"Tax resident nowhere" is one of the most repeated phrases in the perpetual-traveler corner of the internet and one of the most poorly understood. The position is legally possible for a narrow set of people, structurally impossible for US citizens, fragile for most EU residents, and operationally fragile for everyone who pulls it off. This guide explains what the phrase actually means under the OECD Model Tax Convention and the major domestic tax statutes, who can realistically use it and for how long, the three practical paths that exist, and the banking, treaty and reporting traps that decide whether the strategy survives a tax-authority enquiry. It is written for three audiences in parallel: US persons, EU residents, and readers based in the rest of the world.

Bright!Tax — US expat tax filings (FBAR + FATCA + FEIE specialists)

What "tax resident nowhere" actually means

Tax residency is not the same as immigration residency, and that confusion is responsible for most of the bad advice on this topic. Immigration residency is granted by a country's immigration authority and decides whether you can legally enter and stay. Tax residency is determined by the tax authority — usually a different agency — and decides whether you owe income tax on worldwide income there. A person can hold a Portuguese D7 visa and not be a Portuguese tax resident; a person can be deemed a German tax resident without any German immigration status at all. Only the second system is in scope here.

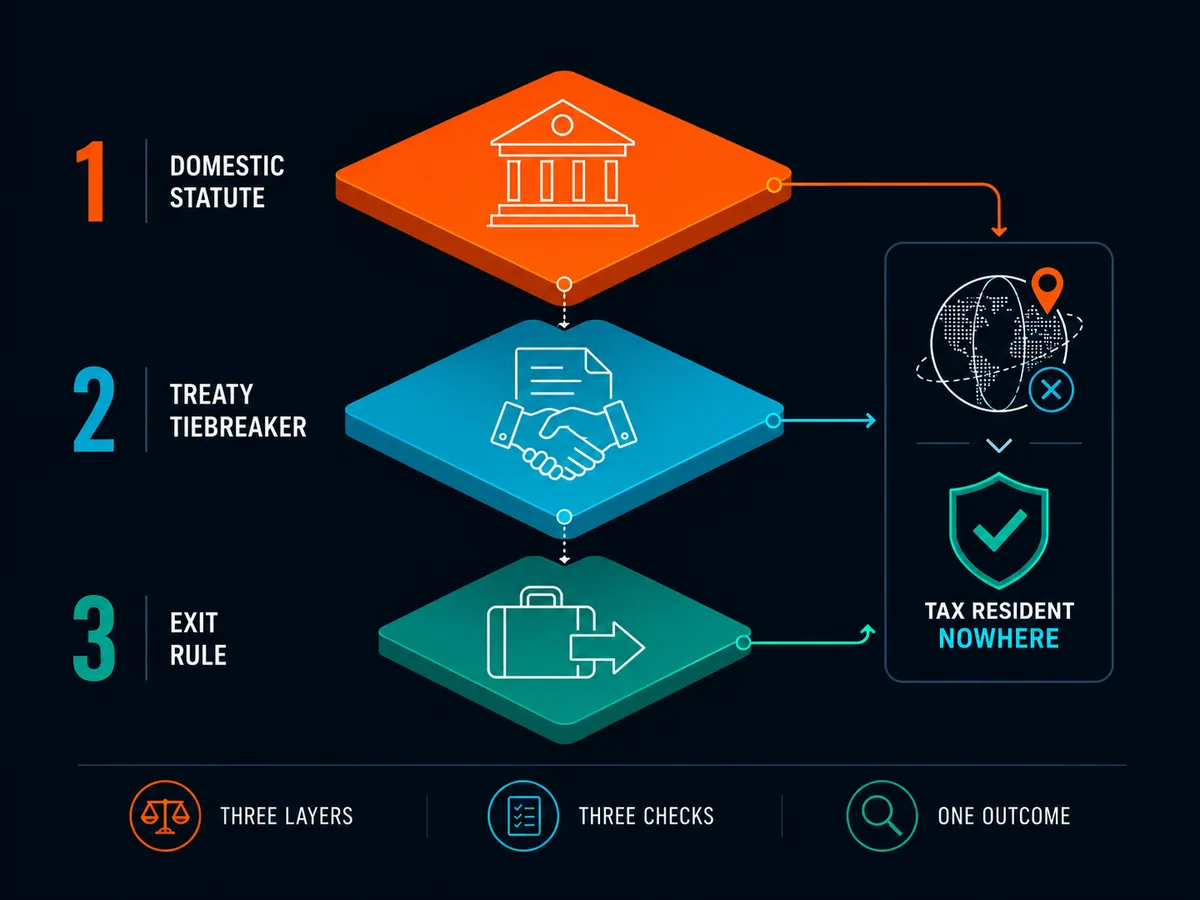

"Tax resident nowhere" describes a person whose facts do not trigger residency under the domestic rules of any country in a given tax year. The position survives a treaty challenge only where the home country either accepts the departure under its own statute or loses an OECD Model Tax Convention Article 4 tiebreaker — and that tiebreaker only operates if a treaty exists. Article 4(2) runs four sequential tests where two states both claim the same person: permanent home, centre of vital interests, habitual abode, nationality, with mutual agreement as the final fallback.

The legal architecture has three layers: each country's domestic residency statute (day count, home test, family test, registration), the bilateral treaty that uses Article 4 to resolve dual residence, and the home country's exit rule. A person who has read all three for every country they touch can design around them. A person who has read only the day-count rule cannot.

Who this applies to — read this first

The relevance of every section below changes sharply depending on the passport you hold and the country that currently claims you as a tax resident. Three positions, three different answers.

US persons

This strategy does not work for US citizens or lawful permanent residents. The United States taxes its citizens on worldwide income regardless of physical location under IRC §1 and IRC §61, confirmed in Cook v. Tait, 265 U.S. 47 (1924). A US citizen with no other tax residency still owes US tax on worldwide income, still files Form 1040, still files FBAR under 31 USC §5314, and still files Form 8938 above the FATCA thresholds.

Two paths exist out: formal renunciation under 8 USC §1481, which triggers the exit tax for covered expatriates under IRC §877A — a mark-to-market deemed sale above $890,000 for 2025; or mitigation through the foreign earned income exclusion of up to $130,000 for 2025 under IRC §911, the foreign housing exclusion, and foreign tax credits. Neither reduces filing complexity. A US person living as a perpetual traveler typically faces more filing complexity, not less, because evidencing FEIE eligibility without a settled foreign tax home is hard. Specialist filers such as Bright!Tax handle this routinely.

EU residents

For an EU citizen currently tax-resident of a member state, two structural obstacles sit between the present position and a clean result. The first is the exit tax — Germany under Außensteuergesetz §6, the Netherlands' conserverende aanslag, France under Article 167 bis CGI, Spain under Article 95 bis of the Personal Income Tax Law. The EU Anti-Tax Avoidance Directive 2016/1164 sets a minimum framework across member states.

The second is the Article 4 tiebreaker, which only helps if a treaty exists. A French resident who exits in favour of Paraguay has no France-Paraguay treaty; if France contests under Article 4B CGI, there is no treaty mechanism to escape. France, Australia and Finland can refuse to accept the departure until new tax residency is documented elsewhere — Finland treats former residents as taxable for up to three years under Income Tax Act §11.

Non-US, non-EU readers

This segment generally has the simplest position. Most non-US, non-EU jurisdictions tax on residence rather than citizenship, accept a clean break when day count and ties are gone, and do not impose individual exit taxes. Risks concentrate around controlled-foreign-company rules (notably UK, Australia, Canada and South Africa), trailing residency rules such as South Africa's ordinarily-resident test, and the rising requirement to produce a foreign tax residency certificate before banks release accounts. The three paths below are most accessible to this segment.

The three practical paths

Three patterns exist in real use, each with a different risk profile.

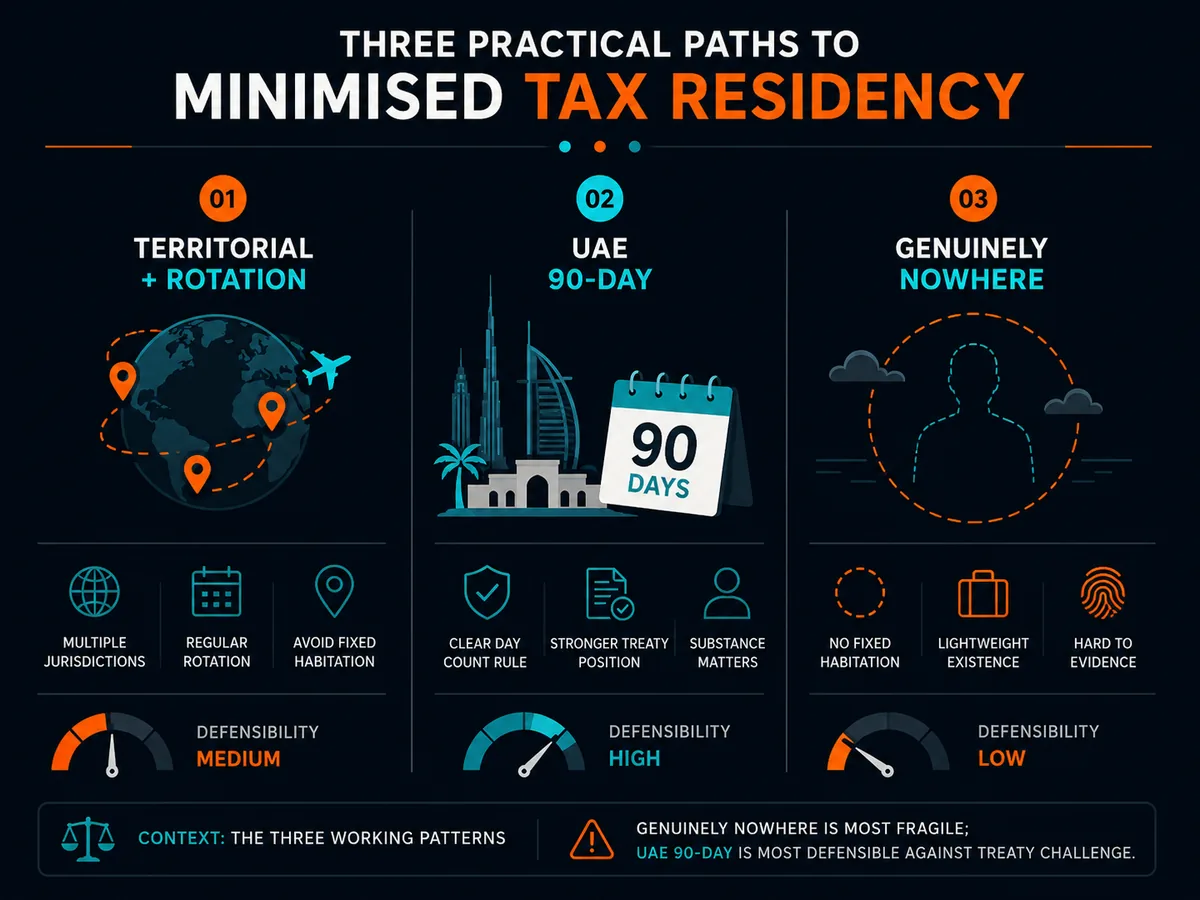

Path one — territorial residency plus rotation

The common pattern pairs formal tax residency in a territorial-taxation country with travel through countries that do not trigger residency. Paraguay, Panama and Costa Rica tax only local-source income; foreign-client revenue through a foreign company sits outside the local net. The holder spends part of the year in the territorial country (in Paraguay's case, often none), rotates through Southeast Asia, and operates through an entity in a third jurisdiction. The status is not "tax resident nowhere" — it is "tax resident where the rate on relevant income is zero." That distinction matters when a bank or home authority asks for a certificate.

Setup runs USD 2,000 to USD 8,000 through a local agent, plus minimal Paraguayan upkeep or a USD 200,000 Panamanian investment under the 2021 Friendly Nations reform. See the zero-percent tax residencies pillar for country detail.

Path two — UAE residency plus the 90-day rule

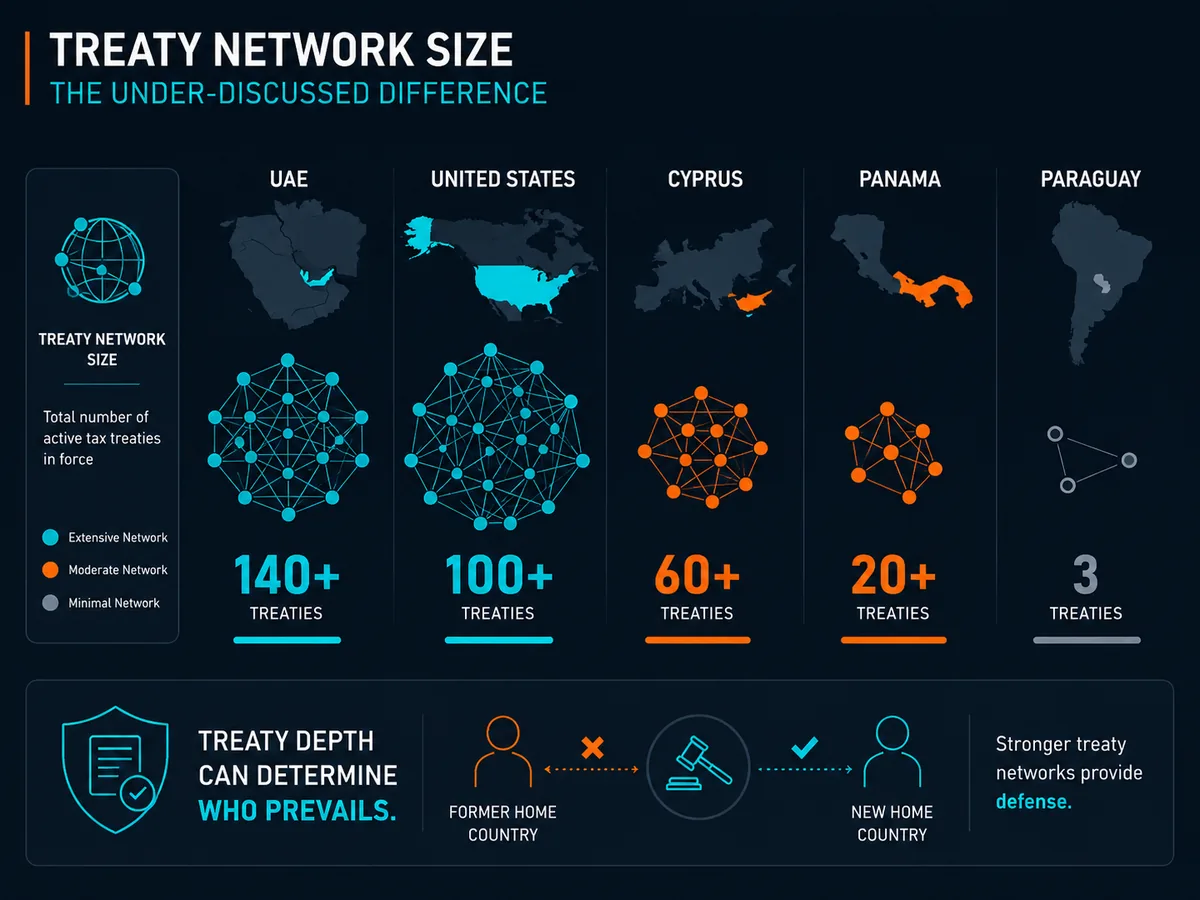

The UAE combines zero personal income tax, a usable tax residency certificate, and around 140 double tax treaties. Individuals qualify under Cabinet Decision No. 85 of 2022 on three bases: principal residence and centre of interests in the UAE; 183 days in any 12-month period; or 90 days for UAE/GCC nationals or valid-residence holders with a permanent home or business there. The 90-day route is the workhorse for the free-zone-licensed founder.

The Federal Tax Authority issues a Tax Residency Certificate via its TRC portal once requirements are met — the document banks request and the one needed to invoke the UAE side of an Article 4 tiebreaker. Setup runs USD 5,000 to USD 12,000 through providers such as SPC Free Zone, with USD 4,000–6,000 annual renewals. The 9% corporate tax above AED 375,000 under Federal Decree-Law No. 47 of 2022 is the trade-off. For treaty defensibility and banking acceptance, stronger than genuine statelessness.

Path three — genuinely nowhere

The pure perpetual-traveler structure has no formal residency anywhere. The holder stays under every country's trigger, holds no permanent home, breaks every home-country tie, and operates through a foreign entity tax-resident where incorporated. Legally possible for citizens of countries that allow clean departure without proof of new residency — Germany, the UK (subject to SRT), the Netherlands (after exit tax), and most Commonwealth jurisdictions other than Australia.

Banks, brokers, insurers, mortgage lenders and trading apps all ask for a tax residency, and CRS reporting requires every institution to attach one to every account. The pattern that works combines this with banking through the operating company where it is tax-resident, rather than personal accounts. Insurance gaps are filled by nomad insurers such as SafetyWing; transactional banking comes from fintechs like Wise that accept a passport plus a verified address. Sustainable for one to three years; longer, friction usually pushes the person into Path one or Path two.

The legal mechanics — domestic rules vs treaty tiebreakers

"Stay under 183 days" is the most repeated wrong sentence in this subject. Every meaningful jurisdiction layers a substantive ties test on top of the day count.

United Kingdom. The Statutory Residence Test in Schedule 45 of the Finance Act 2013 combines automatic overseas tests, automatic UK tests and a sufficient ties test. Five ties — family, accommodation, work, 90-day, country — set the day threshold. A leaver with no UK ties can spend up to 182 days; with four ties, residency triggers at 16.

Germany. Residency under §8 and §9 Abgabenordnung is triggered by either habitual abode (six months continuous) or domicile (Wohnsitz — an available, used home). Renting out a German flat at arm's length usually breaks the Wohnsitz; keeping a key to a relative's spare room does not.

France. Article 4B CGI treats a person as resident if their foyer, principal place of stay, professional activity or centre of economic interests is in France. Any one triggers residency. France often requires proof of new residency before accepting departure.

United States — substantial presence test. For non-citizens, the substantial presence test under IRC §7701(b) requires 31 days in the current year plus a weighted three-year sum (current + 1/3 prior + 1/6 year before) totalling 183 or more. US citizens are taxed regardless.

OECD MTC Article 4. Where two countries both claim a person, a bilateral treaty applies Article 4(2). Full text is in the condensed OECD MTC and summarised in IRS Publication 519. Sequential tests: permanent home, centre of vital interests, habitual abode, nationality, mutual agreement.

The tiebreaker only operates between treaty partners. Paraguay's nine treaties make it a far weaker treaty position than the UAE's 140, regardless of headline rate.

What goes wrong

The strategy fails most often at the bank, not the tax authority. The Common Reporting Standard, adopted by over 120 jurisdictions, requires every participating institution to identify the tax residency of every account holder and report balances annually. A holder who lists "none" is flagged and often off-boarded within 30 to 60 days under internal compliance policies.

No tax residency certificate equals no private bank account. Most non-US private banks now require an issued certificate; fintechs are more flexible but increasingly require a tax identification number tied to a country.

No certificate does not equal exemption from home-country claim. Domestic statutes in France, Germany, Spain and the Netherlands operate independently of whether the leaver took up a new residency. Until the home exit rule is satisfied — which often requires producing a new certificate — the home state continues to claim worldwide income.

Bank de-risking. Banks regularly exit clients whose stated residency sits on the EU list of non-cooperative jurisdictions. Panama appears periodically; the UAE was on the grey list until 2024. A residency that is paper-compliant can still cost banking access.

CRS reporting still flows. It goes to wherever the bank believes the holder lives — often the passport country, which is then well placed to reassert residency.

FBAR for US persons. US citizens with no tax residency anywhere still owe FBAR. Non-wilful penalties run up to $10,000 per violation under 31 USC §5321; wilful failures can reach 50% of account balance. Form 8938 under FATCA is owed in parallel.

Trailing residency rules. Finland treats former residents as taxable for up to three years under Income Tax Act §11; Sweden applies five-year rules to leavers retaining essential ties; South Africa's ordinarily-resident test extends residency beyond day counts.

Comparison table

| Country | Domestic residency rule | Tax residency certificate? | Treaty network | Best for |

|---|---|---|---|---|

| Paraguay | 120+ days in practice plus economic activity registration (SET) | Available after SET registration | ~9 treaties | Travellers who need a paper home and accept a thin treaty network |

| UAE | 90 days with local home/business, otherwise 183 (Cabinet Decision 85) | Issued by FTA via the TRC portal | ~140 treaties | Founders wanting treaty defensibility and banking quality |

| Panama | 180 days plus economic interests (Article 762-N Fiscal Code) | Issued by DGI | ~17 treaties | Latin American hub, USD banking |

| Cyprus | 60 days (no other 183-day residence) or standard 183 days | Issued by Cyprus Tax Department | ~65 treaties | EU passport-holders wanting an EU base |

| Germany | Habitual abode 6 months continuous, or Wohnsitz (§8/§9 AO) | Issued by Bundeszentralamt für Steuern | ~95 treaties | Reference rule — the rule to escape, not adopt |

| United Kingdom | Statutory Residence Test (Schedule 45 Finance Act 2013) | Issued by HMRC | ~130 treaties | Reference rule for UK leavers |

| France | Foyer / 183 / professional / economic centre (Article 4B CGI) | Issued by DGFiP | ~125 treaties | Reference rule — strict, multi-factor |

| United States (citizens) | Citizenship-based (IRC §1) | N/A — Form 6166 issued for treaty purposes | ~70 treaties | Not escapable without renunciation |

Sources: OECD Model Tax Convention, UAE Federal Tax Authority, HMRC Statutory Residence Test, IRS Publication 519, PwC Worldwide Tax Summaries.

When this strategy actually works

The honest profile of the person for whom tax-resident-nowhere is a sound plan is narrower than the genre suggests. Five conditions in combination.

A non-US passport. US citizens cannot use this strategy. The only US-side path to a comparable position is renunciation, a separate decision with its own consequences.

Income roughly in the USD 50k–130k range. Below that, operational friction usually costs more than the tax saved. Above it, the cost of failure if a tax authority reasserts residency rises sharply and a formal low-tax residency starts to look better.

No minor children and no spouse in the home country. A spouse remaining in a high-tax country with a job, a home and a family life there will, in most OECD-style frameworks, pull the departing partner back under the centre-of-vital-interests test. Children in school in the home country produce the same result.

No permanent home retained. The single fastest way to lose a tiebreaker is to keep a home in the old country that remains available. An empty apartment, keys left with family, or a furnished room "for visits" all qualify as available homes under the OECD test.

Meticulous travel records. Boarding passes, passport stamps, hotel receipts, electronic border-system reports, and a contemporaneous travel log per country per year. The person who cannot prove they were under the threshold loses every challenge on burden-of-proof grounds.

For the person who meets all five, the strategy is legal, defensible and frequently used for the period between leaving a high-tax country and settling in a low-tax one. For someone meeting four, it produces audit risk that surfaces years later. For three or fewer, it is almost always cheaper to formalise a low-tax residency from the start.

Final CTA

Ready to act on this?

Bright!Tax — US expat tax filings (FBAR + FATCA + FEIE specialists). For US persons reading this, the perpetual-traveler structure does not change the US filing obligation; Soveraine readers go to the front of the line through our partner link, and you fund independent editorial in the process.

Sources

- OECD Model Tax Convention on Income and on Capital. https://www.oecd.org/tax/treaties/model-tax-convention-on-income-and-on-capital-condensed-version-20745419.htm

- OECD Common Reporting Standard. https://www.oecd.org/tax/automatic-exchange/

- IRS Publication 519 — US Tax Guide for Aliens. https://www.irs.gov/publications/p519

- IRS — Substantial Presence Test. https://www.irs.gov/individuals/international-taxpayers/substantial-presence-test

- IRC §1 — Tax imposed. https://www.law.cornell.edu/uscode/text/26/1

- IRC §61 — Gross income defined. https://www.law.cornell.edu/uscode/text/26/61

- IRC §877A — Tax responsibilities of expatriation. https://www.law.cornell.edu/uscode/text/26/877A

- IRC §911 — Citizens or residents of the United States living abroad. https://www.law.cornell.edu/uscode/text/26/911

- IRC §7701(b) — Definition of resident alien and nonresident alien. https://www.law.cornell.edu/uscode/text/26/7701

- 8 USC §1481 — Loss of nationality by native-born or naturalised citizen. https://www.law.cornell.edu/uscode/text/8/1481

- 31 USC §5314 / §5321 — FBAR and penalties. https://www.law.cornell.edu/uscode/text/31/5314

- UAE Cabinet Decision No. 85 of 2022. https://mof.gov.ae/

- UAE Federal Tax Authority. https://tax.gov.ae/en/

- UAE Federal Decree-Law No. 47 of 2022 — Corporate tax. https://mof.gov.ae/corporate-tax/

- HMRC RDR3 — Statutory Residence Test. https://www.gov.uk/government/publications/rdr3-statutory-residence-test-srt

- Abgabenordnung §8 / §9 — German residency. https://www.gesetze-im-internet.de/ao_1977/__8.html

- Außensteuergesetz §6 — German exit tax. https://www.gesetze-im-internet.de/astg/__6.html

- Code général des impôts Article 4B — French residency. https://www.legifrance.gouv.fr/codes/article_lc/LEGIARTI000006302201/

- Code général des impôts Article 167 bis — French exit tax. https://www.legifrance.gouv.fr/codes/article_lc/LEGIARTI000043661449/

- EU Anti-Tax Avoidance Directive 2016/1164. https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=celex%3A32016L1164

- EU list of non-cooperative jurisdictions for tax purposes. https://www.consilium.europa.eu/en/policies/eu-list-of-non-cooperative-jurisdictions/

- Paraguay Subsecretaría de Estado de Tributación. https://www.set.gov.py/

- Dirección General de Ingresos de Panamá. https://www.dgi.gob.pa/

- PwC Worldwide Tax Summaries. https://taxsummaries.pwc.com/