An Employer Identification Number is the federal tax ID the IRS assigns to a business entity — nine digits, issued once, used for every federal filing and bank account that entity ever opens. For a non-US resident with a US LLC, getting one is the second step after formation and the prerequisite for almost everything that follows: opening a Mercury or Relay account, accepting payouts through Stripe, filing the annual Form 5472 disclosure, even buying a domain through a US-billed registrar. This article covers how non-residents legitimately get an EIN without an SSN or ITIN — what Form SS-4 actually requires, the three submission routes the IRS publishes, real wait times in 2026, and the line-by-line entries that cause rejections when filled in wrong. It is written for three groups: US persons (who have the easiest path), EU residents, and readers outside both blocs.

Doola — US LLC + EIN + tax filings, built for non-residents

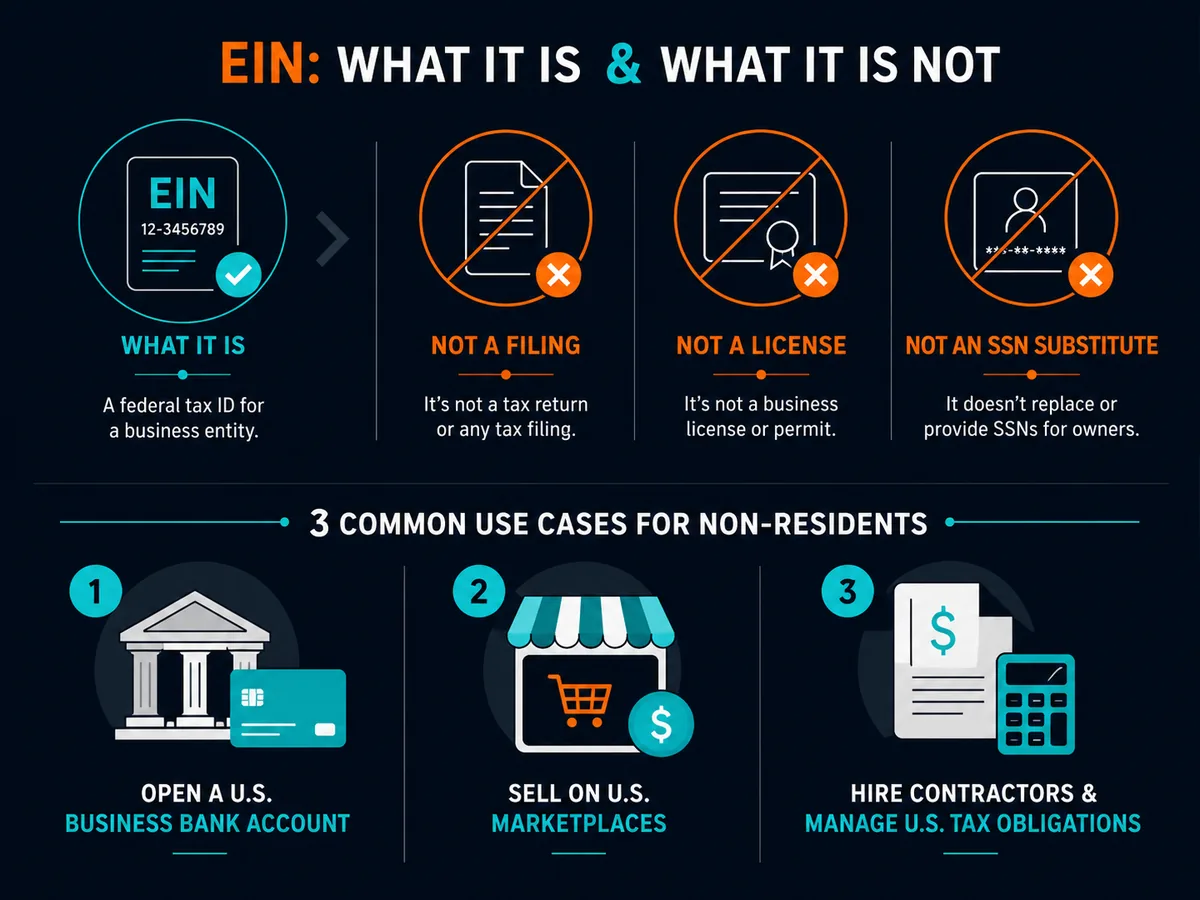

What an EIN actually is

An EIN is the entity-level identifier the IRS issues under Internal Revenue Code §6109, which gives the Secretary of the Treasury authority to require taxpayer identifying numbers on any return, statement or other document. The application form is IRS Form SS-4, and the number it produces takes the form XX-XXXXXXX. Every US business — corporation, partnership, multi-member LLC, single-member LLC that has elected corporate treatment, employer, and a long list of trusts and estates — is required to have one.

It is also useful to be precise about what an EIN is not. It is not, on its own, a tax filing. Getting an EIN does not register you for any tax, does not trigger any payment, and does not by itself create any reporting obligation. The reporting obligations come from what the entity does after the EIN exists — earning income, hiring employees, or, for a foreign-owned single-member LLC, the standalone Form 5472 requirement under IRC §6038A. An EIN is also not a substitute for an SSN in any personal context: you cannot use it to open a personal bank account, get a personal credit card, or take out a consumer loan. It is an entity ID, full stop.

Three groups commonly need one urgently. Foreign-owned single-member LLCs need an EIN to file the Form 5472 + pro-forma 1120 package each year, with $25,000-per-failure penalties for missing it. Any LLC opening a US business bank account needs the EIN before the bank will even accept the application. Sole proprietors hiring their first employee need an EIN to register for payroll taxes — but sole proprietors without employees and without a separate entity can use their personal SSN on Schedule C, which is why so many US freelancers never bother getting one.

Who needs an EIN — read this first

US persons

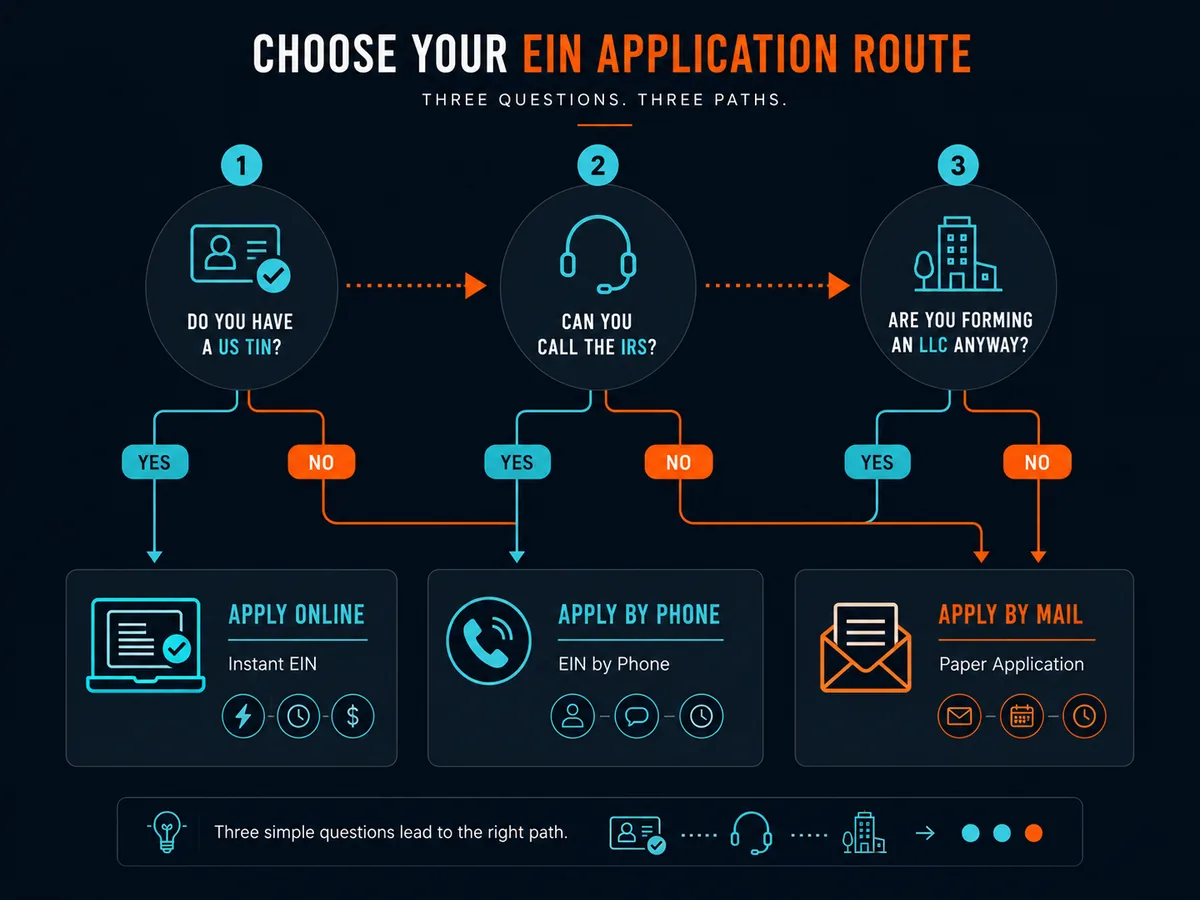

If you have an SSN or ITIN and you are forming a US LLC or corporation, the IRS EIN online application issues your EIN instantly. The session runs for 15 minutes, requires a valid US-recognised taxpayer identifier, and produces the CP 575 confirmation immediately as a downloadable PDF. The online service is available Monday through Friday, 7am-10pm ET. There is no charge. No fax, no waiting, no phone call. US persons should stop reading here and use the online route — the rest of this guide is written for applicants who do not have an SSN or ITIN.

EU residents

EU residents forming a US LLC almost never have a US taxpayer ID at the point of EIN application. The online application is closed to you, but the IRS publishes three alternatives in the SS-4 instructions: phone, fax, and mail. The phone route — the international EIN line at +1-267-941-1099, open Monday-Friday 6am-11pm Eastern Time — issues the EIN during the call and is the fastest path for anyone comfortable speaking English about LLC structure for 20-40 minutes. The fax route takes around four weeks. The mail route takes 4-8 weeks. EU residents holding an ITIN from prior US activity can use the online tool, but most never need an ITIN and apply without one.

Non-US, non-EU readers

The mechanics are identical to the EU path. Same three routes — phone, fax, mail — and the same SS-4 form. The phone option remains the fastest if you can comfortably handle a 30-minute conversation with an IRS agent about your entity. If your English is hesitant or the time difference makes calling difficult, fax is the practical default. The IRS does not discriminate by nationality on Form SS-4; it discriminates by whether you have a US-recognised TIN. The instructions for the "Foreign" entry in line 7b apply to every applicant without one, regardless of country.

The three routes

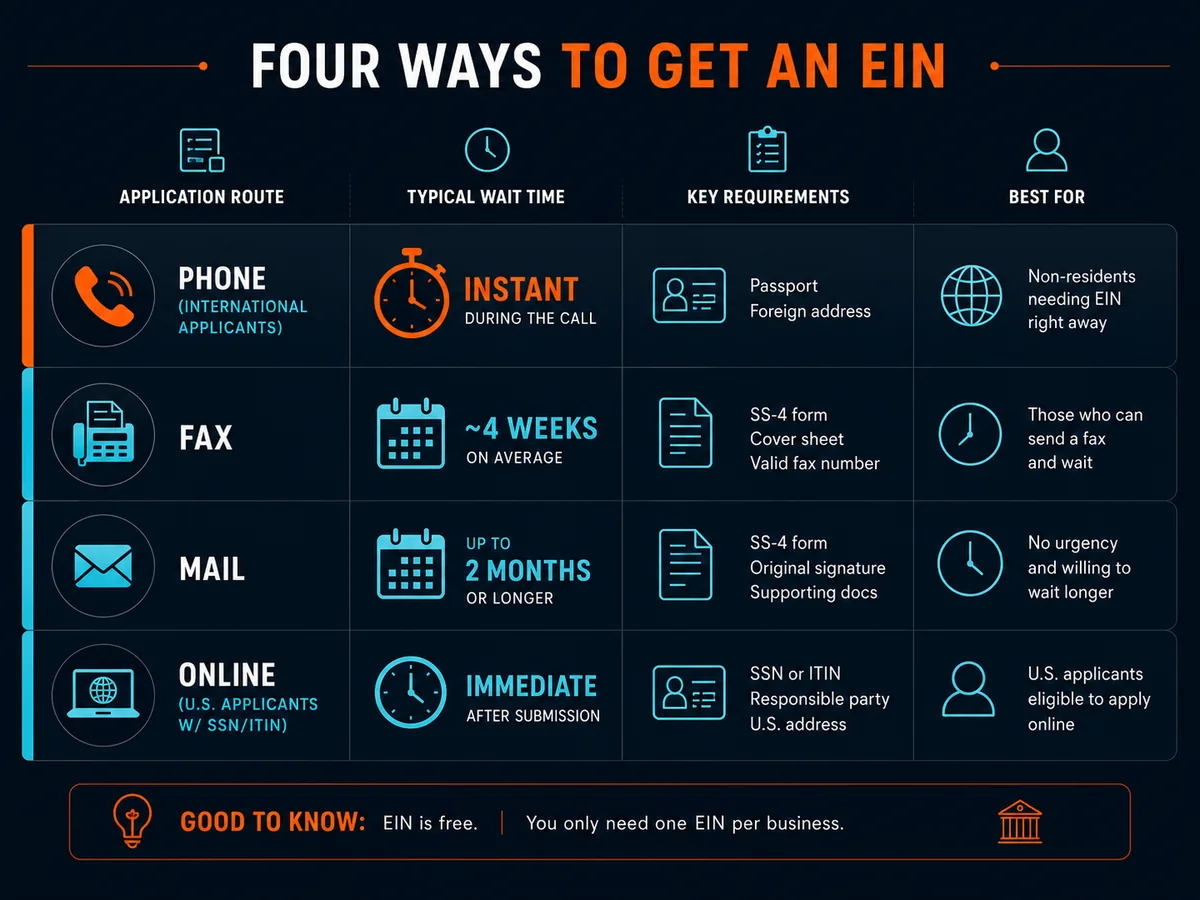

Online (US-based applicants only)

The IRS EIN Assistant is a session-based web wizard that walks you through the equivalent of Form SS-4 and issues the EIN at the end. It requires the responsible party's SSN, ITIN or existing EIN. There is a hard daily limit — one EIN per responsible party per day — and the session expires after 15 minutes of inactivity. If your structure qualifies, this is the fastest, cheapest and most reliable route. CP 575 prints to the screen and is delivered by mail within four weeks for archival. The route is closed to applicants without a US-recognised TIN; the wizard rejects the session at the TIN step.

By phone (fastest for non-residents)

The IRS Business and Specialty Tax Line for international applicants is +1-267-941-1099, open Monday-Friday 6am-11pm Eastern Time. The number is documented on the IRS International Taxpayers — Application for EIN page and in the SS-4 instructions. It is not toll-free, and call charges from outside the US can be significant — a VoIP service like Skype, Zoom or a softphone using a US calling plan keeps the cost trivial.

Prepare before dialling. The agent will work through the SS-4 form with you line by line: legal entity name, formation state, business address, responsible party name and address, the "Foreign" entry in 7b, entity type (Other LLC, plus the description "Foreign-owned single-member LLC, disregarded entity" or equivalent), reason for applying, and the principal business activity. Have your certificate of formation, your responsible party's passport details, and the LLC's US business address open in front of you. The agent issues the EIN verbally during the call — write it down twice — and mails the CP 575 confirmation to the address you give for the business. Hold times in 2025-2026 typically run 15-45 minutes; early morning Eastern Time (6-8am ET) has the shortest queues.

By fax or mail

The fax route is the published fallback for international applicants who cannot or prefer not to call. The international fax number for SS-4 is +1-855-215-1627 (from inside the US: +1-304-707-9471 — the IRS publishes the current numbers on its Where to File Your Taxes (for Form SS-4) page; verify before sending). Submit the completed and signed SS-4, plus a cover sheet indicating that you would like the EIN returned by fax to your fax number. The IRS typically faxes the EIN back within four business days when both the application and the return fax line are operating correctly, but published normal turnaround is four weeks and slow periods stretch to six.

If you do not have a fax line, services like Fax.Plus, eFax, HelloFax and SRFax all provide a US-numbered virtual fax for $5-10/month. You only need one month of service. The IRS will not fax to an international number, so the return fax line must be a US number — almost all virtual fax providers issue these by default.

Mail submission goes to:

Internal Revenue Service Attn: EIN International Operation Cincinnati, OH 45999

The mail route works but is the slowest path — typically 4-8 weeks, sometimes longer if the application has errors that trigger a request for correction. There is no reason to choose mail over fax or phone unless you cannot use the other two.

Filling SS-4 line by line

The SS-4 is two pages. Most lines are obvious; a handful cause rejections. The notes below cover the lines that consistently trip up non-residents.

Line 1 — Legal name of entity. Exactly as registered with the state. "Mountain Trail LLC," not "Mountain Trail." A mismatch forces a correction request and adds weeks.

Lines 4a/4b — Mailing address. Where the IRS mails CP 575. Use the LLC's US business address — typically the virtual mailbox covered in our US proof of address piece. Do not use the registered agent address; the IRS knows them and CP 575 may not be forwarded reliably.

Line 6 — County and state of principal business. The US county where the LLC is registered. For a Wyoming LLC, often Laramie County; for a New Mexico LLC, Bernalillo or Santa Fe. Google the county for the city your formation document lists.

Line 7a — Responsible party. The natural person who controls the entity. For a single-member LLC, the sole member. The IRS requires a human being, not another entity. Use your full legal name as it appears on your passport.

Line 7b — SSN, ITIN or EIN of responsible party. If you have an SSN or ITIN, enter it. If you do not, enter the word Foreign. Detail in the next section.

Lines 8a-8c — LLC indicators. Yes to 8a (it is an LLC). 8b = number of members (1 for a single-member LLC). 8c asks whether the LLC was organised in the US — Yes, by assumption.

Line 9a — Type of entity. Select "Other" and write a descriptive phrase. For a foreign-owned single-member LLC without a corporate election, "Foreign-owned single-member LLC, disregarded entity" is the standard wording. For multi-member, "Foreign-owned LLC taxed as partnership." If you have filed Form 8832 to elect corporate treatment, "LLC electing to be taxed as a C corporation" — with the tax consequences explored in our Stripe Atlas and Form 5472 pieces.

Line 9b — State of incorporation. The US state shown on your articles of organisation.

Line 10 — Reason for applying. "Started a new business," then a one-line description: "e-commerce," "consulting services," "SaaS." The IRS uses this for industry classification only.

Line 11 — Date business started. The date on your articles of organisation. Use US date format: month/day/year. This is the single most common error from European applicants — 03/06/2026 means 6 March to a European and 3 June to the IRS. Write the month first.

Line 12 — Closing month of accounting year. December for almost everyone.

Lines 13-15 — Employees. Most non-resident LLCs have none. Enter 0 or N/A.

Lines 16-17 — Principal activity and product. One-line category and one-line specific description. "Online sales of consumer goods," "marketing consulting services," "software-as-a-service platform."

Line 18 — Prior EIN. No for any first-time application by this exact legal entity.

Signature block. Signed under penalty of perjury. Title for an LLC member is typically "Member" or "Managing Member."

Why "Foreign" goes in box 7b

The IRS published instructions for Form SS-4 explicitly address the responsible-party identifier for international applicants. Under the heading "Specific Instructions" for Line 7b, the SS-4 instructions state that if the responsible party is a non-US person and does not have an SSN, ITIN or EIN, the applicant should enter "Foreign" in this field. There is no special form, no separate procedure, no waiver request. The word "Foreign," written in the box, is the entire procedure.

This is grounded in IRC §6109, which gives the IRS authority to require taxpayer identifiers on returns. The regulation under §6109 — 26 CFR §301.6109-1(b)(2) — provides that a foreign person who is not required to furnish a TIN under another rule need not have one. The SS-4 instruction operationalises this by accepting "Foreign" as the entry. The IRS has been processing EIN applications this way for decades; it is the standard non-resident path, not a loophole.

What is not legitimate is fabricating a number that resembles an SSN or ITIN to bypass this requirement. The form signature attests that the entries are true under penalty of perjury. "Foreign" is the correct answer for a non-resident responsible party without a US TIN; any other answer that is not truthful exposes the signer to perjury liability and guarantees rejection if discovered.

What "free EIN" services actually do

A search for "EIN for non-resident" returns dozens of services charging $50-300 for what they call an EIN application. The IRS charges nothing. What these services sell is the labour of filling out and submitting the SS-4 on your behalf — usually by fax, sometimes by phone using a CAF (Centralised Authorisation File) number that lets them act as a Third Party Designee. The form they file is the same Form SS-4 you would file yourself, and the EIN that comes back is the same nine-digit identifier issued by the same IRS unit.

The legitimate version of this service is a formation provider bundling EIN with LLC setup. Doola includes EIN in its formation packages, handles the phone or fax submission, and covers the back-and-forth if the IRS requests clarification. Firstbase does the same for global founders. Northwest sells EIN as a $50 add-on to its formation service. Bizee bundles it into mid-tier plans. For someone forming an LLC anyway, the marginal cost of having the service handle the EIN is usually $0-100 and saves a phone call or a fax setup. For someone with an already-formed LLC and no service relationship, the DIY route is straightforward.

What is not legitimate, and what some sites blur, is presenting a free government service as a paid one without disclosing that you can apply yourself. Reputable services are upfront that the IRS does not charge. Avoid any service that implies the EIN itself costs money.

After you get the EIN

The IRS issues an EIN confirmation called CP 575. It states the entity name, the EIN, and the assignment date, and it is mailed once to the address on Form SS-4. Banks treat CP 575 as the gold-standard proof of EIN — Mercury, Relay, Chase, Bank of America and the major fintechs all accept it. Keep the PDF, print a backup, and store it where you store your formation certificate.

If you lose CP 575 or never receive it, you cannot get a replacement. The IRS issues CP 575 exactly once. The substitute is Form 147c, an EIN verification letter you request by calling the Business and Specialty Tax Line at +1-800-829-4933 (or +1-267-941-1099 from outside the US) and asking the agent to send one. 147c functions as a CP 575 equivalent at every bank we have tested, but the request adds a 1-3 week mail delay and a fresh phone call. The lesson is to save CP 575 the moment it arrives.

A handful of banks — usually older regional banks — ask for CP 575 specifically on IRS letterhead and refuse photocopies. This is rare and getting rarer. For most non-resident-friendly banks (Mercury, Relay, Wise USD via Wise Business, Payoneer), a clear PDF scan or screenshot of CP 575 is sufficient.

Comparison of the four EIN routes

| Route | Wait time | Requires SSN/ITIN? | Cost | Best for |

|---|---|---|---|---|

| IRS EIN Online | Instant (within 15-min session) | Yes | Free | US persons and ITIN holders |

| IRS phone (+1-267-941-1099) | During the call, 20-40 min | No — write "Foreign" in 7b | Free + call charges | Non-residents fluent in English |

| Fax to +1-855-215-1627 | 4 weeks typical (1-6 weeks observed) | No — write "Foreign" in 7b | Free + ~$10/mo fax service | Non-residents preferring written submission |

| Mail to Cincinnati EIN International Operation | 4-8 weeks (sometimes longer) | No — write "Foreign" in 7b | Free + postage | Last resort when fax and phone unavailable |

| Paid service (Doola, Firstbase, Northwest add-on) | 1-3 weeks typical | Service handles | $0-100 bundled, $50-300 standalone | Forming LLC anyway, valuing turnkey delivery |

Common mistakes and how to avoid them

Writing the date in European format. Line 11 expects month/day/year. 03/06/2026 means 3 June 2026 to the IRS, not 6 March 2026. Triple-check every date on the form.

Using the registered agent address on lines 4a/4b. CP 575 mails to this address. If a registered agent forwards mail but does not scan it, you may never see your EIN confirmation. Use a virtual mailbox or your own US address.

Naming an entity as the responsible party. The IRS requires a natural person. Naming "Mountain Trail Holdings LLC" as the responsible party for "Mountain Trail LLC" triggers rejection. Name the human owner.

Applying before the LLC exists. Form SS-4 should follow state formation, not precede it. An EIN tied to a not-yet-formed entity becomes a recordkeeping mess.

Leaving 7b blank. A blank 7b causes rejection. The instruction is to write "Foreign" — the word is required, not optional.

Mislabelling the entity on 9a. Selecting "Sole proprietor" for an LLC is wrong even for single-member LLCs. Select "Other" and write the descriptive phrase. The IRS uses this to flag the filing requirements that follow — get it right.

Treating "Foreign-owned disregarded entity" as a tax election. The disregarded-entity classification is the default for single-member LLCs without a Form 8832 election. Writing it on 9a does not elect anything; it accurately describes the default. The Form 5472 obligation under IRC §6038A attaches automatically — see our Form 5472 piece.

Forgetting to update IRS when the address changes. Form 8822-B must be filed within 60 days of any address change for the business. Missed IRS notices remain enforceable whether you saw them or not.

When to consult a qualified professional

The SS-4 itself is straightforward enough that most non-residents complete it correctly without help. The questions where a US CPA earns their fee are downstream: whether to elect corporate treatment via Form 8832, how the LLC's classification affects state-level tax registration, and how the EIN-bearing entity fits into the owner's home-country tax filings. For Form 5472, a foreign-owned single-member LLC with any reportable transaction needs a US tax preparer with international experience — the penalties are punishing and the return is non-trivial.

The Soveraine view: get the EIN yourself if you have the time and the language, and use a bundled formation-plus-EIN service if you do not. Both produce the same nine-digit identifier and the same CP 575. What matters more than how you obtain the EIN is what you do with it afterwards — and that almost always benefits from professional advice.

FAQ

Can a non-US resident get an EIN without an SSN or ITIN

Yes. The IRS publishes a specific path for international applicants whose responsible party has neither an SSN nor an ITIN. You complete Form SS-4 and write "Foreign" in line 7b instead of a taxpayer identifier. The form is then submitted by phone (+1-267-941-1099), by fax (+1-855-215-1627 from outside the US), or by mail to the IRS in Cincinnati. The online EIN Assistant is the only route closed to you — it requires a US-recognised TIN. Every other route is open, free, and explicitly authorised under IRC §6109 and the SS-4 instructions.

How long does an EIN application take for a non-resident

By phone, the IRS issues the EIN during the call — typically 20-40 minutes once you reach an agent, with wait times that vary by hour and season. By fax, expect 4 weeks as the published norm, with 2-6 weeks observed in practice in 2025-2026. By mail, expect 4-8 weeks and sometimes longer. The online application is instant but unavailable to applicants without an SSN or ITIN. The phone route is the fastest for anyone comfortable speaking US-accented English about LLC structure on a recorded line.

Do I need an ITIN before I can apply for an EIN

No. The two identifiers serve different purposes and have no application dependency between them. An ITIN is a personal taxpayer ID for an individual who needs to file a US tax return but is ineligible for an SSN. An EIN is the entity-level federal tax ID for a business. A foreign-owned LLC needs an EIN to file its information returns (Form 5472 and pro-forma 1120) and to open bank accounts. The owner only needs an ITIN if they themselves owe US tax — for most disregarded-entity single-member LLCs with no US-source income, the ITIN can wait or never be needed.

Should I pay a service $200 to get my EIN

Only if your time is worth more than the wait. The IRS charges nothing for an EIN. A formation service that bundles EIN with LLC setup — Doola, Firstbase, Northwest's EIN add-on — earns its fee by handling the phone call, the documentation packet and the back-and-forth with the IRS. For non-residents who are also forming the LLC, the bundled price is usually defensible. For someone who already has an LLC and 30 minutes free during US business hours, the phone application costs nothing and produces the same nine-digit number.

What goes on line 7b of Form SS-4 if I have no SSN, ITIN or EIN

The word "Foreign". The IRS Form SS-4 instructions explicitly direct international applicants whose responsible party has none of those identifiers to enter "Foreign" in the SSN/ITIN/EIN field. This is not a workaround or a grey area — it is the published instruction. Leaving the field blank or fabricating an identifier causes rejection and, in the case of fabrication, exposes the applicant to perjury liability under the form's signature attestation. "Foreign" is the correct entry.

What is CP 575 and why do banks ask for it

CP 575 is the IRS confirmation letter that arrives after an EIN is assigned. It states the entity name, EIN, and the date of assignment, and it is the document banks treat as the gold-standard proof that the EIN is real. The IRS issues CP 575 only once, by mail to the address on Form SS-4. If you lose it or never receive it, you cannot get a replacement — instead, you request Form 147c (an EIN verification letter) by calling the IRS Business and Specialty Tax Line at +1-800-829-4933 (or the international line for non-residents). 147c functions as a CP 575 substitute and is accepted at Mercury, Relay, Chase and every major US bank.

Can I apply for an EIN before my LLC is officially formed

Technically yes, but it is a bad idea. The EIN is tied to the entity name and formation state on Form SS-4. If your LLC name changes between application and formation, or the state denies your formation document, you end up with an EIN attached to an entity that does not exist. The clean sequence is: form the LLC with the state, receive the certificate of formation, then file SS-4 with the exact legal name as registered. Most state formations complete in 1-7 days; the delay before EIN application is small relative to the cost of fixing a mismatched EIN later.

Does the responsible party on Form SS-4 have to be a US person

No. The responsible party is the individual who ultimately owns or controls the entity — for a single-member LLC, that is the sole member; for a multi-member LLC, typically the managing member. The IRS requires that this person be a natural person (not another entity) and that they have effective control over the entity's funds and assets. There is no nationality or residency requirement. A French resident who owns a Wyoming LLC names themselves as the responsible party, enters their French address in 7a, and writes "Foreign" in 7b. The IRS issues the EIN regardless.

This guide is editorial. We hold affiliate relationships with Doola, Northwest Registered Agent, Firstbase, Bizee, Relay and Wise, disclosed via our affiliate disclosure. Nothing here is tax or legal advice — see our disclaimer.

Ready to act on this?

Doola — US LLC + EIN + tax filings, built for non-residents. Soveraine readers go to the front of the line through our partner link, and you fund independent editorial in the process.

Sources

- IRS — About Form SS-4, Application for Employer Identification Number: https://www.irs.gov/forms-pubs/about-form-ss-4

- IRS — Apply for an Employer Identification Number (EIN) Online: https://www.irs.gov/businesses/small-businesses-self-employed/apply-for-an-employer-identification-number-ein-online

- IRS — Instructions for Form SS-4 (PDF): https://www.irs.gov/pub/irs-pdf/iss4.pdf

- IRS — Where to File Your Taxes (for Form SS-4): https://www.irs.gov/filing/where-to-file-your-taxes-for-form-ss-4

- IRS — Taxpayer Identification Numbers (TIN): https://www.irs.gov/individuals/international-taxpayers/taxpayer-identification-numbers-tin

- IRS — About Form 8832, Entity Classification Election: https://www.irs.gov/forms-pubs/about-form-8832

- IRS — About Form 8822-B, Change of Address or Responsible Party (Business): https://www.irs.gov/forms-pubs/about-form-8822-b

- 26 U.S. Code § 6109 — Identifying numbers: https://www.law.cornell.edu/uscode/text/26/6109

- 26 CFR § 301.6109-1 — Identifying numbers: https://www.ecfr.gov/current/title-26/chapter-I/subchapter-F/part-301/subject-group-ECFR65eb40c47e35dab/section-301.6109-1

- 26 U.S. Code § 6038A — Information with respect to certain foreign-owned corporations: https://www.law.cornell.edu/uscode/text/26/6038A