The phrase "offshore bank account" is the most abused term in international finance. For most of the 20th century it meant secrecy — numbered accounts in Switzerland, Cayman shell companies, undeclared balances in Liechtenstein. That version is gone. After fourteen years of FATCA and eight years of the OECD Common Reporting Standard, every chartered bank in every jurisdiction worth banking in reports your balances, interest and gains to your home tax authority annually. What survives is the legitimate version: multi-currency holding, cross-border business operations, counterparty risk spread across jurisdictions, and access to currencies your home banking system does not offer. This guide explains what that looks like, who it suits, and what it costs.

Wise — Multi-currency account in 40+ currencies, regulated, FATCA + CRS compliant by default

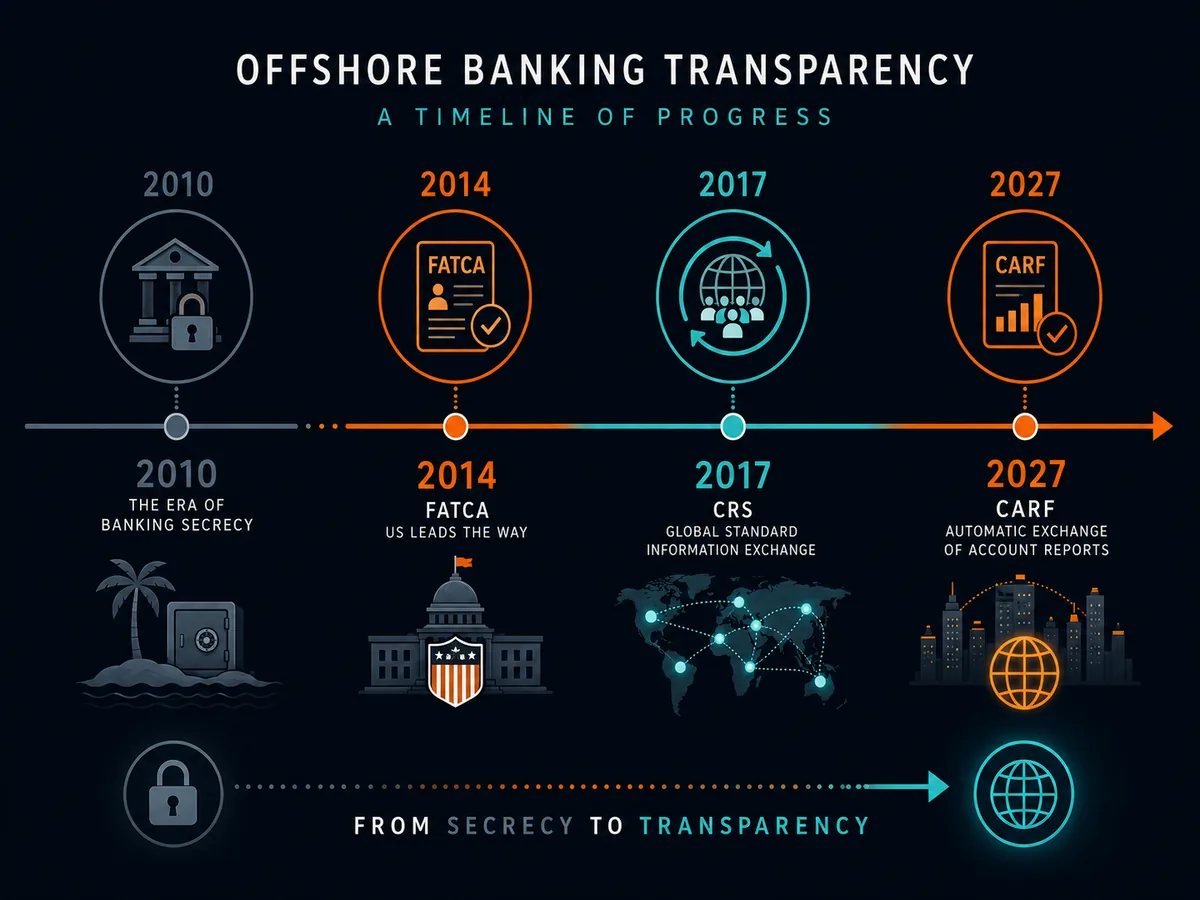

What "offshore" actually means in 2026

An offshore bank account is any deposit or transaction account held at a regulated financial institution in a jurisdiction other than the one where you are tax resident. That is the entire definition. It is not a special product, not a tax structure, and not a secrecy device.

The historical version did rely on secrecy. Until the early 2010s, Swiss bank-secrecy laws criminalised the disclosure of client identity, Cayman and BVI banks did not exchange information with foreign tax authorities by default, and a US or European tax resident could open an account abroad with reasonable confidence that no one at home would find out. Two reforms ended that.

The first was the US Foreign Account Tax Compliance Act, enacted in 2010 and effective from 2014 (IRS — FATCA overview). FATCA requires any non-US financial institution wanting access to US markets to identify its US-person customers and report account details to the IRS. Banks that refuse face 30% withholding on US-source payments. More than 110 jurisdictions have FATCA agreements with the United States.

The second was the OECD Common Reporting Standard, in operation since 2017 (OECD — Automatic Exchange of Information). CRS does globally what FATCA does for the US: every participating jurisdiction's banks identify the tax residency of every account holder and exchange that data annually with the home country. Over 120 jurisdictions participate, including every meaningful financial centre — Switzerland, Singapore, Hong Kong, the UAE, Cayman, BVI, Bermuda, Panama, Luxembourg, Liechtenstein, Jersey, Guernsey and the Isle of Man.

The OECD has now extended this to crypto. The Crypto-Asset Reporting Framework (CARF) applies from 2027, requiring crypto exchanges, brokers and certain wallet providers to report under the same model (OECD — CARF).

The practical consequence: in 2026, opening an offshore account does not hide anything. Your home tax authority will receive a full report on the account within months of year-end. The legitimate reasons to open one are about access and diversification, not concealment.

Who this applies to — read this first

The reporting consequences of an offshore bank account differ sharply by your citizenship and tax residency. Read the section that matches your status.

US persons (citizens and green-card holders)

An offshore bank account is never an asset-hiding play for a US person. FATCA reports US-person accounts globally, and US tax law requires independent disclosure.

Two filings apply. FBAR (FinCEN Form 114) is required if aggregate foreign account balances exceed $10,000 at any point in the calendar year (FinCEN — FBAR). Form 8938 under FATCA applies above higher thresholds — $50,000 at year-end or $75,000 at any point for unmarried filers in the US, doubled for joint filers, much higher for filers abroad ($200,000 / $300,000 unmarried, $400,000 / $600,000 joint) (IRS — Form 8938).

US persons also owe US tax on worldwide income under 26 U.S. Code § 61. Interest, capital gains in foreign brokerages, and foreign mutual funds (typically PFICs under IRC §1291) are all US-taxable. Soveraine's guides on FBAR and FATCA filing go deeper. Non-filing penalties reach $10,000 per non-wilful FBAR violation and the greater of $100,000 or 50% of the account balance per wilful one (31 USC §5321).

EU residents

For EU tax residents, your offshore bank account is automatically reported to your home tax authority under CRS and, within the EU, under Directive 2014/107/EU (DAC2). The bank reports balance, interest, dividends and gross proceeds annually (European Commission — DAC2).

Several EU countries impose extra duties on the taxpayer side. Spain's Modelo 720 requires Spanish residents to declare foreign accounts, securities and real estate over €50,000 — the original penalty regime was struck down by the European Court of Justice in 2022 (Case C-788/19), but the filing duty remains. Germany requires Anlage AUS. France requires Form 3916 for every foreign account, no minimum. CFC rules across the EU under the Anti-Tax Avoidance Directive (ATAD) may also attribute foreign-company income back to resident shareholders.

Non-US, non-EU residents

CRS coverage varies. Most major centres participate — Singapore, Hong Kong, UAE, Switzerland, Cayman, Panama, Bermuda — but enforcement quality differs. The US itself does not participate in CRS, only FATCA; a few Pacific island states have notable gaps.

If you are tax resident in a territorial regime (Singapore, Hong Kong, Malaysia, Panama, Costa Rica, Georgia, UAE), an offshore account holding foreign-sourced income may not be locally taxable provided the funds are not remitted. Rules are jurisdiction-specific; Singapore narrowed its foreign-sourced income exemption in 2024–2025 (IRAS).

Why people open offshore accounts in 2026 (legitimately)

The marketing copy is still stuck in 1995. The real reasons to open one in 2026 are mundane and defensible.

Currency diversification. Holding USD, EUR, GBP or CHF outside your home country reduces exposure to a single currency and banking system. Argentine, Lebanese, Nigerian and Turkish residents have learned this through capital controls and devaluations.

Cross-border business. A consultant invoicing US clients from Berlin benefits from receiving USD into a USD account rather than converting at the German bank's retail FX rate. A Hong Kong ecommerce founder selling on Amazon US needs a USD-receiving account.

Lower fees and better FX. Retail FX spreads at high-street banks run 2%–4% over mid-market. Wise, Revolut and Statrys charge 0.4%–1%. On six-figure annual flows the saving compounds.

Capital controls. Residents of Argentina, Lebanon, Egypt, Nigeria, Pakistan and retail China hold offshore accounts as a hedge against blocked access. Argentine middle-class savers holding USD in Uruguay or Miami is the canonical example.

Estate planning. Where succession law at home is rigid (forced heirship in France, Italy, Spain), accounts in jurisdictions with flexible succession rules can complement an estate plan. Niche, requires specialist advice, but real.

Counterparty risk diversification. Bank failures happen. Depositors at SVB, Credit Suisse, First Republic and several Russian banks in 2022–2023 were reminded that single-jurisdiction concentration carries its own risk.

None of these require secrecy. All are achievable with a fully-reported account.

The realistic shortlist by audience

Most "best offshore banks" lists are written by people who have never opened one. The realistic options in 2026 break into seven categories.

Multi-currency EMIs (Wise, Revolut, Payoneer, Airwallex)

Regulated as electronic money institutions, not chartered banks. Wise (UK FCA, US FinCEN MSB) and Revolut (Lithuanian banking licence) lead in the West; Airwallex leads Asia-Pacific; Payoneer handles marketplace payments. No minimum, online onboarding in days, multi-currency receiving, low FX spreads. Balances are safeguarded at partner banks, not insured the same way as a bank deposit. Best for cross-border freelancers and small-to-mid businesses with under $250,000 in working capital.

Singapore (DBS Treasures, OCBC Premier, UOB Privilege)

The premium tier. DBS Treasures requires SGD 350,000 (about US$260,000) AUM; OCBC Premier SGD 200,000; UOB Privilege SGD 350,000. Regulated by the Monetary Authority of Singapore (MAS). SDIC deposit insurance covers SGD 100,000 per depositor per bank. Non-resident opening typically requires in-person visit and source-of-funds documentation. US persons accepted with FATCA paperwork. Best for high-income professionals and family offices.

Hong Kong (HSBC Premier, Hang Seng Prestige, Statrys, Citibank)

HSBC Premier requires HKD 1 million (about US$128,000) in total relationship balances. Statrys is the SME-friendly option — no minimum, multi-currency, designed for non-resident small businesses, regulated by Hong Kong Customs and Excise as a Money Service Operator. Hong Kong banks tightened non-resident onboarding after 2020; expect 4–8 weeks. US persons accepted with FATCA documentation. Hong Kong Deposit Protection Scheme covers HKD 800,000 per depositor per bank.

UAE (Mashreq, Emirates NBD, ADCB, FAB)

UAE retail banking requires UAE residency — visa, Emirates ID, proof of address. Once resident, opening is fast (1–2 weeks); minimums range from AED 3,000 (about US$820) to AED 100,000+ for priority banking. Mashreq Neo and Liv are digital-first for residents. UAE has no personal income tax but applies a 9% corporate tax above AED 375,000 (UAE Ministry of Finance). UAE participates in CRS.

Switzerland (UBS, Pictet, Lombard Odier, Julius Bär)

The classical private banks are open at the top end only. New-client minimums start at CHF 500,000 and rise to CHF 5 million-plus at the most exclusive houses. Swiss bank-secrecy law was effectively dismantled for cross-border tax matters in 2014; FINMA supervises and Switzerland implements CRS in full (FINMA). UBS and Pictet accept US persons selectively under FATCA-qualified intermediary regimes; many smaller cantonal banks no longer do. Esisuisse deposit protection covers CHF 100,000 per depositor per bank.

Caribbean (Cayman, BVI, Bermuda, Bahamas)

Increasingly hard to open as a non-resident. Minimums at surviving private banks (Butterfield, RBC Caribbean, Cayman National) start at US$250,000–500,000. Heavy documentation, in-person visit, often a home-country banking reference. The Caribbean's offshore appeal has narrowed sharply since CRS — every listed jurisdiction participates and all have economic-substance legislation. For most readers, no longer worth the friction.

Channel Islands and Isle of Man (HSBC Expat, Lloyds International, Standard Bank)

HSBC Expat, based in Jersey, is the most accessible offshore account for English-speaking customers — £50,000 in HSBC savings, investments or sole annual income, multi-currency across 20+ currencies, and US persons explicitly accepted. Jersey participates in CRS. Behaves like a UK retail account for most purposes. Lloyds International (Isle of Man) and Standard Bank International (Jersey) offer similar products at similar minimums.

CRS + FATCA — the reporting reality

Every bank in a CRS-participating jurisdiction reports your balances annually to your tax-residency country. There is no opt-out and no small-account exception.

At opening, the bank captures a self-certification of tax residency and cross-checks it against address, phone numbers and any indicia (mailing address in another country, standing instructions to a third country, power of attorney elsewhere). What gets reported: name, address, tax identification number, date of birth, account number, year-end balance, gross interest, gross dividends, other income from financial assets, and gross proceeds from financial-asset sales (OECD — CRS Standard).

The participating list includes virtually every meaningful financial centre — Switzerland, Singapore, Hong Kong, UAE, Cayman, BVI, Bahamas, Bermuda, Jersey, Guernsey, Isle of Man, Liechtenstein, Luxembourg, Malta, Cyprus, Panama, Andorra, Monaco. The United States is the conspicuous exception — it has FATCA but does not reciprocate fully under CRS. This is the basis of the (largely true) claim that the US itself has become the last meaningful banking-secrecy jurisdiction — for non-US persons banking in the US, though never for US persons banking abroad.

FATCA operates in parallel. Every non-US financial institution holding a US-person account reports it to the IRS via the local tax authority or directly. The IRS cross-checks against FBAR and Form 8938 filings.

From 2027, the OECD Crypto-Asset Reporting Framework extends the same model to crypto exchanges, brokers and certain wallet providers (OECD — CARF). The era of unreported crypto holdings is ending on the same timeline that unreported bank accounts ended a decade ago.

Comparison table

| Jurisdiction | Minimum AUM (typical) | Multi-currency | Accepts US persons | CRS participant | Best for |

|---|---|---|---|---|---|

| Wise (EMI, multi-jurisdiction) | $0 | 40+ currencies | Yes | N/A — EMI reports under CRS/FATCA | Cross-border freelancers, SMEs |

| Revolut Business (EU) | $0 | 30+ currencies | Yes (US entity) | Yes | EU-based SMEs, frequent travellers |

| Singapore (DBS Treasures) | US$260,000 | Yes | Yes (with FATCA) | Yes | High-income professionals, family offices |

| Hong Kong (HSBC Premier) | US$128,000 | Yes | Yes (with FATCA) | Yes | Asia-active business owners |

| Hong Kong (Statrys SME) | $0 | Yes | Yes | Yes | Non-resident small businesses |

| UAE (Mashreq, ENBD) | US$820+ (residents only) | Yes | Yes (with FATCA) | Yes | UAE tax residents |

| Switzerland (UBS, Pictet) | CHF 500,000+ | Yes | Selectively | Yes | Genuine private banking clients |

| Jersey (HSBC Expat) | £50,000 income/assets | Yes | Yes | Yes | English-speaking expats, US persons |

| Caribbean (Cayman, BVI) | US$250,000+ | Yes | Selectively | Yes | Established trust/corporate structures |

Minimums and policies change. Verify directly with each institution before relying on any number above.

What "offshore" cannot do for you in 2026

Worth saying plainly, because the marketing still implies otherwise.

It does not reduce your tax. Income is taxed by the country (or countries) of your tax residency, regardless of where the account sits. Moving a Wise account from Belgium to Singapore does not change a Belgian tax bill. The only legal way to reduce tax is to change tax residency itself — and that requires moving your life, not just an account.

It does not hide assets. CRS and FATCA report. The only assets that remain unreported are those outside the participating banking system (physical cash, gold, crypto pending CARF), each with serious drawbacks at scale.

It does not escape sanctions. US OFAC sanctions reach globally through USD clearing and correspondent banking. Russian, Iranian and Venezuelan persons have discovered that an account in a non-US jurisdiction does not protect them once correspondent banks decline to clear USD on their behalf. The Bank Secrecy Act and Patriot Act §312 (31 USC §5318(i)) give US regulators direct visibility into correspondent flows.

It does not replace a domestic bank. Mortgages, business credit lines, payroll and secured lending are easier and cheaper at a bank where the underlying asset sits. An offshore account complements; it rarely replaces.

It does not solve the US-person problem. US citizens and green-card holders owe tax and reporting on worldwide income and accounts. The only ways out are renunciation (with potential exit tax under IRC §877A) or formal abandonment of LPR status. See Soveraine's guide on renouncing American citizenship.

The opening-account playbook

Define purpose first. Multi-currency receiving for a freelance business is a different requirement from a USD reserve for currency hedging, and different again from a private-banking relationship for a seven-figure portfolio. The right institution differs at each tier.

Confirm eligibility against tax residency. Singapore retail banks accept most nationalities including US persons. UAE retail banks require UAE residency. Caribbean private banks often require an introduction. Swiss private banks accept US persons only at specific houses. Establish the menu before filling forms.

Prepare KYC documents. Standard pack: passport (often two photo IDs), proof of address under three months old, source-of-funds statement, tax residency certificate where required, and for US persons IRS Form W-9. Corporate accounts add certificate of incorporation, beneficial ownership disclosure (10% or 25% threshold), articles, register of directors and shareholders, and proof of operating address.

Budget the visit. Singapore, Hong Kong, Switzerland and the UAE typically require an in-person visit for non-residents. Budget $2,000–$8,000 in travel. Jersey (HSBC Expat) and most EMIs onboard fully remotely.

Budget the time. Two to twelve weeks is realistic. Swiss private banks and Singapore premium tiers regularly take three months. EMIs open in days.

Fund through a clean channel. Initial funding from an account in your own name, at a bank in your country of tax residence, via SWIFT wire with a clear reference. Cross-border cash and third-party payments are refused.

Maintain operating discipline. Use the account consistently with the declared purpose. Sudden volume spikes, payments from sanctioned jurisdictions, or layering-like patterns trigger AML review.

The traps

Debanking risk. Even compliant accounts at major institutions can be closed without detailed explanation if residency, business or transaction pattern changes. Always keep a backup account at a second institution in a different jurisdiction.

CRS reporting holes. A small number of jurisdictions report late or incompletely — typically smaller Caribbean and Pacific island states. The data lags; you are still reported. Filing your home-country disclosure regardless is the only defensible posture.

Correspondent-banking risk. Smaller banks in smaller jurisdictions rely on a handful of correspondent banks in New York and London to clear USD and EUR. If a correspondent cuts the relationship, the local bank can no longer settle international payments. Mexico, Belize, several Pacific islands and parts of the Caribbean have lost correspondent relationships in the last five years.

The fee stack. Headline fees rarely tell the full story. SWIFT charges ($15–$50), intermediary bank fees ($10–$30 per leg), FX spread (2%–4% at retail banks vs 0.4%–1% at EMIs), account-maintenance, inactivity and minimum-balance shortfall fees can together cost 1%–3% of balance annually at the wrong institution. Read the fee schedule in full before opening.

Currency-control surprises. Some host jurisdictions restrict outbound transfers — India's LRS ($250,000/year), China's $50,000 annual quota, various African and Latin American limits.

Mismatching business registration and operator residence. Incorporate in Estonia or Delaware, hold the account at Wise or Mercury, operate from Berlin or Madrid — under the place-of-effective-management test, EU tax authorities will frequently deem the company a domestic tax resident regardless. The account is incidental; the structural mismatch is what creates the exposure.

When to consult a professional

Before opening any offshore account beyond a multi-currency EMI for routine business, speak to:

- A tax advisor in your country of tax residence — reporting, declaration thresholds, CFC implications.

- A tax advisor in the country where the account sits — local source-of-funds requirements and any local tax on interest or gains.

- For US persons, a cross-border CPA — FBAR, Form 8938, PFIC analysis, foreign trust reporting (Form 3520) and exit-tax planning are not optional.

- For complex structures, an international tax attorney — wherever a foreign company, trust or foundation sits between you and the account.

Two professionals minimum: one home-country, one account-jurisdiction. The most expensive errors happen when one side optimises in isolation.

For related Soveraine guides see Opening a Company Bank Account, Best US Business Bank Accounts for Foreign-Owned LLCs, the Wise Business Bank Account review, and our pillars on FBAR and FATCA filing requirements.

Ready to open one?

Wise — multi-currency holding in 40+ currencies, regulated, reports to your tax authority by default. The lowest-friction starting point for a legitimate offshore account in 2026. Soveraine readers go through our partner link, and you fund independent editorial in the process.

FAQ

What is an offshore bank account in 2026?

An offshore bank account is simply a deposit or transaction account held at a chartered bank — or a regulated electronic money institution — in a jurisdiction other than the one where you are tax resident. The 20th-century version, defined by secrecy and undisclosed balances, no longer exists in any country worth banking in. Since the OECD Common Reporting Standard rolled out from 2017 and US FATCA from 2014, banks in 120+ jurisdictions report account balances, interest, dividends and gross proceeds to your home tax authority annually. What survives in 2026 is the legitimate use case: multi-currency holding, cross-border business operations, currency diversification, and counterparty risk spread across jurisdictions.

Are offshore bank accounts legal?

Yes, in almost every country. Holding a foreign bank account is legal for US persons, EU residents and most other nationalities provided you report it. US citizens must file FinCEN Form 114 (FBAR) if aggregate foreign account balances exceed $10,000 at any point in the calendar year, and Form 8938 under FATCA above higher thresholds. EU residents are automatically reported under CRS but may have additional declaration duties — Germany and Spain both require taxpayer-level disclosure on the annual return. Failing to report is what creates legal trouble, not the account itself. A handful of countries (Iran, North Korea, Russia under certain conditions) restrict their own residents from holding foreign accounts.

What is the best offshore bank account for non-residents?

There is no single best account because the right choice depends on your tax residency, the currencies you need and how much you can deposit. For internet-first freelancers and small companies moving under $250,000, a regulated electronic money institution like Wise, Revolut or Payoneer covers most needs at the lowest cost. For account balances of $200,000 to $1 million, Singapore (DBS Treasures, OCBC Premier) and Hong Kong (HSBC Premier, Statrys) remain the most accessible chartered-bank options for non-residents. For balances above $1 million, Swiss private banks (UBS, Pictet, Lombard Odier) still take new clients selectively. US persons face the narrowest menu — many non-US banks refuse them outright because of FATCA compliance cost.

How much money do you need to open an offshore bank account?

It depends entirely on the institution. Electronic money institutions like Wise and Revolut have no minimum and open in days. Statrys in Hong Kong opens with no minimum balance for small businesses. Standard retail accounts at HSBC Expat require £50,000 in savings, investments or income. Singapore's DBS Treasures requires SGD 350,000 (about US$260,000) in assets under management. Hong Kong's HSBC Premier requires HKD 1 million (about US$128,000). Swiss private banks typically require CHF 500,000 to CHF 1 million for new clients. UAE retail accounts can open with AED 3,000 to AED 25,000 but require UAE residency. Caribbean private banks have largely moved upmarket to US$250,000+ minimums.

Does CRS report my offshore bank account to my home country?

Yes, if the account is held in any of the 120+ jurisdictions participating in the OECD Common Reporting Standard. Each participating bank identifies the tax residency of every account holder, then reports your name, address, tax identification number, account number, account balance at year end, gross interest, gross dividends, gross proceeds from financial asset sales, and certain insurance contract values to its local tax authority, which forwards the data to your home country's tax authority annually. There is no opt-out. The OECD Crypto-Asset Reporting Framework (CARF) extends the same reporting model to crypto exchanges and wallet providers from 2027 in participating jurisdictions.

Do offshore banks accept US citizens in 2026?

Many do not. US FATCA imposes withholding and reporting obligations on any foreign financial institution that holds US-person accounts, and the compliance cost is high enough that smaller banks simply refuse to onboard US citizens or green-card holders. The institutions that do accept US persons in 2026 include HSBC Expat (Jersey), Interactive Brokers (regulated brokerage with cash management), Swiss private banks at the top end (UBS, Pictet — selectively), and Singapore's larger banks for qualifying private clients. Wise and most major US-licensed EMIs accept US persons without issue because they file IRS Form 1099 directly. US persons should expect to fill out IRS Form W-9 at account opening and accept that the bank will report to the IRS via the local tax authority.

What does an offshore bank account actually cost?

Cost has three components. First, account-keeping: chartered banks typically charge $10 to $50 per month, often waived above a minimum balance; EMIs charge $0 to $15. Second, transaction costs: SWIFT wires cost $15 to $50 outbound, FX conversion adds 0.4% to 3% over mid-market depending on provider (Wise sits at 0.4%-1%, retail banks at 2%-4%). Third, setup costs: in-person account opening trips to Singapore or Switzerland run $2,000 to $8,000 in travel; introducer fees for Swiss private banks range from $5,000 to $25,000 if you use one. The hidden cost is time — chartered-bank onboarding for non-residents takes four to twelve weeks of document collection and sometimes a personal visit.

What is the difference between an offshore bank and an EMI like Wise?

A chartered bank holds your deposits on its own balance sheet under a banking licence issued by a national regulator (FCA in the UK, MAS in Singapore, HKMA in Hong Kong, FINMA in Switzerland), and your deposits are covered by that jurisdiction's deposit insurance scheme up to a defined limit. An electronic money institution like Wise, Revolut or Payoneer holds your money in segregated safeguarded accounts at partner banks under an EMI licence — your funds are protected from the EMI's insolvency but are not insured the same way as a chartered-bank deposit. EMIs cannot lend your money out, cannot offer credit products in most cases, and are generally cheaper and faster to open. Both report under CRS and FATCA where applicable.

This pillar is editorial. We disclose affiliate relationships where they exist — see our affiliate disclosure and editorial policy. Nothing here is tax, legal or financial advice — see our disclaimer.

Sources

- OECD — Automatic Exchange of Information portal: https://www.oecd.org/tax/automatic-exchange/

- OECD — Common Reporting Standard: https://www.oecd.org/tax/automatic-exchange/common-reporting-standard/

- OECD — Crypto-Asset Reporting Framework (CARF): https://www.oecd.org/tax/exchange-of-tax-information/crypto-asset-reporting-framework-and-amendments-to-the-common-reporting-standard.htm

- IRS — Foreign Account Tax Compliance Act (FATCA): https://www.irs.gov/businesses/corporations/foreign-account-tax-compliance-act-fatca

- IRS — Summary of FATCA Reporting for U.S. Taxpayers (Form 8938 thresholds): https://www.irs.gov/businesses/corporations/summary-of-fatca-reporting-for-u-s-taxpayers

- FinCEN — Report of Foreign Bank and Financial Accounts (FBAR): https://www.fincen.gov/report-foreign-bank-and-financial-accounts

- 31 USC §5321 — FBAR penalty regime: https://www.law.cornell.edu/uscode/text/31/5321

- 31 USC §5318(i) — Patriot Act §312 correspondent banking due diligence: https://www.law.cornell.edu/uscode/text/31/5318

- 26 USC §61 — Gross income defined: https://www.law.cornell.edu/uscode/text/26/61

- 26 USC §877A — Expatriation tax: https://www.law.cornell.edu/uscode/text/26/877A

- European Commission — DAC2 administrative cooperation: https://taxation-customs.ec.europa.eu/dac2_en

- EU Anti-Tax Avoidance Directive (ATAD): https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32016L1164

- Spain — Modelo 720 foreign asset declaration: https://sede.agenciatributaria.gob.es/Sede/en_gb/declaraciones-informativas-otros-impuestos-tasas/modelo-720-2017-y-anteriores.html

- IRAS Singapore — Taxable and non-taxable income: https://www.iras.gov.sg/taxes/individual-income-tax/basics-of-individual-income-tax/what-is-taxable-what-is-not

- Monetary Authority of Singapore (MAS): https://www.mas.gov.sg/

- FINMA — Swiss Financial Market Supervisory Authority: https://www.finma.ch/en/

- UAE Ministry of Finance — Corporate Tax: https://mof.gov.ae/corporate-tax/

- HSBC Expat (Jersey): https://www.expat.hsbc.com/

- Statrys (Hong Kong): https://statrys.com/