pass-through).

The liability protection is comparable. The choice is about taxation, formalities, and how you intend to raise money and reward people.

Taxes: pass-through vs double taxation

This is the heart of it.

- LLC (default): profit passes through to owners and is taxed once on their personal returns. No entity-level federal income tax. See sole prop vs LLC for how the pass-through works.

- C-corporation: the company pays a flat 21% federal corporate tax on profit. When it then distributes dividends, shareholders pay tax again. That is the famous "double taxation." In exchange, a C-corp can retain earnings at the corporate rate, deduct a wide range of benefits, and — importantly for founders — issue Qualified Small Business Stock (QSBS), which can exempt a large slice of capital gains on a future sale.

- S-corporation: a pass-through like an LLC, but with restrictions (max 100 shareholders, US persons only, one class of stock). An LLC can elect S-corp tax treatment without becoming a corporation.

Because an LLC can elect S-corp or C-corp tax treatment, the legal form does not lock your tax outcome — but the corporation form is required for the investor-facing benefits.

The one reason to incorporate: raising capital

If you intend to raise venture capital, you will almost certainly need a Delaware C-corporation. Investors prefer it because:

- It issues stock, including preferred shares with the rights funds expect.

- It supports an employee stock-option pool.

- It qualifies for QSBS capital-gains treatment.

- It matches the standard legal documents the venture industry uses, and many funds cannot hold LLC interests for their own tax reasons.

This is why startups built to raise money incorporate as Delaware C-corps from day one — often through Stripe Atlas or a similar service. If you are not raising institutional equity, you usually do not need this complexity.

Paperwork and cost

An LLC is lighter to run: few required formalities, simpler filings. A corporation must adopt bylaws, maintain a board, hold annual meetings and keep minutes — more administration and more accounting cost. For a solo operator or small partnership not seeking investment, that overhead is pure friction.

The non-resident angle

For non-US founders, the same logic applies with a twist:

- Not raising VC? A US LLC is usually right — generally no US federal income tax if there is no US-effectively-connected income, but you must file Form 5472.

- Raising from US investors? You will likely need a Delaware C-corp, commonly set up through Stripe Atlas or Firstbase.

Stripe Atlas forms a Delaware C-corp, issues founder stock and gets you investor-ready.

Common mistakes

Incorporating as a C-corp "to look serious." Unless you are raising venture capital, the double taxation and formalities usually cost more than they are worth.

Assuming "Inc" saves tax. A C-corp can mean more total tax via double taxation; the saving for most small firms is the LLC's single layer.

Forgetting the LLC can elect S-corp status. You often get the self-employment-tax saving without becoming a corporation.

Non-residents choosing a C-corp by default. A C-corp creates US tax filing and potential entity-level tax you may not need if you are not raising equity.

When to consult a qualified professional

Talk to a startup attorney or CPA if you plan to raise venture capital, grant equity to employees, have co-founders with unequal stakes, or are a non-resident weighing an LLC against a C-corp. The structure is hard and costly to change after investors are on the cap table.

Soveraine is an editorial publication, not a law or accounting firm. Read our editorial policy and disclaimer before acting on anything in this article.