Wise Business is a multi-currency account aimed at companies and freelancers that move money across borders. It is not a bank, and the distinction matters more than the marketing suggests. This review covers what the account actually does, what it costs, who it suits by tax residency, and the reporting obligations that follow once you open one. It is written for three groups: US persons (citizens and green-card holders), EU tax residents, and readers resident outside both blocs. The same product behaves differently for each, mostly because of tax law rather than anything Wise controls.

Wise Business — Multi-currency business banking with lifetime affiliate cookie

What the Wise Business account is

Wise Business is a multi-currency account operated by Wise Payments Limited (UK, FCA-authorised as an Electronic Money Institution under reference 900507) and its regulated subsidiaries, including Wise US Inc., a FinCEN-registered Money Services Business. [source: FCA Register — Wise Payments Limited] [source: FinCEN MSB Registrant Search — Wise US Inc.]

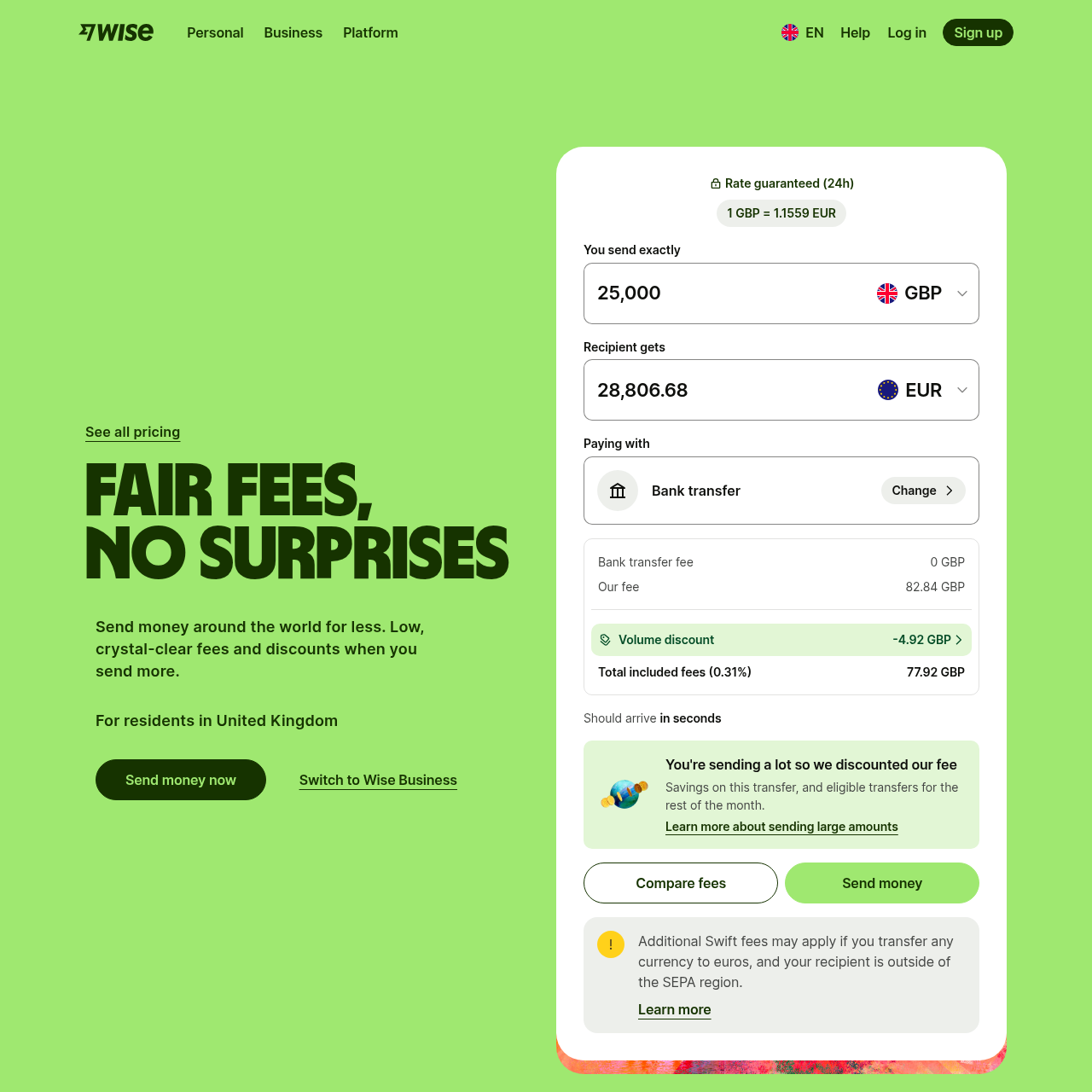

The account lets a business hold balances in 40+ currencies, receive payments via local account details in 8-10 currencies (USD ACH and wire, EUR IBAN, GBP sort code, AUD BSB, and others), send payments to 160+ countries at the mid-market FX rate plus a disclosed fee, and issue debit cards to team members. There is a one-time setup fee — $31 in the US as of May 2026 — and no monthly fee. [source: Wise US Business Pricing]

It is not a chartered bank. Balances are safeguarded in segregated accounts at partner banks rather than held on Wise's own balance sheet. In the US, this means Wise customer funds receive FDIC pass-through insurance up to $250,000 per customer at the partner bank, subject to the bank's standard limits — not the broader deposit protection a chartered bank offers directly. [source: Wise US — How your money is protected]

Who this applies to — by tax residency

The Wise Business product is the same everywhere it's offered. The tax and reporting consequences are not. Read the section that matches your status.

US persons (citizens and green-card holders)

A Wise Business account held by a US LLC, S-corp or C-corp is a domestic account if opened through Wise US Inc. with US business documentation. If you open an account through a foreign Wise entity tied to a non-US company, the account is a foreign financial account for FBAR purposes.

You must file FinCEN Form 114 (FBAR) if aggregate foreign account balances exceed $10,000 at any point in the calendar year. [source: FinCEN FBAR filing requirements] FATCA Form 8938 may also apply at higher thresholds. [source: IRS Form 8938 thresholds]

US citizens cannot escape US tax by routing income through a Wise account in another currency or country. Worldwide income is taxable under 26 U.S. Code § 61. If you own a foreign corporation that holds the Wise account, GILTI and Subpart F rules may apply. Talk to a CPA before structuring anything.

EU freelancers and digital nomads

For an EU tax resident running a sole proprietorship or company, a Wise Business account opened via Wise Europe SA (Belgium) is an EU account. It will be reported under the Common Reporting Standard and under DAC2 to your country of tax residence. [source: European Commission — DAC2 / Administrative cooperation]

Tax residence is determined by national rules — typically the 183-day test, plus "centre of vital interests" tests that override day-counting in many countries (France, Spain, Germany). A Wise account does not change your tax residence. If you move to Portugal, Estonia or Cyprus and continue to spend most of the year in your prior country, that prior country will likely still tax you.

CFC rules in most EU jurisdictions attribute the income of low-taxed foreign subsidiaries back to the resident shareholder. Holding the Wise account inside a Dubai or Hong Kong company while you live in Berlin does not solve the German tax problem. [source: EU Anti-Tax Avoidance Directive (ATAD) — Articles 7-8 CFC rules]

Non-US, non-EU readers

If you are tax-resident in a territorial-tax jurisdiction (Singapore, Hong Kong, UAE, Panama, Georgia, Malaysia under MM2H) or a country with weak CFC enforcement, the Wise Business account is the most flexible part of the picture. Local tax authorities receive CRS reports, but the underlying liability depends on whether the income is locally sourced.

A Singapore-resident consultant invoicing US clients via a Wise USD account, doing the work from Singapore, owes Singapore tax on the income — but Singapore's territorial system may exempt foreign-sourced income remitted under certain conditions. [source: IRAS — Taxable and non-taxable income] Confirm with a local tax advisor before assuming anything.

What it costs and how long it takes

Pricing varies by region. The numbers below are for the US product as of May 2026 and should be verified at Wise's pricing page before relying on them.

| Item | US Cost | Notes |

|---|---|---|

| Account opening | $31 one-time | Waived in some regions |

| Monthly fee | $0 | No minimum balance |

| Receive USD (ACH/wire) | Free | Local details included |

| Receive EUR/GBP/AUD/etc | Free | 8-10 currencies with local details |

| Send USD domestic ACH | From $1.74 | Varies by amount |

| Send international (EUR example) | 0.43% + fixed fee | Mid-market rate, no markup |

| Currency conversion | 0.43%-1% typical | Disclosed before each transfer |

| Debit card | $3 per card | Issued in USD |

| ATM withdrawal | $1.50 + 2% over $100/month | First $100/month free |

| Wise Interest (USD) | Up to 3.66% APY | Opt-in, US business eligibility varies |

Account opening timeline. Most verified businesses receive approval within 2-5 business days. Complex structures (multi-shareholder, non-resident directors, regulated industries) take 1-3 weeks and sometimes require additional documents: certificates of incorporation, beneficial ownership confirmation, source-of-funds statements. Crypto-adjacent businesses are frequently rejected.

If you're comparing alternatives: Wise Business competes most directly with Mercury (US-only, bank partnership model), Revolut Business (EU-strong), and Airwallex (Asia-Pacific strong). For most cross-border freelance and consulting work, Wise wins on FX cost transparency. For US-only operations needing credit, Mercury or a domestic bank is better. We have no affiliate relationship with Wise — links here are direct.

Common mistakes and how to avoid them

Treating Wise as a deposit account. Funds are safeguarded, not insured the same way as a chartered bank. Do not park more than your operating runway in a Wise balance. Use a bank for reserves.

Mismatching business registration and operator residence. If your company is incorporated in Estonia but you live in Spain and operate the business from a Madrid apartment, Spanish tax authorities will likely deem the company a Spanish tax resident under the place-of-effective-management test. Wise will open the account; the Spanish tax bill arrives later.

Ignoring 1099-K and CRS reports. Wise reports. If you receive payments through it, the IRS or your local tax authority already knows. File accordingly.

Assuming "non-resident" company structures hide ownership. Wise requires beneficial ownership disclosure for any individual holding 25% or more, in line with FinCEN's Beneficial Ownership Information rule and EU AML Directive 6. [source: FinCEN BOI Reporting] Anonymous structures will not pass onboarding.

Underestimating closure risk. Keep a backup account at a second provider. Account closures, while uncommon, are disruptive when they happen and recovery of held balances can take weeks.

When to consult a qualified professional

Before opening a Wise Business account tied to a non-resident company, before moving tax residence, and before any structure that involves a foreign company plus a foreign account, speak to:

- A tax advisor in your country of tax residence — for CFC, exit tax and reporting questions.

- A tax advisor in the country of company incorporation — for substance and local compliance.

- For US persons, a CPA familiar with international structures — GILTI, Subpart F, Form 5471 and FBAR are not optional.

A Wise account is a tool. The tax position around it is the thing that determines whether the setup is legal optimisation or an expensive mistake.

FAQ

Can I use Wise as a business bank account?

You can use Wise Business as your operating account for sending, receiving and holding money in 40+ currencies, but it is not a bank in the legal sense. In the US, Wise is a licensed money transmitter; in the UK it is an Electronic Money Institution authorised by the FCA. Balances are safeguarded in segregated accounts at partner banks, not protected by FDIC pass-through in the same way as a chartered bank deposit. For most freelancers and small companies operating cross-border, that is acceptable. For holding large reserves long-term, a chartered bank is safer.

Is Wise good for business accounts?

Wise is strong for cross-border payments, multi-currency receiving and low FX spread — its core pitch. It is weaker as a sole banking relationship: no overdraft, no business loans, no interest on most currencies (USD pays up to 3.66% APY via Wise Interest as of 2026, subject to eligibility), and limited integration with cash deposit. For an internet-first business that bills clients abroad, it is among the best available. For a brick-and-mortar business with payroll, suppliers and credit needs in one country, a domestic bank is still the better primary account.

Why is Wise closing accounts?

Wise closes accounts when verification fails, when activity does not match the declared business purpose, or when transactions trigger AML flags. Common triggers: receiving payments from sanctioned jurisdictions, sudden volume spikes without explanation, mismatch between the business country of registration and the operator's residence, or refusal to supply requested documents. Wise is required under EU Directive 2015/849 and US BSA rules to file Suspicious Activity Reports and to offboard customers it cannot risk-assess. Closure is rarely arbitrary — but the threshold is lower than at a traditional bank because the margins are thinner.

Is Wise legal in the USA?

Yes. Wise US Inc. is registered with FinCEN as a Money Services Business and licensed as a money transmitter in 49 states plus Puerto Rico and DC. It is publicly listed on the London Stock Exchange. Using Wise as a US person or US business is entirely legal. What is not legal is using any account — Wise or otherwise — to avoid US tax filing obligations. US citizens and green-card holders owe tax on worldwide income regardless of where the account sits, and FBAR (FinCEN Form 114) applies to foreign accounts above $10,000 aggregate.

What is the downside of Wise?

Three real downsides. First, it is not a bank — no deposit insurance in the conventional sense, no credit products, no relationship manager. Second, account closures happen with limited recourse; appeals are slow and outcomes opaque. Third, larger transfers can trigger compliance holds that freeze funds for days or weeks while documentation is reviewed. For a business that needs predictable access to operating capital, that uncertainty matters. The fee transparency and FX pricing are genuinely good — but they are not a substitute for a banking relationship if your business needs one.

Does Wise report to the IRS?

Yes, where required. Wise issues Form 1099-K to US account holders meeting the federal threshold (over $2,500 in 2025, dropping to $600 in 2026 under current IRS guidance — confirm with your tax advisor). It also complies with FATCA, meaning non-US Wise entities report US-person account holders to the IRS via their local tax authority. Wise cannot help you hide income from the IRS, and does not try to. For non-US persons, Wise reports under the OECD Common Reporting Standard to your country of tax residence.

This review is editorial. We have no affiliate relationship with Wise. See our affiliate disclosure and editorial policy for how we handle commercial relationships. Nothing here is tax or legal advice — see our disclaimer.

Ready to act on this?

Wise Business — Multi-currency business banking with lifetime affiliate cookie. Soveraine readers go to the front of the line through our partner link, and you fund independent editorial in the process.

Sources

- FCA Register — Wise Payments Limited: https://register.fca.org.uk/s/firm?id=001b000000MfFRyAAN

- FinCEN MSB Registrant Search: https://www.fincen.gov/msb-registrant-search

- Wise US Business Pricing: https://wise.com/us/pricing/business

- Wise US Customer Protection: https://wise.com/us/legal/customer-protection

- FinCEN — Report of Foreign Bank and Financial Accounts (FBAR): https://www.fincen.gov/report-foreign-bank-and-financial-accounts

- IRS — Summary of FATCA Reporting for U.S. Taxpayers: https://www.irs.gov/businesses/corporations/summary-of-fatca-reporting-for-u-s-taxpayers

- 26 U.S. Code § 61 — Gross income defined: https://www.law.cornell.edu/uscode/text/26/61

- European Commission — DAC2 administrative cooperation: https://taxation-customs.ec.europa.eu/dac2_en

- EU Anti-Tax Avoidance Directive (ATAD): https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32016L1164

- IRAS Singapore — Taxable and non-taxable income: https://www.iras.gov.sg/taxes/individual-income-tax/basics-of-individual-income-tax/what-is-taxable-what-is-not

- FinCEN — Beneficial Ownership Information Reporting: https://www.fincen.gov/boi