Modified adjusted gross income — MAGI — is one of the most important numbers in the US tax code that almost nobody can define on demand. It decides whether you can fund a Roth IRA, whether you owe the 3.8% investment-income surtax, what you pay for Medicare, and whether you qualify for health-insurance subsidies. The confusion is real and partly the IRS's fault: there is no single MAGI. This guide explains what MAGI is, how it differs from AGI, the add-backs that quietly raise it, and — crucially for our readers — why US expats who think the foreign earned income exclusion removed their income often discover it is still counted. Written for US persons.

Bright!Tax — US expat tax specialists who model MAGI correctly across FEIE, IRAs and the NIIT.

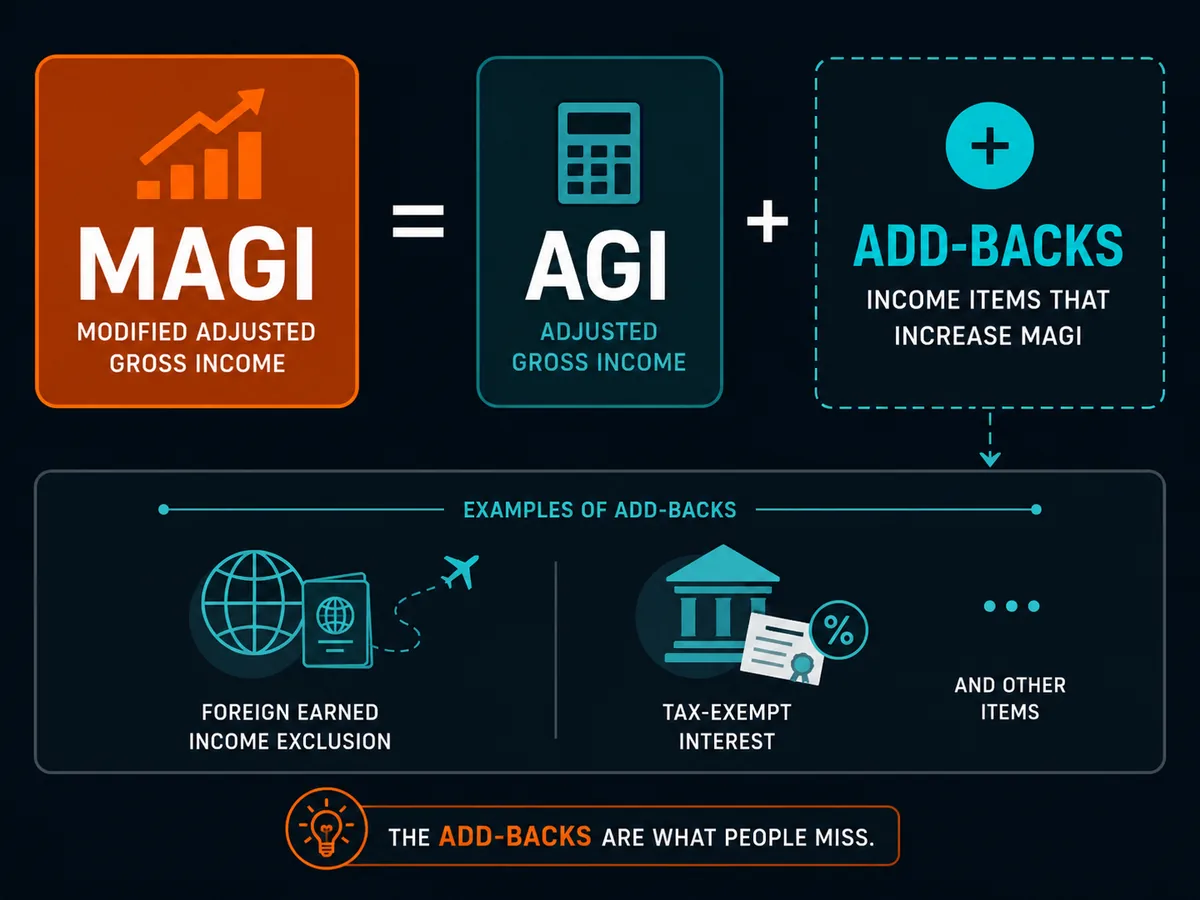

Start with AGI

Everything begins with adjusted gross income (AGI) — the figure on line 11 of Form 1040. AGI is your total income (wages, interest, dividends, business profit, capital gains) minus a set of "above-the-line" adjustments (deductible IRA contributions, the deductible half of self-employment tax, student loan interest, HSA contributions, and so on). It is a single, fixed number for the year.

MAGI takes that AGI and adds certain things back. That is the whole concept. The reason MAGI exists is that Congress wanted eligibility for various benefits to be measured on a broader income figure than AGI — one that does not let people qualify simply because they excluded or deducted income. So for each benefit, the law specifies which exclusions and deductions get added back.

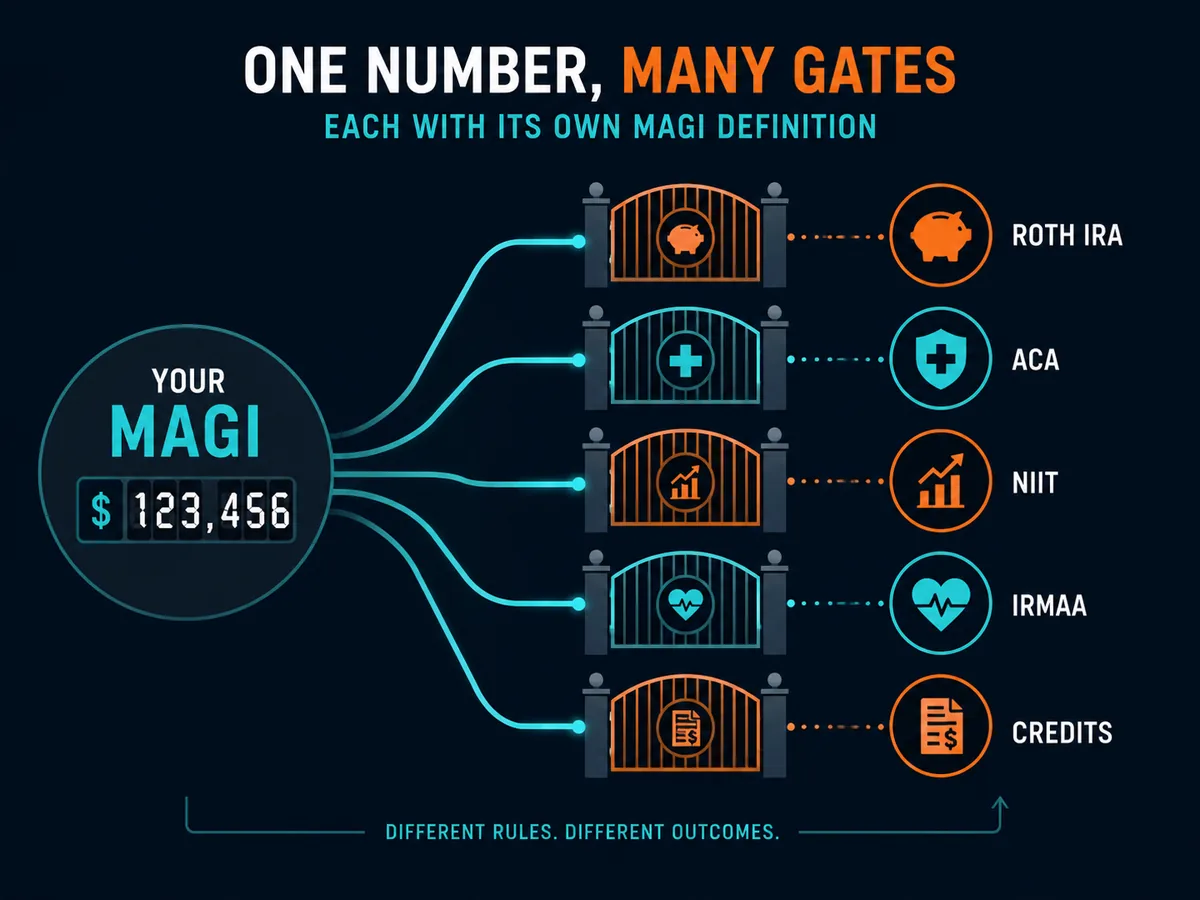

There is no single MAGI

This is the part that trips up even experienced filers. MAGI is purpose-specific. The add-backs differ depending on what you are testing:

- Roth IRA eligibility adds back the foreign earned income exclusion, foreign housing exclusion/deduction, the traditional-IRA deduction, the student loan interest deduction, and a few others.

- ACA premium tax credit adds back tax-exempt interest, excluded foreign earned income, and the non-taxable portion of Social Security benefits.

- Net Investment Income Tax (3.8%) adds back the foreign earned income exclusion to AGI.

- Medicare IRMAA surcharges use AGI plus tax-exempt interest (and look back two years).

So a single taxpayer can legitimately have three or four different MAGIs in the same year. Always use the worksheet in the specific IRS publication or form instructions for the benefit in question rather than a one-size formula.

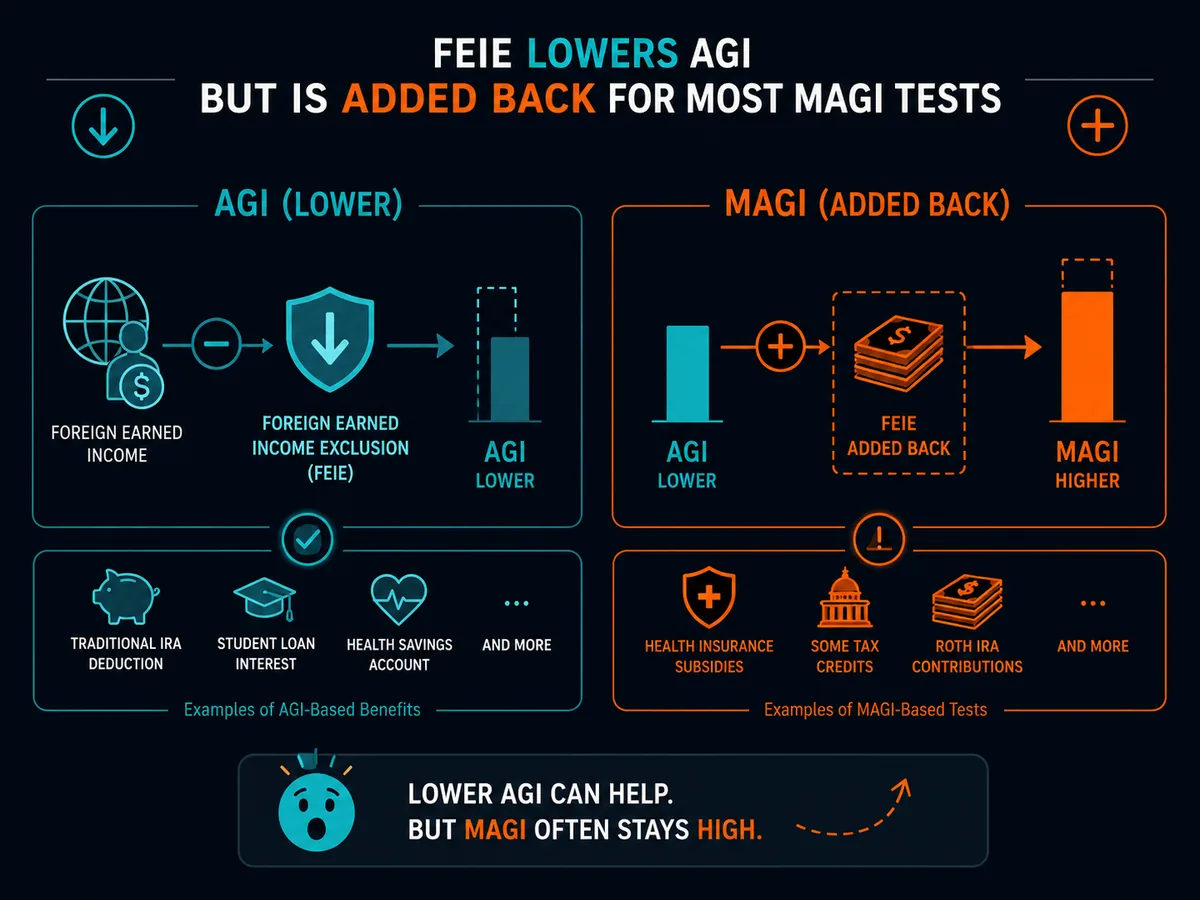

The expat trap: the FEIE comes back

For Soveraine's readers abroad, this is the headline. The Foreign Earned Income Exclusion lets you exclude foreign salary from taxable income, which lowers your AGI. But for most MAGI calculations, the excluded amount is added straight back.

The practical consequences:

- Roth IRA: an expat who excludes their entire salary under the FEIE may have little or no AGI — but because the FEIE is added back for Roth MAGI, they can be over the income limit and unable to contribute. Worse, with all earned income excluded, they may have no earned income left to contribute at all.

- Education and child credits: the added-back income can push the expat over phase-out thresholds they assumed they were under.

- Net Investment Income Tax: the FEIE add-back can expose investment income to the 3.8% surtax.

This is why many cross-border advisers steer high-earning expats toward the Foreign Tax Credit instead of the FEIE — the FTC does not exclude income, so it does not create the same MAGI add-back problem, and it preserves earned income for retirement contributions.

What MAGI controls

MAGI is the gatekeeper for a long list of provisions. The big ones:

- Roth IRA contributions — phased out above income limits.

- Traditional IRA deduction — limited if you (or a spouse) are covered by a workplace plan.

- ACA premium tax credit — health-insurance subsidies are calculated on household MAGI.

- Net Investment Income Tax — a 3.8% surtax on investment income above a MAGI threshold.

- Medicare IRMAA — higher Part B and Part D premiums above MAGI tiers, based on your return from two years prior.

- Child Tax Credit and education credits — phased out by MAGI.

- Student loan interest deduction — phased out by MAGI.

Because these thresholds are not all indexed the same way and some have steep "cliffs" (cross by a dollar, lose the whole benefit), MAGI planning near year-end can be worth real money.

How to calculate yours

- Find your AGI on line 11 of Form 1040.

- Identify which benefit you are testing (Roth IRA, ACA, NIIT, etc.).

- Pull the add-back list from that benefit's IRS worksheet — do not assume the add-backs are the same as another benefit's.

- Add those items back to AGI. The result is your MAGI for that purpose.

- Compare it to the relevant threshold for the tax year.

If you exclude foreign income, deduct student loan interest, hold municipal bonds, or contribute to an IRA, your MAGI will be meaningfully higher than your AGI — model it before you act, not after.

Common mistakes

Assuming MAGI equals AGI. For many people they differ by thousands of dollars once add-backs are applied.

Assuming the FEIE removes income for all purposes. It lowers AGI but is added back for most MAGI tests — the single most common expat error.

Using one MAGI everywhere. The Roth, ACA, NIIT and IRMAA definitions differ. Use the right worksheet.

Forgetting the IRMAA two-year lookback. A high-income year can raise your Medicare premiums two years later, after you have retired into a lower income.

When to consult a qualified professional

Get advice if: you are an expat deciding between the FEIE and the Foreign Tax Credit; your income is near a Roth, NIIT or IRMAA threshold; you hold significant investment income or municipal bonds; or you are planning Roth conversions and need to manage MAGI cliffs across years.

Soveraine is an editorial publication, not a tax firm. Read our editorial policy and disclaimer before acting on anything in this article.