The Foreign Earned Income Exclusion (FEIE) lets qualifying US citizens and resident aliens working abroad exclude a slice of their foreign salary from US federal income tax. For 2026 that slice is $132,900 per person. It is not a loophole, not a secret, and not a way to escape US tax filing — it is a statutory exclusion under Internal Revenue Code §911. This article explains who it applies to, when it beats the Foreign Tax Credit, and where readers most often trip over the rules. It is written for US persons. If you are not a US citizen or green-card holder, the FEIE does not apply to you — skip to the section below.

Bright!Tax — US expat tax filings (FBAR + FATCA + FEIE specialists)

What the foreign earned income exclusion actually is

The FEIE is an election. You file Form 2555 with your US tax return and exclude up to a capped amount of foreign-earned wages or self-employment income from your taxable income.

Key points the marketing pages tend to gloss over:

- It only covers earned income. Wages, salary, professional fees, self-employment net income. Not dividends, interest, capital gains, rental income, or pensions.

- It does not eliminate self-employment tax. Social Security (12.4%) and Medicare (2.9%) still apply unless a totalisation agreement with your country of residence says otherwise.

- It does not remove your filing obligation. US citizens file annually on worldwide income regardless of where they live. The FEIE reduces tax, not paperwork.

- It stacks with the housing exclusion. A separate calculation on Form 2555 lets you exclude qualifying foreign housing costs above a base amount.

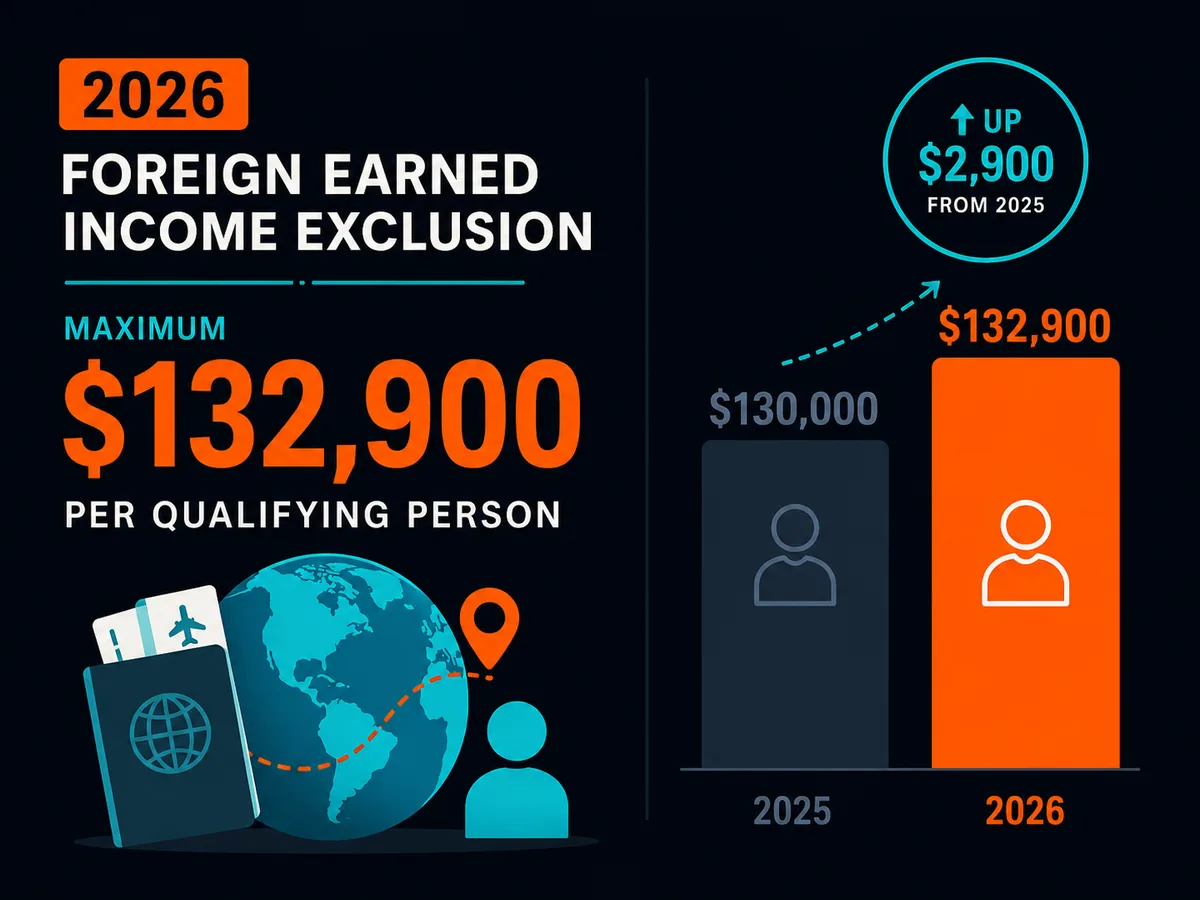

For tax year 2026, the maximum exclusion is $132,900 per qualifying person [source: TODO — IRS Rev. Proc. 2025-XX confirming 2026 inflation adjustment]. The 2025 figure was $130,000, per the IRS Figuring the FEIE page.

Who this applies to — by nationality

US persons (citizens and green-card holders)

The FEIE is built for you. The US is one of two countries on earth (the other is Eritrea) that taxes its citizens on worldwide income regardless of residence. The FEIE, the Foreign Tax Credit, and the foreign housing exclusion are the three main tools that prevent double taxation. None of them remove the filing obligation. The only way to fully end US worldwide taxation is renunciation — and that triggers its own exit tax under IRC §877A for "covered expatriates".

EU freelancers and digital nomads

The FEIE does not apply to you. If you are a French, German, Spanish or Italian tax resident, your home country taxes you on worldwide income — and applies its own residency tests (the 183-day rule, centre of vital interests, habitual abode). You may have access to your own country's foreign-income reliefs or expat regimes (Italy's impatriati, Portugal's old NHR scheme, Spain's Beckham law). Those are separate from the FEIE.

Non-US, non-EU readers

The FEIE is irrelevant to you. Most non-US jurisdictions tax on a residential or territorial basis, which means leaving the country generally ends the tax obligation. This is the reader segment for whom international tax planning works most cleanly — you simply do not have the citizenship-based taxation problem.

Who qualifies for the foreign earned income exclusion

Three requirements, all of which must be met:

- Tax home in a foreign country. Your regular place of business must be outside the US.

- Foreign earned income. Income earned for services performed while physically in a foreign country.

- Either the bona fide residence test or the physical presence test.

The bona fide residence test

You must be a bona fide resident of a foreign country (or countries) for an uninterrupted period that includes an entire tax year, per IRS guidance. This is qualitative — visa status, family ties, length of stay, and intent all weigh in. Short trips back to the US are allowed but you must intend to return to your foreign residence.

The physical presence test

You must be physically present in a foreign country (or countries) for at least 330 full days during any 12-month period. Full days mean midnight-to-midnight on foreign soil. Travel days that include US territory or international waters generally do not count. This is the cleaner test for digital nomads, but it is also where most claims fall apart in audit — see the physical presence test page.

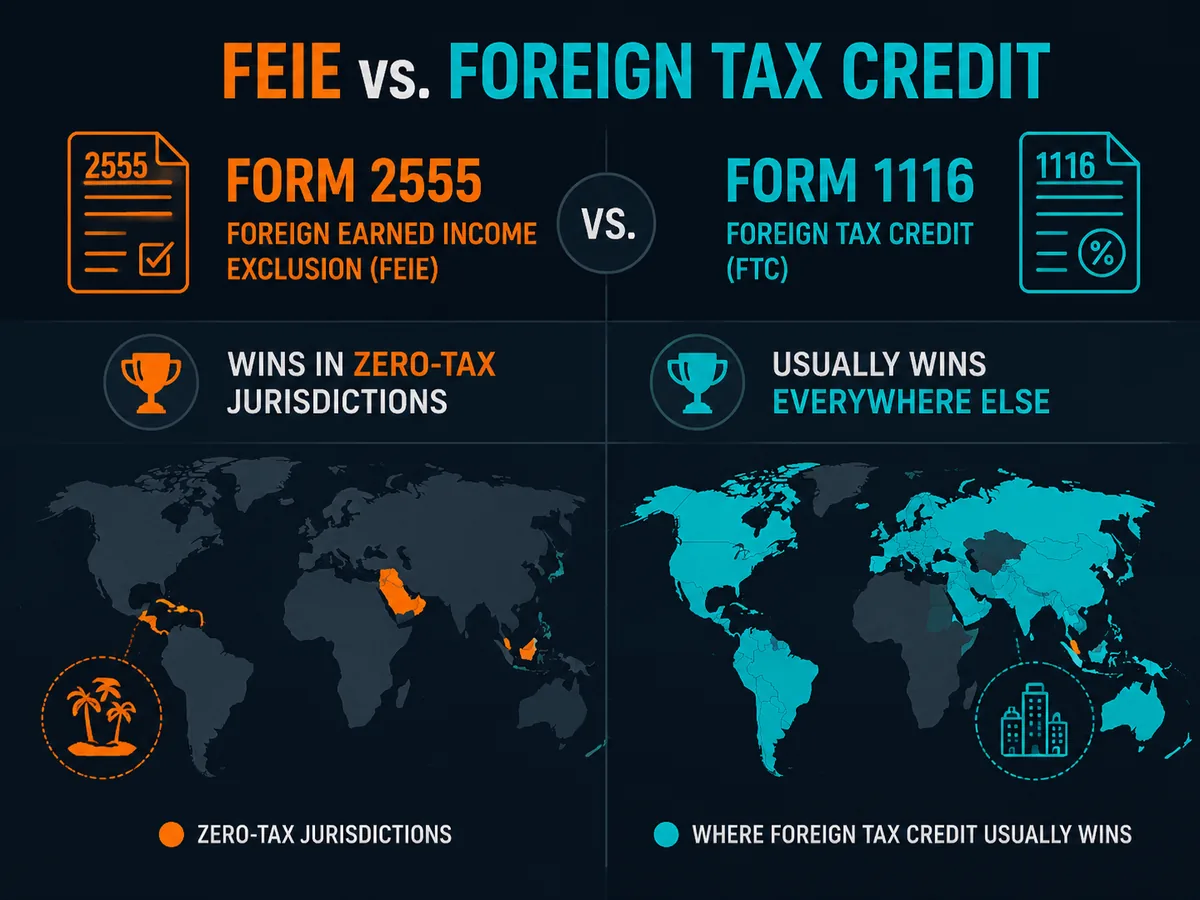

Should you file Form 2555 or Form 1116

This is the most consequential decision in expat tax planning, and the answer is not always the FEIE.

| Your situation | Better choice | Why |

|---|---|---|

| Live in a high-tax country (DE, FR, UK, NL) | Form 1116 (FTC) | Foreign tax already paid usually exceeds US tax owed; FTC generates carryforward credits |

| Live in a zero/low-tax country (UAE, Bahamas, Bermuda) | Form 2555 (FEIE) | No foreign tax to credit; exclusion is the only relief |

| Income above the FEIE cap in a high-tax country | Form 1116 on full amount | Avoids stacking-rule complications |

| Want to contribute to a traditional or Roth IRA | Form 1116 | FEIE-excluded income is not "compensation" for IRA purposes |

| Earning under $50k in a mid-tax country | Run both calculations | The answer depends on bracket interaction |

Once revoked, the FEIE election cannot be made again for five tax years without IRS consent (IRC §911(e)(2)). Treat the choice as semi-permanent.

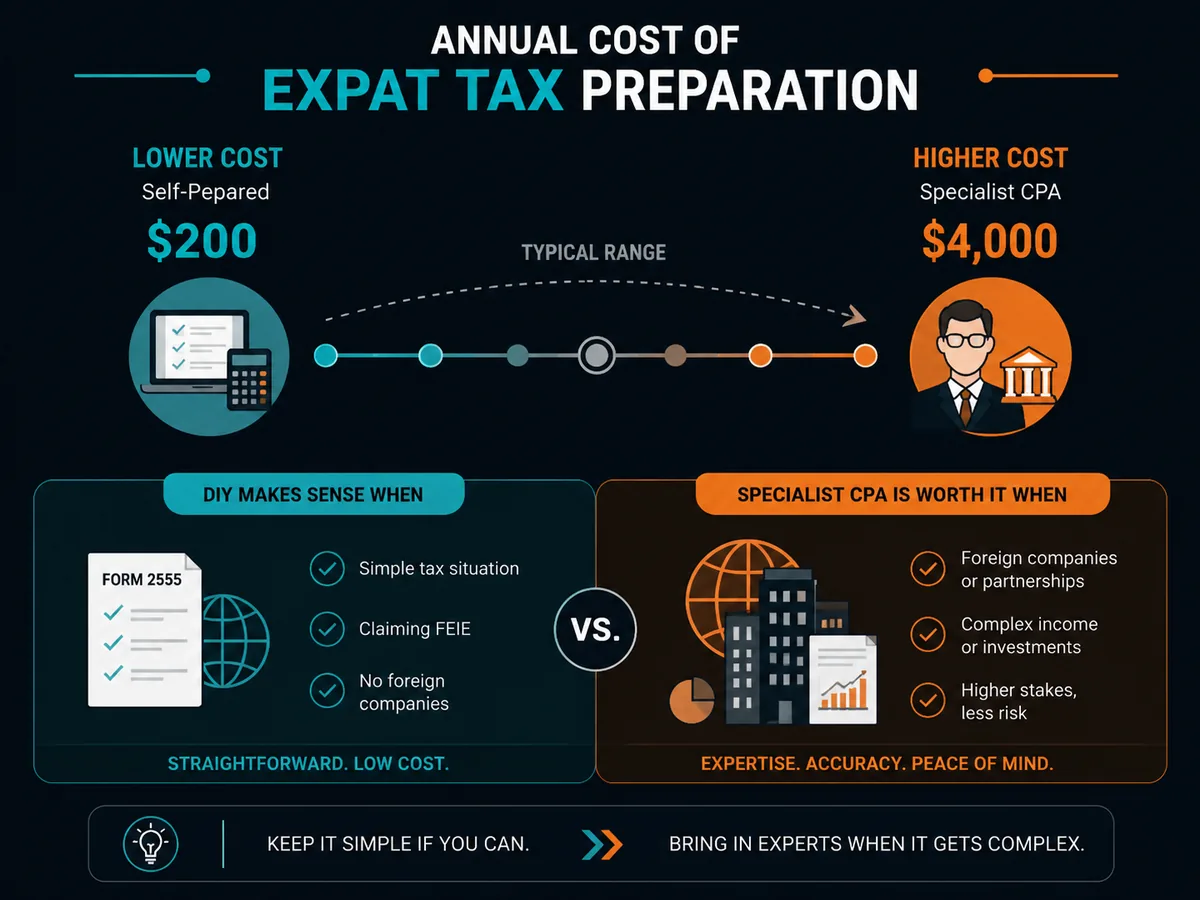

Realistic costs and timeline

| Item | Cost / time |

|---|---|

| Self-prepared Form 2555 via tax software | $50-200/year |

| Specialist expat CPA, simple return | $500-1,200/year |

| Specialist expat CPA, self-employed with foreign company | $1,500-4,000/year |

| Streamlined Filing Compliance Procedures (catch-up for non-filers) | $2,000-6,000 one-off |

| Time to qualify under physical presence test | 12 months (330 days) |

| Time to qualify under bona fide residence | One full tax year minimum |

Specialist expat preparers worth knowing about — listed editorially, no affiliate relationship: Greenback Expat Tax Services, Taxes for Expats, 1040 Abroad, Bright!Tax. Standard tax-software options like TaxSlayer and TurboTax both handle Form 2555 for straightforward situations.

Common mistakes and how to avoid them

Miscounting days. A "full day" abroad is 24 hours starting and ending in a foreign country. The day you leave the US does not count. The day you arrive back does not count. International flight time over US territory complicates things. Keep a spreadsheet with arrival and departure stamps.

Claiming the FEIE on the wrong income. Pensions, Social Security, dividends, interest, rental income, and capital gains are not eligible. Only earned income.

Forgetting FBAR and Form 8938. FinCEN Form 114 is due if your foreign accounts exceed $10,000 in aggregate at any point in the year. Form 8938 thresholds are higher and depend on filing status. Both are separate from your 1040.

Assuming an offshore company solves the problem. It does not. US persons who own foreign corporations face Controlled Foreign Corporation rules, Subpart F income, GILTI (Global Intangible Low-Taxed Income), and Forms 5471 and 8992. Incorporating in Dubai or the Caymans does not let a US citizen escape US tax filing. Anyone telling you otherwise is selling something.

Self-employment tax surprise. The FEIE excludes income from regular income tax, not from self-employment tax. A US freelancer in Thailand still owes 15.3% SE tax on net earnings, because Thailand has no totalisation agreement with the US.

When to consult a qualified professional

The FEIE looks simple on Form 2555. The interactions are not. Consult a US-licensed CPA or Enrolled Agent who specialises in expat returns if any of the following apply:

- You own equity in a foreign company or are self-employed through one.

- You have not filed US returns for one or more years while abroad (Streamlined Filing may apply).

- You moved partway through the tax year and need to allocate days across multiple tax homes.

- You are considering renunciation or have net worth above $2 million (covered expatriate threshold).

- You receive equity compensation (RSUs, ISOs) while abroad.

A second opinion from a tax professional in your country of residence is also worth the few hundred dollars. The two systems interact in ways that matter.

FAQ

Who qualifies for the foreign earned income exclusion?

You must be a US citizen or resident alien with a tax home in a foreign country, and you must pass either the bona fide residence test (resident of a foreign country for an uninterrupted tax year) or the physical presence test (330 full days in any 12-month period). Only earned income counts — wages, salary, self-employment income. Dividends, interest, pensions and capital gains are not eligible. You also have to file a US return and elect the FEIE on Form 2555.

What is the foreign earned income exclusion for 2026?

For tax year 2026, the maximum exclusion is $132,900 per qualifying person, up from $130,000 in 2025. Married couples where both spouses qualify can each claim the full amount, potentially excluding $265,800 of combined earned income. The figure is indexed to inflation and updated annually by the IRS in Revenue Procedure releases. The housing exclusion or deduction is calculated separately on top of the FEIE and varies by city.

Should I file Form 2555 or Form 1116?

It depends on the tax rate of your country of residence. If you live in a high-tax country (Germany, France, UK, most of Western Europe), Form 1116 — the Foreign Tax Credit — usually produces a better result and preserves your ability to contribute to an IRA. If you live in a low- or zero-tax country (UAE, Bahamas, parts of Southeast Asia), Form 2555 is generally better. You can use both in the same year, but not on the same dollar of income.

How does the IRS know if you have foreign income?

Through FATCA (Foreign Account Tax Compliance Act), foreign banks report US account holders directly to the IRS. Through FBAR (FinCEN Form 114), you self-report foreign accounts over $10,000 aggregate. Many countries also share tax information through the OECD Common Reporting Standard, though the US itself does not participate in CRS. Assume any foreign account in your name is visible to the IRS. Non-disclosure penalties are severe — up to $10,000 per non-willful FBAR violation.

What does foreign earned income exclusion mean on FAFSA?

FAFSA (the US federal student aid form) asks for excluded foreign income to be added back into the calculation of expected family contribution. Even though the FEIE removes the income from your taxable income on Form 1040, FAFSA treats it as available resources. Parents claiming the FEIE should expect their child's aid package to be calculated as if the excluded amount were ordinary income. This catches many expat families by surprise.

What are common mistakes with the FEIE?

Miscounting days for the physical presence test (travel days touching US territory often do not count); claiming the FEIE on income that is not earned (rental, dividends, pensions); failing to file FBAR and Form 8938 alongside the 1040; revoking the election and not realising you cannot re-elect for five years without IRS consent; assuming self-employment tax is excluded — it is not. SE tax still applies unless a totalisation agreement covers you.

Ready to act on this?

Bright!Tax — US expat tax filings (FBAR + FATCA + FEIE specialists). Soveraine readers go to the front of the line through our partner link, and you fund independent editorial in the process.

Sources

- Internal Revenue Code §911 — https://www.law.cornell.edu/uscode/text/26/911

- IRS, Foreign Earned Income Exclusion — https://www.irs.gov/individuals/international-taxpayers/foreign-earned-income-exclusion

- IRS, Figuring the Foreign Earned Income Exclusion — https://www.irs.gov/individuals/international-taxpayers/figuring-the-foreign-earned-income-exclusion

- IRS, Bona Fide Residence Test — https://www.irs.gov/individuals/international-taxpayers/foreign-earned-income-exclusion-bona-fide-residence-test

- IRS, Physical Presence Test — https://www.irs.gov/individuals/international-taxpayers/foreign-earned-income-exclusion-physical-presence-test

- IRS, About Form 2555 — https://www.irs.gov/forms-pubs/about-form-2555

- IRS, About Form 8938 — https://www.irs.gov/forms-pubs/about-form-8938

- IRS, Controlled Foreign Corporation FAQs — https://www.irs.gov/businesses/international-businesses/controlled-foreign-corporation-cfc-frequently-asked-questions

- IRS, Expatriation Tax (IRC §877A) — https://www.irs.gov/individuals/international-taxpayers/expatriation-tax

- SSA, Totalisation Agreements — https://www.ssa.gov/international/agreements_overview.html

- FinCEN BSA E-Filing (FBAR) — https://bsaefiling.fincen.treas.gov/main.html