On 1 January 2026, the United States began collecting a new federal excise tax on certain money transfers sent abroad. It is small — 1% — but the rule that decides who pays is narrow and easy to misread. This article explains what the US tax on remittance actually is, who it hits, who is exempt, and how it interacts with the separate remittance and outbound-transfer rules that apply to EU residents and to readers sending money from India, the Gulf and other non-US jurisdictions. We will not tell you how to evade it. We will tell you, with primary sources, where the legal lines are.

Bright!Tax — US expat tax filings (FBAR + FATCA + FEIE specialists)

What is tax on remittance

A remittance tax is a levy charged on money transferred across borders, usually from a worker in a high-income country to a recipient in their home country. Most countries do not impose one. The economic consensus, including the World Bank's 2017 analysis, is that remittance taxes are regressive, push transfers into informal channels, and raise little revenue relative to their compliance cost.

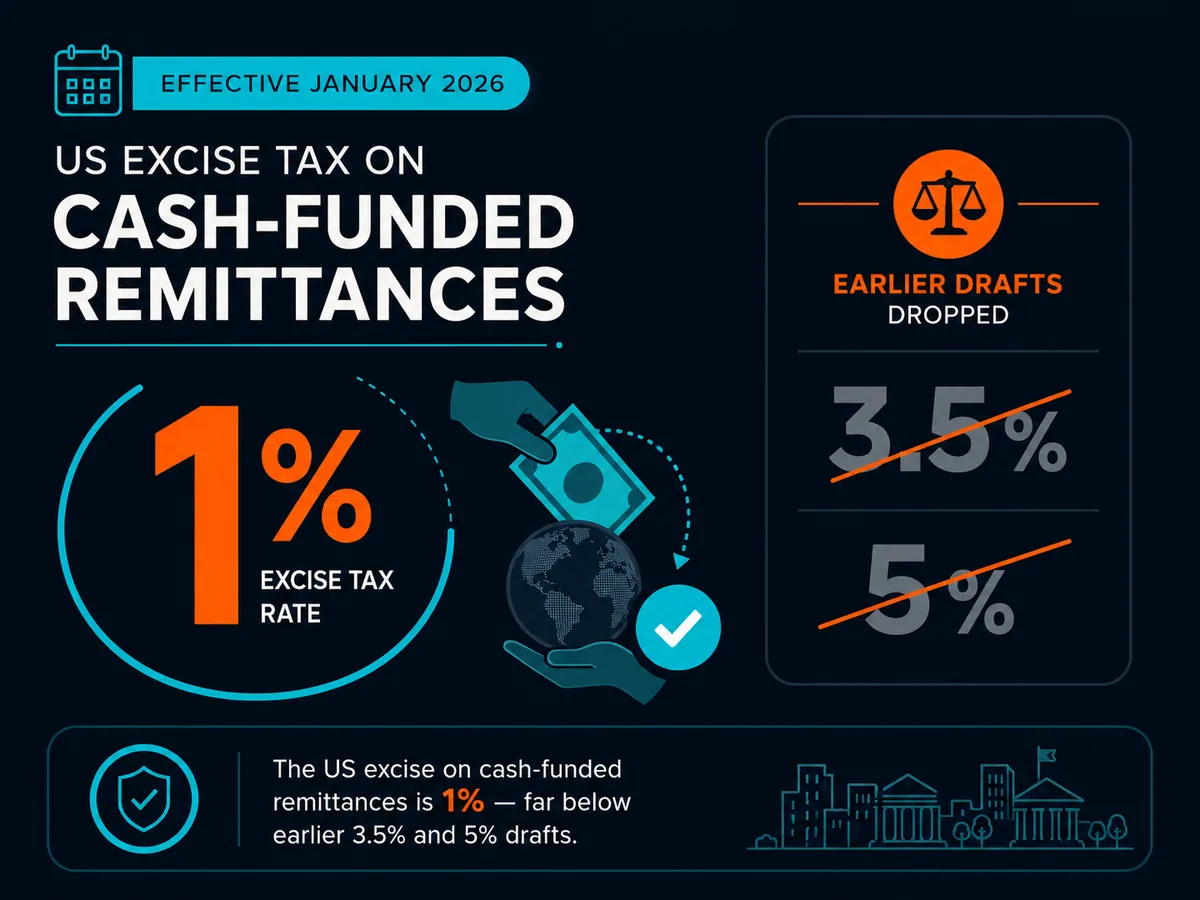

The United States changed course in 2025. The One Big Beautiful Bill Act added new section 4475 to the Internal Revenue Code, imposing a 1% excise tax on qualifying remittance transfers. The law took effect on 1 January 2026. India operates a different mechanism — Tax Collected at Source on outbound transfers under the Liberalised Remittance Scheme — which is a withholding, not an excise. The two are often confused. They are not the same thing.

Who this applies to

Your nationality and tax residency determine which rules bind you. The new US excise tax is jurisdictional: it depends on where the transfer is sent from, not who is sending it. But other regimes — citizenship-based taxation, controlled foreign corporation rules, exit taxes — layer on top.

US persons (citizens and green-card holders)

If you are a US citizen or green-card holder, you are subject to US tax on your worldwide income regardless of where you live. The 1% excise on remittance is a separate, transaction-level tax — it applies to transfers you initiate from inside the United States, whether you are a citizen, resident alien, or visitor. It does not replace your Form 1040 obligations, FBAR (FinCEN Form 114), or FATCA Form 8938.

A common misreading: the tax does not apply to US persons living abroad sending money between two foreign accounts. The transfer must originate from within the United States.

EU freelancers and digital nomads

EU tax residents are generally not subject to the US excise unless they are physically funding a transfer from inside the US. EU member states do not, as a rule, tax outbound remittances directly. What does apply: the 183-day rule and the "centre of vital interests" test under most double-tax treaties, controlled foreign corporation rules under ATAD, and — in countries like France, Germany, Spain, the Netherlands — exit taxes on unrealised capital gains when you move tax residency outside the EU.

If you are an EU freelancer billing a US client, the funds you receive into an EU bank are not "remittances" subject to the US excise. They are income, taxed where you are resident.

Non-US, non-EU readers

Readers in territorial-tax jurisdictions — UAE, Singapore, Hong Kong, Panama, Georgia, Paraguay — typically face neither outbound remittance tax nor worldwide-income taxation on foreign-source funds. India, the Philippines and several Latin American countries do impose outbound transfer charges or withholdings; check your domestic rules. The US excise still catches you if you initiate a cash-funded transfer from US soil — for example, while travelling.

The 1% federal remittance tax under the OBBB Act

Internal Revenue Code section 4475, added by the One Big Beautiful Bill Act, imposes a 1% excise tax on the amount of each remittance transfer from a sender in the United States to a person located in a foreign country, where the transfer is made through a remittance transfer provider.

The statute, read with IRS Notice 2025-55, produces these operational rules:

- Rate: 1% of the gross transfer amount.

- Trigger: the sender funds the transfer with cash, a money order, a cashier's check, or a similar physical instrument.

- Exclusion: transfers funded by debit from an account at a US financial institution, or by a US-issued debit or credit card, are not subject to the tax.

- Collector: the remittance transfer provider — defined by reference to the Electronic Fund Transfer Act, 15 USC § 1693o-1.

- Deposit schedule: quarterly; the first deposit was due April 2026.

- Penalty relief: the IRS granted relief from failure-to-deposit penalties for the first three quarters of 2026, provided the provider deposits the tax by the fourth-quarter due date.

The law does not exempt transfers below any dollar threshold. A $50 cash money order to a relative abroad attracts $0.50 in tax. There is also no recipient-country exemption: a transfer to Canada is treated the same as a transfer to Nigeria.

What "cash or similar physical instrument" means

This is where the rule bites. Per the IRS guidance, the tax applies when "the sender provides funds using cash or other similar physical instruments." That includes:

- Banknotes and coin handed to an agent

- Money orders

- Cashier's checks

- Traveler's checks

It excludes:

- ACH transfers from a US checking or savings account

- Online wire transfers debited from a US bank account

- Card-funded transfers via Wise, Remitly, Western Union online, Xoom, MoneyGram online, or a bank's app

The funding method, not the brand or the destination, decides taxability. A $1,000 transfer to Mexico through Western Union's website, funded by debit card, is exempt. The same transfer in cash at a Western Union agent is taxable.

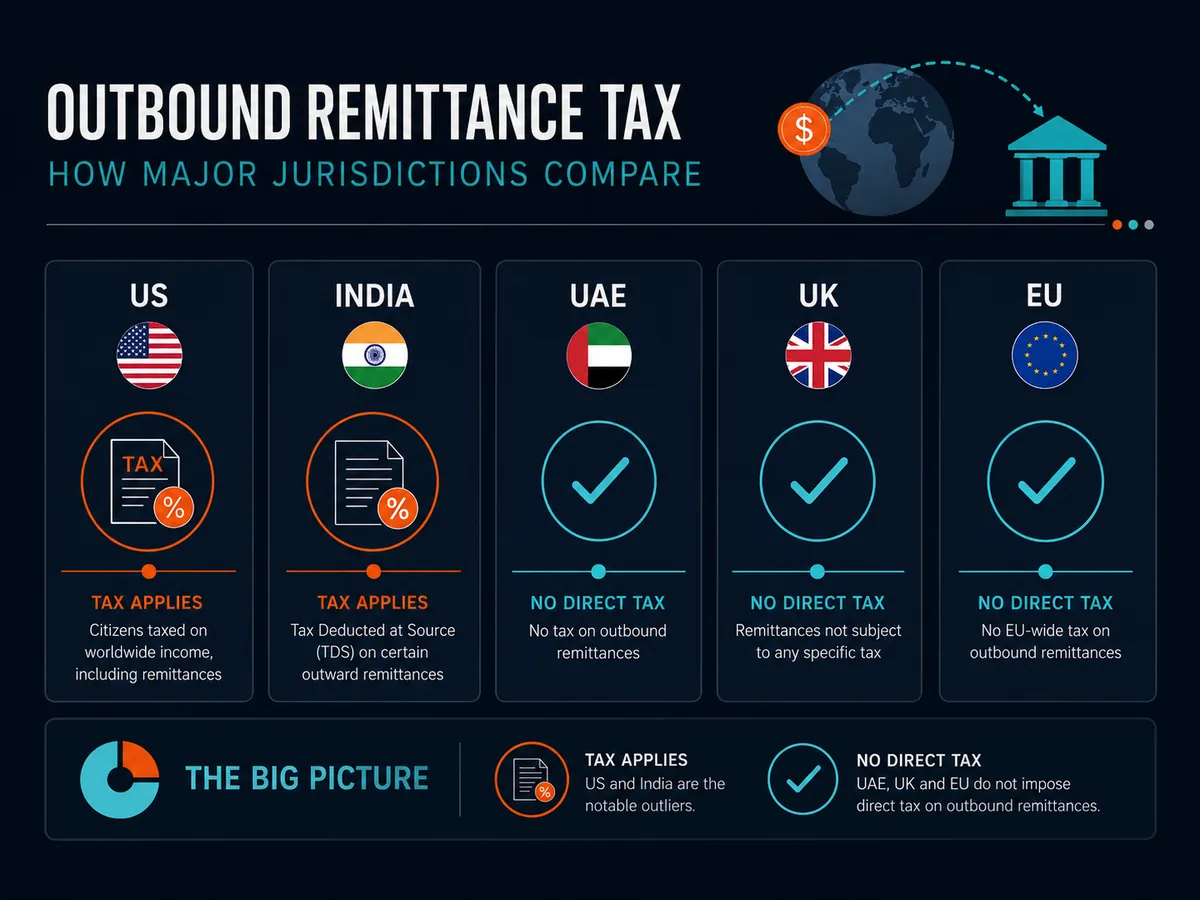

Is there a tax on remittances

For US-originating transfers: yes, since 1 January 2026, under IRC section 4475. For most other countries: no direct excise, but several jurisdictions impose related charges.

| Country | Mechanism | Rate | Threshold |

|---|---|---|---|

| United States | Federal excise (IRC §4475) | 1% | None; cash-funded only |

| India | TCS under LRS | 20% (5% for education/medical above threshold) | ₹7 lakh / FY |

| Pakistan | None on outbound | — | — |

| UAE | None | — | — |

| Saudi Arabia | None (2015 proposal abandoned) | — | — |

| EU member states | None direct; some FTT proposals | — | — |

| United Kingdom | None | — | — |

Sources: IRS Notice 2025-55; Indian Income Tax Act, Section 206C(1G); [source: TODO — UK HMRC confirmation no outbound remittance tax].

How do I avoid 20% TCS on foreign remittance from India

Indian residents face a different regime: Tax Collected at Source under the Liberalised Remittance Scheme. It is not an excise tax — it is a prepayment of income tax, collected by the authorised dealer (your bank) when you remit abroad.

Current rules (as of FY 2025-26, [source: TODO — confirm against latest Finance Act]):

- Aggregate threshold: ₹7 lakh per financial year across all outward remittances under LRS.

- Below ₹7 lakh: no TCS for most purposes.

- Above ₹7 lakh, education funded by loan: 0.5%.

- Above ₹7 lakh, education or medical (self-funded): 5%.

- Above ₹7 lakh, other purposes (investment, gifts, travel beyond tour packages): 20%.

You cannot legally avoid TCS by structuring transfers under the ₹7 lakh threshold across multiple banks — banks report to the income tax department under LRS and the aggregate is computed at PAN level. Splitting through family members' PANs is a reportable transaction if the funds are economically yours; treating it otherwise risks scrutiny under benami and anti-avoidance rules.

What you can legitimately do:

- Use the credit, not avoidance. TCS is creditable against your final income tax liability. If your tax bill is lower than the TCS collected, you get a refund.

- Time large transfers across financial years to use two annual thresholds.

- Use the education-loan route if remitting tuition: the rate drops to 0.5% when the remittance is funded by a sanctioned education loan.

- Keep documentation of the purpose code — tour packages, investment, education each have different treatment.

None of this is evasion. It is using the statute as drafted.

How to avoid the 1% US remittance tax

The only legal way to "avoid" the 1% excise is to choose a funding method outside the statute's scope. There is no penalty for doing so — it is exactly what the law contemplates.

Use an account-funded transfer. Initiate the transfer online or through your bank's app, funded by debit from a US checking or savings account. This is excluded by IRS Notice 2025-55.

Use a debit or credit card. Card-funded transfers through services like Wise, Remitly or Xoom are not subject to the excise.

Aggregate transfers when you must use cash. The tax is per-transaction on the gross amount. If you genuinely need to remit cash, fewer larger transfers cost the same in tax as many small ones — but the provider's flat fee per transfer is usually the larger cost anyway.

Open a US account if you do not have one. This is the right answer for non-resident workers currently sending cash. Most US banks accept ITIN-holders; community banks and credit unions are often more flexible than national chains.

What does not work — and what we will not write about as if it does — is layering through third-country intermediaries, structuring transfers below reporting thresholds to avoid Bank Secrecy Act flags, or using informal value transfer systems (hawala). The first two are reportable; the third is unlicensed money transmission under 31 USC § 5330 and a federal crime.

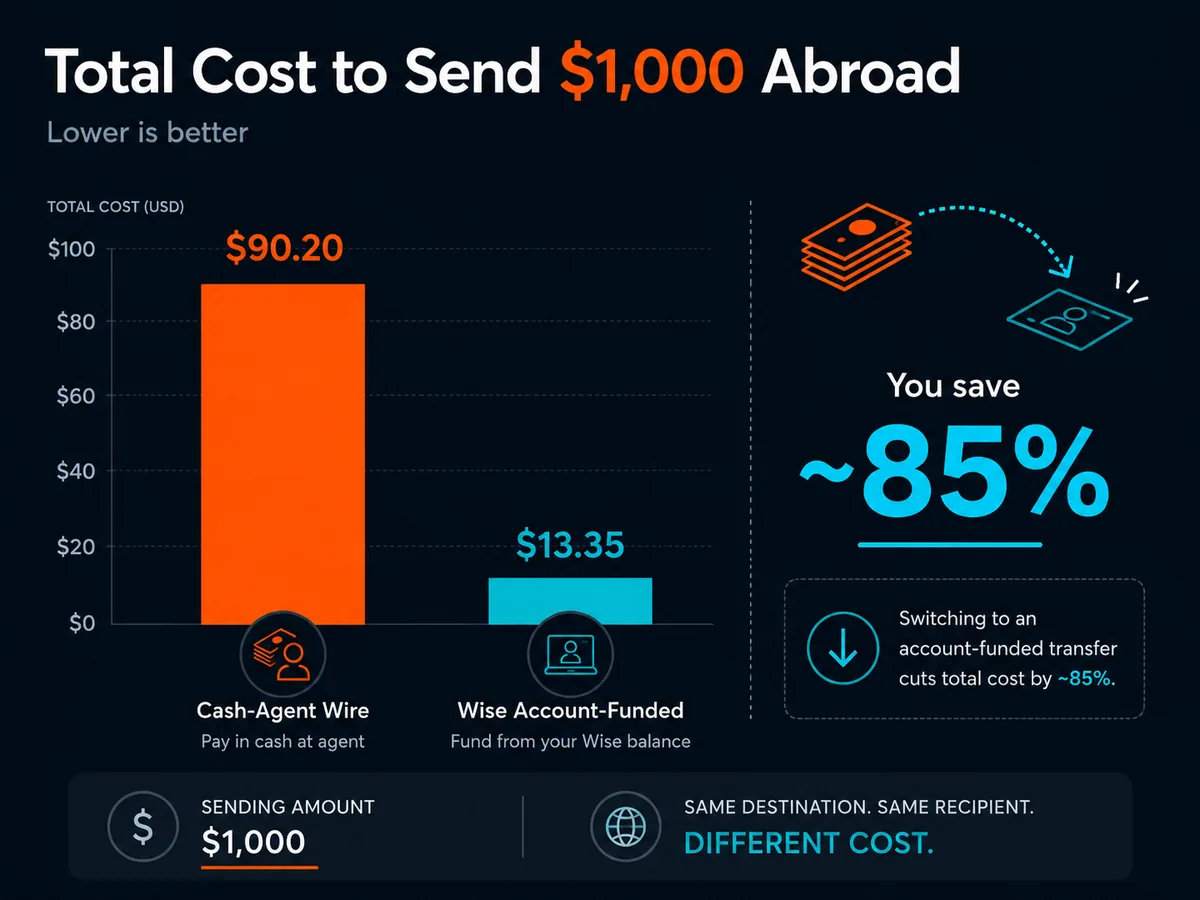

Realistic costs, fees and timeline

The 1% excise is small relative to the provider markup on most cash transfers. Western Union, MoneyGram and similar walk-in services typically take 4-8% in combined fees and FX margin on a cash transfer. The new tax adds another percentage point.

| Transfer type | $1,000 send | Excise tax | Provider fee + FX | Total cost |

|---|---|---|---|---|

| Cash at Western Union agent | $1,000 | $10 | ~$50-80 | $60-90 |

| Western Union online, debit card | $1,000 | $0 | ~$20-40 | $20-40 |

| Wise, USD account funded | $1,000 | $0 | ~$6-12 | $6-12 |

| Bank wire, in-branch cash deposit then wire | $1,000 | $10 | ~$35-50 | $45-60 |

| Bank wire, online from existing account | $1,000 | $0 | ~$25-40 | $25-40 |

Estimates based on November 2025 published pricing; check current rates. Wise pricing: wise.com/us/pricing. Western Union pricing varies by corridor.

Disclosure: Soveraine has no current affiliate relationship with any of the providers above. We mention Wise because, on the corridors we have tested, it has the lowest all-in cost for account-funded transfers under $10,000. For larger transfers or unusual corridors, a dedicated FX broker often beats it; for cash-out at the recipient end in countries with limited banking, Remitly or MoneyGram may be the only practical option.

Common mistakes and how to avoid them

Assuming the rate is 3.5% or 5%. Earlier drafts of the OBBB Act proposed those rates and a broader base. Both were dropped before enactment. The statute as signed is 1%, cash-only.

Assuming all wire transfers are taxed. Online wires from your existing US bank account are not subject to the excise. The trigger is the physical funding instrument, not the rail.

Assuming the tax is on the recipient. It is not. The sender pays at the point of transfer; the provider remits. Recipients abroad face their own country's rules on incoming transfers, which are unrelated.

For US persons abroad: assuming an offshore company solves anything. US citizens are taxed on worldwide income regardless of where they live or where their company is incorporated. Subpart F, GILTI, and CFC reporting under Forms 5471 and 8865 apply. The Foreign Earned Income Exclusion (IRC § 911) excludes up to $130,000 of earned income in 2025, indexed for inflation — that is the meaningful US-person lever, not corporate structuring.

Indian residents: treating TCS as a final cost. It is a prepayment. File your return, claim the credit, get the refund if you have overpaid. Form 26AS will show the TCS deposited against your PAN.

EU residents: ignoring exit tax planning. If you are moving outside the EU and hold significant unrealised gains, several jurisdictions (Germany, France, the Netherlands) deem a sale on departure. Plan the year, not the day.

When to consult a qualified professional

The 1% excise is mechanical. You probably do not need an adviser for it. The rules around it are not.

Consult a cross-border tax professional — licensed in both your home and target jurisdictions — before you:

- Change tax residency

- Set up a foreign company while remaining a US person

- Transfer assets above $100,000 abroad as a US person (Form 3520 territory)

- Move from an EU member state with exit tax exposure

- Begin earning foreign-source income while remaining tax-resident in a high-tax jurisdiction

Soveraine is editorial. We do not give individual tax advice. Our editorial policy and disclaimer explain how we work; our affiliate disclosure lists commercial relationships.

Ready to act on this?

Bright!Tax — US expat tax filings (FBAR + FATCA + FEIE specialists). Soveraine readers go to the front of the line through our partner link, and you fund independent editorial in the process.

FAQ

Is there a tax on remittances?

Yes, in the US since 1 January 2026, under IRC section 4475 added by the One Big Beautiful Bill Act. The rate is 1% of the gross transfer amount. It applies only to transfers from inside the US, funded by cash or similar physical instruments such as money orders and cashier's checks. India operates a different mechanism — Tax Collected at Source under the Liberalised Remittance Scheme — at rates between 0.5% and 20% depending on purpose and amount. Most other countries do not impose a direct outbound remittance tax.

What is the 1% remittance tax in 2026?

A federal excise tax on cash-funded cross-border money transfers from the United States, codified at IRC section 4475. The provider collects it at the point of sale and deposits it quarterly with the IRS. There is no minimum threshold and no recipient-country exemption. Transfers funded electronically from a US bank account, or by US-issued debit or credit card, are excluded. The IRS granted penalty relief for failures to deposit during the first three quarters of 2026.

How do I avoid the 1% remittance tax legally?

Fund your transfer from a US bank account or with a US-issued card rather than cash. The statute and IRS Notice 2025-55 exclude account-funded and card-funded transfers from the excise. Services like Wise, Remitly, Xoom, and the online platforms of Western Union and MoneyGram all accept account or card funding. This is not avoidance in any pejorative sense — it is using the rule as drafted. What does not work, and is illegal, is structuring transfers below Bank Secrecy Act reporting thresholds or using unlicensed money transmitters.

Is there a 5% or 3.5% tax on remittances in the US?

No. Earlier drafts of the One Big Beautiful Bill proposed those rates and applied them more broadly, including to non-citizens regardless of funding method. Both were dropped during the legislative process. The enacted statute sets the rate at 1% and limits the base to cash-equivalent funded transfers. Articles still referencing 3.5% or 5% are describing obsolete bill drafts, not current law. If you read a piece dated before mid-2025 citing those numbers, it is out of date.

How do I avoid 20% TCS on foreign remittance from India?

You cannot avoid TCS through structuring — banks report to the income tax department at PAN level, and aggregation across institutions is automatic. What works is treating TCS as the prepayment it is: file your Indian return, claim the credit on Form 26AS, and recover any overpayment as a refund. To minimise cash-flow impact, time large transfers across financial years to use two annual ₹7 lakh thresholds, and use the education-loan funding route (0.5% rate) for tuition remittances where eligible.

Does the US remittance tax apply to wire transfers?

Only to wires funded with cash or a cash equivalent at a teller window. A wire initiated from your online banking, debited from an existing US checking or savings account, is not a q