An Individual Taxpayer Identification Number is a nine-digit number the IRS issues to people who must appear on a US federal tax return but cannot get a Social Security number. It is a personal identifier, not a business one — and that single distinction is where most non-residents go wrong. A large share of foreign founders who search for how to get an ITIN do not actually need one: they have confused the personal ITIN with the entity-level EIN their LLC uses. This guide draws the line precisely. It covers who genuinely needs an ITIN, why owning a US LLC usually is not one of those reasons, Form W-7 line by line, the three ways to apply, the documents the IRS will and will not accept, the tax-return-attachment rule and its five exceptions, real 2026 timelines, and the expiration and renewal rules. It is written for US persons, EU residents, and readers outside both blocs.

Doola — US LLC, EIN and tax filings handled for non-residents

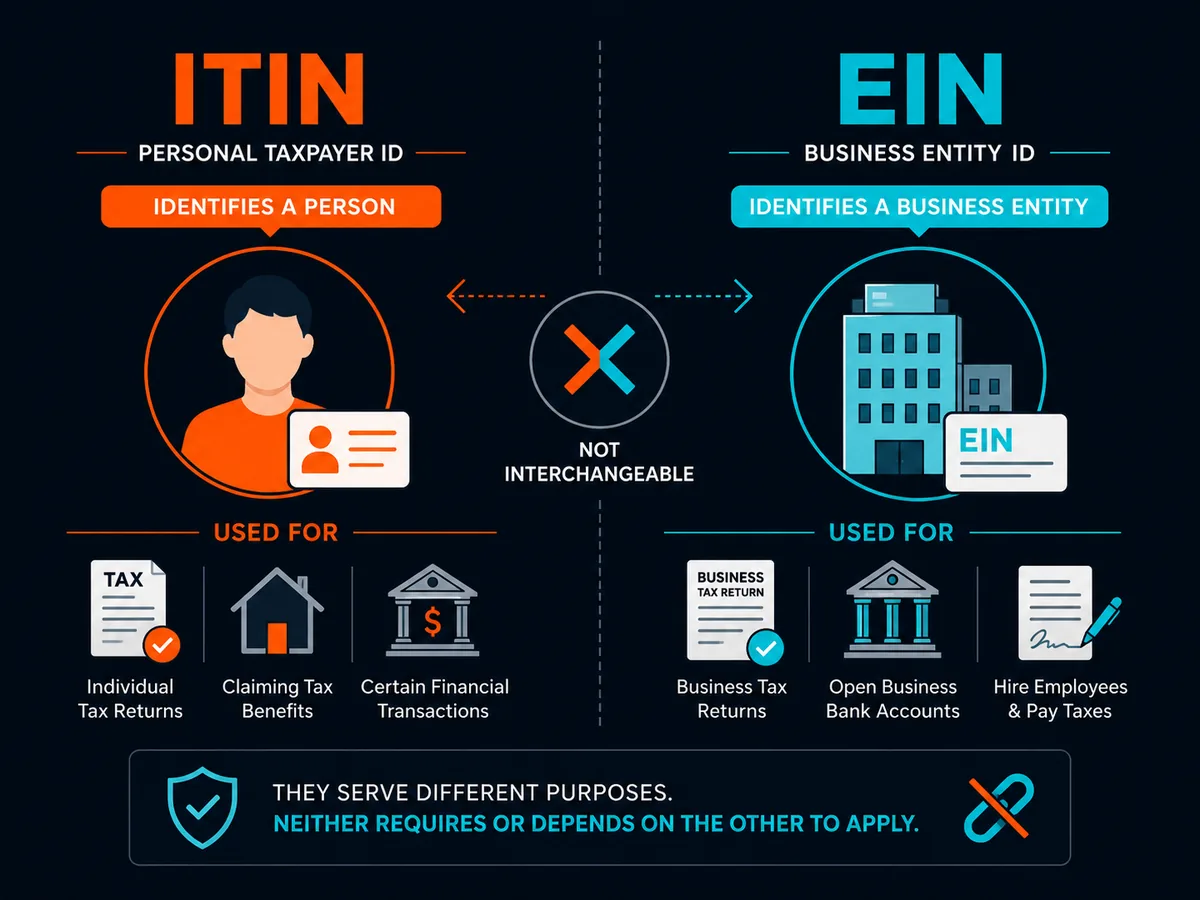

What an ITIN is — and what it is not

An ITIN is a tax processing number. The IRS issues it, under its authority to require taxpayer identifying numbers, to individuals who are "required for U.S. federal tax purposes to have a U.S. taxpayer identification number but who do not have and are not eligible to get a Social Security number." It always begins with the digit 9. The application form is IRS Form W-7, and the number does exactly one thing: it lets a specific human being be identified on a US federal tax return or an IRS information document.

It is worth being blunt about the limits. An ITIN is not work authorisation. It does not entitle you to Social Security benefits or the Earned Income Tax Credit. It is not proof of legal immigration status, and it is not a substitute for an SSN in any non-tax context — you cannot use it to open a personal bank account or build US credit the way an SSN allows. It exists solely so the IRS can process a filing that has to name you. When the tax reason disappears and the number goes unused, it eventually expires.

Most importantly for this audience, an ITIN is not a business identifier. The number your LLC or corporation uses to file returns, open a business bank account and issue payroll is the Employer Identification Number — a separate nine-digit code applied for on a different form, through a different IRS unit. Confusing the two is the single most common and most expensive mistake foreign founders make, and it is worth its own section.

ITIN vs EIN — the distinction that saves you weeks

Here is the scenario we see constantly. A founder in Lisbon or Lagos forms a US LLC, reads that they will need a "US tax number," and applies for an ITIN. Weeks later they are still waiting, their bank application is stalled, and they have not even started the thing they actually needed. The LLC's tax number is an EIN, and it can be obtained in a single phone call or fax while the ITIN sits in a 7-to-11-week queue it never needed to be in.

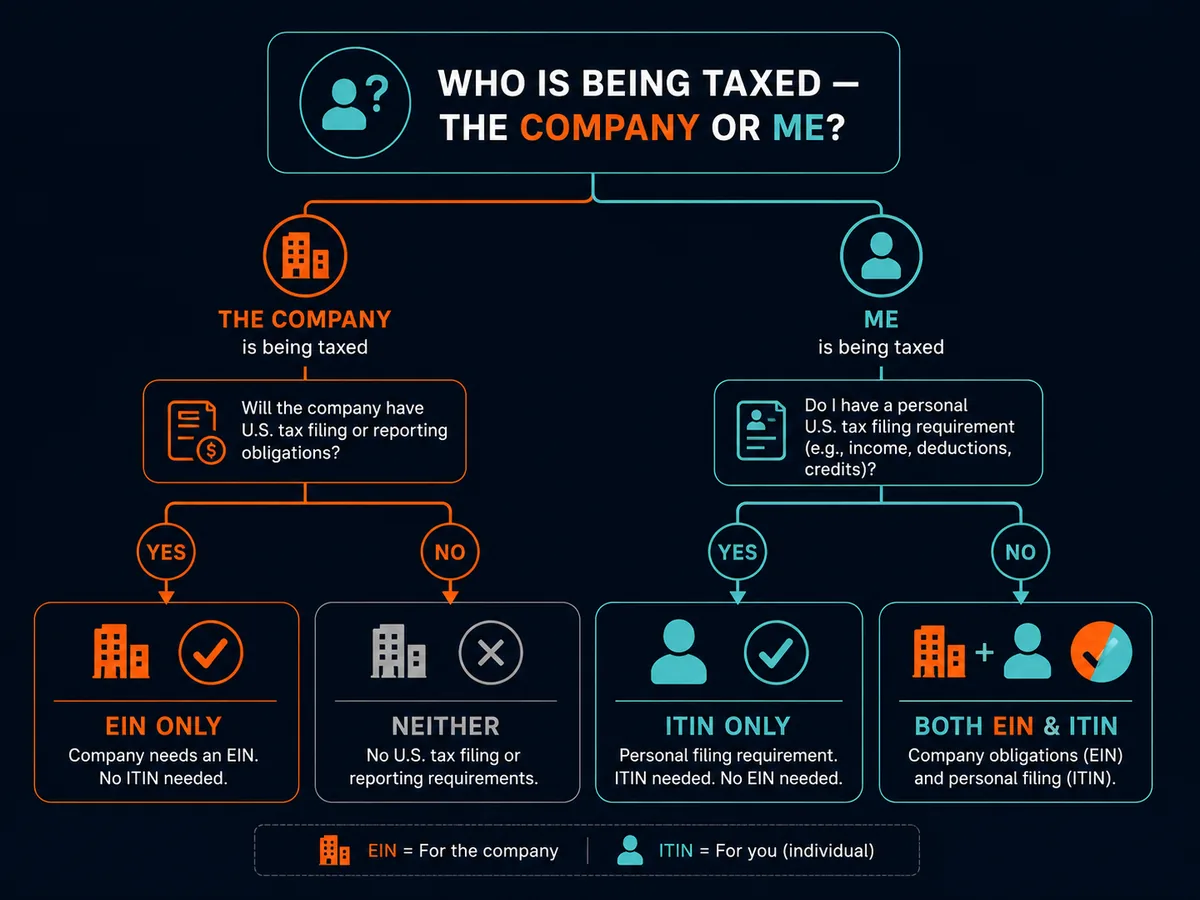

The clean way to hold it in your head: the EIN belongs to the company, the ITIN belongs to you as a person. Your LLC opens its Mercury or Relay account with the EIN. Your LLC files its annual Form 5472 and pro-forma 1120 with the EIN. Stripe onboards the LLC with the EIN. None of that requires an ITIN, because none of it requires you personally to be a line on a US return. The full mechanics of getting the entity number are in our EIN for non-US residents guide — read that first if the company number is what you actually need.

You reach for an ITIN only when the tax event lands on you rather than the company. That happens when you personally have US-source income taxed on a Form 1040-NR, when you claim a treaty benefit in your own name, when you sell US real property and FIRPTA withholding applies to you, or when someone else's US return has to name you as a spouse or dependent. For the typical foreign-owned single-member LLC with no US-effectively-connected income, that day may never come — which is exactly why the single-member LLC non-resident path so often needs an EIN and no ITIN at all.

Who actually needs an ITIN

Form W-7 asks you to state your reason, and the boxes double as the definitive list of who qualifies. If you do not fit one of them, you do not get an ITIN.

- Box a — Nonresident alien claiming a tax treaty benefit. You are invoking a provision of a US income tax treaty, and the treaty claim requires you to be identified. Understanding whether you even are a nonresident alien is worth settling first — see what is a nonresident alien.

- Box b — Nonresident alien filing a US federal tax return. You have a filing obligation on a Form 1040-NR, typically because you earned income effectively connected with a US trade or business, and you have no SSN.

- Box c — US resident alien filing a return. You meet the substantial presence test and must file a Form 1040 but cannot get an SSN.

- Boxes d and e — Dependent or spouse of a US citizen or resident alien being claimed on that person's return.

- Boxes f and g — Nonresident alien student, professor or researcher, or the dependent or spouse of a nonresident visa holder.

- Box h — Other, used for the exception categories where a return is not attached, such as third-party withholding on passive income.

For the founder audience, the reasons that matter most are Box a (treaty benefit), Box b (a 1040-NR because you have effectively connected income), and the FIRPTA disposition case, which falls under Exception 4 below. If you hold US real property through a structure and sell it, the buyer must withhold under FIRPTA and you will need an ITIN to file for any refund of over-withheld tax. That single event puts more non-residents into the ITIN system than almost anything else. Choosing a corporate structure changes the analysis too — the trade-offs are covered in our US C-corp for non-residents piece and, for the entity's own reporting, the pillar IRS Form 5472 guide.

Form W-7 line by line

Form W-7 is a single page, but a handful of fields cause the rejections that add months. The notes below cover the lines that consistently trip up non-residents.

Reason for applying (top of form). Tick exactly one box, a through h, matching the list above. If you tick box a (treaty) or h (exception), you also complete the treaty country and article number, or the exception reference, on the same line. A mismatch between the box you tick and the return or exception evidence you attach is the most common cause of a CP566 "need more information" notice.

Line 1a — Legal name. Your full name exactly as it appears on your passport or the identity document you submit. Not a nickname, not an anglicised spelling.

Line 1b — Name at birth, if different from 1a.

Line 2 — Applicant's mailing address. Where the IRS sends the CP565 approval notice and returns your documents. Use an address where post reliably reaches you. This is where a US mailing address can help, though a reliable home-country address is acceptable.

Line 3 — Foreign (non-US) address. Your actual residential address in your home country. Do not leave this blank if you live abroad; a PO box alone is not acceptable here.

Lines 4 and 5 — Date and place of birth. Use the country name as it appears on your passport.

Line 6a — Country of citizenship. Spell the country in full.

Line 6b — Foreign tax ID number, if your country issues one. Enter your home-country taxpayer number.

Line 6c — US visa type and number, only if you hold one. Most non-resident founders leave this blank.

Line 6d — Identification documents submitted. Tick which documents you are enclosing and enter their numbers and expiry. If you submit a passport, this is the only line that needs a document — more on that below.

Line 6e/6f — Prior ITIN or IRSN, if the IRS has ever issued you one. If you are renewing, this is where the existing number goes.

Signature block. The form is signed under penalty of perjury. A delegate (a parent for a minor, or an appointed agent) can sign in limited circumstances, but an adult applicant signs personally. An unsigned W-7 is rejected outright.

The tax-return rule and its five exceptions

The default, and the point most guides skip, is that Form W-7 does not travel alone. Under the Form W-7 instructions, you normally attach a valid, completed federal tax return to the W-7, and the IRS processes the two together — the ITIN is assigned and then immediately used to process that return. You leave the SSN area blank for each ITIN applicant on the return. If you send a W-7 with no return and no valid exception, it is rejected.

The IRS publishes five exceptions where a return is not attached because the ITIN is needed before any return is due. For non-residents these are the routes that matter:

- Exception 1 — Third-party withholding on passive income. Bank or brokerage interest, partnership distributions of effectively connected income, or pension and annuity payments where a withholding agent needs your ITIN to report and withhold correctly.

- Exception 2 — Wages, scholarships or gambling income claiming treaty benefits. Certain compensation or scholarship income where a treaty reduces or eliminates withholding.

- Exception 3 — Mortgage interest subject to third-party reporting. Where a lender must report mortgage interest paid by you.

- Exception 4 — Dispositions of US real property interests (FIRPTA). A foreign person selling US real estate, where the buyer withholds tax under FIRPTA and the seller needs an ITIN to reconcile it. This is the big one for property-owning non-residents.

- Exception 5 — Certain foreign corporate representatives meeting IRS e-filing requirements.

If you qualify for an exception, you attach the supporting evidence the instructions specify for that category — a signed withholding statement, a treaty letter, a closing statement for a property sale — instead of a tax return. If you do not, you wait until you have a return to file and submit them together.

The three ways to apply

Route 1 — Mail original documents to Austin

You send the signed Form W-7, your federal tax return (or exception evidence), and your original identity documents — or copies certified by the issuing agency — to the IRS ITIN Operation. Ordinary notarised copies are not accepted; the IRS requires the original or an issuing-agency certified copy. The mailing address is:

Internal Revenue Service Austin Service Center, ITIN Operation P.O. Box 149342 Austin, TX 78714-9342

For couriers that will not deliver to a PO box, the private-delivery address is Internal Revenue Service, ITIN Operation, Mail Stop 6090-AUSC, 3651 S. Interregional Highway 35, Austin, TX 78741. The IRS states it returns your documents within 60 days. For a non-resident, that means your passport could be inside the US postal and IRS system for two months. If it is your only travel document, that is rarely acceptable — which is the whole argument for the next route.

Route 2 — Certifying Acceptance Agent (recommended for non-residents)

A Certifying Acceptance Agent is a person or firm the IRS has authorised to verify your identity documents and certify them to the IRS on your behalf. CAAs operate both inside the US and internationally, and this is the route most non-residents should take. The CAA reviews your passport in person (or via a supervised video process where permitted), certifies it, completes the W-7 with you, and submits the package — so your original passport never leaves your possession and never goes in the post. CAAs charge a fee, but for anyone applying from abroad the fee buys real protection against losing an irreplaceable document. You can find authorised agents through the IRS acceptance agent directory. A tax-focused provider such as Bright!Tax can also handle the surrounding US return, since the W-7 usually has to be attached to one.

Route 3 — IRS Taxpayer Assistance Center

A Taxpayer Assistance Center (TAC) that offers ITIN document authentication can verify most of your supporting documents in person at no charge, so you keep your originals. The catch is geography and scheduling: TACs are in the US only, they operate by appointment, and appointments can be weeks out. For a non-resident who is not already travelling to the US, a TAC is impractical. For someone physically in the US on a visit, it is a free alternative to a CAA.

Documents the IRS will accept

The IRS lists thirteen acceptable documents to prove identity and foreign status. At least one must carry your photograph unless the applicant is a dependent under 14. The decisive point for adults is the passport rule: a single valid passport is a standalone document — if you submit it, you need nothing else. Every other route requires a combination of two documents, one to prove identity and one to prove foreign status.

| Document | Proves identity | Proves foreign status | Standalone? |

|---|---|---|---|

| Passport | Yes | Yes | Yes — the only standalone document |

| National identification card (with photo, name, address, DOB, expiry) | Yes | Yes | No — pair with another |

| US Citizenship & Immigration Services (USCIS) photo ID | Yes | Yes | No |

| US or foreign driver's licence | Yes | No | No |

| Foreign voter registration card | Yes | Yes | No |

| Foreign military identification card | Yes | Yes | No |

| US state identification card | Yes | No | No |

| Visa issued by the US Department of State | Yes | Yes | No |

| Civil birth certificate (required for dependents under 18) | Yes | Yes | No |

| Medical records (dependents under 6 only) | Yes | Yes | No |

| School records (dependents under 14, or under 24 if a student) | Yes | Yes | No |

The practical takeaway for a non-resident founder is simple: use your passport, and the document question disappears. This is also why the CAA route is so clean — the one document that matters is exactly the one you least want to mail, and a CAA lets you keep it.

Timelines in 2026

The IRS asks you to allow about 7 weeks to be notified of your ITIN application status. During the peak filing window — 15 January to 30 April — or if you apply from outside the United States, expect 9 to 11 weeks. These are notification timelines that assume a complete, signed, error-free package. The most common cause of delay is not IRS backlog but applicant error: an unsigned W-7, a wrong reason box, a photocopy where a certified document was required, or a return with a mismatch. Any of those produces a CP566 notice requesting more information and effectively restarts the clock.

Three outcomes are possible. CP565 is the approval notice carrying your assigned ITIN. CP566 asks for missing information or documents. CP567 is a rejection. If you apply through a CAA outside peak season with a passport, you are firmly at the shorter end of the range; if you mail original documents from abroad in March, you are at the longer end and your passport is gone for weeks on top of it.

Expiration and renewal

An ITIN is not permanent. Under the rule the IRS applies, if your ITIN is not included on at least one US federal tax return for three consecutive tax years, it expires on 31 December of that third year. An ITIN used on any return within a rolling three-year window stays active, and a single filing resets the counter to zero. So an ITIN issued for a one-off FIRPTA sale, and then never used again, will quietly lapse.

Renewal uses the same Form W-7 — you tick the renewal option and enter the existing number. You can renew before you next file if you know a filing is coming, which spares you the delay of renewing mid-season. Filing a return with an expired ITIN is not fatal, but the IRS warns it causes processing delays and can disallow certain credits until the renewal is processed, which can shrink a refund. The discipline is to check your ITIN's status before each filing season and renew ahead of need rather than discovering the lapse when your return stalls.

When to use a professional

The W-7 itself is a one-page form most people can complete. Where a professional earns their fee is the surrounding judgement: confirming you actually need an ITIN rather than just an EIN, choosing the correct reason box and exception, preparing the 1040-NR or treaty statement the W-7 must attach to, and — for anyone abroad — certifying your passport so it never leaves your hands. A Certifying Acceptance Agent covers the document problem; a cross-border tax firm such as Bright!Tax covers the return that goes with it. For founders whose real need is the company number and its annual filings, a formation-and-compliance provider like Doola handles the EIN and the Form 5472 package, leaving the ITIN question to be assessed only if and when a personal filing event arises.

The Soveraine view: most non-residents who think they need an ITIN need an EIN instead. Settle the entity number first, confirm whether any personal US filing genuinely lands on you, and only then reach for Form W-7 — and when you do, use a CAA so your passport stays in your pocket.

FAQ

Do I need an ITIN if I own a US LLC

Usually not. Owning a US LLC does not by itself create a personal US filing obligation, and the LLC's own federal tax ID is an EIN, not an ITIN. You need an ITIN only when you personally must appear on a US federal tax return and cannot get an SSN — for example, you have effectively connected income taxed on a Form 1040-NR, you are claiming a tax treaty benefit, you are disposing of US real property under FIRPTA, or you are being claimed on someone else's return. A foreign-owned single-member LLC with no US-source income files Form 5472 with a pro-forma 1120 using its EIN, and the owner often needs no ITIN at all. Get the EIN first; assess the ITIN separately.

What is the difference between an ITIN and an EIN

An ITIN is a personal taxpayer identification number for an individual who must be on a US federal tax return but is ineligible for a Social Security number. An EIN is an entity identifier for a business — the number your LLC or corporation uses to file returns and open bank accounts. The two are not interchangeable and there is no dependency between them: you apply for an EIN on Form SS-4 and for an ITIN on Form W-7, through different IRS units. Many foreign LLC owners wrongly believe they need an ITIN to run the company. They need an EIN for the entity; they need an ITIN only if they personally trigger a US filing requirement.

Can I get an ITIN without filing a tax return

Only if you qualify for one of the five published exceptions. The default rule under the Form W-7 instructions is that you must attach a valid, completed federal tax return to your W-7 — the ITIN and the return are processed together. The exceptions cover situations where a return is not yet due but an ITIN is still needed: third-party withholding on passive income such as bank interest or partnership distributions (Exception 1), certain wages or scholarships claiming treaty benefits (Exception 2), reportable mortgage interest (Exception 3), dispositions of US real property under FIRPTA (Exception 4), and certain foreign corporate representatives (Exception 5). If none apply, you file W-7 with your return.

How long does it take to get an ITIN in 2026

The IRS asks you to allow about 7 weeks to be notified of your ITIN status. During peak filing season — 15 January to 30 April — or if you apply from outside the United States, expect 9 to 11 weeks. These are notification timelines, not just mailing times, and they assume a complete, error-free application. Missing documents or an unsigned Form W-7 trigger a CP566 notice asking for more information, which restarts much of the clock. Applying outside peak season through a Certifying Acceptance Agent is the most reliable way to stay at the shorter end of the range.

Do I have to mail my passport to the IRS

Not if you use a Certifying Acceptance Agent or an IRS Taxpayer Assistance Center. If you apply by mail on your own, you must send either your original passport or a copy certified by the issuing agency — the IRS does not accept ordinary notarised copies — and it can be gone for up to 60 days. For a non-resident, mailing an original passport abroad is a serious risk. A Certifying Acceptance Agent (CAA) can verify your passport in person and certify it to the IRS, so the original never leaves your hands. That single benefit is why most non-residents use a CAA rather than the mail route.

Does an ITIN expire

Yes. If your ITIN is not included on at least one US federal tax return for three consecutive tax years, it expires on 31 December of that third year. An ITIN used on any return within a three-year window stays active, and a single filing resets the clock. Expired ITINs are not cancelled — you renew them on the same Form W-7, ticking the renewal box, and you can renew before filing if you know you will need it. Filing a return with an expired ITIN causes processing delays and can disallow certain credits until the renewal clears, so check the status before each filing season.

Can I apply for an ITIN before I have a tax reason to

Generally no. The ITIN is issued to support a specific US federal tax purpose, and the W-7 asks you to state that reason and, in most cases, attach the return that proves it. You cannot obtain an ITIN speculatively 'to have on file' the way you might get an EIN in advance. The practical sequence for a non-resident is: form the entity and get its EIN first, then apply for an ITIN only when a personal filing event actually arises — treaty claim, effectively connected income, a FIRPTA sale, or an obligation to appear on a US return. Applying without a qualifying reason results in rejection.

This guide is editorial. We hold affiliate relationships with Doola, Bright!Tax, Mercury and Relay, disclosed via our affiliate disclosure. Nothing here is tax or legal advice — see our disclaimer.

Sort the company number first

Most non-residents who search for an ITIN actually need an EIN for their entity. Doola sets up your US LLC, files for the EIN, and handles the annual Form 5472 package — so you only chase an ITIN if a personal filing event genuinely arises.

Sources

- IRS — About Form W-7, Application for IRS Individual Taxpayer Identification Number: https://www.irs.gov/forms-pubs/about-form-w-7

- IRS — How do I apply for an ITIN?: https://www.irs.gov/individuals/how-do-i-apply-for-an-itin

- IRS — Instructions for Form W-7: https://www.irs.gov/instructions/iw7

- IRS — Individual Taxpayer Identification Number (ITIN): https://www.irs.gov/individuals/individual-taxpayer-identification-number

- IRS — How to renew an ITIN: https://www.irs.gov/tin/itin/how-to-renew-an-itin

- IRS — Acceptance Agent Program: https://www.irs.gov/individuals/international-taxpayers/acceptance-agents

- IRS — Taxpayer Identification Numbers (TIN): https://www.irs.gov/individuals/international-taxpayers/taxpayer-identification-numbers-tin

- IRS — Reporting and paying tax on U.S. real property interests (FIRPTA): https://www.irs.gov/individuals/international-taxpayers/firpta-withholding