A "0% tax residency" is one of the most-searched and most-misrepresented phrases in international tax. The accurate version is narrower than the headline. A handful of countries levy no personal income tax. A larger group taxes only locally sourced income. Almost none of them release a US citizen from US tax, and very few release a European resident from their home country's claim without an aggressive break in ties. This guide covers the five residencies that most often appear in the conversation — Paraguay, Georgia, the United Arab Emirates, Panama and Thailand — with primary sources, real costs and the catches a brochure will not mention. It is written for three audiences in parallel: US persons, EU residents and freelancers, and readers based in the rest of the world.

Bright!Tax — US expat tax filings (FBAR + FATCA + FEIE specialists)

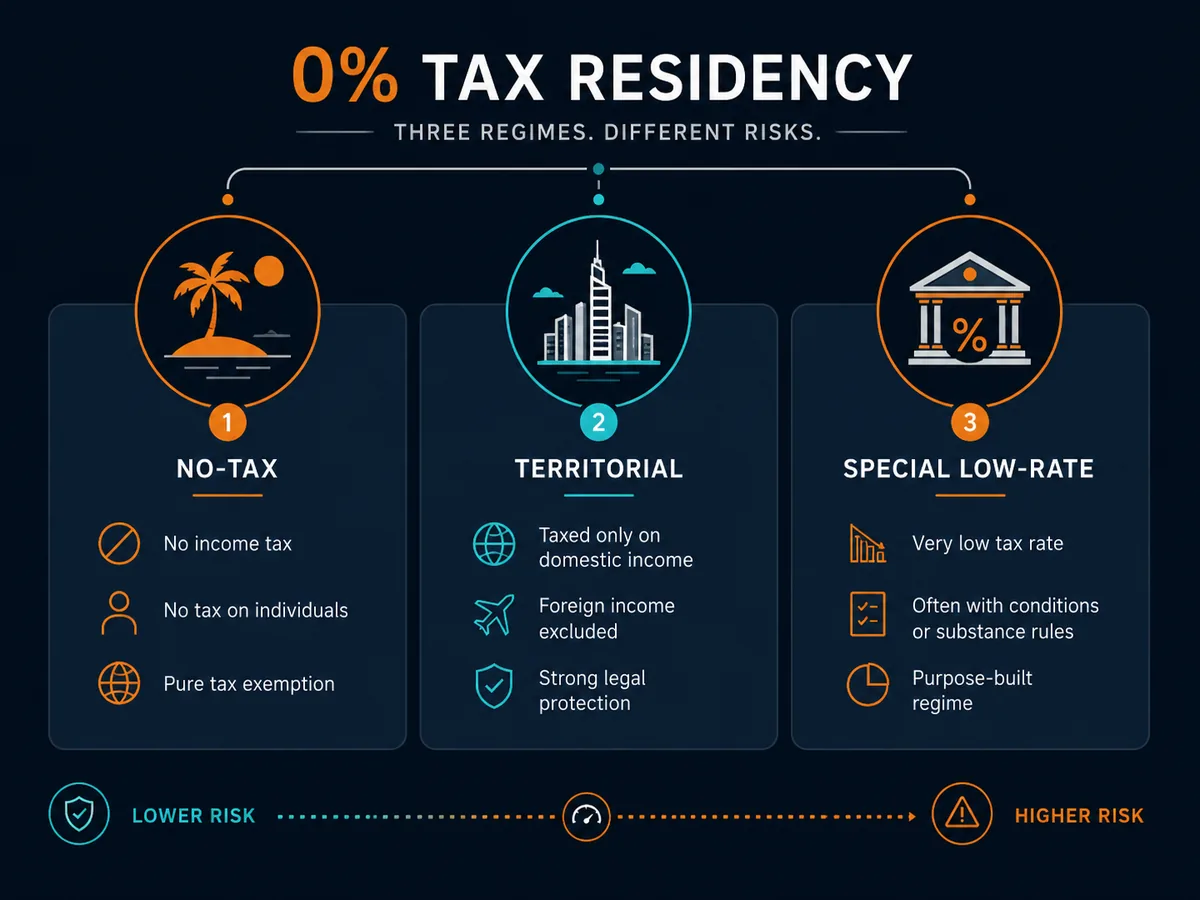

What "0% tax residency" actually means

The phrase collapses three very different ideas into one. Pulling them apart is the precondition for any sensible planning.

No personal income tax at all. A small group of jurisdictions levy zero personal income tax on wages, self-employment income and most investment income. The six Gulf Cooperation Council states fall here — the United Arab Emirates, Bahrain, Kuwait, Oman, Qatar and Saudi Arabia — along with the Bahamas, Bermuda, the Cayman Islands, Monaco, Vanuatu and Brunei (PwC Worldwide Tax Summaries: UAE individual taxes, PwC: Bahamas). In several of these, a corporate-level tax still applies above thresholds — the UAE introduced a 9% corporate tax on business profits above AED 375,000 from June 2023 under Federal Decree-Law No. 47 of 2022.

Territorial taxation. A larger group taxes local-source income at normal rates but exempts foreign-source income entirely. Paraguay, Panama, Costa Rica, Malaysia and Hong Kong apply variants of this. For a person whose income comes from foreign clients into a foreign company, the local effective rate on that foreign income is 0% even though the country is not a "no income tax" jurisdiction (Hong Kong Inland Revenue: territorial source principle).

Special low-rate regimes. A third group taxes residents but at flat low rates or under preferential micro-business regimes. Georgia's 1% individual entrepreneur regime on revenue up to GEL 500,000 (roughly USD 185,000 at June 2026 rates) is the canonical example — there is no 0% headline, but for an in-scope solo founder the bill is small enough to be functionally close (Revenue Service of Georgia: small business status).

A "0%" headline is honest only when the writer is clear which of these three is at work and which country owns the right to tax the rest of the person's economic life.

Who this applies to — read this first

The relevance of every country below changes sharply depending on the passport you hold and the country that currently claims you as a tax resident.

US persons

For US citizens and green-card holders, none of these residencies stops the US filing obligation. The US taxes its citizens on worldwide income regardless of residence under IRC §1 and IRC §61. What a foreign residency unlocks is the foreign earned income exclusion of up to $130,000 for tax year 2025 (IRS Rev. Proc. 2024-40), the foreign housing exclusion, and foreign tax credits for any local tax paid. None of those eliminate self-employment tax, GILTI exposure on a controlled foreign corporation under IRC §951A, passive income tax above the cap, or the FBAR and FATCA reporting obligations. A US person planning to use a UAE or Paraguay residency to claim the FEIE should engage a specialist filer before the move — Bright!Tax, Greenback and MyExpatTaxes are the most cited.

EU freelancers and digital nomads

For an EU citizen who is currently a tax resident of an EU member state, picking up a Paraguayan cédula or a UAE Emirates ID does nothing on its own. The home state's tax claim survives until residency there is genuinely severed under that state's domestic rules and, where relevant, under an OECD Model Tax Convention Article 4 tiebreaker (OECD MTC Article 4). Several states impose an exit tax on unrealised capital gains for departing residents — Spain under Article 95 bis of the Personal Income Tax Law, the Netherlands' conserverende aanslag on substantial shareholdings, France's IRC Article 167 bis. A second-residency without a clean exit from the first is not a tax plan; it is double exposure waiting to be discovered.

Non-US, non-EU readers

Readers based outside the US and EU generally face a simpler picture, because most home jurisdictions tax on residence rather than citizenship and accept a clean break when residence is shifted. The risk concentrates around CFC rules in the home country (notably for UK, Australian, Canadian and South African nationals), exit taxes, and the increasingly common requirement to produce a foreign tax residency certificate before bank or broker accounts are released. The five residencies below are most accessible to this segment.

The five residencies

Paraguay

Paraguay operates a territorial tax system — only Paraguayan-source income is taxed. Foreign-source income earned by a tax resident is not subject to the personal income tax of 10%. For an online freelancer or e-commerce operator invoicing foreign clients into a non-Paraguayan company, the effective Paraguayan rate on that foreign income is zero.

The residency route is the friendliest in the region. Under the Migrations Law administered by the Dirección General de Migraciones, applicants attend in person in Asunción, file a short document set (criminal record check, birth certificate, proof of means) and are issued a temporary residency. The cédula de identidad typically follows within a few months. There is no minimum-stay requirement to maintain the residency itself.

Becoming a tax resident is not automatic from holding the cédula. The Paraguayan tax authority SET treats tax residency as a question of being present and registered for tax purposes — typically demonstrated by either physical presence of more than 120 days or a registered local economic activity. A bare cédula without registration may not produce the residency certificate other countries demand.

Total cost through a local agent is usually USD 2,000 to USD 4,000. After two years on temporary residency the holder can convert to permanent residency for up to 10 years.

The gotcha. Paraguay has a thin treaty network — fewer than ten double tax agreements in force (IBFD: Paraguay treaty list) — so any tiebreaker dispute with a higher-tax home country is resolved under that country's domestic law, not a treaty. A French or German exit from tax residency to Paraguay is brittle if the person spends most of their year somewhere else.

Georgia

Georgia combines visa-free entry for 365 days for over 90 nationalities (Ministry of Foreign Affairs of Georgia: visa policy) with a 1% turnover tax for registered solo operators.

The mechanism is "small business status," granted to an individual entrepreneur registered with the Revenue Service. Annual turnover up to GEL 500,000 (about USD 185,000) is taxed at 1%; turnover above is taxed at 3% on the excess until the status is revoked. Registration costs around GEL 100 and is completed in one working day. Filings are monthly turnover declarations.

Becoming a Georgian tax resident requires 183 days of physical presence in any rolling 12-month period under Article 34 of the Tax Code of Georgia. A separate high-net-worth resident status is available without day requirements for individuals with property worth more than GEL 3 million or qualifying income history.

Banking is solid by regional standards. Bank of Georgia and TBC Bank both work with non-residents, both maintain English-language platforms, and both have been historically more flexible on crypto-derived inflows than most European institutions.

The gotcha. The 1% rate applies to gross turnover, not net profit, and is limited to active business income — passive investment income, dividends and royalties are taxed under the standard personal income tax of 20%. The small-business regime also excludes certain professional services such as legal, medical and consultancy work in some interpretations; written clarification from the Revenue Service before registration is worth the half-hour.

United Arab Emirates

The UAE is the most familiar of the five and the most expensive. Personal income tax remains at 0% under Federal Tax Authority guidance, but a 5% VAT applies and a 9% federal corporate tax took effect for financial years starting on or after 1 June 2023 on business profits above AED 375,000, under Federal Decree-Law No. 47 of 2022. Small business relief is available for revenue up to AED 3 million per year under Ministerial Decision No. 73 of 2023.

The standard route is incorporation in one of the 40-plus free zones (SPC Free Zone, IFZA, RAKEZ, Meydan, DMCC) followed by an investor visa, medical test, biometrics and Emirates ID issuance in person. A local partner such as SPC Free Zone handles formation and immigration together. Setup runs USD 5,000 to USD 12,000 in year one and USD 4,000 to USD 6,000 in annual renewals.

Tax residency for individuals is governed by Cabinet Decision No. 85 of 2022. An individual qualifies if their principal place of residence and centre of financial and personal interests is in the UAE, or they were physically present for 183 days in a 12-month period, or — critically — for 90 days if they are a UAE/GCC national or hold valid UAE residence with a permanent place of residence or business in the country. The 90-day route is the workhorse for the free-zone-licensed founder. To keep an investor visa active the holder must not be outside the country for more than six consecutive months (UAE GDRFA).

Banking is the second reason to pick the UAE. Emirates NBD, Mashreq, ADCB and the regional branch networks accept multi-currency accounts and integrate with international payment processors without the correspondent-banking trust deficit that affects Paraguayan and Panamanian institutions.

The gotcha. The 9% corporate tax on profit above AED 375,000 is not avoided by clever salary structures alone — the transfer pricing rules applied since 2024 cap "reasonable" owner remuneration. Free-zone qualifying income remains at 0% only where the substance test under Article 18 of the Decree-Law is met, which requires real activity in the zone and excludes mainland-customer income in many cases.

Panama

Panama uses the same territorial principle as Paraguay but adds USD-denominated banking and a city built around international business. Local-source income is taxed at progressive rates up to 25% above USD 50,000; foreign-source income is not taxed for residents under Article 694 of the Fiscal Code administered by the Dirección General de Ingresos.

The dominant route is the Friendly Nations Visa introduced in 2012 and reformed in 2021, available to nationals of around 50 countries. The 2021 reform replaced the old "open a bank account and incorporate" path with three substantive routes: a job offer from a Panamanian employer, real estate purchase of at least USD 200,000, or a fixed-term bank deposit of at least USD 200,000. Application costs through a local attorney run USD 5,000 to USD 8,000 plus the qualifying investment.

Initial residency is granted for two years, then permanent residency may be applied for. Naturalisation is possible after five years of permanent residency with continuous presence and an integration exam. The 180-day annual presence requirement for tax residency is set in Article 762-N of the Fiscal Code.

Banking is the practical reason to choose Panama over Paraguay. Banco General, Banistmo, Multibank and Global Bank work routinely with international clients, accounts are USD-denominated by default, and correspondent banking relationships into the US system remain intact.

The gotcha. The 2021 visa reform raised the entry bar significantly and the temporary-to-permanent conversion now requires demonstrable continued connection to Panama. Panama also appears periodically on the EU list of non-cooperative jurisdictions, which can trigger defensive measures by EU banks and tax authorities on payments to Panamanian counterparties.

Thailand

Thailand operates a remittance-based system. A tax resident — anyone present 180 days or more in a calendar year under Section 41 of the Revenue Code — is taxed on Thai-source income at progressive rates to 35%, and on foreign-source income only to the extent it is remitted into Thailand.

The structure changed materially in 2024. Under Departmental Instruction No. Paw 161/2566, foreign-source income earned from 1 January 2024 onwards is taxable when remitted in any tax year, closing the old "wait one calendar year, remit tax-free" reading.

The remaining structure that works pairs Thai personal residency with a foreign company. A Hong Kong, Singapore or US LLC owns the operating business and retains profits offshore; the founder lives in Thailand on a Long-Term Resident visa or a retirement visa. Only funds remitted to Thai bank accounts for living expenses are taxable. On a USD 24,000 annual remittance the personal income tax under the progressive schedule is in the order of THB 35,000 to THB 50,000 — under USD 1,500 — with the balance accumulating outside the Thai tax net.

The Long-Term Resident visa, introduced in 2022 under the Board of Investment, grants a 10-year stay and a flat 17% personal income tax rate for highly skilled professionals, plus reduced reporting burdens for wealthy global citizens and pensioners.

The gotcha. Thailand has CFC-style anti-avoidance powers under Section 76 bis of the Revenue Code for companies "carrying on business in Thailand." Running an offshore company from a desk in Chiang Mai with Thai employees creates exactly the substance that rule targets. The structure also assumes the foreign company is genuinely resident in its place of incorporation — using a Hong Kong company with no Hong Kong substance is increasingly viewed unfavourably by both Hong Kong's Inland Revenue Department and Thai authorities.

Comparison table

| Country | Headline rate | Days required | Setup cost | Tax-residency certificate? | Best for |

|---|---|---|---|---|---|

| Paraguay | 0% on foreign income (territorial) | None for residency; 120+ for tax residency in practice | USD 2,000 – 4,000 | Available with active SET registration | Travellers who need a paper home and do not need a strong treaty network |

| Georgia | 1% on turnover up to GEL 500,000 | 183 days | USD 100 – 500 | Issued by Revenue Service for tax residents | Solo freelancers and consultants under USD 185k revenue |

| UAE | 0% personal, 9% corporate above AED 375k | 90 with local home/business, otherwise 183 | USD 5,000 – 12,000 + USD 4–6k annual | Issued by FTA after meeting Cabinet Decision 85 criteria | Founders who want banking quality and a livable base |

| Panama | 0% on foreign income (territorial) | 180 days | USD 5,000 – 8,000 + USD 200k investment | Issued by DGI for tax residents | USD banking, Latin American hub, citizenship in 5 years |

| Thailand | 0% on un-remitted foreign income | 180 days | USD 2,000 – 6,000 (LTR or retirement) | Issued by Revenue Department | Long-term Asia base willing to manage remittance discipline |

Sources: PwC Worldwide Tax Summaries, Revenue Service of Georgia, UAE Federal Tax Authority, Dirección General de Ingresos de Panamá, Thai Revenue Department.

Why "go where you're treated best" doesn't mean go anywhere with 0%

The phrase that drives most of this category — "go where you're treated best" — is sound advice with a misread tail. The misread is to assume that a 0% jurisdiction is automatically a treaty-defensible result. It is not.

The OECD tiebreaker. Where two countries both claim the same person, the OECD Model Tax Convention Article 4(2) applies a sequential test — permanent home, centre of vital interests, habitual abode, nationality, mutual agreement. A French national with an apartment in Paris, a wife and children in France, and a Paraguayan cédula will lose the tiebreaker to France. Paraguay's lack of a France treaty makes the result worse, not better.

Substance over form. Home-state CFC rules and OECD BEPS Action 6 reduce the value of bare corporate residency (OECD BEPS Action 6). A UAE free-zone company with no employees and one director who lives in Berlin is increasingly characterised as German-resident under Außensteuergesetz §8 and the German place-of-management rule.

The Common Reporting Standard. Every country covered here except the United States participates in the CRS and reports foreign tax residents' account balances to their home country annually. A French resident with a UAE bank account does not have privacy from France.

Exit before entry. A clean break from the old residency is at least as important as the new one — cross-border advisors at Henley & Partners and La Vida repeat this constantly. Deregister, sell or rent the family home at arm's length, move spouse and dependents, close domestic accounts, document the move, pay any exit tax owed.

The promise of "0% tax" is real for someone who has built the substance to defend it. Multi-currency banking and nomad-grade health insurance are tools that make the substance easier; they are not substitutes for it.

Final CTA

Ready to act on this?

Bright!Tax — US expat tax filings (FBAR + FATCA + FEIE specialists). For US persons exploring any of the five residencies above, the US filing obligation does not pause; Soveraine readers go to the front of the line through our partner link, and you fund independent editorial in the process.

Sources

- PwC Worldwide Tax Summaries — UAE individual taxes. https://taxsummaries.pwc.com/united-arab-emirates/individual/taxes-on-personal-income

- UAE Ministry of Finance — Corporate Tax. https://mof.gov.ae/corporate-tax/

- UAE Federal Tax Authority. https://tax.gov.ae/en/

- UAE Cabinet Decision No. 85 of 2022 — Tax residency for natural persons. https://mof.gov.ae/

- Revenue Service of Georgia — Small business status. https://www.rs.ge/Default.aspx?TabID=494&lang=en-US

- Tax Code of Georgia. https://matsne.gov.ge/en/document/view/1043717

- Dirección General de Ingresos de Panamá. https://www.dgi.gob.pa/

- Servicio Nacional de Migración de Panamá. https://www.migracion.gob.pa/

- Thai Revenue Department — Departmental Instruction No. Paw 161/2566. https://www.rd.go.th/english/

- Thailand Board of Investment — Long-Term Resident visa. https://www.boi.go.th/

- Paraguay Subsecretaría de Estado de Tributación. https://www.set.gov.py/

- Paraguay Dirección General de Migraciones. https://www.migraciones.gov.py/

- Hong Kong Inland Revenue Department — Territorial source principle. https://www.ird.gov.hk/eng/paf/bus_pft_tsp.htm

- OECD Model Tax Convention on Income and on Capital. https://www.oecd.org/tax/treaties/model-tax-convention-on-income-and-on-capital-condensed-version-20745419.htm

- OECD Common Reporting Standard. https://www.oecd.org/tax/automatic-exchange/

- OECD BEPS Action 6. https://www.oecd.org/tax/beps/beps-actions/action6/

- EU list of non-cooperative jurisdictions for tax purposes. https://www.consilium.europa.eu/en/policies/eu-list-of-non-cooperative-jurisdictions/

- IRS Rev. Proc. 2024-40 — Annual inflation adjustments. https://www.irs.gov/pub/irs-drop/rp-24-40.pdf

- IRC §911 — Citizens or residents of the United States living abroad. https://www.law.cornell.edu/uscode/text/26/911

- IRC §951A — Global intangible low-taxed income. https://www.law.cornell.edu/uscode/text/26/951A