Stripe Atlas and a dozen other formation services will happily incorporate a Delaware C-Corp for you in two days. Most non-residents reading this article should not let them. The C-Corp exists for one specific purpose — raising US institutional venture capital — and outside that lane it is materially worse than a Delaware LLC: more expensive to form, more expensive to maintain, and stacked with two layers of tax where the LLC has one. This article covers when the structure is genuinely right, when it is wrong, and the real numbers behind both — written for US persons, EU tax residents, and readers based outside both blocs.

What a C-Corp actually is

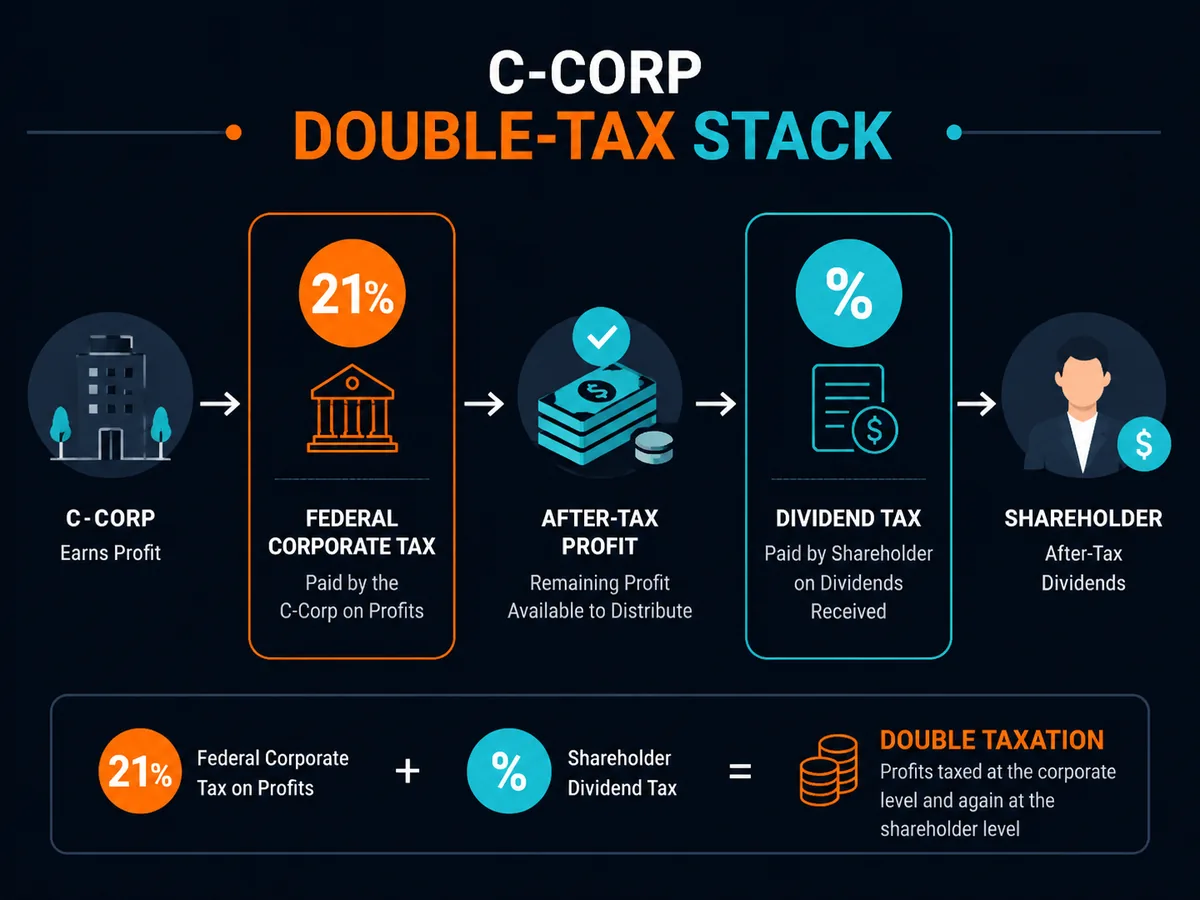

A C-Corporation is a legal entity formed under state corporate law and taxed under Subchapter C of the Internal Revenue Code. It is a separate taxable person — distinct from its shareholders, directors and officers — which is the feature that makes it useful for fundraising and burdensome for everything else.

Stripe Atlas — Delaware C-Corp or LLC with Stripe banking built in

A C-Corp pays a flat 21% federal income tax on its profits under 26 U.S. Code § 11. A Delaware-formed C-Corp that operates entirely outside Delaware owes no Delaware corporate income tax on out-of-state income, but does owe an annual franchise tax and report — minimum $450 for most small entities using the assumed par value capital method, due 1 March, per the Delaware Division of Corporations.

The second tax layer is the structural problem. Once the corporation has paid its 21%, any dividend to shareholders is taxed again at the shareholder level. For a non-resident, the default US withholding on dividends is 30% under 26 U.S. Code § 1441, reduced if a treaty applies. A Delaware LLC, by contrast, is a pass-through: profits flow to members and are taxed once, on personal returns according to the member's own residency rules. No 21% corporate layer, no dividend withholding.

Who this applies to — read this first

The C-Corp question lands very differently depending on where you live and what kind of taxpayer you are. Pick the section that matches.

US persons (citizens and green-card holders)

A US person not actively raising venture capital almost always wants an LLC. Pass-through avoids the 21% corporate layer, qualifies you to elect S-Corp treatment under 26 U.S. Code § 1361, and simplifies administration.

The single argument pulling US persons toward a C-Corp despite the double tax is Qualified Small Business Stock under 26 U.S. Code § 1202: non-corporate shareholders can exclude up to $10 million (or 10x basis) of capital gain on qualifying C-Corp stock held five years. For a venture-backed founder with a credible exit, the exclusion is enormous. For a bootstrapped consultant, it is irrelevant.

EU residents

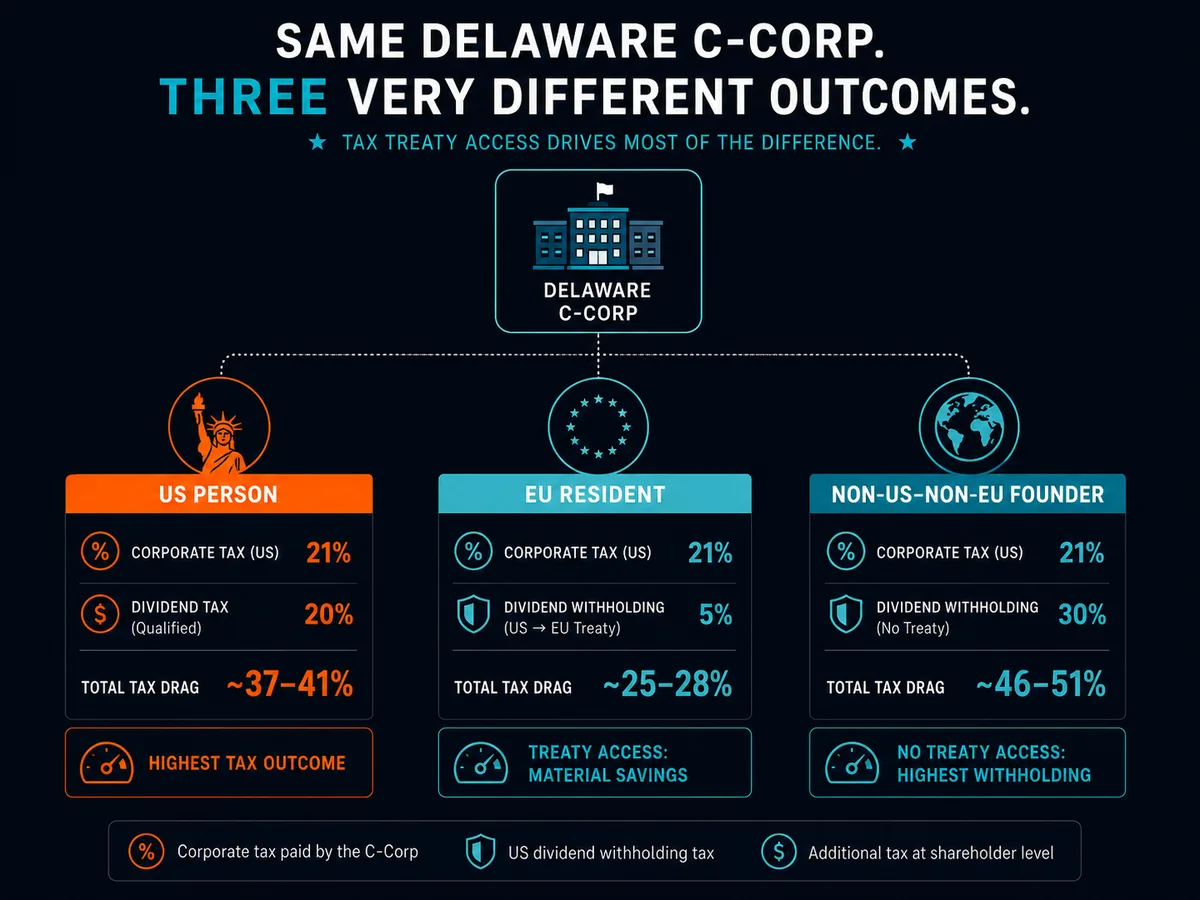

EU-US tax treaties typically reduce US dividend withholding to 5% (for 10%+ holdings) or 15% (portfolio holdings) under Article 10 of the relevant bilateral treaty — but home-country dividend taxation then layers on top. Germany taxes dividends at 26.375%, France applies the prélèvement forfaitaire unique at 30%, the Netherlands applies 26.9%, each with a credit for foreign withholding.

The EU Anti-Tax Avoidance Directive (ATAD) GAAR lets authorities disregard structures whose primary purpose is tax avoidance. Routing operations through a Delaware C-Corp purely to defer home-country tax can fail GAAR scrutiny in France, Germany, Spain and Italy. The C-Corp is not, by itself, a tax-planning tool for EU residents.

Non-US, non-EU readers

Treaty access dominates the outcome. If your country has a US tax treaty (UK, Australia, Japan, Canada, South Korea, India, Singapore, UAE), treaty-reduced withholding lands at 5–15%. If not (much of Latin America beyond Mexico, large parts of Africa and Southeast Asia), the default 30% applies to every dividend with no credit available. A Brazilian founder running a profitable Delaware C-Corp pays 21% federal corporate tax then 30% on each dividend repatriated, before Brazilian tax — an effective rate above 45%. An LLC avoids the entire stack.

When the C-Corp is right

There are three honest reasons a non-resident founder should choose a Delaware C-Corp over an LLC. All three are narrow.

Raising US venture capital

This is the dominant reason and effectively the only structural one. Every US VC term sheet — Y Combinator's SAFE, the NVCA model documents, every Series A boilerplate — assumes a Delaware C-Corporation. Funds register securities purchases on SEC Form D under Regulation D, and the legal infrastructure (preferred stock, liquidation preferences, anti-dilution clauses, option pools) requires a corporate structure.

US institutional investors will not fund a Delaware LLC. They will not fund a Wyoming C-Corp. They will, in rare cases, fund a foreign holding company with a Delaware C-Corp subsidiary — the "flip" — but that is a $20,000–$50,000 legal exercise billed back after closing. If you have a credible plan to raise US VC within 12–18 months, incorporate as a Delaware C-Corp from day one. If not, do not pre-emptively pay the corporate tax cost on the off-chance you might raise later. Conversion from LLC to C-Corp costs $3,000–$8,000 in legal fees when you actually need it.

US payroll for US-based employees

LLC or C-Corp, both can hire US employees through Gusto, Rippling or Deel. The C-Corp simplifies equity compensation: Incentive Stock Options (ISOs) under 26 U.S. Code § 422 are available only from corporations. Profits-interest equivalents through an LLC are technically possible but heavier to document, and US employees frequently mis-handle the tax filings. If your plan is to hire ten or more US employees with equity, the C-Corp pays for itself in reduced friction.

Dividend-friendly institutional investors

Some US institutional LPs — tax-exempt pensions, university endowments, sovereign wealth funds — face Unrelated Business Taxable Income (UBTI) under 26 U.S. Code § 511 when holding LLC interests. The C-Corp blocks UBTI because it is itself a tax-paying entity. If your investor base will include those LPs, the C-Corp is structurally required.

When the C-Corp is wrong

The mirror-image list is longer and applies to most readers.

Single owner with no fundraising plans

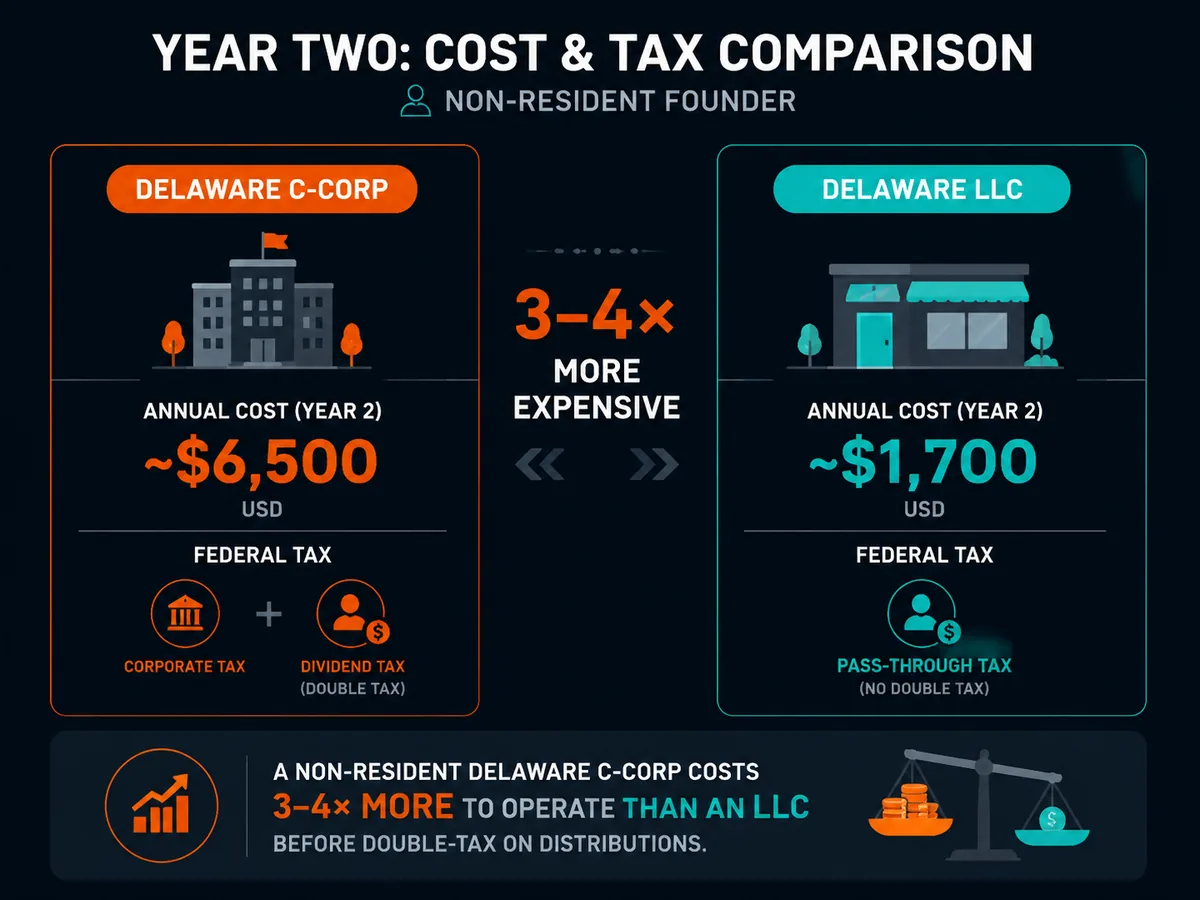

A solo non-resident founder running a profitable SaaS through a Delaware C-Corp pays 21% federal corporate tax on retained profits, then withholding on every dollar paid out. The equivalent LLC pays zero US federal income tax (assuming no effectively connected income) and zero withholding on owner distributions. At $200,000 of profit, the annual difference is roughly $42,000 in US federal tax the LLC owner does not pay.

Operating company with retained earnings

A company that reinvests most of its profit into growth still pays the 21% federal corporate tax in cash, every year, before reinvestment. The LLC passes the income to the owner, who pays personal tax on it — and in territorial-tax jurisdictions, that personal tax can be substantially lower than 21%. A Singapore-resident founder running a profitable SaaS LLC may owe close to zero US tax. The same business through a C-Corp pays the full 21% before any of that.

Solo consultant or freelancer

For US-resident solo consultants the LLC with S-Corp election is the cost-optimised structure. Non-residents cannot elect S-Corp treatment — the §1361 shareholder restriction bars non-resident aliens — so this lever is not available to foreign founders. But the underlying point holds: a freelance consultant has no use for the C-Corp's structural features and pays a real cash penalty by adopting it.

Delaware vs Wyoming vs Nevada

Three states get pitched as C-Corp jurisdictions. Only one is the real answer.

Delaware dominates for two reinforcing reasons. The Court of Chancery is a non-jury business court with 230+ years of corporate case law decided by specialist chancellors — outcomes are unusually predictable. And US venture capital has standardised on Delaware: investor expectations, law-firm templates, accelerator paperwork and option-plan precedents all assume Delaware law. Cost is real (minimum $450 franchise tax and report, registered agent $50–$300) but for a venture-track corporation paying anything else is malpractice.

Wyoming offers lower fees and stronger asset-protection statutes per the Wyoming Secretary of State. A Wyoming C-Corp's annual report is $60 minimum. For a closely held operating company that will never seek institutional capital, Wyoming is cheaper — but for anyone who might raise, Wyoming forces a conversion to Delaware that costs more than the savings.

Nevada markets aggressive privacy but charges higher annual fees than Wyoming ($150 list fee + $200 business licence + commerce tax above $4M revenue) and offers no genuine advantage. The Nevada pitch is largely marketing.

The non-resident incorporation flow

Mechanics are standardised across providers. The differences are price, polish and post-formation extras.

Stripe Atlas charges $500 flat. The fee covers Delaware filing, first-year registered agent, founder stock at appropriately low par value (typically $0.00001 per share on 10,000,000 authorised shares), 83(b) election letter templates, a basic cap table, EIN application, bylaws and board-consent templates, and a bank introduction — historically to Mercury. Atlas's defaults are venture-track. For a non-resident raising US VC, this is the path of least resistance.

Firstbase offers C-Corp formation in a similar price band with a non-resident-first interface. Doola defaults to LLC but supports C-Corp formation, leaning heavier on bookkeeping and tax prep. Northwest Registered Agent is the unbundled option — Delaware filing ($109 for a C-Corp), Northwest's basic service ($39), EIN add-on ($200+ for non-residents) — but you do the founder paperwork yourself.

For banking, Mercury remains the default for venture-track startups; Relay is the common backup when Mercury declines.

Tax filings after C-Corp incorporation

A C-Corp generates more paperwork than an LLC. Plan for the following annually.

Form 1120 — the federal corporate income tax return — is mandatory regardless of revenue. Due 15 April for calendar-year corporations.

Form 1042 and 1042-S are required whenever the corporation pays dividends or other US-source amounts to foreign shareholders. They report the gross amount paid and the tax withheld, even when treaty rates reduce withholding to zero. Missing these triggers penalties under 26 U.S. Code § 6651.

Form 5472 applies when 25%+ of the corporation is owned by a single foreign shareholder and the corporation has any "reportable transactions" with that shareholder — capital contributions, loans, distributions, payments for services. The penalty for missing it is $25,000 per form, per year, per the IRS Form 5472 instructions.

Delaware annual report and franchise tax are due 1 March. Most small C-Corps owe the $450 minimum ($50 report + $400 franchise tax) using the assumed par value capital method. Corporations that default to the authorised shares method on 10,000,000 shares face an $85,165 franchise tax bill — a notorious trap for Atlas-formed startups. Always elect assumed par value. The Delaware Division of Corporations franchise tax calculator is the authoritative reference.

State corporate income tax applies wherever the corporation has nexus. A non-resident-owned C-Corp with no US physical presence usually owes no state corporate tax outside Delaware.

Budget $1,500 to $4,000 a year for a US CPA experienced in non-resident-owned corporations. Bright!Tax and similar specialists handle this routinely.

C-Corp vs LLC for non-residents — comparison

| Feature | Delaware C-Corp | Delaware LLC |

|---|---|---|

| Federal corporate income tax | 21% on profits | None (pass-through) |

| Shareholder/member-level tax | Dividend withholding 0–30% + home country | Home country only (if no ECI) |

| Annual Delaware filing | $450+ franchise tax & report | $300 franchise tax |

| Federal tax form | 1120 (full return) | 1120 + 5472 (information only, if foreign-owned single-member) |

| VC-fundable | Yes — required by US VC convention | No — US VCs decline |

| Stock options (ISO/NSO) | Yes | Profits interests only, harder to administer |

| QSBS §1202 benefit | Yes (for US shareholders) | No |

| S-Corp election available | No (with non-resident shareholder) | Possible — but blocked by non-resident shareholders |

| Typical formation cost | $500 (Stripe Atlas) to $1,500 (with lawyer) | $39–$500 (Northwest to Atlas) |

| Typical annual tax-prep cost | $1,500–$4,000 | $400–$1,000 |

| Best for | Raising US VC; multi-employee equity plans | Bootstrapped non-residents; single owner; consulting/agency/SaaS |

Common mistakes and how to avoid them

Picking the C-Corp because Atlas defaults to it. Stripe Atlas's UI nudges toward C-Corp because the canonical Atlas user is a YC-track startup. If you are not raising, manually switch to LLC at signup. The $500 is identical; the ongoing tax cost is not.

Ignoring the Delaware franchise tax method. The default authorised-shares calculation on 10,000,000 shares exceeds $85,000. The assumed par value capital method drops this to $400. The Division of Corporations will not warn you — you must elect the favourable method on the annual report.

Missing Form 5472 on shareholder transactions. Capital contributions from a foreign owner, loans, distributions back to the owner — all reportable. The $25,000-per-form penalty is enforced. Keep a clean log and file 5472 when in doubt.

Assuming a C-Corp lowers your home-country tax. It does not. It adds a 21% US layer the LLC lacks, and your home country still taxes you on dividends, salary or CFC-imputed income.

Forming a Wyoming C-Corp expecting to raise from US VCs. They will not fund it. Conversion to Delaware costs $5,000+ and creates messy tax basis questions. If raising is the plan, Delaware from day one.

When to consult a qualified professional

Before incorporating a US C-Corp, speak to a US CPA experienced in non-resident-owned corporations (Form 1120 + 1042 + 5472 is unforgiving), a tax advisor in your country of residence (for dividend treatment and place-of-effective-management exposure), and — if you are forming to raise — a US start-up lawyer to review founder agreements, vesting and 83(b) elections before signing anything Atlas or Firstbase generated.

Soveraine publishes editorial guidance, not legal or tax advice. See our editorial policy and disclaimer.## FAQ

Should a non-resident form a US C-Corp or an LLC?

Almost every non-resident reading this question should form an LLC, not a C-Corp. The C-Corp exists for one narrow use case — raising US institutional venture capital — and US VCs require a Delaware C-Corp by convention. For everything else (bootstrapped SaaS, agency work, freelance, e-commerce, consulting), the LLC is cheaper, pass-through for tax, and avoids the 21% federal corporate income tax plus the dividend layer. Form a C-Corp only if you have an active fundraising plan with named US investors. Otherwise, an LLC does the job for less money and less paperwork.

What is the federal tax rate on a US C-Corp?

The federal corporate income tax is a flat 21% under 26 U.S. Code § 11, applied to the C-Corp's net profits regardless of who owns the company or where they live. Distributions to shareholders are then taxed again at the shareholder level — this is the double-tax problem. For a non-resident shareholder, US withholding tax on dividends is 30% by default under §1441, reduced to 5%, 10% or 15% if a treaty applies. Home-country tax on the dividend may follow. The combined effective rate often lands between 35% and 45% before treaty credits.

Why does Delaware dominate C-Corp formations?

Two reasons. The Delaware Court of Chancery is a non-jury business court with 230+ years of corporate case law, making outcomes more predictable than in any other US state. And US venture capital has standardised on Delaware C-Corps — almost every term sheet, every law firm template, every option-plan precedent assumes Delaware corporate law. Wyoming and Nevada are cheaper but no serious institutional investor will fund a non-Delaware corporation without converting it first, which costs $5,000+ in legal fees. If you are raising US VC, pay the Delaware premium upfront.

Can a non-resident own 100% of a US C-Corp?

Yes. Unlike an S-Corp (which is restricted to US persons and certain trusts), a C-Corp has no citizenship or residency requirement on shareholders, directors or officers. A non-resident can incorporate, hold 100% of the stock, and serve as sole director. The corporation still needs a registered agent in the state of incorporation, an EIN from the IRS, and US-source bank arrangements. Stripe Atlas, Firstbase and Doola all handle non-resident C-Corp formations end-to-end.

What ongoing US tax filings does a C-Corp require?

Annually: Form 1120 (the corporate income tax return) with the IRS, plus state corporate income tax returns wherever the corporation has nexus. Delaware C-Corps owe an annual report and franchise tax due 1 March — minimum $450 (a $50 report fee plus $400 minimum franchise tax) for most small corporations using the assumed par value capital method. If the corporation pays dividends or other reportable amounts to foreign shareholders, Form 1042 and 1042-S are required even when treaty rates reduce withholding to zero. Budget $1,500 to $4,000 a year for a CPA to handle this properly.

Does Stripe Atlas form C-Corps for non-residents?

Yes, and the C-Corp is Atlas's default entity choice. The $500 flat fee covers Delaware filing, first-year registered agent, founder stock issuance with par value, 83(b) election letters for founders, a basic cap table, EIN application and a bank introduction (typically Mercury). It does not cover ongoing tax filings, franchise tax, or post-formation share issuances to investors. For a venture-track startup that intends to raise within twelve months, Atlas is reasonable. For a non-resident who is not raising, Atlas is the wrong tool — pick an LLC through a registered agent instead.

Can a US C-Corp held by a non-resident make an S-Corp election?

No. The S-Corp election under 26 U.S. Code § 1361 is restricted to corporations whose shareholders are US persons, certain US trusts, or specific exempt organisations. A non-resident shareholder disqualifies the entire corporation from S-Corp status. This is a structural feature of US tax law, not a paperwork obstacle. Non-resident founders who want pass-through treatment must use an LLC (which is treated as a partnership or disregarded entity for US federal tax) rather than a corporation.

What is QSBS and does it help non-resident shareholders?

Qualified Small Business Stock under 26 U.S. Code § 1202 lets non-corporate US shareholders exclude up to $10 million (or 10x basis) of capital gain on the sale of qualifying C-Corp stock held five years. It is a major reason US founders accept the double-tax cost of a C-Corp. Non-residents do not benefit from §1202 because they are generally not subject to US capital gains tax on stock sales in the first place — the FIRPTA exception aside. If you are a non-resident, the QSBS argument does not apply to you, and one of the main pro-C-Corp arguments evaporates.

This article is editorial. See our affiliate disclosure and editorial policy for how we handle commercial relationships. Nothing here is tax or legal advice — see our disclaimer.

Ready to act on this?

Stripe Atlas — Delaware C-Corp or LLC with Stripe banking built in. Soveraine readers go to the front of the line through our partner link, and you fund independent editorial in the process.

Sources

- 26 U.S. Code § 11 — Tax imposed on corporations: https://www.law.cornell.edu/uscode/text/26/11

- 26 U.S. Code § 1441 — Withholding of tax on nonresident aliens: https://www.law.cornell.edu/uscode/text/26/1441

- 26 U.S. Code § 1361 — S corporation defined: https://www.law.cornell.edu/uscode/text/26/1361

- 26 U.S. Code § 1202 — Partial exclusion for gain from certain small business stock: https://www.law.cornell.edu/uscode/text/26/1202

- 26 U.S. Code § 422 — Incentive stock options: https://www.law.cornell.edu/uscode/text/26/422

- 26 U.S. Code § 511 — Imposition of tax on unrelated business income: https://www.law.cornell.edu/uscode/text/26/511

- 26 U.S. Code § 6651 — Failure to file tax return or to pay tax: https://www.law.cornell.edu/uscode/text/26/6651

- Delaware Division of Corporations — Franchise tax and annual report: https://corp.delaware.gov/paytaxes/

- Wyoming Secretary of State — Business Division: https://sos.wyo.gov/Business/

- IRS Form 5472 instructions: https://www.irs.gov/forms-pubs/about-form-5472

- SEC Form D — Notice of Exempt Offering of Securities: https://www.sec.gov/forms

- EU Anti-Tax Avoidance Directive (ATAD): https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32016L1164

- Stripe Atlas: https://stripe.com/atlas