"Nonresident alien" is an IRS term, not an immigration one, and it controls how much US tax a non-American actually owes. Get the status right and a non-US founder can run a US business paying little or no US income tax; get it wrong and you either overpay or face penalties. This guide explains who counts as a nonresident alien, the two residency tests, what income the US can reach, and why the status sits at the centre of the non-resident-founder playbook. Written primarily for non-US persons.

Doola — US company formation, EIN and the Form 5472 filings nonresident owners must not miss.

The definition

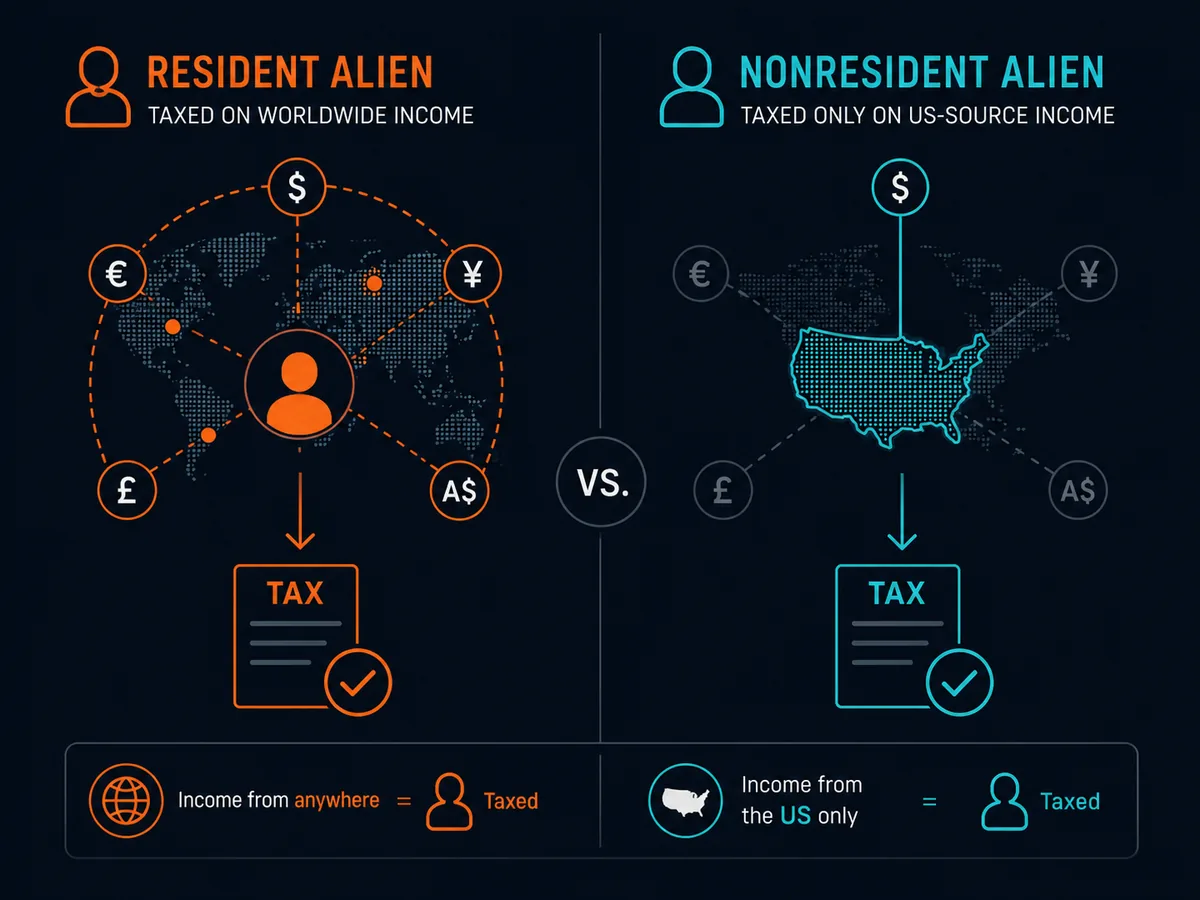

A nonresident alien is anyone who is (1) not a US citizen and (2) not a US resident for tax purposes. You are a US resident for tax — a resident alien — if you meet either of two tests:

- The green-card test: you hold lawful permanent residence (a green card).

- The substantial-presence test: you spend enough time in the US under the IRS day-count formula.

Fail both, and you are a nonresident alien. The label is about tax, set by the IRS rules on residency, and it is independent of your visa status.

The stakes are large: a resident alien is taxed on worldwide income like a citizen; a nonresident alien is taxed only on US-source income. For a founder living abroad, that difference is the whole game.

The substantial-presence test

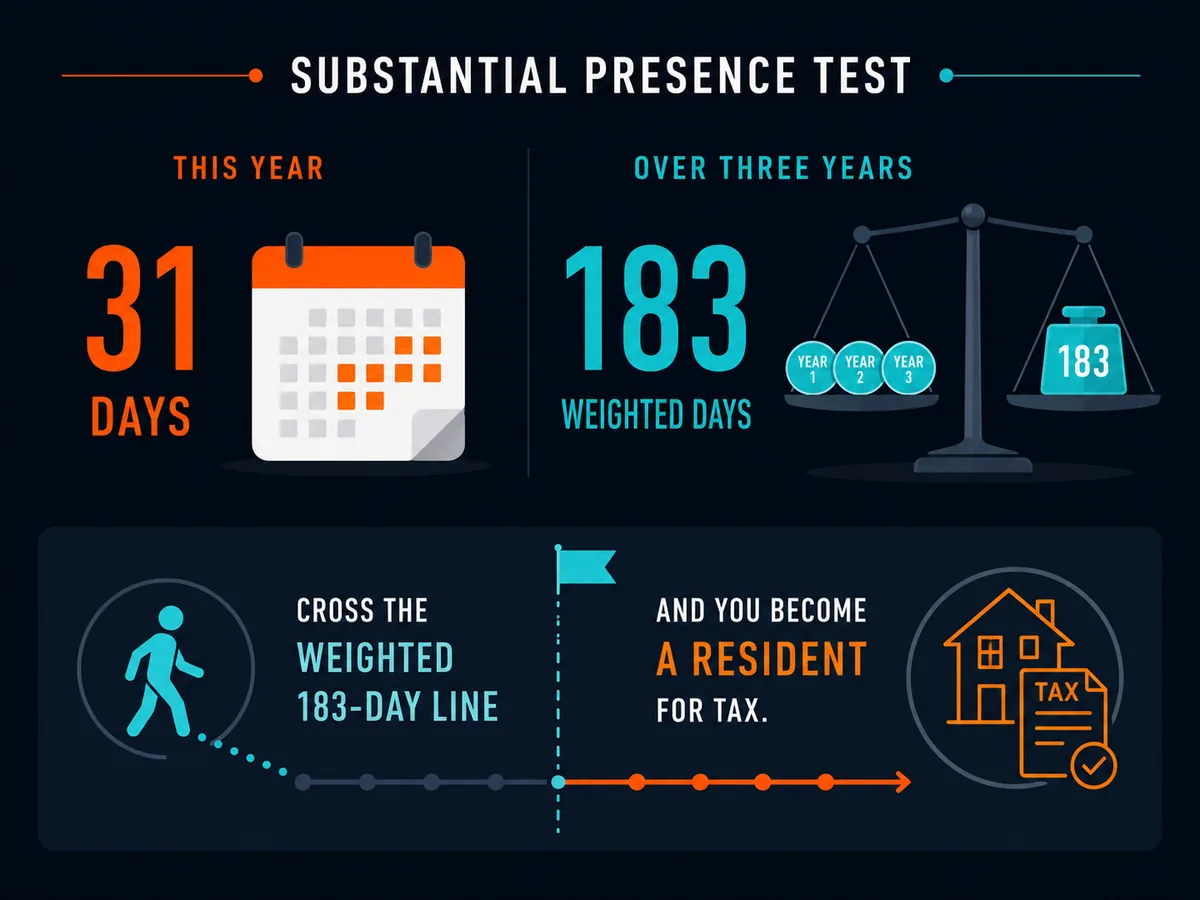

This is the test most non-citizens need to watch, because spending too much time in the US can flip you to resident status. You meet it if both are true:

- You were present in the US at least 31 days in the current year, and

- You were present 183 days over a three-year window, counting:

- all days this year, plus

- one-third of last year's days, plus

- one-sixth of the days from two years ago.

If the weighted count reaches 183, you become a resident alien and the US taxes your worldwide income. Frequent US visitors — founders doing US roadshows, snowbirds — should track days carefully. Certain people (students, diplomats, some teachers) get exempt-day treatment, and a "closer connection" exception or a treaty tie-breaker can sometimes preserve nonresident status.

What the US can tax: FDAP vs ECI

A nonresident alien's US-source income falls into two buckets, taxed very differently:

- FDAP income — fixed or determinable annual or periodical income: US dividends, interest, rents, royalties. Generally taxed at a flat 30% withholding at source, unless a tax treaty reduces the rate. No deductions.

- ECI — income effectively connected with a US trade or business. Taxed at the normal graduated rates after deductions, on a net basis, via Form 1040-NR.

Foreign-source income of a nonresident alien is generally outside US tax altogether. This is the structural reason a non-resident can sell software or services to US customers from abroad and owe no US income tax — that income is typically foreign-source, not ECI.

Why it matters for founders

This status is the foundation of the non-resident US-business playbook:

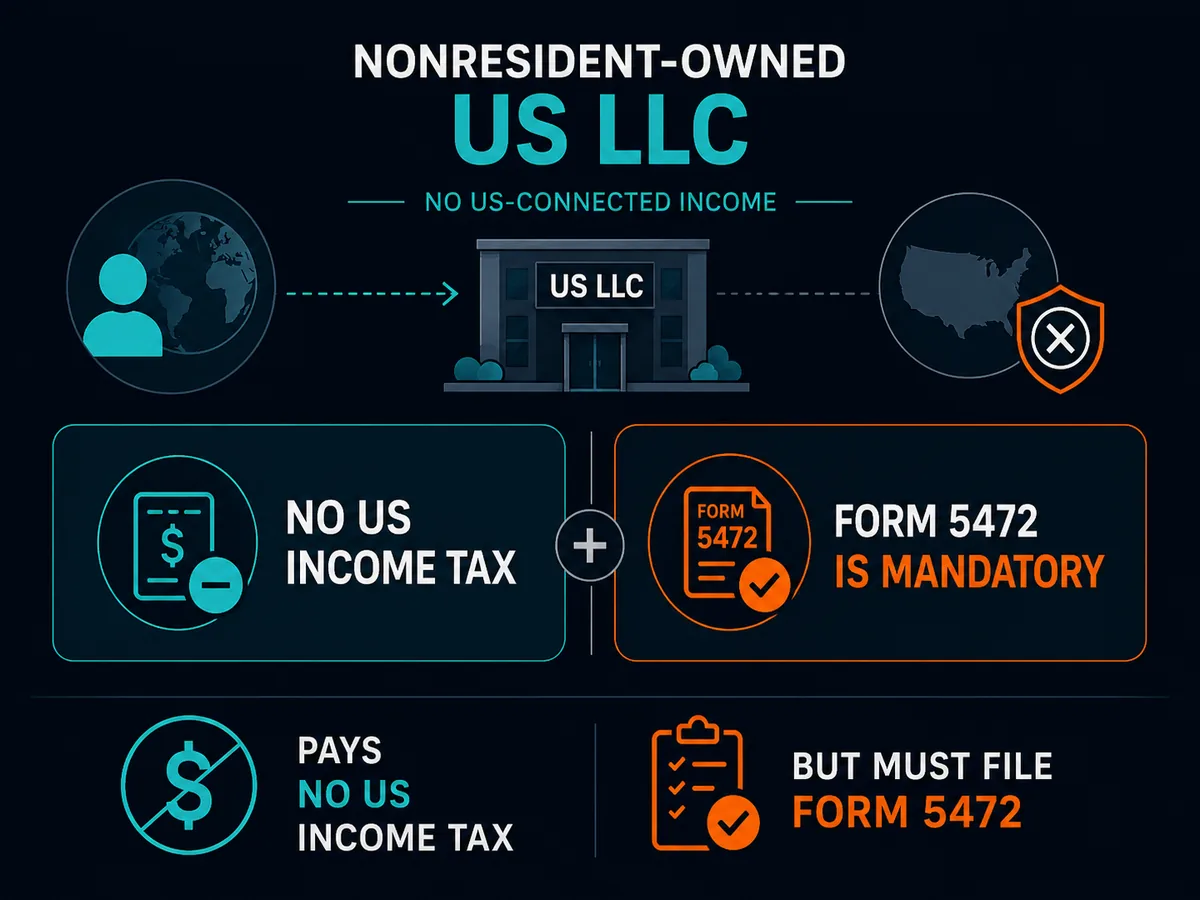

- A nonresident alien who owns a single-member US LLC with no US-effectively-connected income generally pays no US federal income tax — but the LLC must file Form 5472 annually ($25,000 penalty if missed) and needs an EIN.

- If the business develops ECI — US employees, a US office, inventory in a US warehouse, services performed while physically in the US — that income becomes US-taxable.

- A nonresident building a startup to raise US capital may instead need a US C-corporation, which changes the tax picture entirely.

Firstbase.io handles formation, EIN and compliance for founders outside the US.

Forms and numbers you will meet

- Form 1040-NR — the nonresident alien income tax return.

- Form W-8BEN — given to US payers to certify foreign status and claim treaty rates (lowers that 30% FDAP withholding).

- ITIN — an Individual Taxpayer Identification Number, for those not eligible for a Social Security number.

Common mistakes

Confusing immigration status with tax status. "Nonresident alien" is a tax classification; your visa does not decide it — the two residency tests do.

Triggering the substantial-presence test by accident. Too many US days flips you to worldwide taxation.

Owning a US LLC and ignoring Form 5472. No tax due does not mean no filing due — the penalty is $25,000.

Not filing W-8BEN. Without it, US payers withhold the full 30% on FDAP income even when a treaty would reduce it.

When to consult a qualified professional

Get advice if you spend significant time in the US, earn US-source income, own or plan to own a US entity, or are unsure whether your income is ECI. A cross-border CPA can confirm your status, file Form 1040-NR and 5472 correctly, and apply any treaty benefits.

Soveraine is an editorial publication, not a tax firm. Read our editorial policy and disclaimer before acting on anything in this article.