Dubai's reputation as a tax haven is half-right and half-marketing. There is no personal income tax, no capital gains tax and no inheritance tax. There is also a 9% federal corporate tax, a 5% VAT, a municipal rent fee, property transfer charges and — for Americans — a US tax return that follows you wherever you go. This guide explains exactly what taxes apply in Dubai in 2026, who they apply to, and how the answer differs depending on whether you hold a US, EU or other passport. It is informational, not advice. Tax positions on residency, corporate structure and reporting should be confirmed with a qualified professional in both your home and target jurisdictions.

SPC Free Zone (Sharjah) — UAE free-zone formation with a public referral programme

What "taxes in Dubai" actually means

Dubai is one of seven emirates of the United Arab Emirates. Most taxes are set at the federal UAE level — VAT, corporate tax, excise duties — and apply identically in Dubai and Abu Dhabi. A few charges are emirate-specific: Dubai levies a 5% municipality fee on residential rent and a 4% property transfer fee through the Dubai Land Department, while Abu Dhabi structures its housing fee differently.

The headline most people quote — 0% personal income tax — is correct and is confirmed by the UAE government's official portal and PwC's UAE individual tax summary. There is no income tax law for individuals at all. No filing, no return, no PAYE.

That does not mean tax-free. It means the tax burden is shifted onto consumption, business profit and specific transactions, and — critically — it does not override the tax obligations imposed on you by your country of citizenship or prior residence.

Who this applies to

The rest of this guide assumes you are physically relocating to Dubai or already live there. The tax outcome depends almost entirely on the passport you hold.

US persons

US citizens and green card holders are taxed on worldwide income regardless of where they live. Moving to Dubai removes the local income tax bill — there was never one — but the IRS return continues. The Foreign Earned Income Exclusion (IRS Publication 54) excludes up to USD 126,500 of earned income for 2024 (indexed annually), provided you meet either the bona fide residence or physical presence test. FBAR (FinCEN Form 114) is required if your aggregate foreign accounts exceed USD 10,000 at any point in the year, and FATCA Form 8938 thresholds apply on top.

If you own a UAE company, Subpart F and GILTI under the Tax Cuts and Jobs Act may pull profits into your US return whether you take them as dividends or not. Form 5471 is mandatory for US owners of foreign corporations. There is no US–UAE tax treaty to soften any of this.

EU freelancers and digital nomads

EU tax residency is not severed by buying a plane ticket. Most member states apply a combination of the 183-day rule, centre of vital interests, habitual abode and nationality tie-breakers under the OECD Model Convention, which most EU bilateral treaties follow. France, Spain, Germany, the Netherlands and Italy all run residency tests that look at where your family lives, where your home is available to you and where your economic interests sit.

Several EU states apply exit taxes on unrealised capital gains when you formally leave — Germany's Wegzugsteuer under §6 AStG and France's exit tax under Article 167 bis CGI are the most cited. CFC rules under the EU's Anti-Tax Avoidance Directive (ATAD, Directive 2016/1164) require many member states to attribute the profits of low-taxed foreign subsidiaries — including UAE companies taxed at 0% or 9% — back to controlling EU shareholders.

In short: moving to Dubai works for EU nationals, but only if you do the paperwork to actually leave, dissolve your home-country economic ties, and structure ownership so CFC rules do not snap your UAE company's profits back.

Non-US, non-EU readers

UK, Australian, Canadian, South African, Indian and most Asian nationals face the cleanest version of the move. The UK's statutory residence test (HMRC RDR3) and similar rules in Australia and Canada provide clear paths to non-resident status. Once non-resident, foreign-source income generally falls outside the home tax net.

CFC enforcement varies. The UK has Controlled Foreign Companies legislation but applies it more narrowly than the EU's ATAD. Australia, Canada and New Zealand have their own attribution rules. Most other countries either have weak CFC rules or no enforcement infrastructure.

This is the segment for whom Dubai's 0% personal income tax delivers what it advertises.

Overview of UAE taxes

| Tax | Rate | Who pays | Source |

|---|---|---|---|

| Personal income tax | 0% | Nobody | u.ae |

| Capital gains tax (individuals) | 0% | Nobody | PwC UAE |

| Inheritance / estate tax | 0% | Nobody | PwC UAE |

| VAT | 5% | Consumers on most goods/services | Federal Tax Authority |

| Corporate tax | 9% above AED 375,000 profit | Businesses (mainland; some free zone exceptions) | Federal Decree-Law No. 47 of 2022 |

| Excise tax | 50% sugary drinks, 100% tobacco/energy drinks | Manufacturers/importers, passed to consumers | Federal Tax Authority |

| Dubai municipality housing fee | 5% of annual rent | Residential tenants, billed via DEWA | [source: TODO — Dubai Municipality housing fee official page] |

| Property transfer fee | 4% | Property buyers (Dubai) | [source: TODO — Dubai Land Department fee schedule] |

| Tourism dirham | AED 7–20 per room per night | Hotel guests | [source: TODO — Department of Economy and Tourism Dubai] |

Who is considered a resident of the UAE

UAE tax residency for individuals is defined by Cabinet Decision No. 85 of 2022, effective from March 2023. An individual is a UAE tax resident if any of the following apply:

- Their usual or primary place of residence and centre of financial and personal interests is the UAE.

- They were physically present in the UAE for 183 days or more in a 12-month period.

- They were physically present for 90 days or more in a 12-month period and hold UAE nationality, a valid residence permit or GCC nationality, and have a permanent place of residence or employment/business in the UAE.

A UAE Tax Residency Certificate can be requested from the Federal Tax Authority and is the document foreign tax authorities will ask for if you claim treaty relief or want to demonstrate the break from prior residency. The certificate matters more for your home country than for the UAE itself — the UAE does not need to confirm your residency to tax you, because it does not tax your income.

Is the UAE tax-free for foreigners

For individuals, yes — on personal income, capital gains, inheritance and net worth. There is no distinction between citizens and foreigners on these heads, because none of them are taxed for anyone. Foreigners cannot become UAE citizens through ordinary routes, so practically every individual paying (or not paying) tax in Dubai is a foreign national on a residence visa.

For businesses, "tax-free" stopped being accurate on 1 June 2023, when the federal corporate tax took effect under Federal Decree-Law No. 47 of 2022. The headline rate is 9% on taxable profit above AED 375,000 (roughly USD 102,000). Below that threshold, the rate is 0%.

Free zone entities can still access a 0% rate on Qualifying Income if they meet the conditions of a Qualifying Free Zone Person — adequate substance in the free zone, qualifying activities, non-qualifying revenue under specific thresholds, and audited financials. The Ministry of Finance has published detailed Cabinet Decisions on what counts. Non-qualifying income within a free zone entity is taxed at 9%.

Types of taxes in the UAE

Personal income tax

There is no personal income tax in the UAE. Salaries, freelance income, dividends, interest, rental income and capital gains received by individuals are not taxed by the UAE.

Corporate tax

Introduced June 2023. 0% on the first AED 375,000 of taxable profit, 9% above. A separate 15% Domestic Minimum Top-up Tax applies from 2025 to UAE entities of multinational groups with consolidated revenue above EUR 750 million, aligning with the OECD's Pillar Two global minimum tax. Almost no freelancers or small business owners will hit this threshold; it is aimed at MNEs.

Value Added Tax

5% on most goods and services since January 2018. Some categories are zero-rated (exports outside the GCC, international transport, certain healthcare and education) or exempt (residential rent after the first supply, life insurance, some financial services). Businesses with taxable supplies above AED 375,000 in the previous 12 months must register. See the Federal Tax Authority.

Excise tax

50% on sugary drinks. 100% on tobacco products, energy drinks and electronic smoking devices. Levied at import or manufacture and passed through to the consumer.

Property-related charges

In Dubai, a 4% transfer fee on property purchase, paid to the Dubai Land Department, typically split or negotiated between buyer and seller (in practice the buyer pays). Residential tenants pay a 5% municipality housing fee, added monthly to the DEWA utility bill, calculated on the annual rent.

Tourism and hospitality

Hotels in Dubai add a tourism dirham of AED 7–20 per room per night depending on the hotel's classification, plus a 10% municipality fee and a 10% service charge. These are not federal taxes but feel like them on the invoice.

Is Dubai 100% tax free

No, and anyone who tells you it is either selling something or has not read a DEWA bill. Personal income is untaxed. Most other economic activity is taxed at modest rates: 5% on consumption, 9% on corporate profit above the threshold, 5% on rent, 4% on property purchases. The aggregate burden for a salaried employee living modestly is materially lower than in any OECD country — but it is not zero.

What taxes do you pay in Dubai

For an individual employee renting an apartment and not running a business:

- 0% on salary

- 5% VAT on most purchases

- 5% housing fee on annual rent (so AED 100,000 rent → AED 5,000 per year, billed monthly with utilities)

- AED 10–60 per night in hotel charges when travelling within the UAE

- Excise baked into the price of sugary drinks, energy drinks and tobacco

For a freelancer or business owner add:

- 9% corporate tax on company taxable profit above AED 375,000 (unless qualifying free zone income)

- 5% VAT registration and filing above the AED 375,000 supplies threshold

For a property buyer add:

- 4% transfer fee at purchase

- Approximately AED 4,000–6,000 in DLD admin and trustee fees

Do US citizens pay taxes in Dubai

Not to the UAE. To the US, yes — always. US citizenship-based taxation under the Internal Revenue Code makes worldwide income reportable regardless of residence.

The practical tools:

- Foreign Earned Income Exclusion (FEIE): up to USD 126,500 of earned income for tax year 2024, indexed for inflation. Requires Form 2555 and either bona fide residence or 330 days of physical presence outside the US in a 12-month period. See IRS Publication 54.

- Foreign Housing Exclusion: an additional carve-out for housing costs above a base amount. The IRS publishes city-specific high-cost limits each year — Dubai is on the list with a higher cap than the standard.

- Foreign Tax Credit (Form 1116): offsets US tax with foreign income tax paid. In Dubai there is no foreign income tax to credit, so this is rarely useful for salary, but matters for US persons with income sourced from other countries.

- FBAR (FinCEN 114): required if aggregate foreign account balances exceed USD 10,000 at any time in the year. Penalties for non-filing start at USD 10,000 per non-wilful violation.

- FATCA Form 8938: thresholds are higher (USD 200,000 end-of-year / USD 300,000 peak for single filers abroad) but it is a separate filing on top of FBAR.

- Form 5471: required for US persons owning 10% or more of a foreign corporation. Penalties for non-filing start at USD 10,000 per form per year.

- GILTI and Subpart F: can attribute UAE company profits to US shareholders before any distribution. A UAE LLC taxed at 9% may still trigger US tax under GILTI, though the 50% deduction and foreign tax credit (Section 250 and Section 960) reduce the effective US rate.

No US–UAE tax treaty exists. This means no tie-breaker rule for dual residency claims, no reduced withholding rates on US-source dividends and interest paid to UAE residents (so the statutory 30% applies unless other rules intervene), and no totalisation agreement for social security.

Renouncing US citizenship is the only mechanism that ends US tax filing obligations. It carries an expatriation tax under IRC Section 877A for covered expatriates and is not a casual decision. Anything short of renunciation — including becoming a UAE tax resident, getting a UAE Tax Residency Certificate, or incorporating a UAE company — does not remove your US filing duty.

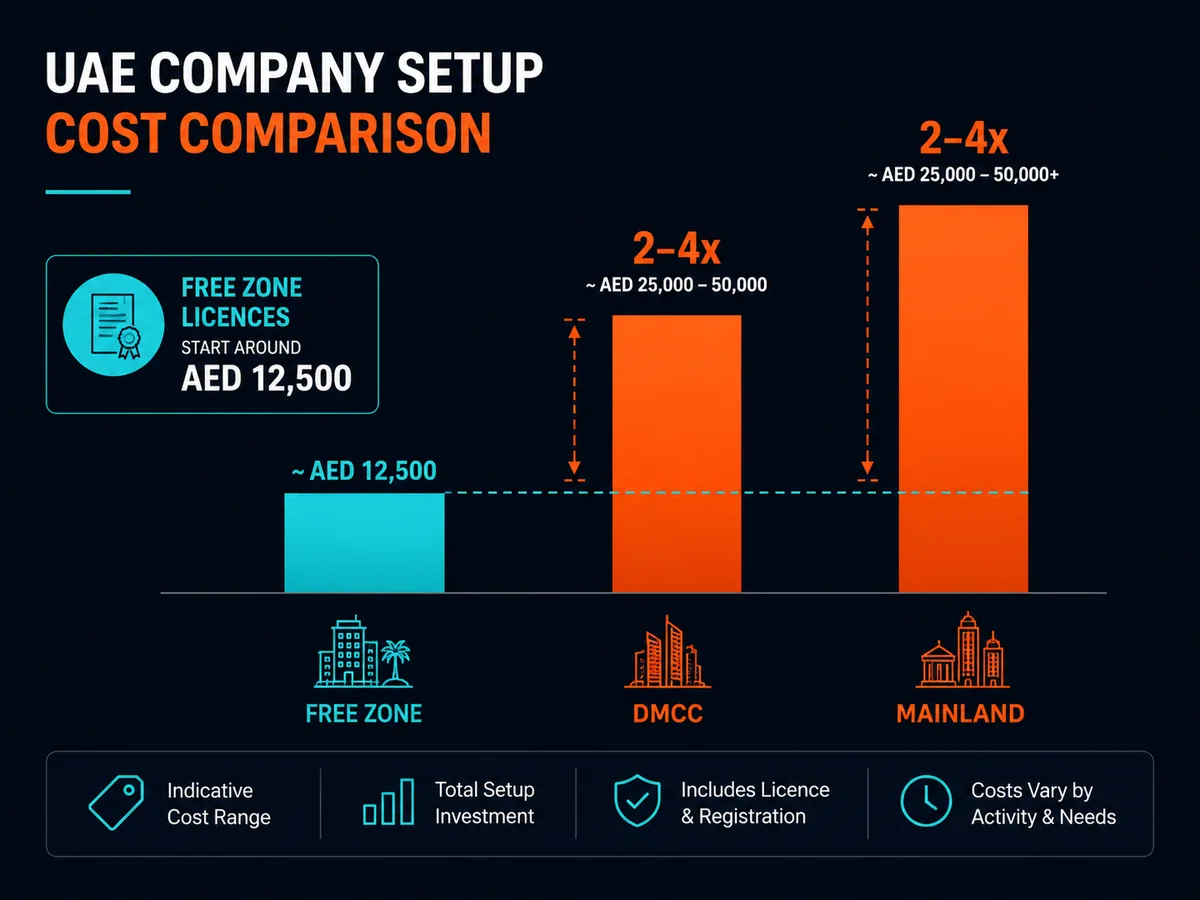

Realistic costs, fees and timeline

| Item | Typical cost (AED) | USD approx | Notes |

|---|---|---|---|

| Mainland LLC setup (DED) | 15,000–30,000 | 4,000–8,000 | Includes trade licence year one |

| Free zone company (IFZA, Meydan, RAKEZ) | 12,500–25,000 | 3,400–6,800 | Bundles vary; visa allocation separate |

| DMCC free zone company | 35,000–60,000 | 9,500–16,300 | Premium free zone, stronger banking access |

| Investor / partner residence visa (2 yr) | 4,000–7,000 | 1,100–1,900 | Per person, including medical and Emirates ID |

| Employment visa (employer-sponsored) | 3,000–6,000 | 800–1,600 | Usually employer pays |

| Golden Visa (10 yr) — investor track | 10,000–15,000 | 2,700–4,100 | Plus AED 2m property or business investment |

| Annual office rent (flexi-desk) | 8,000–18,000 | 2,200–4,900 | Required for most licences |

| Annual residential rent (1BR, decent area) | 70,000–130,000 | 19,000–35,000 | Plus 5% housing fee |

| Mandatory health insurance | 5,000–15,000 per person | 1,400–4,100 | More for older applicants or families |

| UAE Tax Residency Certificate | 1,750 + 50 | 490 | Federal Tax Authority fee |

Setup from arrival to functioning company with bank account typically takes 6–12 weeks. Bank account opening is the bottleneck; expect 4–8 weeks and detailed source-of-funds questions. Substance — a real office, real activity, not a PO box — matters both for UAE corporate tax qualifying status and for defending residency against your former home country.

Common mistakes and how to avoid them

Claiming UAE residency without breaking the prior one. The most expensive mistake EU nationals make. Spending 200 days in Dubai does not end French or Spanish tax residency if your spouse, kids and primary home stay behind. Document the move: deregister from local civil registries, close or transfer the home, move dependants, terminate domestic ties. Keep evidence.

Assuming no treaty means no problem for Americans. The absence of a US–UAE treaty means more friction, not less. US-source income remains subject to full statutory withholding, and there is no treaty tie-breaker if both countries claim you. Plan around it; do not ignore it.

Forgetting CFC rules. A UAE company owned by an EU or UK resident can have its profits attributed back under the ATAD or UK CFC legislation. Owning a UAE company through a UAE residence works; owning one while still tax-resident in Munich or Madrid often does not.

Treating "free zone = 0% tax forever". Since June 2023 the 0% free zone rate is conditional on being a Qualifying Free Zone Person and earning Qualifying Income. Substance requirements, audited accounts and qualifying-activity tests apply. Many free zone companies will fall into the 9% rate on at least part of their income. Read the Cabinet Decisions or get a UAE tax adviser to read them for you.

Skipping FBAR and Form 5471 because no UAE tax is due. US reporting obligations are independent of whether tax is owed. Penalties for non-filing are flat-rate and brutal. File on time even

Ready to act on this?

SPC Free Zone (Sharjah) — UAE free-zone formation with a public referral programme. Soveraine readers go to the front of the line through our partner link, and you fund independent editorial in the process.