IRS Form 5472 is the information return that turns an otherwise quiet US LLC or corporation into a reporting entity the moment a foreign owner is involved. It is short, it carries a $25,000 minimum penalty, and since 2017 it applies to single-member LLCs that owe no US tax at all. This article covers what the form is, who has to file it, what counts as a reportable transaction, and how the rules land differently depending on whether you hold a US, EU or other passport. It does not cover the full mechanics of US corporate tax, transfer pricing studies, or treaty-based return positions — those are separate questions you should run past a qualified preparer.

Bright!Tax — US expat tax filings (FBAR + FATCA + FEIE specialists)

What IRS Form 5472 is

Form 5472, formally titled Information Return of a 25% Foreign-Owned U.S. Corporation or a Foreign Corporation Engaged in a U.S. Trade or Business, is filed under Internal Revenue Code sections 6038A and 6038C. It is an attachment to a corporate income tax return — usually Form 1120 — not a stand-alone filing.

The form's job is disclosure, not taxation. It tells the IRS three things: who owns the US entity, who its foreign related parties are, and how much money moved between them during the year. The IRS uses that data to police transfer pricing under IRC section 482 and to spot undisclosed foreign ownership of US business structures.

A separate Form 5472 is required for each foreign related party with whom the reporting corporation had reportable transactions. Three foreign related parties means three Forms 5472.

The current revision is dated December 2023, and the instructions were last updated in December 2024.

Who this applies to — by nationality and structure

The rules apply to entities, but the practical consequences depend on the owner's tax residence and citizenship. Read the segment that matches you.

US persons

If you are a US citizen or green-card holder, Form 5472 is unlikely to be your primary reporting concern — but it can still apply. You owe Form 5472 if you control a US corporation that is at least 25% foreign-owned (for example, a US C-corp with a foreign co-founder holding a quarter of the shares), or if you operate a foreign corporation that is engaged in a US trade or business.

What you cannot do is use the form, or the disregarded-LLC structure behind it, to step outside US worldwide taxation. The US taxes its citizens and residents on global income regardless of where the entity sits. If you own a foreign corporation, you are also likely looking at Form 5471, GILTI, Subpart F, and FBAR filings. A US-owned single-member LLC does not file Form 5472 because it is owned by a US person, not a foreign one.

EU freelancers and digital nomads

A common structure: an EU-resident freelancer forms a Wyoming or Delaware single-member LLC, treats it as a flow-through entity, and bills international clients through it. Under Treasury Regulations §1.6038A-1, that LLC is treated as a domestic corporation for Form 5472 purposes only. It must file every year there is a reportable transaction with the foreign owner — and there always is, because funding the LLC is itself reportable.

This is the segment that gets caught most often. The LLC owes no US federal income tax, the owner assumes "no tax = no filing", and the $25,000 penalty arrives by mail. Separately, the income earned through the LLC is taxable in your country of residence under domestic rules — including CFC regimes implemented under ATAD — and may be caught by exit taxes if you move.

Non-US, non-EU readers

If you are tax-resident in a territorial-tax jurisdiction (UAE, Panama, Georgia, Paraguay, Malaysia for foreign-source income, and others), a US disregarded LLC can be a clean billing and banking vehicle for non-US-source service income. The LLC still has to file Form 5472 — that obligation does not vary by the owner's nationality. What varies is the downstream tax treatment in your home jurisdiction.

You should also check whether your country has a CFC regime, even a weak one, and whether local rules treat the LLC as transparent or as a foreign corporation. The answer changes which form, if any, you owe at home.

What counts as a reportable transaction

A reportable transaction is any monetary or non-monetary exchange between the reporting corporation and a foreign related party. The categories are laid out in Parts IV, V and VI of the form:

- Sales and purchases of inventory, tangible property and intangibles

- Rents and royalties paid or received

- Interest paid or received on loans

- Commissions, premiums, and amounts paid for services

- Loans and loan repayments

- Capital contributions from the owner to the entity

- Distributions from the entity to the owner

- Any other amount that affects taxable income, even if reported on the books only

For a foreign-owned single-member LLC, the initial capital contribution — the money you wire in to fund the bank account — is reportable. So is every distribution you take. So is paying yourself for services rendered through the entity. In practice, this means almost every active LLC has reportable transactions in every year of its life.

Amounts go on the form in US dollars at the spot rate on the transaction date. The instructions permit a reasonable approximation if exact daily rates are impractical, but the rate used must be consistent and documented.

How filing works in practice

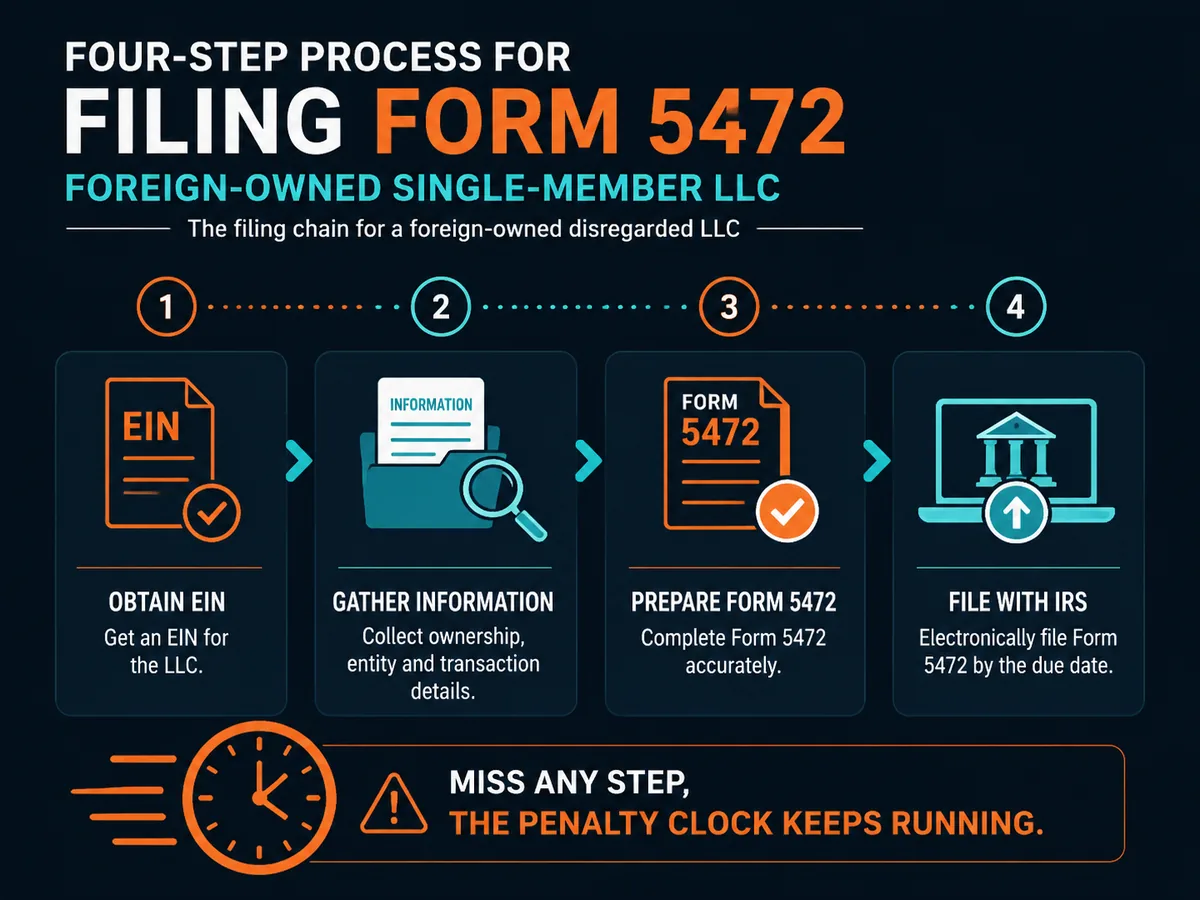

For a foreign-owned single-member LLC, the mechanics are:

- Obtain an EIN from the IRS using Form SS-4. As a foreign owner without an SSN or ITIN, you file by fax or mail and write "Foreign" on the responsible-party SSN line.

- File a pro forma Form 1120 — name, address, EIN, tax year. The income and deduction lines are left blank. Write "Foreign-owned U.S. DE" across the top per the Form 1120 instructions.

- Attach Form 5472, completed for each foreign related party.

- Mail or fax the package to the address in the Form 5472 instructions. E-filing is available for corporations through authorised software but is not practical for most disregarded-entity filers.

The deadline is the 15th day of the fourth month after year-end — April 15 for a calendar-year filer. A six-month extension is available via Form 7004, filed by the original due date.

Realistic costs, fees and timeline

Numbers below are typical 2025 market rates. They are illustrative — confirm with the provider before engaging.

| Item | Typical cost (USD) | Notes |

|---|---|---|

| EIN application (DIY by fax) | $0 | 4–8 weeks turnaround for foreign applicants |

| EIN via third-party | $150 – $300 | 1–3 weeks; service files SS-4 on your behalf |

| Form 5472 + pro forma 1120 (DIY) | $0 | High error rate; not recommended |

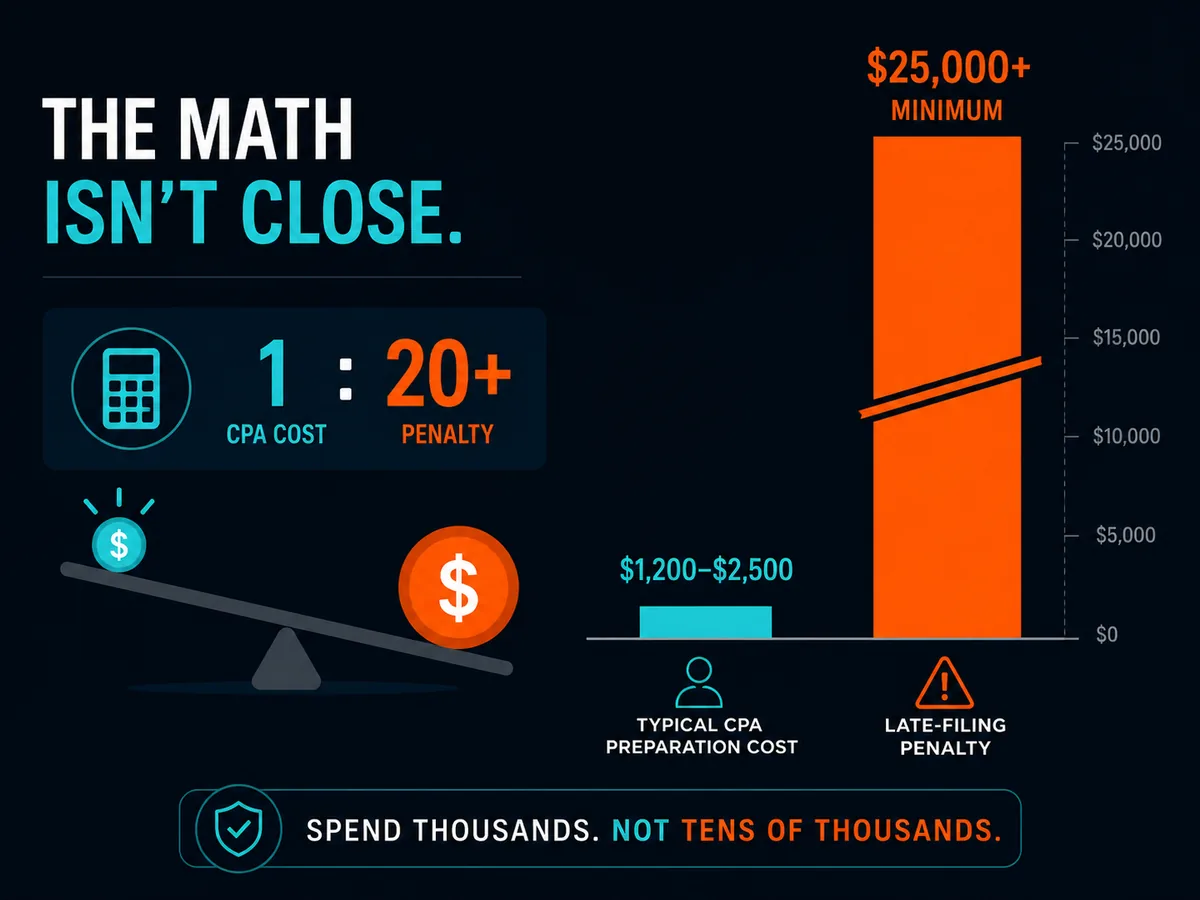

| Form 5472 + 1120 prep by CPA | $400 – $1,200 | Single foreign related party, single-member LLC |

| Complex multi-party 5472 prep | $1,500 – $5,000+ | Multiple related parties, transfer pricing |

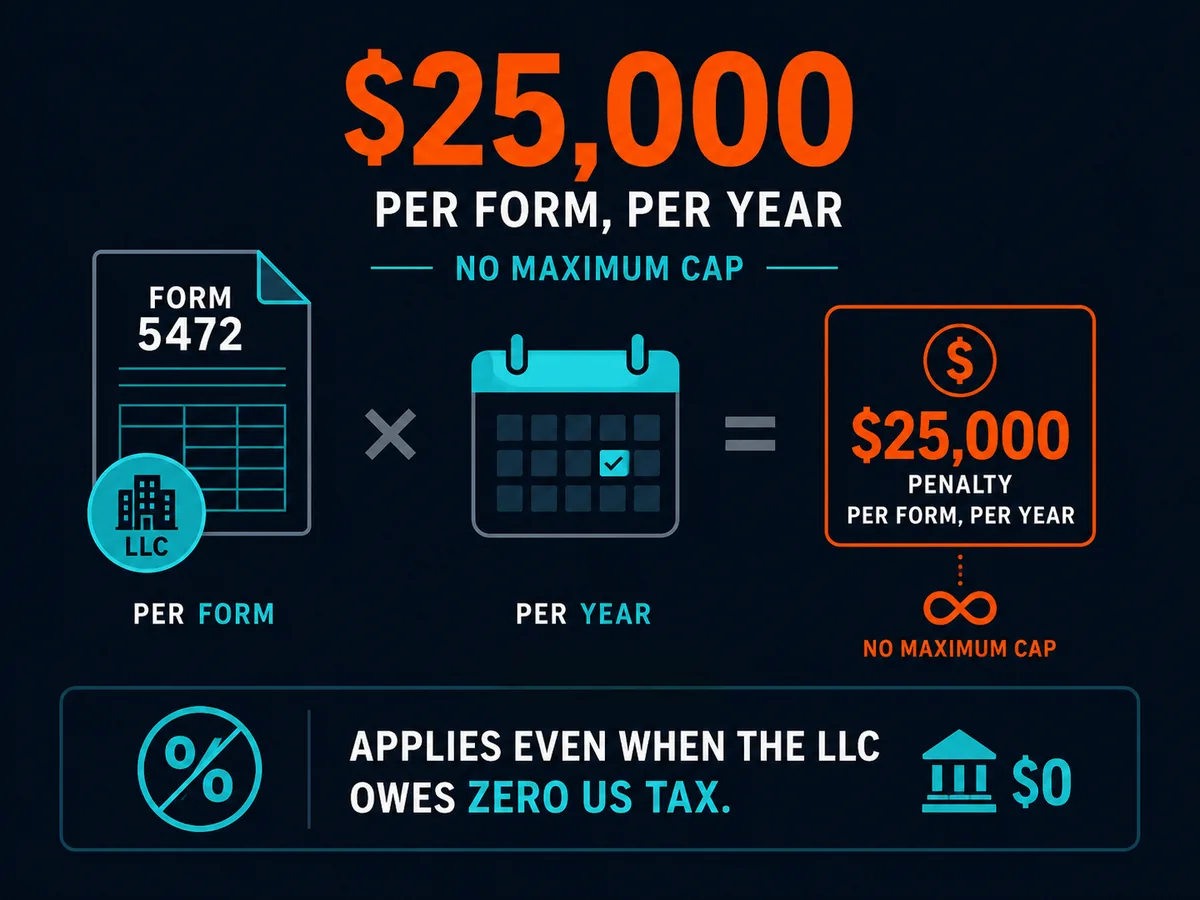

| Late-filing penalty | $25,000 minimum | Per form, per year; +$25,000 per 30 days after IRS notice |

| Streamlined or DIIRSP submission | $2,000 – $7,500 | Professional fees; penalty waiver not guaranteed |

A first-year filing typically runs: 4–8 weeks for the EIN, 2–4 weeks for documentation gathering, 1–2 weeks for preparation, then the filing itself. Plan the timeline backwards from 15 April.

We do not recommend specific tax-preparation services in this article because the right preparer depends on your residence country, the complexity of your transactions, and whether you need transfer-pricing documentation. If you want a starting point, the AICPA member directory and the IRS Directory of Federal Tax Return Preparers are both free, non-affiliate resources. See our affiliate disclosure for our policy on paid recommendations.

Common mistakes and how to avoid them

Assuming no tax means no filing. This is the single most common error among foreign-owned LLC owners. The LLC files because of the ownership structure, not because of income. Mark April 15 in your calendar from the day you form the entity.

Missing the initial capital contribution. First-year filers often report the year's operating transactions and forget the wire that funded the bank account on day one. That is itself a reportable transaction and goes on Part IV or V depending on how it is characterised.

Using the wrong exchange rate methodology. Mixing average annual rates for some transactions and spot rates for others without documentation invites questions. Pick one approach, document it, and apply it consistently.

Filing Form 5472 without the pro forma 1120. The 5472 is an attachment. A standalone 5472 mailed to the IRS will not be processed and the penalty clock keeps running.

Confusing related-party loans with capital contributions. A loan from the foreign owner to the LLC must have documentation, an interest rate that satisfies the applicable federal rates, and reporting on the interest paid. Without that, the IRS can recharacterise it as a contribution — changing the basis position.

Treating the LLC as anonymous. Form 5472 names the direct and ultimate beneficial owner. The Corporate Transparency Act layered separate beneficial-ownership reporting on top until 2025 enforcement changes. Anonymity at the federal level is not what these structures provide — bank-level privacy at most, and only relative to public registries.

When to consult a qualified professional

Form 5472 is not a DIY project once any of the following are true:

- You have more than one foreign related party

- The LLC has substantial intercompany transactions or charges management fees

- You took distributions or contributions during a year you also changed tax residence

- You are a US person with a foreign corporation that triggers 5472 alongside 5471, GILTI or Subpart F

- You missed prior-year filings and are weighing the Delinquent International Information Return Submission Procedures, Streamlined Filing Compliance Procedures, or Voluntary Disclosure Practice

For the simplest case — a non-US resident with a single-member Wyoming LLC, one bank account and no employees — a competent international tax CPA can prepare the package for under $1,000. The math against a $25,000 penalty is straightforward.

You should also retain advice in your country of tax residence, not only in the US. The US filing tells you nothing about how your home country taxes the LLC's profits, applies CFC rules, or treats distributions. See our editorial policy and disclaimer on the limits of what general editorial content can do for your specific situation.

FAQ

What is the purpose of Form 5472?

Form 5472 is an information return — not a tax return — that the IRS uses to monitor transactions between a US entity and its foreign related parties. It exists under Internal Revenue Code sections 6038A and 6038C. The form tells the IRS who owns the US entity, who it transacts with abroad, and how much money moves across the border. It is the principal reporting tool the IRS has against transfer-pricing abuse and undisclosed foreign ownership of US business structures, including single-member LLCs treated as disregarded entities.

What happens if I don't file Form 5472?

The penalty is $25,000 per form, per year, applied automatically and assessed without a hearing. If the IRS sends a notice of failure and you do not file within 90 days, an additional $25,000 accrues for every 30-day period of continued non-compliance. There is no maximum cap. Wilful failure can also trigger criminal liability under IRC section 7203. The penalty applies even when the entity owes no US tax and even when the only reportable transaction was the capital contribution that formed it.

Do I need to report Form 5498 on my tax return?

No, and the two forms are unrelated. Form 5498 is an IRA contribution information return that your IRA custodian files with the IRS — you keep it for your records but do not attach it to Form 1040. It surfaces in search results next to Form 5472 because of the numeric similarity, not because the rules overlap. If you are a foreign-owned US LLC owner asking about 5498, you are almost certainly looking for 5472.

Does an LLC need to file Form 5472?

Yes, if it is foreign-owned and a disregarded entity for US tax purposes. Since the 2017 regulations under Treas. Reg. §1.6038A-1, a single-member LLC owned by a non-US person is treated as a domestic corporation solely for Form 5472 reporting. It must obtain an EIN, file a pro forma Form 1120 with Form 5472 attached, and report every reportable transaction — including the initial capital contribution and any owner distributions. Multi-member LLCs taxed as partnerships file Form 8865 instead.

What counts as a reportable transaction?

Anything that moves money or value between the US entity and a foreign related party. That includes sales, rents, royalties, interest, commissions, loans, loan repayments, capital contributions and distributions. For a foreign-owned disregarded LLC, even a $100 transfer from the owner's personal account to fund the LLC's bank account is reportable. The instructions to Form 5472 list the categories on Parts IV through VI. Amounts are reported in US dollars at the spot rate on the transaction date.

Does the IRS have a one-time forgiveness program?

There is no formal one-time forgiveness, but two routes exist. First-Time Abate (FTA) administrative relief can waive penalties if you have a clean compliance record for the prior three years — but the IRS has historically refused FTA for Form 5472 penalties, treating them as event-based rather than failure-to-file penalties. The Delinquent International Information Return Submission Procedures allow late filing with a reasonable cause statement. For wilful non-compliance, the Streamlined Filing Compliance Procedures or a Voluntary Disclosure Practice submission are the recognised paths. None are automatic.

Ready to act on this?

Bright!Tax — US expat tax filings (FBAR + FATCA + FEIE specialists). Soveraine readers go to the front of the line through our partner link, and you fund independent editorial in the process.

Sources

- IRS — About Form 5472: https://www.irs.gov/forms-pubs/about-form-5472

- IRS — Form 5472 (Rev. December 2023) PDF: https://www.irs.gov/pub/irs-pdf/f5472.pdf

- IRS — Instructions for Form 5472 (12/2024): https://www.irs.gov/instructions/i5472

- Internal Revenue Code §6038A (Cornell LII): https://www.law.cornell.edu/uscode/text/26/6038A

- Treasury Regulations §1.6038A-1 (eCFR): https://www.ecfr.gov/current/title-26/chapter-I/subchapter-A/part-1/subject-group-ECFRfc6e96fff1d04f7/section-1.6038A-1

- IRC §951A (GILTI, Cornell LII): https://www.law.cornell.edu/uscode/text/26/951A

- IRS — About Form 5471: https://www.irs.gov/forms-pubs/about-form-5471

- IRS — Instructions for Form 1120: https://www.irs.gov/instructions/i1120

- IRS — Applicable Federal Rates: https://www.irs.gov/applicable-federal-rates

- FinCEN — Report of Foreign Bank and Financial Accounts (FBAR): https://www.fincen.gov/report-foreign-bank-and-financial-accounts

- FinCEN — Beneficial Ownership Information: https://www.fincen.gov/boi

- European Commission — Anti-Tax Avoidance Directive: https://taxation-customs.ec.europa.eu/anti-tax-avoidance-directive_en

- IRS — Directory of Federal Tax Return Preparers: https://irs.treasury.gov/rpo/rpo.jsf