The Foreign Tax Credit (FTC) is the most powerful — and most under-used — relief in the US expat tax code. Most US persons abroad reach for the Foreign Earned Income Exclusion first because it looks simpler: one form, one cap, no baskets. But for anyone in a high-tax country, holding passive investments, drawing a pension or earning above the FEIE cap, the FTC is structurally better. There is no dollar limit on foreign tax you can credit — only a per-basket §904 ceiling. This guide covers what the credit is, how the four post-TCJA baskets work, how the §904 limit is computed, the FEIE interaction, and the traps that cost real money.

Bright!Tax — US expat tax filings (FBAR + FATCA + FEIE specialists)

What the Foreign Tax Credit actually is

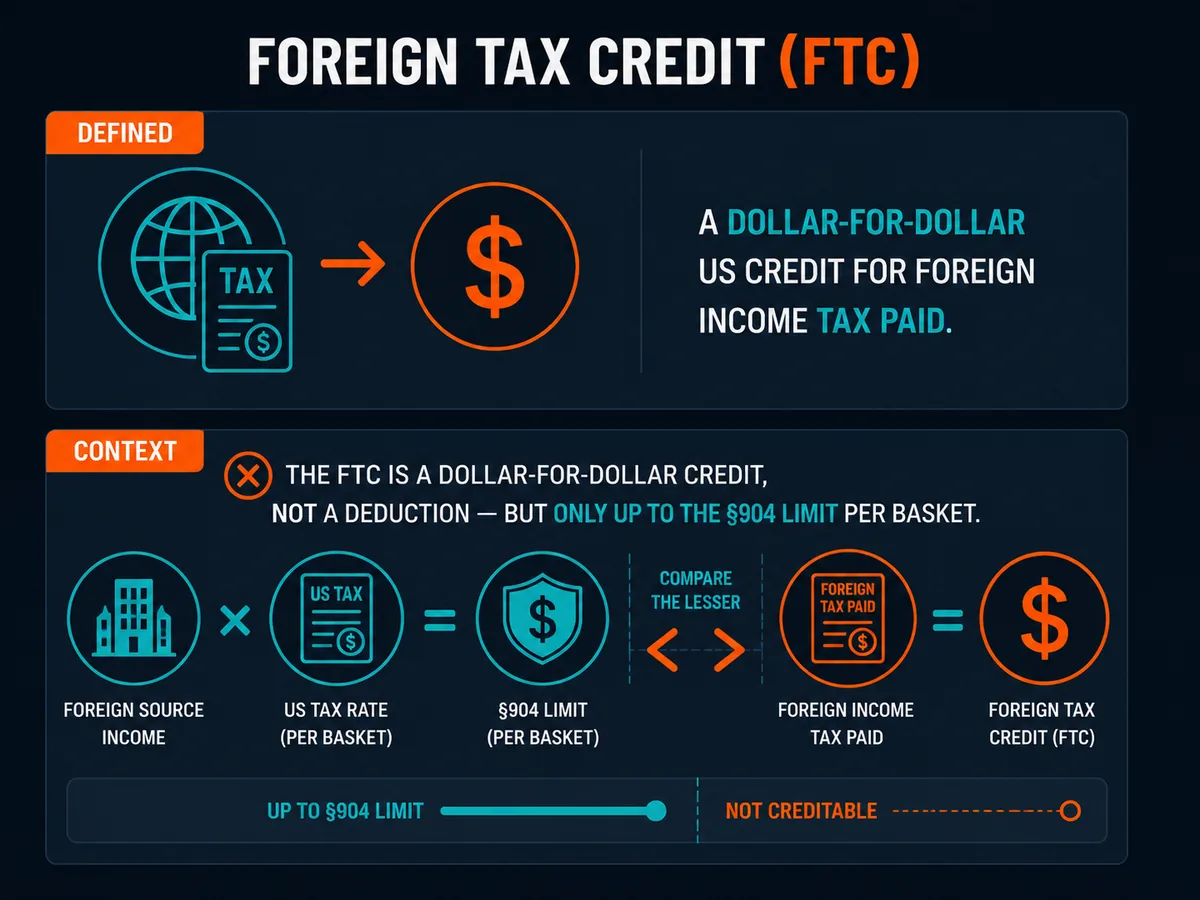

The Foreign Tax Credit is a non-refundable, dollar-for-dollar credit against US federal income tax for income tax paid or accrued to a foreign country or US possession. The statutory authority is Internal Revenue Code §901, which allows a credit for "income, war profits, and excess profits taxes paid or accrued during the taxable year to any foreign country or to any possession of the United States," subject to the limitation in §904.

It is computed on Form 1116 by individuals and Form 1118 by C corporations.

Publication 514 sets four requirements: the tax must be imposed on you, paid or accrued, the legal and actual foreign liability, and an income tax — or a tax in lieu of one under Treas. Reg. §1.903-1. Penalties, interest, fines, and taxes used to subsidise the taxpayer are not creditable.

A key choice sits inside §901: a taxpayer can either credit foreign tax dollar-for-dollar against US tax, or deduct it as an itemised deduction. The election is annual but binding — per Pub 514, "If you choose to take a credit for any qualified foreign taxes in a year, you must take the credit for all qualified foreign taxes paid or accrued in that year. You cannot deduct any of them." The credit is materially better for almost every taxpayer.

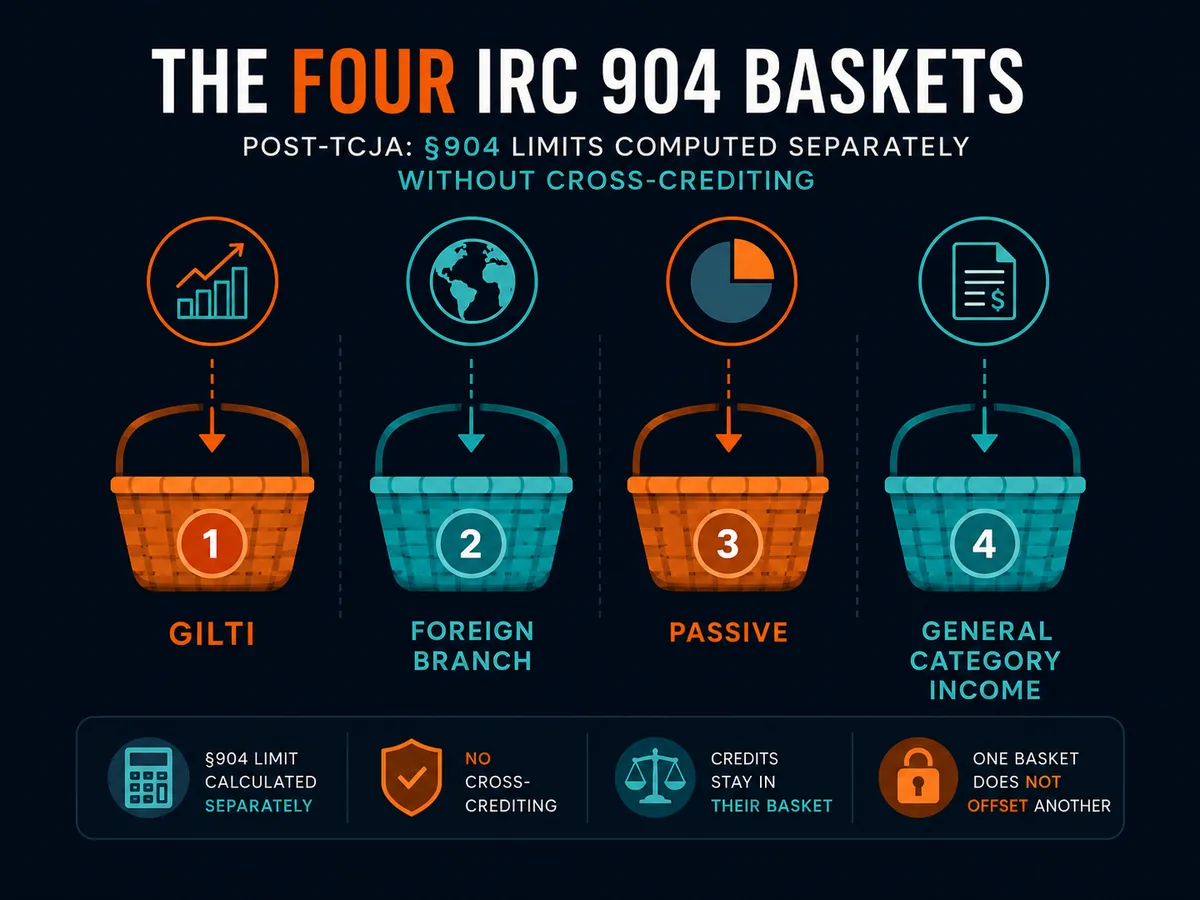

The four §904 baskets (post-2017 TCJA)

The single most important structural feature of the FTC is that foreign income does not all flow into one pot. Under IRC §904(d), foreign income is sorted into separate-limit categories — "baskets" — and the §904 limit is computed and applied independently for each. There is no cross-crediting between baskets, in either direction, in the same year.

The 2017 Tax Cuts and Jobs Act rewrote §904(d). Before TCJA there were two baskets. After TCJA there are four:

| Basket | What it contains | Carryover |

|---|---|---|

| §951A (GILTI) | Global Intangible Low-Taxed Income inclusions from CFCs | None — no carryback, no carryforward |

| Foreign branch | Business profits of a US person attributable to one or more qualified business units (QBUs) outside the US | 1 year back / 10 years forward |

| Passive | Dividends, interest, royalties, rents, annuities, capital gains, net gains from foreign currency, certain commodities | 1 year back / 10 years forward |

| General | Everything else — wages, active business income, financial services income, services fees | 1 year back / 10 years forward |

Source: Form 1116 instructions and IRC §904(d)(1).

Two more "baskets" appear on Form 1116 in practice: lump-sum distributions (Form 4972) and certain income re-sourced by treaty (its own section below).

Why the baskets matter: excess passive-basket tax cannot offset general-basket US tax — a retiree in Spain paying high Spanish tax on US dividends cannot use that surplus to shelter a small consulting fee. A loss in one basket reduces only that basket and triggers separate-limitation-loss recapture later. GILTI sits in its own basket with no carryover at all.

Who this applies to — read this first

The FTC is a US-tax concept. Its relevance to you depends entirely on whether you are inside the US tax system.

US persons (citizens, green-card holders, resident aliens)

This article is primarily for you. The US taxes its citizens and lawful permanent residents on worldwide income regardless of residence. The FTC is the principal mechanism stopping the US from double-taxing dollars already taxed by your country of residence. A US-citizen engineer in Berlin paying ~42% German tax on a €100,000 salary would otherwise owe US federal tax on top.

EU residents (non-US citizens, no green card)

The IRS FTC does not apply to you. EU member states determine residency and worldwide-income taxation under their own rules, and each has its own foreign-tax relief — France's crédit d'impôt étranger, Germany's §34c EStG credit, Spain's deducción por doble imposición internacional. The structure often mirrors the US system because both descend from the OECD model, but the calculation is your country's, not the IRS's. Read this article only if you also hold a US green card or citizenship.

Non-US, non-EU readers

The FTC is not relevant unless you are a US person. If you are a Singaporean, Emirati, Paraguayan or other non-US national, the IRS has no claim on your worldwide income. Where this matters: advising a US-citizen partner or co-founder, or weighing a US green card for work — the FTC mechanics determine whether your US tax bill will be substantial or near zero.

FTC vs FEIE — when each one wins

The FEIE sits in IRC §911 and excludes a capped slice of foreign-earned income — wages and self-employment net income — from US taxable income. For tax year 2026 the cap is $132,900 per qualifying person, up from $130,000 in 2025. It does not cover passive income and does not eliminate self-employment tax.

The FTC credits foreign income tax against US tax on the same foreign-source income. It covers all income types — wages, dividends, capital gains, pensions, rental income — with no per-dollar cap, only the §904 limit per basket. The decision, simplified:

| You live in / earn… | Better tool | Why |

|---|---|---|

| Low- or zero-tax country (UAE, Bahamas, Paraguay, Cayman, Monaco, Brunei, Vanuatu) | FEIE | No foreign tax to credit; exclusion is the only relief |

| High-tax country (Germany, France, UK, Netherlands, Belgium, Denmark, Australia) | FTC | Foreign tax already paid usually exceeds the US tax on the same income; FTC generates carryover credits |

| Income well above the FEIE cap | FTC on the full amount | FEIE leaves the excess fully exposed; FTC scales with no cap |

| Mostly passive income — dividends, capital gains, pensions | FTC | FEIE does not cover passive income at all |

| Want to contribute to a traditional or Roth IRA | FTC | FEIE-excluded income is not "compensation" for IRA purposes — using FEIE blocks IRA contributions |

| US-citizen retiree in a high-tax country | FTC | Retirees have no earned income to exclude |

| Self-employed with mid-to-high foreign tax rate | FTC | Avoids the SE-tax surprise and preserves carryover |

Two structural reasons FTC quietly wins more often than expected: FEIE is sticky — once revoked, the election cannot be re-made for five tax years without IRS consent (§911(e)(2)); and FTC produces a carryover asset, while FEIE does not.

In low-tax jurisdictions, FEIE remains the right answer for most expat freelancers. In high-tax EU countries, the FTC is almost always better. The trap is assuming FEIE is simpler and therefore better — an assumption that costs thousands a year and forecloses IRA contributions over a career.

How to actually compute the FTC

The mechanics live on Form 1116. One form per basket. The calculation has three big steps.

Step 1 — Determine foreign-source income (per basket)

Per Pub 514, compensation for personal services is sourced on a time basis — where the services were physically performed. A consultant who spent 200 of 240 working days in Spain sources 200/240 of the fee as foreign. Interest is sourced to the payer's residence; dividends to the country of incorporation of the paying corporation; rents to the property location; capital gains under IRC §865 generally to the seller's residence (with major exceptions for real estate and inventory).

Step 2 — Allocate and apportion deductions

Deductions definitely related to a class of gross income are allocated to that class. Those not definitely related are apportioned across all classes by gross income ratios. Business interest goes to general-category income, investment interest to passive, home mortgage interest by use of the financed property. State income tax allocation is governed by Treas. Reg. §1.861-8 and §1.861-20. This is where most filers — and many software packages — go wrong.

Step 3 — Apply the §904 limit

The statutory limit, from IRC §904(a):

The total amount of the credit taken under section 901(a) shall not exceed the same proportion of the tax against which such credit is taken which the taxpayer's taxable income from sources without the United States … bears to his entire taxable income.

In plain arithmetic, per basket:

FTC limit = (foreign-source taxable income in basket / total taxable income) × US tax before FTC

The allowed credit is the lesser of (a) foreign tax paid or accrued in the basket, or (b) the §904 limit for that basket. Excess goes to the carryover pool.

Worked example: a US citizen tax-resident in Germany earns €100,000 (≈ $108,000) in general-basket wages, pays €36,000 (≈ $39,000) German tax, and has no other income. US tax on $108,000 after standard deduction is roughly $14,500.

- §904 limit (general) = ($108,000 / $108,000) × $14,500 = $14,500

- Foreign tax paid = $39,000

- Allowed FTC = lesser of the two = $14,500

- US tax owed = $0

- Excess carried back 1 year / forward 10 years = $24,500

The German tax wipes out US liability and produces a $24,500 carryover — an asset with real value in any future year where foreign tax falls below US tax on the same income.

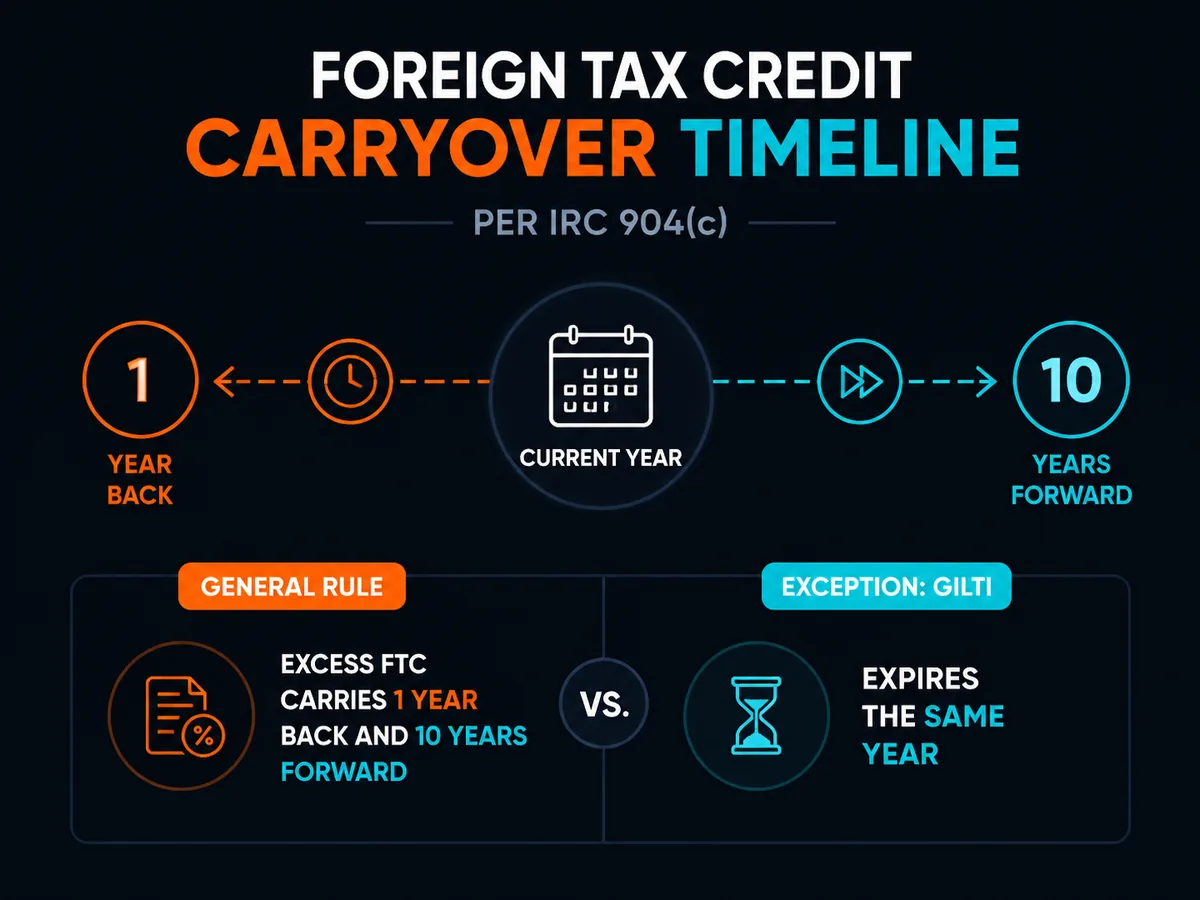

The carryover question

Under IRC §904(c), unused FTC carries back 1 year, then forward up to 10 succeeding tax years, in order. Per basket — passive-basket excess can only offset future passive-basket US tax, never general. GILTI is the harsh exception: §951A excess credits cannot be carried back or forward at all, which is why GILTI planning differs so sharply from ordinary FTC planning.

Strategically: a big-bonus year in Germany at 47% effective banks credits for the future; a later move to a low-tax country burns them when the US rate bites; a heavily-taxed foreign capital gain creates passive-basket credits good for a decade.

Carryovers are tracked on Form 1116, Schedule B (formalised in 2021). Failing to file Schedule B is the easiest way to lose carryover credits in an audit. Keep historical Schedule Bs for the full 10-year window, plus the §6501 statute period.

Treaty-resourced FTC and tax-home elections

Treaty resourcing. US bilateral tax treaties typically include a "resourcing" clause in the relief-from-double-taxation article (usually Article 23 or 24). The clause re-sources what would otherwise be US-source income as foreign-source for FTC purposes when the treaty grants the foreign country primary taxing rights. The classic case: a US citizen in the UK receiving US-source pension distributions. Without resourcing, those would be US-source and UK tax paid on them would be unrelieved. Article 24(4) of the US-UK income tax treaty re-sources the income as UK-source.

Treaty-resourced income goes into its own Form 1116 basket. When the position reduces US tax by more than $10,000, Form 8833 disclosure is required under IRC §6114. Penalty for non-disclosure: $1,000 per position ($10,000 corporate) under §6712.

§6013(g) election — a US citizen with a non-resident-alien spouse can elect under IRC §6013(g) to treat the NRA spouse as a US resident. This unlocks joint filing and full use of the §904 limit at the joint level, but subjects the NRA spouse's worldwide income to US tax. Binding until revoked, and once revoked cannot be remade. A meaningful FTC lever, but a serious commitment.

The US-Germany, US-France and US-Spain treaties each contain resourcing language that changes the FTC calculation for residents of those countries. Read the actual bilateral treaty, not the US Model Convention.

Comparison — FTC vs FEIE for a typical case

A US-citizen freelancer earning $120,000 of services income while bona fide resident of each of the following countries. Simplified: no other income, standard deduction, no dependents, no state tax. Foreign tax estimates are rough effective rates on the bracket.

| Country | Foreign tax rate (approx) | Foreign tax paid | FEIE benefit (US tax) | FTC benefit (US tax) | Winner |

|---|---|---|---|---|---|

| Germany | ~38% effective | $45,600 | ~$0 (under cap) but blocks IRA, no carryover | $0 US tax + ~$30k carryover, IRA preserved | FTC |

| United Kingdom | ~32% effective | $38,400 | ~$0 under cap | $0 US tax + ~$23k carryover | FTC |

| United Arab Emirates | 0% (personal) | $0 | $0 US tax up to cap | Cannot credit zero — full US tax owed | FEIE |

| Paraguay | ~0–10% territorial | $0–$12,000 | $0 US tax up to cap | Partial credit, balance owed | FEIE |

| Singapore | ~15% effective | $18,000 | $0 US tax up to cap | $18,000 credit, balance ~$2k owed | FEIE marginally |

| Spain (Beckham regime) | 24% flat | $28,800 | $0 US tax up to cap | Carryover generated, IRA preserved | FTC if IRA matters |

Source: country-specific rates per OECD Tax Database 2024 and national tax authority schedules. Always run the actual numbers — bracket interaction, housing exclusion, self-employment tax and state residency can flip the result.

In zero-tax jurisdictions FEIE is the only relief available. Above roughly 25–30% effective foreign tax, FTC wins — and the IRA preservation argument tilts it further. The common error is a US-citizen freelancer in Berlin running FEIE on autopilot because that is what the first Google result said.

The traps

FTC is non-refundable and cannot exceed US tax on the same income. Pay $50,000 Danish tax on income where US tax would be $12,000 and the FTC is $12,000. The $38,000 difference becomes a carryover. The FTC offsets US tax — it does not generate cash.

FTC and FEIE cannot apply to the same dollar. Per Pub 514: "You cannot take a credit or a deduction for foreign taxes paid on income you exclude under the foreign earned income exclusion or the foreign housing exclusion." Foreign tax must be allocated pro-rata between excluded and non-excluded portions; only the non-excluded portion enters the FTC calculation. Most expat tax software handles this; many human filers do not.

PFIC interaction. Foreign mutual funds, foreign ETFs and many foreign pension funds are Passive Foreign Investment Companies under IRC §1297. PFIC distributions and gains are taxed at the highest ordinary rate plus an interest charge under §1291, and FTC interaction is hostile — credit may not fully offset the PFIC penalty. A US investor holding a UK ISA in iShares funds, or a German Riester wrapper, can find FTC effectively useless against PFIC tax. The fix is structural: hold US-domiciled funds.

State tax residency. The FTC is federal only. California, New York and several others tax worldwide income of residents with no FTC equivalent. A US citizen who moves to Lisbon but keeps a California driver's licence, rental property and mailing address may still be a California resident — taxed on foreign income with no foreign-tax relief. See our bona fide resident guide and tax resident nowhere.

§911(d)(5) bar. Filing a foreign return as non-resident to avoid foreign tax (some nomad-visa structures encourage this) bars bona fide residence under §911(d)(5) — forcing you off FEIE. Often a feature, not a bug. See the FEIE pillar.

Failing to file Schedule B. Since 2021 the IRS has required Schedule B for any FTC carryover. Filers who never claimed unused credit, then need it in a later low-foreign-tax year, struggle to defend the historical carryover without contemporaneous Schedule Bs. File it every year you have a carryover.

GILTI. A US shareholder of a controlled foreign corporation has annual GILTI inclusions under IRC §951A. FTC on GILTI sits in its own basket with no carryover. For US founders incorporated in the UAE, Singapore or Estonia the GILTI hit can be substantial and the FTC offset partial. A §962 election to be taxed at corporate rates can help — adjacent context in IRS Form 5472.

When to consult a professional

Doing the FTC right is highly profitable and easy to get wrong. Engage a cross-border CPA or Enrolled Agent if:

- You live in a high-tax country and your software default is FEIE.

- You have GILTI inclusions or own equity in a foreign company.

- You have PFIC exposure (foreign mutual funds, ETFs, wrapped pensions).

- You have unused FTC carryovers never tracked on Schedule B.

- You are weighing a §6013(g) election or already made one.

- You receive treaty-resourced income.

- Your state of last US residence is California, New York, Oregon, New Mexico, South Carolina or Virginia.

Two professionals, not one: a US-side preparer for Form 1116, and a host-country tax advisor for the foreign side. The most expensive errors happen when one side optimises in isolation.

Adjacent guides: the Foreign Earned Income Exclusion for the FEIE side of the same decision, FBAR for the parallel reporting obligation, and renouncing American citizenship for the only mechanism that ends the whole system. See our editorial policy and affiliate disclosure.

Ready to act on this?

Bright!Tax — US expat tax filings (FBAR + FATCA + FEIE specialists). Soveraine readers go to the front of the line through our partner link, and you fund independent editorial in the process.

FAQ

What is the foreign tax credit?

The foreign tax credit is a non-refundable, dollar-for-dollar US tax credit for income tax paid to a foreign country. It is the main statutory relief from double taxation for US citizens, green-card holders, US resident aliens, and US-formed entities. The legal basis is Internal Revenue Code §901. The credit is computed on Form 1116 (Form 1118 for corporations), separately for each of four §904 categories — passive, general, GILTI and foreign branch — and is capped by the §904 limitation. Excess credits carry back one year and forward ten years.

What is the difference between the foreign tax credit and the foreign earned income exclusion?

The FEIE excludes a capped amount of foreign-earned wages from US taxable income; the FTC credits foreign income tax already paid against US tax on the same foreign-source income. FEIE wins in low- or zero-tax countries and for income below the cap ($132,900 for tax year 2026). FTC wins in high-tax countries — Germany, France, the UK, the Netherlands — and for passive income, capital gains, pensions and any income above the FEIE cap. You can use both in the same year, but not on the same dollar of income.

How is the foreign tax credit limit calculated?

Under IRC §904(a), the credit cannot exceed: (foreign-source taxable income in the category / total taxable income) × US tax before credit. The calculation is run separately for each of the four §904 baskets — there is no cross-crediting. The limit prevents the FTC from reducing US tax on US-source income. Any foreign tax above the limit is unused and either carried back one year or forward up to ten years per §904(c).

What are the four foreign tax credit baskets?

Under IRC §904(d) as amended by the 2017 Tax Cuts and Jobs Act, foreign income is sorted into four separate-limit categories: (1) Section 951A category — GILTI inclusions from controlled foreign corporations; (2) Foreign branch category — business profits of US persons attributable to qualified business units abroad; (3) Passive category — dividends, interest, rents, royalties, capital gains; (4) General category — everything else, primarily active business and wage income. Each basket has its own §904 limit and its own carryover pool.

What happens to unused foreign tax credit?

Unused FTC creates an excess that can be carried back one tax year and carried forward up to ten succeeding tax years, under IRC §904(c). The carryover is computed per basket — a passive-basket excess can only offset future passive-basket US tax, not general-basket tax. GILTI-basket excess credits cannot be carried back or forward at all. Practically, this means high-foreign-tax years bank credits for future years when the foreign rate falls below the US rate.

Do I need to file Form 1116?

Yes, in nearly all cases. Form 1116 is the individual taxpayer's calculation of the FTC and §904 limit. The de minimis exception waives Form 1116 if total creditable foreign taxes are under $300 ($600 if married filing jointly), all of it is passive-category income reported on a qualified payee statement (1099-DIV, 1099-INT, K-1), and the taxpayer elects on Schedule 3. Above those thresholds, or for any general, GILTI or foreign-branch income, Form 1116 is required. Corporations file Form 1118 instead.

Can I take the foreign tax credit on income excluded under the FEIE?

No. IRC §911 and IRS Publication 514 are explicit: "You cannot take a credit or a deduction for foreign taxes paid on income you exclude under the foreign earned income exclusion or the foreign housing exclusion." If your FEIE excludes part of your wages, you must allocate the foreign tax paid pro-rata and only credit the portion attributable to non-excluded income. This is the single most common error in FEIE-FTC stacking.

Does the foreign tax credit reduce state income tax?

Generally no. The FTC is a federal credit only. Most US states do not offer an equivalent credit for foreign income tax paid. California, for example, taxes worldwide income of its residents and does not allow an FTC. The handful of states that do (a partial credit in some cases, or none at all) treat foreign tax very differently from federal rules. State residency must be severed separately before moving abroad to avoid state tax stacking on top of US federal tax.

Sources

- Internal Revenue Code §901 — Taxes of foreign countries and of possessions of the United States. https://www.law.cornell.edu/uscode/text/26/901

- Internal Revenue Code §904 — Limitation on credit. https://www.law.cornell.edu/uscode/text/26/904

- Internal Revenue Code §905 — Applicable rules. https://www.law.cornell.edu/uscode/text/26/905

- Internal Revenue Code §911 — Citizens or residents of the United States living abroad. https://www.law.cornell.edu/uscode/text/26/911

- Internal Revenue Code §951A — Global intangible low-taxed income (GILTI). https://www.law.cornell.edu/uscode/text/26/951A

- IRS Publication 514 — Foreign Tax Credit for Individuals. https://www.irs.gov/publications/p514

- IRS Instructions for Form 1116 — Foreign Tax Credit (Individual, Estate, or Trust). https://www.irs.gov/instructions/i1116

- IRS Publication 519 — US Tax Guide for Aliens. https://www.irs.gov/publications/p519

- IRS Form 8833 — Treaty-Based Return Position Disclosure. https://www.irs.gov/forms-pubs/about-form-8833

- Treasury — US Model Income Tax Convention 2016. https://home.treasury.gov/policy-issues/tax-policy/treaties

- IRS — United Kingdom (UK) tax treaty documents. https://www.irs.gov/businesses/international-businesses/united-kingdom-uk-tax-treaty-documents

- Tax Cuts and Jobs Act of 2017 — Public Law 115-97, amending IRC §904(d) and creating §951A.