"LLC or S-corp?" is one of the most-searched questions in US small-business formation, and almost every guide answers it as if both options are open to everyone. They are not. Buried in the Internal Revenue Code is a rule that decides the question outright for a large share of the people asking it: an S-corporation cannot have a nonresident alien as a shareholder. If you are not a US citizen or a US tax resident, the S-corp is closed to you before the tax maths even begins — and no accountant, formation service or clever holding structure changes that. This guide is written for two readers. The first is a US person weighing a plain LLC against an S-corp election to cut self-employment tax. The second is a non-resident who needs to understand why the S-corp is off the table and what the real alternative — disregarded LLC versus C-corporation — actually is.

Doola — US LLC + EIN + tax filings, built for non-residents

The rule that decides it: no nonresident-alien shareholders

Start with the statute, because it settles the question for most Soveraine readers before anything else. Internal Revenue Code §1361(b)(1) defines a "small business corporation" — the thing that is eligible to elect S-corporation treatment — and it does so by exclusion. A corporation does not qualify if it:

- has more than 100 shareholders (subparagraph A);

- has a shareholder that is not an individual, other than an estate or certain trusts (subparagraph B);

- has a nonresident alien as a shareholder (subparagraph C); or

- has more than one class of stock (subparagraph D).

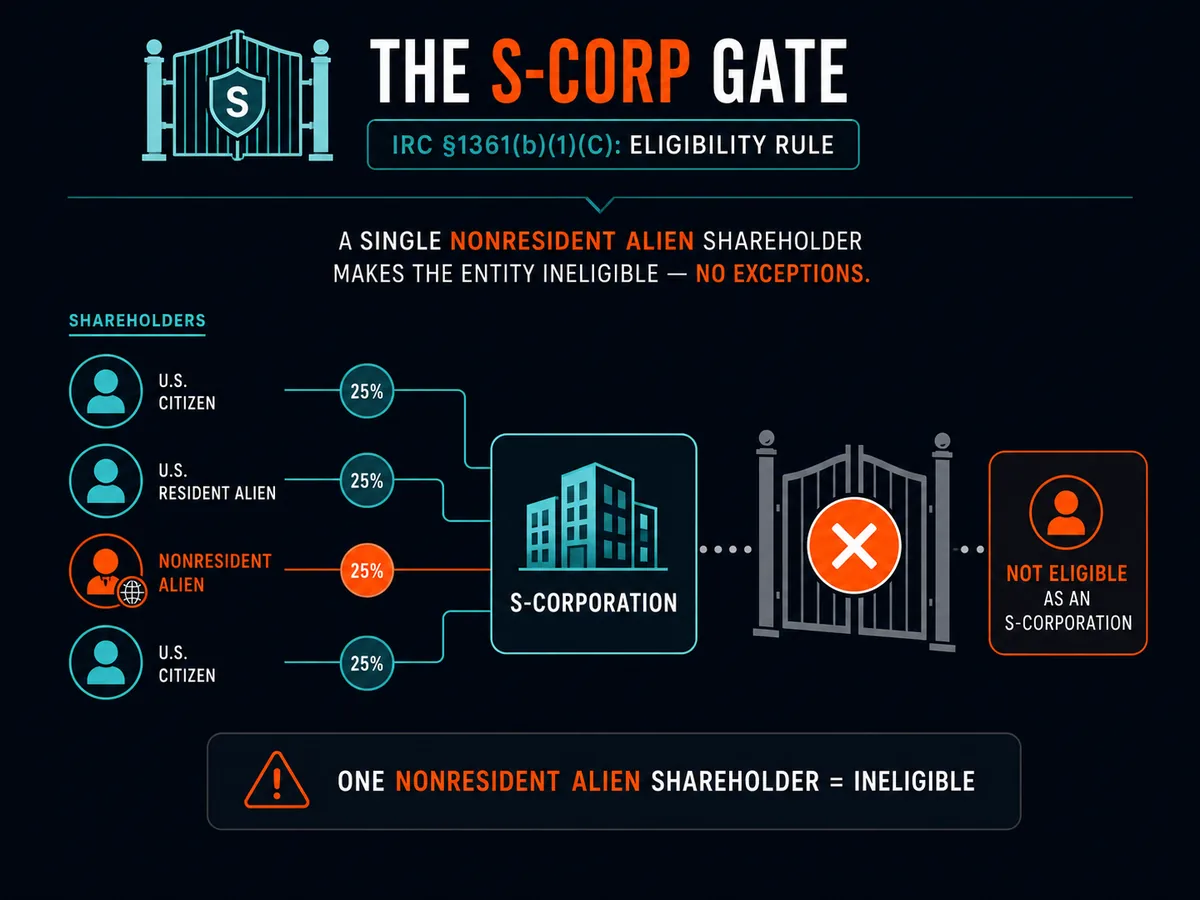

Subparagraph (C) is the one that matters here. The text is blunt: a corporation cannot be a small business corporation if it has "a nonresident alien as a shareholder." There is no threshold, no de minimis exception, no waiver. One nonresident-alien shareholder — even holding a single share — makes the entity ineligible, and if the election was already in place, it terminates it. A "nonresident alien" for this purpose is anyone who is neither a US citizen nor a US tax resident under the substantive-presence or green-card tests. If that describes you, the S-corporation does not exist as an option, full stop.

This is why so much of the generic "LLC vs S-corp" content on the web is actively misleading for an international audience. It presents the S-corp as a universal tax-optimisation lever when, for a French freelancer, a Nigerian SaaS founder or a Singaporean e-commerce seller, it is a lever they are legally forbidden to pull. Understanding this rule first saves you from chasing a structure you can never hold.

"S-corp" is a tax election, not an entity

The second thing almost every guide gets wrong is treating "S-corp" as a kind of company you go and form. You cannot. No Secretary of State issues an "S-corporation." What you form under state law is an LLC or a corporation. The "S" is a federal tax classification you layer on top by filing IRS Form 2553 with the IRS, electing to be taxed under Subchapter S of the Code.

That means the real comparison is not "LLC versus S-corp" as two rival entities. It is three tax treatments that can sit on top of one or two underlying entities:

- LLC, default treatment — a single-member LLC is disregarded (taxed as if the owner earned the income directly); a multi-member LLC is a partnership. Profit passes through to the owners and, for an active business, is subject to self-employment tax.

- LLC (or corporation) with an S-election — still a pass-through, but the owner's take is split into W-2 wages and distributions, and only the wages carry payroll tax.

- C-corporation — a separate taxpayer that pays 21% corporate income tax, with a second layer of tax when profits are distributed as dividends.

Because the S-election sits on top of a state entity, it changes nothing about your liability shield, your registered agent, your operating agreement or your annual state report. It is purely a tax overlay. This distinction — entity versus election — is the same one at the heart of our broader LLC vs Inc comparison, and it is worth internalising before you read another word of tax advice.

How the S-corp saves tax (for US persons)

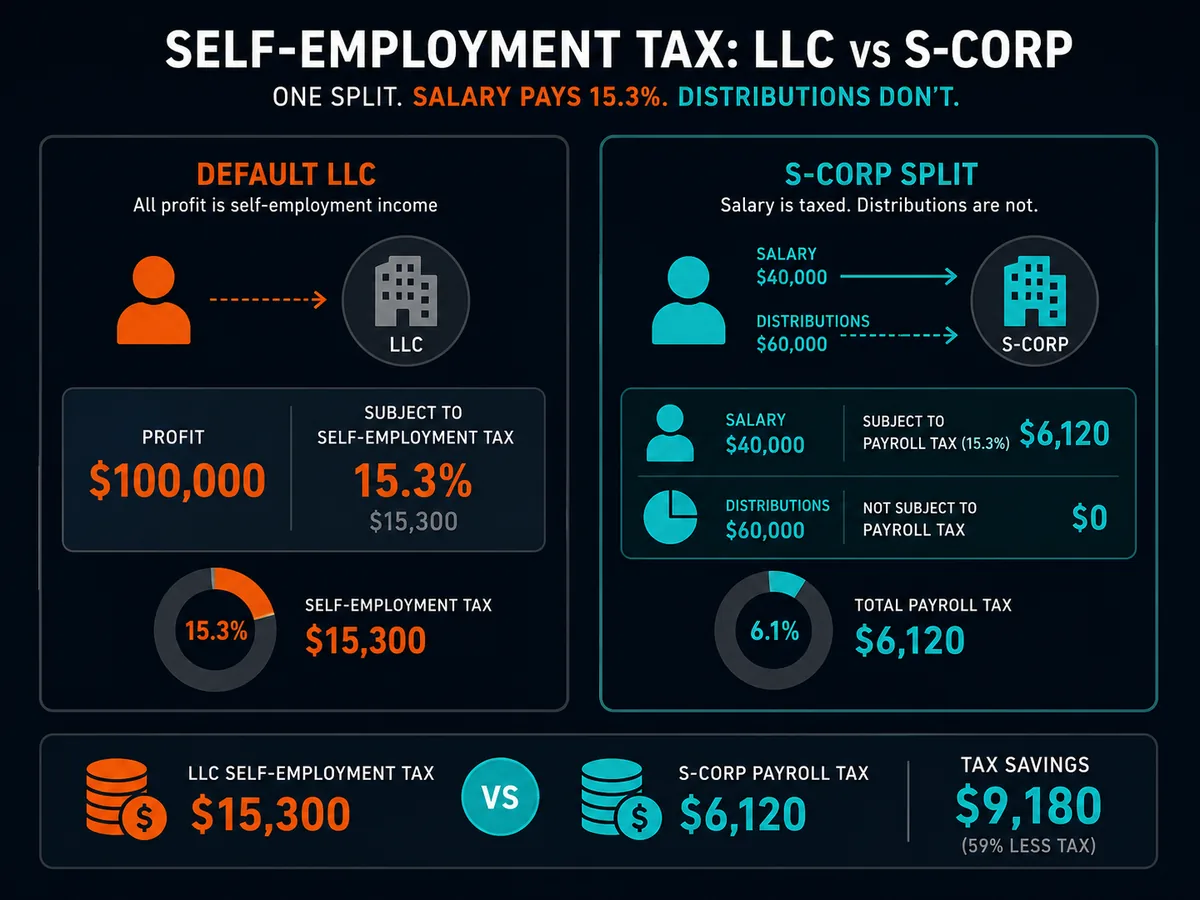

For a US person, the S-corp's appeal is one number: self-employment tax. A default single-member LLC's entire net profit from an active trade or business is subject to self-employment tax at 15.3% — 12.4% for Social Security and 2.9% for Medicare. The 12.4% Social Security portion applies only up to the annual wage base, which is $184,500 for 2026; the 2.9% Medicare portion has no ceiling, and a further 0.9% Additional Medicare Tax applies above $200,000.

Here is the mechanism. When your LLC is taxed as an S-corp, you become an employee of your own company. You pay yourself a salary through payroll, and that salary carries the full 15.3% in combined employer and employee FICA. The remaining profit — what is left after your salary — comes to you as a distribution, and distributions from an S-corp are not subject to self-employment or FICA tax at all. That difference is the whole saving.

A simplified example. Suppose your LLC nets $120,000 and you would pay yourself a reasonable salary of $70,000.

- Default LLC: all $120,000 is exposed to self-employment tax. The 15.3% bites (with a small deduction adjustment) on essentially the whole figure.

- LLC taxed as S-corp: only the $70,000 salary carries the 15.3% payroll tax. The remaining ~$50,000 distribution escapes it entirely. At 15.3%, that is roughly $7,650 saved in a single year, before payroll and filing costs.

The saving scales with the gap between total profit and reasonable salary. A business netting $250,000 with a $90,000 salary shelters $160,000 from the Medicare portion and part of the Social Security portion — a materially larger number. This is why S-corp elections cluster among profitable US-based consultants, agencies and solo professionals.

The catch: reasonable salary, payroll and real cost

The saving is not free, and the IRS has spent decades closing off the obvious abuse. If distributions escape payroll tax and salary does not, the temptation is to pay yourself a $1 salary and take everything as a distribution. That is illegal, and it is the single most litigated issue in S-corp taxation.

Reasonable compensation is mandatory

An S-corp shareholder who provides more than minor services must be paid reasonable compensation as W-2 wages before taking distributions. The IRS guidance on S-corporation compensation is explicit: where a shareholder receives or is entitled to receive cash or property, the corporation must determine and report a reasonable salary for the services performed. "Reasonable" means what you would have to pay an unrelated person to do the same job — judged on training, duties, time, comparable market pay, and the like.

The courts back the IRS hard. In David E. Watson, P.C. v. United States (8th Cir. 2012), an accountant who paid himself $24,000 while his firm distributed roughly $200,000 was reassessed on a reasonable salary of $91,044, with back payroll taxes, penalties and interest. Set your salary too low and you are not saving tax — you are deferring an assessment. A defensible S-corp salary is high enough that the distribution saving is real but not aggressive, and that ceiling limits how much you can actually shelter.

The overhead is not trivial

Running an S-corp adds fixed costs a plain LLC never incurs:

- Payroll. You must run formal payroll — withholding, quarterly Form 941, annual W-2, and usually a payroll provider at roughly $40–80/month.

- A separate tax return. An S-corp files Form 1120-S plus a Schedule K-1 to each shareholder — a corporate-style return most people cannot self-prepare, so budget $800–2,000/year for a CPA.

- State-level tax. Some states levy a franchise tax or an S-corp surcharge (California, for example, imposes a 1.5% entity-level tax with an $800 minimum) that erodes the federal saving.

- Bookkeeping discipline. Reasonable-salary defensibility and clean payroll demand tidier books than a disregarded LLC needs.

Add it up and the annual overhead runs $1,500–4,000 before the first dollar of tax is saved. That is the number the breakeven hinges on.

When the election actually beats the overhead

Put the saving and the overhead side by side and a rough threshold appears. The self-employment tax saved is 15.3% of the profit you can defensibly take as distribution rather than salary; the overhead is a largely fixed $1,500–4,000/year. The election starts to make sense once net profit is comfortably above your reasonable salary with enough left over to shelter — in practice, somewhere around $40,000 to $80,000 of net profit for most solo operators.

- Below ~$40,000 net: almost never worth it. After paying a reasonable salary there is little profit left to take as distribution, and the payroll plus 1120-S cost typically exceeds the tax saved.

- ~$40,000–80,000 net: the grey zone. It depends on your reasonable salary, your state's entity taxes, and whether you value the simplicity of a plain LLC. Model it on real numbers.

- Above ~$80,000 net: the saving usually clears the overhead comfortably, and the case for electing gets stronger as profit rises — until the Social Security wage base caps the 12.4% portion and the marginal saving narrows to the 2.9% Medicare slice.

Two caveats keep this honest. First, the breakeven is a starting point, not a formula — a high-cost-of-living profession with a naturally high reasonable salary shelters less than a business where a modest salary is genuinely defensible. Second, you can elect later. Many US founders run a default LLC for the first year or two and file the S-election once profit is reliably in the zone, which avoids paying for payroll and an 1120-S before the business can support them. The choice between a plain LLC and an S-corp is closely related to the sole proprietor versus LLC decision one step earlier in a US person's journey.

Non-residents: your real choice is LLC vs C-corp

Everything above assumes you can elect S-corp status. If you are a nonresident alien, you cannot — §1361(b)(1)(C) forecloses it — so the self-employment-tax game is not one you are playing. There is a quiet silver lining: a nonresident-owned disregarded single-member LLC with no US employees, no US office and no dependent agent generally has no US self-employment tax exposure to optimise in the first place, because the SE tax attaches to a US trade or business carried on by a US person. For most non-resident solo founders, the S-corp's entire benefit is solving a problem you do not have.

So your decision collapses to two genuine options.

Disregarded single-member LLC (the usual answer)

For a non-resident freelancer, consultant, e-commerce seller or SaaS founder operating solo, a single-member LLC is almost always the right structure. It is a pass-through, taxed only on US-source income effectively connected to a US trade or business; for many location-independent founders selling to a global market with no US nexus, that US tax can be zero. The main federal compliance is the annual Form 5472 + pro-forma 1120 information return, backed by an EIN you can get without an SSN. It is cheap, fast to form, and light to run. This is the default we recommend for the large majority of non-resident readers.

US C-corporation (when you need it)

The US C-corporation for non-residents is the entity you reach for when the LLC's simplicity is not what you need. Choose it when you plan to raise money from US venture capital or angels (investors expect a Delaware C-corp), issue stock options to a team, retain profits inside the company at the flat 21% corporate rate rather than passing them to yourself, or want a single clean US taxpayer that files its own return. The price of that is the C-corp's defining feature: two layers of tax — 21% at the corporate level, then tax again on dividends when profit is distributed, with 30% US withholding on dividends to a non-resident unless a tax treaty reduces it. Forming a C-corp means filing articles of incorporation and running corporate formalities the LLC does not require. Our dedicated guide walks through exactly when that second tax layer earns its keep.

The one structure that is never on your menu, no matter how your business grows, is the S-corp. If a formation service or forum post suggests a non-resident "elect S-corp for the tax savings," that advice is simply wrong on the law.

The comparison table

The table below sets the three tax treatments side by side, with the column that most guides omit entirely: whether a nonresident alien is eligible.

| Feature | LLC (default) | LLC + S-corp election | C-corporation |

|---|---|---|---|

| What it is | State entity, default tax treatment | State entity + IRS Form 2553 election | State entity, default corporate tax |

| Federal tax treatment | Pass-through (disregarded / partnership) | Pass-through, salary + distribution split | Separate taxpayer, 21% corporate rate |

| Layers of tax | One (owner level) | One (owner level) | Two (corporate + dividend) |

| Self-employment / payroll tax | 15.3% on all active net profit (US persons) | 15.3% on salary only; distributions exempt | N/A — owner is a W-2 employee/shareholder |

| Reasonable-salary rule | No | Yes — mandatory before distributions | Yes, if owner works in the business |

| Annual federal return | Schedule C / Form 1065 (or 5472+1120 if foreign-owned) | Form 1120-S + K-1 | Form 1120 (+ 5472 if foreign-owned) |

| Nonresident alien eligible? | Yes | No — barred by IRC §1361(b)(1)(C) | Yes |

| Best suited to | Solo founders, non-residents, low overhead | Profitable US persons above ~$40–80k net | Fundraising, equity plans, retained earnings |

Read the eligibility row first if you are a non-resident: two of the three columns are open to you, and the middle one — the whole reason people search "LLC vs S-corp" — is not.

How to actually elect (US persons)

If you are a US person and the numbers point to electing, the mechanics are straightforward. You file Form 2553, Election by a Small Business Corporation, signed by all shareholders. The timing rule matters: to have the election apply for the current tax year, you generally must file within 2 months and 15 days of the start of that tax year (by 15 March for a calendar-year taxpayer electing for that year), or at any time in the preceding tax year. The IRS does grant late-election relief under Revenue Procedure 2013-30 if you file within roughly three years and 75 days and can show reasonable cause, but do not rely on it — file on time.

Once the election is in place you must run payroll from day one of S-corp treatment, set a defensible reasonable salary, and file Form 1120-S annually. Most US owners hand the payroll and the 1120-S to a service. Formation platforms that also handle ongoing compliance — ZenBusiness and Bizee among them — offer S-corp election and payroll add-ons, and a US CPA is well worth the fee to set the salary and file the return correctly the first year.

When to consult a professional

The LLC-versus-S-corp decision is genuinely numbers-driven, and the numbers are personal: your net profit, your defensible salary, your state's entity taxes, and your appetite for administrative work. A US CPA can model the breakeven on your actual figures in an hour and is the right person to set a reasonable salary you can defend if examined. For non-residents, the professional questions are different — not "S-corp or not" (that is settled) but whether your activity creates a US trade or business, whether you have US-source effectively connected income, and whether an LLC or C-corp better fits your funding and home-country tax position.

The Soveraine view: if you are a US person netting comfortably above your reasonable salary, model the S-corp election seriously — the self-employment-tax saving is real and often several thousand dollars a year. If you are a non-resident, forget the S-corp entirely and decide between a disregarded LLC and a C-corp on the basis of whether you are raising money and issuing equity. In both cases, the entity is easy; the tax treatment is where the money is.

FAQ

Can a non-US resident own an S-corporation

No. Internal Revenue Code §1361(b)(1)(C) states plainly that a corporation cannot qualify as an S-corporation if it has "a nonresident alien as a shareholder." The moment a nonresident alien holds even one share, the S-election is invalid or terminates. This is not a paperwork hurdle you can plan around — it is a hard eligibility bar written into the statute. A non-resident's real choice is therefore between a disregarded single-member LLC (default pass-through treatment, taxed only on US-source income) and a US C-corporation (a separate taxpayer that files its own return). The S-corporation is simply not on the menu for anyone who is not a US citizen or a US tax resident.

Is an S-corp a type of company or a tax status

It is a tax status, not an entity type. You cannot walk into a Secretary of State office and "form an S-corp." You form an LLC or a corporation under state law, then file IRS Form 2553 to elect S-corporation treatment for federal tax purposes. The underlying entity — its liability shield, its state filings, its ownership records — is unchanged. What changes is how the IRS taxes the profits: an S-corp splits the owner's income into wages (subject to payroll tax) and distributions (not subject to self-employment tax), which is the entire source of the potential saving.

How much profit do you need before an S-corp election is worth it

As a rough rule of thumb, the payroll and administrative overhead of running an S-corp starts to pay off somewhere around $40,000 to $80,000 of net profit, once the business can comfortably pay a reasonable salary and still leave meaningful profit for distributions. Below that, the cost of payroll processing, a separate corporate-style tax return (Form 1120-S), and a bookkeeper often exceeds the self-employment tax saved. The exact breakeven depends on your reasonable salary, your state, and how much you value the administrative simplicity of a plain LLC. Model it on your real numbers before electing.

What is the reasonable salary requirement for an S-corp

An S-corp owner who works in the business must pay themselves "reasonable compensation" as W-2 wages before taking tax-advantaged distributions. The IRS requires this because wages carry payroll tax and distributions do not, so paying an artificially low salary to dodge tax is a known abuse. Courts have repeatedly sided with the IRS — in David E. Watson, P.C. v. United States the Eighth Circuit upheld a large reassessment where an accountant paid himself a token salary. Reasonable means what you would pay an unrelated employee for the same work. Set it too low and you invite reclassification, penalties and interest.

What is the difference between an LLC taxed as an S-corp and a C-corp

An LLC taxed as an S-corp is a pass-through: profit flows to the owner's personal return once, and the S-election only changes how much of that profit escapes self-employment tax. A C-corporation is a separate taxpayer. It pays the 21% federal corporate income tax on its profit, and shareholders then pay tax again on dividends — the classic double taxation. For a US person with an operating business, the S-corp usually wins on total tax. For a non-resident who cannot use an S-corp at all, the C-corp is the entity that raises venture capital, issues stock options and gives a clean single US taxpayer — at the cost of that second layer of tax on distributed profit.

Does electing S-corp status affect my limited liability protection

No. Limited liability comes from the state-law entity — the LLC or corporation — not from the federal tax election. Filing Form 2553 to be taxed as an S-corp changes nothing about the liability shield, the registered agent, the operating agreement, or your state annual report. You still maintain the same corporate formalities and separation between personal and business assets. The tax election and the liability shield are two entirely separate layers: one is federal tax law, the other is state entity law. Electing or revoking S-corp status leaves your protection exactly where it was.

If I am a non-resident, should I choose an LLC or a C-corp

For most non-resident solo founders and freelancers with no US staff or office, a disregarded single-member LLC is the simpler and cheaper structure: pass-through treatment, tax only on US-source income, and an annual Form 5472 disclosure. Choose a US C-corporation when you plan to raise institutional funding, issue equity to a team, retain profits inside the company at the 21% rate, or need the credibility of a Delaware C-corp for US investors. The S-corp is not an option either way. Our C-corp guide walks through when the second layer of tax is worth accepting.

This guide is editorial. We hold affiliate relationships with Doola, ZenBusiness and Bizee, disclosed via our affiliate disclosure. Nothing here is tax or legal advice — see our disclaimer.

Ready to act on this?

Doola — US LLC + EIN + tax filings, built for non-residents. Whether you need a disregarded LLC or a C-corp, Soveraine readers go to the front of the line through our partner link, and you fund independent editorial in the process.

Sources

- 26 U.S. Code § 1361 — S corporation defined (nonresident-alien shareholder bar at (b)(1)(C)): https://www.law.cornell.edu/uscode/text/26/1361

- IRS — About Form 2553, Election by a Small Business Corporation: https://www.irs.gov/forms-pubs/about-form-2553

- IRS — S Corporation Compensation and Medical Insurance Issues (reasonable compensation): https://www.irs.gov/businesses/small-businesses-self-employed/s-corporation-compensation-and-medical-insurance-issues

- IRS — S Corporation Employees, Shareholders and Corporate Officers: https://www.irs.gov/businesses/small-businesses-self-employed/s-corporation-employees-shareholders-and-corporate-officers

- IRS — Self-Employment Tax (Social Security and Medicare Taxes): https://www.irs.gov/businesses/small-businesses-self-employed/self-employment-tax-social-security-and-medicare-taxes

- Social Security Administration — Contribution and Benefit Base (2026 wage base $184,500): https://www.ssa.gov/oact/cola/cbb.html

- IRS — About Form 1120-S, U.S. Income Tax Return for an S Corporation: https://www.irs.gov/forms-pubs/about-form-1120-s

- David E. Watson, P.C. v. United States, 668 F.3d 1008 (8th Cir. 2012): https://www.irs.gov/pub/irs-utl/watson_v_us.pdf