Relay approves a meaningful share of foreign-owned LLC applications that Mercury and the traditional banks decline. That single fact is the most useful starting point, because most guidance on US business banking for non-residents is written as if every application is approved and every fintech is interchangeable. They are not. This is the honest map: which providers actually take foreign-owned LLCs in 2026, which reject most non-residents, what documents matter, and how the three audience groups — US persons with an SSN, EU residents with an EIN-only foreign-owned LLC, and applicants from outside both blocs — should approach the question differently.

Relay — US business banking that often approves non-resident-owned LLCs Mercury rejects

Why "best" depends on who you are

There is no single best US business bank account for a foreign-owned LLC. There is a best provider for your residency, tax-ID status, business activity and funding source — and a different one if any of those change.

A US citizen with an SSN forming a single-member Wyoming LLC can walk into Chase tomorrow. A Dutch consultant with an EIN-only Delaware LLC selling SaaS to US clients has a clean Mercury or Relay path. A Pakistani drop-shipper with the same LLC will be filtered out by Mercury's risk model before a human reads the application. Wise Business and Payoneer remain open; chartered banks are closed without a US trip and an ITIN.

Activity matters as much as residency. Drop-shipping, lead generation, anything crypto-adjacent, payment facilitation, gambling and adult content trip underwriting models. Plain consulting, SaaS, agency work and Shopify or Amazon e-commerce clear them more often than not, provided the country of residence is not itself flagged.

Who this applies to — read this first

The same question has three answers depending on who is asking.

US persons (US SSN)

If you hold a US Social Security number, every door is open. Mercury and Relay accept you on the strength of the SSN alone. Chase and Bank of America will open business accounts for a US-resident SSN holder without friction. The interesting choice is between a chartered bank for reserves, lending and credit cards, and a fintech like Mercury for product polish and Stripe-grade integrations. Most US founders end up holding both.

EU residents (foreign-owned LLC, EIN-only)

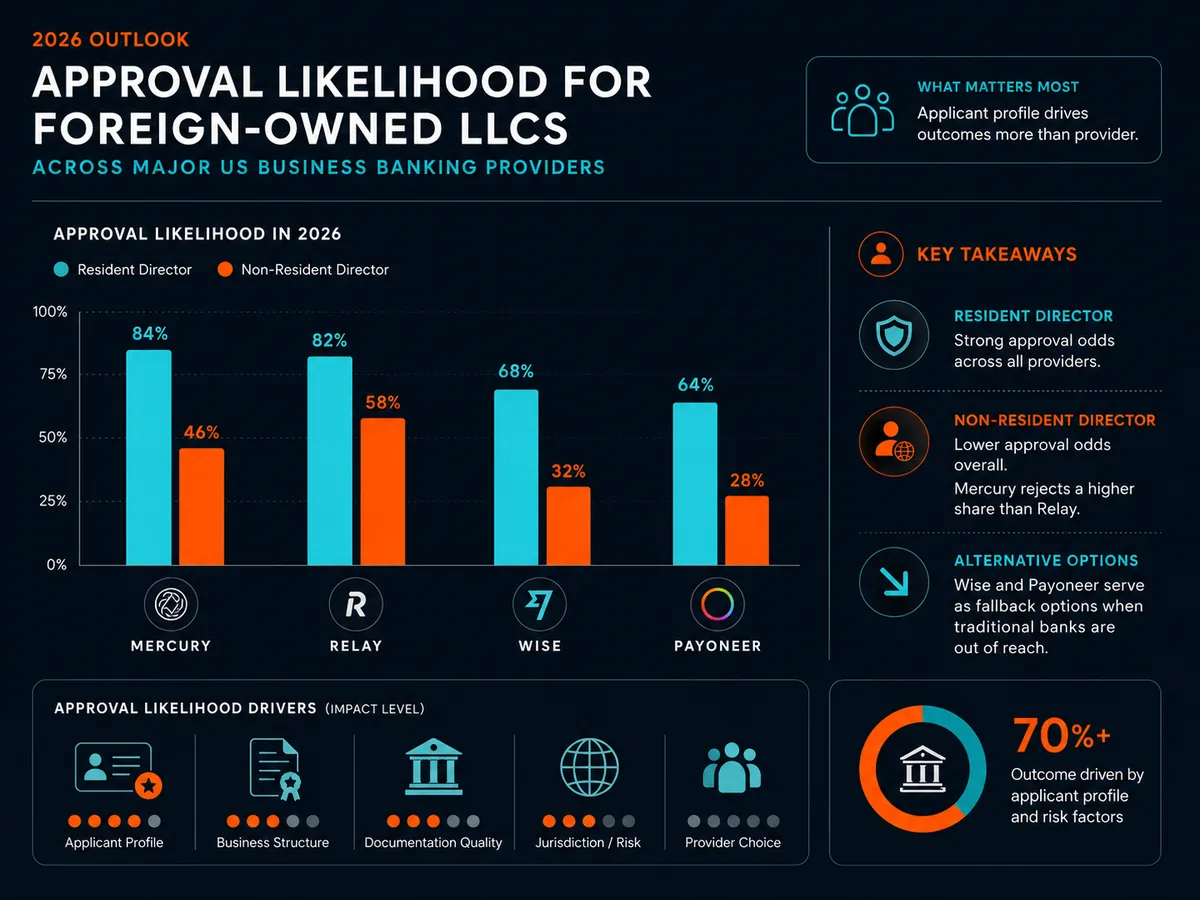

The most common reader of this article — an EU tax resident who has formed a US LLC for an internet business and now needs a US dollar account. The EIN is the only US identifier. Mercury accepts a meaningful share of these applicants but rejects others without explanation, with the rejection rate climbing for residents of certain Eastern European and Mediterranean countries. Relay accepts a larger share, particularly when Mercury declines. Wise Business is the multi-currency backbone almost everyone in this group should also hold.

Non-US, non-EU readers

For residents of Latin America, Africa, the Middle East outside the GCC, Central Asia and South-East Asia, the filters tighten. Mercury declines most applicants from this group. Relay accepts more but is not universal. The realistic shortlist is Relay first, Wise Business and Payoneer as fallbacks, and Airwallex for e-commerce or Asian-currency receivables. The chartered US banks are accessible only via a US trip with an ITIN, a verified US residential address and a US mobile number that does not flag as VoIP.

The realistic shortlist for non-residents

These are the providers worth applying to in 2026. Fees, approval policy, and supported countries change frequently — verify at each provider's disclosure page before applying.

Relay

Relay Financial Technologies, Inc. operates the Relay account in partnership with Thread Bank (Member FDIC). [source: FDIC BankFind — Thread Bank] The product is a US business checking account with up to 20 individual checking accounts under a single legal entity — useful for envelope-style cash management where sub-accounts hold tax reserves, payroll, and operating cash separately. Relay accepts foreign-owned LLCs with an EIN and no SSN, and has built a reputation among non-resident founders for approving applications other US fintechs decline.

No monthly fee on the standard plan, free incoming domestic wires, Mastercard debit cards in USD. Outgoing international wires cost a flat fee plus partner-bank FX margin. Stripe, PayPal, QuickBooks and Xero integration is standard. The main weakness is a smaller credit-card ecosystem than Mercury. For a foreign-owned LLC whose primary need is a working US dollar checking account with reliable ACH and wires, Relay is the most defensible default in 2026.

Mercury (with caveats)

Mercury operates through partner banks Choice Financial Group and Column N.A., both FDIC-insured chartered banks. [source: FDIC BankFind] The product is excellent — clean UX, strong Stripe and QuickBooks integration, no monthly fees, free domestic wires, virtual and physical cards. For a US-formed LLC whose beneficial owner is in a country Mercury risk-scores comfortably, it is among the strongest fintech business accounts available.

The honest part: Mercury rejects a significant share of foreign-owned LLC applications. Common triggers include residence in restricted countries (which expanded in 2024-2025), business activity Mercury considers high-risk, templated formation-service paperwork, and use of a registered-agent address as the only business address. Rejections are usually delivered without specific reason. If your residency or activity falls into a flagged category, plan for Relay as the realistic landing spot.

Wise Business

Wise US Inc. is a FinCEN-registered Money Services Business and a licensed money transmitter in 49 states plus DC and Puerto Rico — not a chartered bank. [source: FinCEN MSB Registrant Search] The account issues US ACH and wire details for receiving USD, plus local account details in EUR, GBP, AUD and other currencies. FX is at the mid-market rate plus a disclosed fee — typically the cheapest available for the small-business segment.

For foreign-owned LLCs, Wise is rarely the primary account but almost always a useful secondary one. It accepts US-formed entities with non-resident owners, charges a one-time setup fee around $31 in the US and no monthly fee. Hold operating USD with Mercury or Relay; route multi-currency receivables and FX through Wise.

Payoneer

Payoneer Global Inc. is a FinCEN-registered Money Services Business that operates US receiving accounts through partner banks. Its strength is for sellers on marketplaces — Amazon, Etsy, Upwork, Fiverr — and for receiving from platforms that disburse to local US account details. Accessible from more countries than Mercury or Relay, including jurisdictions those two decline. The trade-off is fewer treasury features, higher FX spread than Wise, and less suitability as an operating account. Use it as a receiving rail and sweep balances out.

Airwallex

Airwallex (USA), Inc. is licensed as a money transmitter and offers multi-currency accounts plus an integrated payment-processing layer that competes with Stripe. It accepts a wider range of company structures than US-focused fintechs — Hong Kong, Singapore, US, UK and EU entities all onboard through similar flows. For a foreign-owned US LLC running global e-commerce with receivables in CNH, JPY or AUD, Airwallex is a credible alternative to the Mercury-plus-Wise pattern.

US-resident options that don't suit non-residents

Listed because non-residents repeatedly ask about them. The short answer: difficult or impossible to open without an SSN and a US visit.

Chase is the gold standard for US business banking — credit cards, lending, broad payment-processor integration, branch network. As a non-resident you need an ITIN, an in-person branch appointment, a verified US residential address and the full LLC document set. Not a remote application.

Bank of America has a similar profile to Chase — friendly to international owners with the right documents and an in-person visit. [source: Bank of America Small Business Checking]

Bluevine advertises a no-fee US business checking account but requires US-resident beneficial owners and a US SSN for the responsible party. Brex restructured its criteria in 2022 and foreign-owned LLCs without a US-resident founder are usually outside its band. Novo is US-resident-only — application gates on SSN and US residential address.

If your only realistic path is a chartered US bank, obtain an ITIN, secure a US mobile number that registers as a true mobile line rather than VoIP, secure a verified US residential address (not a PO box, not most virtual-mailbox addresses) and book branch appointments at Chase, BofA and Wells Fargo for the same week.

The application playbook

The steps below assume you have already formed the LLC and obtained the EIN. If you have not, the EIN-without-SSN path is on IRS Form SS-4: a foreign responsible party submits the form by fax or mail to the IRS international applicant unit, and the EIN is returned within four to six weeks. [source: IRS — How to Apply for an EIN]

Use a verifiable business address, not just the registered-agent address. Mercury, Relay and the chartered banks all check whether the company address resolves to a real business location. A registered-agent address is fine for state filings; it is a red flag at onboarding because every templated LLC uses it. A virtual business address that returns a real street suite — iPostal1 is one common option — passes the check more often.

Bring a clean, honest description of the business activity. Bank Secrecy Act compliance requires US institutions to risk-rate customers based on activity. [source: FinCEN — Bank Secrecy Act overview] Vague descriptions ("e-commerce consulting") underperform specific ones ("software development for European fintech clients, billing $5-15k per month per client via Stripe USD payouts").

Prepare beneficial-ownership documentation. Every individual holding 25% or more of the LLC needs to be identified under FinCEN's beneficial ownership rule. [source: FinCEN — Beneficial Ownership Information Reporting] Passport, proof of address dated within 90 days, and personal contact details are minimum.

Have a backup ready before the first application closes. If Mercury rejects, Relay should already be staged — business activity stops while accounts are pending.

Comparison table

Values below should be verified at each provider's own pricing and policy page before opening an account.

| Provider | Foreign-owned LLC approval | EIN only ok? | Monthly fee | Free incoming wire | Best for |

|---|---|---|---|---|---|

| Relay | Frequently approves where others decline | Yes | $0 | Yes, domestic | Operational US banking, sub-account cash management |

| Mercury | Selective; rejects many non-residents | Yes | $0 | Yes, domestic | US-formed startups with comfortable risk profile |

| Wise Business | Broad acceptance | Yes | $0 (~$31 setup) | Yes, USD ACH/wire | Multi-currency receivables and FX |

| Payoneer | Broad acceptance | Yes | $0 | Yes, USD | Marketplace sellers and platform payouts |

| Airwallex | Broad acceptance, e-commerce focus | Yes | $0 entry tier | Yes, USD | Multi-currency e-commerce, integrated processing |

| Chase Business | Possible with US trip + ITIN | Often requires SSN/ITIN | $15, waivable | No | Chartered-bank deposit, credit cards, lending |

| Bank of America | Possible with US trip + ITIN | Often requires SSN/ITIN | $16-29, waivable | No | Chartered-bank deposit and broad services |

| Bluevine | Usually declined for non-residents | Often requires SSN | $0 | Limited | US-resident small businesses |

| Brex | Usually declined for non-residents | US-resident criteria | $0 | Yes | Venture-backed US startups |

| Novo | Declined for non-residents | Requires SSN | $0 | Limited | US-resident solo founders |

What this isn't

Almost every fintech in the realistic shortlist for non-residents is a Money Services Business or licensed money transmitter — not a chartered bank. Mercury and Relay sit on top of FDIC-insured partner banks; Wise, Payoneer and Airwallex are MSBs with funds safeguarded at partner institutions. FDIC pass-through insurance applies at the partner-bank level, subject to the standard $250,000 per depositor, per ownership category limit at each insured bank. [source: FDIC Deposit Insurance Coverage]

In practice: for operating cash of a few hundred thousand dollars and below, the fintech providers behave like banks for every reasonable purpose. For meaningful treasury balances, the chartered-bank relationship — Chase, BofA or a sweep network with per-bank limits documented in writing — is the cleaner answer. Do not park multi-million-dollar reserves in a single Wise or Payoneer balance.

These accounts also do not change the tax position of the LLC or its owners. A foreign-owned single-member US LLC is a disregarded entity by default and files Form 5472 with Form 1120 annually; the foreign owner remains taxable on US-effectively-connected income and may owe withholding on US-source FDAP. [source: IRS — Form 5472] Holding the bank account does not create or remove US tax obligations.

The default sequence for a freshly-formed foreign-owned US LLC: open Relay as the primary checking account, Wise Business as the multi-currency layer, and apply to Mercury second, accepting the rejection risk. Add Payoneer for marketplace payouts, Airwallex for Asian-currency receivables, and plan a US trip for chartered-bank accounts once revenue justifies the friction. The cost of getting this wrong is not a closed account — it is six weeks of stalled cash flow while a single rejection cascades through operations. Stage redundancy from day one.

This article is editorial. We have affiliate relationships with several providers above — see the affiliate disclosure and editorial policy. Not tax, legal or financial advice — see the disclaimer.

Ready to open the account?

Relay is the realistic first application for most foreign-owned LLCs in 2026 — frequently approves where Mercury declines, no monthly fee, up to 20 sub-accounts under one entity, and clean integration with Stripe and QuickBooks. Soveraine readers go through our partner link, and your signup funds independent editorial.

Sources

- FinCEN MSB Registrant Search: https://www.fincen.gov/msb-registrant-search

- FDIC BankFind Suite: https://banks.data.fdic.gov/bankfind-suite/bankfind

- FDIC Deposit Insurance Coverage: https://www.fdic.gov/resources/deposit-insurance/

- FinCEN — Bank Secrecy Act overview: https://www.fincen.gov/resources/statutes-and-regulations/bank-secrecy-act

- FinCEN — Beneficial Ownership Information Reporting: https://www.fincen.gov/boi

- IRS — How to Apply for an EIN: https://www.irs.gov/businesses/small-businesses-self-employed/how-to-apply-for-an-ein

- IRS — About Form 5472: https://www.irs.gov/forms-pubs/about-form-5472

- Bank of America Small Business Checking: https://www.bankofamerica.com/smallbusiness/deposits/business-checking/