Renouncing American citizenship is the formal, irrevocable act of ending your status as a US national, usually by swearing an oath before a consular officer abroad. This guide is written for the person actually considering it — most often a US citizen living overseas who has hit the wall of citizenship-based taxation, FATCA banking exclusion, or the cumulative cost of annual compliance. It covers the legal mechanism, the State Department fee, the exit tax, the timeline in 2026 and the mistakes that turn a clean exit into a multi-year tax problem. It does not cover political motivations, and it is not a substitute for advice from a cross-border tax attorney.

Greenback Expat Tax — Streamlined Procedure + amnesty + standard US expat returns

What renouncing American citizenship actually means

Renunciation is one of seven "expatriating acts" listed in Section 349(a) of the Immigration and Nationality Act, codified at 8 U.S.C. § 1481. The relevant subsection for most people is § 1481(a)(5): appearing in person before a US diplomatic or consular officer in a foreign state and signing an oath of renunciation in the form prescribed by the Secretary of State.

The result is a Certificate of Loss of Nationality (CLN), Form DS-4083, approved by the State Department in Washington and returned to the post that took your oath. The CLN is the document banks, foreign tax authorities and immigration officials will ask for. Until it is approved, you are still a US citizen for every legal purpose, including tax.

Two things to understand from the start. First, renunciation is permanent. The Department of State explicitly warns that the act "is irrevocable and cannot be set aside absent successful administrative or judicial appeal" — and successful appeals are rare. Second, it does not by itself close out your tax obligations. Those are handled separately through the IRS, and the two processes do not talk to each other.

Who this applies to — by nationality and residency

The decision to renounce only makes sense in context. The same passport produces very different problems depending on where the holder lives and what other citizenships they hold.

US persons living abroad

This is the core audience. A US citizen tax-resident in another country pays tax in their country of residence and, on top of that, files a US return on worldwide income under the citizenship-based taxation rule confirmed in IRC § 1 and § 61. The Foreign Earned Income Exclusion (USD 126,500 for tax year 2024, indexed annually) and foreign tax credits eliminate double taxation for most wage earners, but they do not eliminate the filing burden, FBAR reporting on FinCEN Form 114, or the FATCA Form 8938 requirement.

For founders, investors and anyone with a foreign company, the picture is worse. GILTI under IRC § 951A and the PFIC rules under § 1297 can produce US tax on foreign business income that has already been taxed locally. Renunciation is the only way to fully escape these rules. A foreign company owned by a non-US person is not a Controlled Foreign Corporation.

EU freelancers and digital nomads with US citizenship

Dual US-EU citizens face the same US compliance burden plus EU rules on tax residency (typically the 183-day test plus centre of vital interests), CFC regimes that vary by member state, and, in several countries, exit taxes when shifting residency. Germany's Außensteuergesetz § 6, France's Article 167 bis CGI and the Netherlands' conserverende aanslag all impose mark-to-market or deferred exit taxes on substantial shareholders. Renouncing the US passport does not change any of that — the EU exit tax is owed to the EU member state, not to the US.

Non-US, non-EU readers

If you are reading this without US citizenship, this article largely does not apply to you. The "renounce to escape worldwide taxation" calculus is a US problem. Most other countries (Eritrea aside) tax on residency, so leaving solves the tax issue without touching the passport. The rest of this guide assumes the reader is a US person.

Legal requirements

To renounce validly under § 1481(a)(5), four conditions must be met:

- Appear in person before a US diplomatic or consular officer.

- Be in a foreign country — renunciation on US soil is only available under the narrower § 1481(a)(6), which is reserved for times of war and effectively never used.

- Sign the oath voluntarily and with the intention of relinquishing US nationality.

- Have legal capacity — be an adult of sound mind. Renunciation by a parent on behalf of a minor is not recognised.

The State Department also expects you to have, or be on track to obtain, another nationality. There is no legal bar to becoming stateless, but consular officers will counsel against it heavily and the 1961 UN Convention on the Reduction of Statelessness makes the consequences severe. In practice, every serious adviser will tell you to secure the second passport in hand before you book the appointment.

How to renounce US citizenship: the step-by-step process

The procedure has not changed materially in years, but the wait times have. Here is the sequence in 2026.

Step 1: Secure a second citizenship

You cannot un-do renunciation. Without another passport, you cannot travel, open a bank account or, in most countries, work legally. Acquire and physically receive your second passport before any other step.

Step 2: Get your US tax affairs in order

The IRS process is separate from the State Department process, but they are linked by Form 8854. You must be able to certify five years of US tax compliance immediately preceding the year of expatriation. If you are behind, the Streamlined Foreign Offshore Procedures are the standard remediation route for non-wilful non-filers and require three years of returns plus six years of FBARs.

Step 3: Book the consular appointment

Each US embassy or consulate sets its own process. Some, like the US Embassy in London, require two appointments — an initial counselling session and a separate oath appointment. Others combine them. Wait times in 2026 range from a few weeks at smaller posts to over a year at high-volume locations like London, Dublin and Toronto. There is no general right to renounce at the post nearest you; some applicants travel to less busy embassies to cut the wait.

Step 4: Attend the appointment and sign the oath

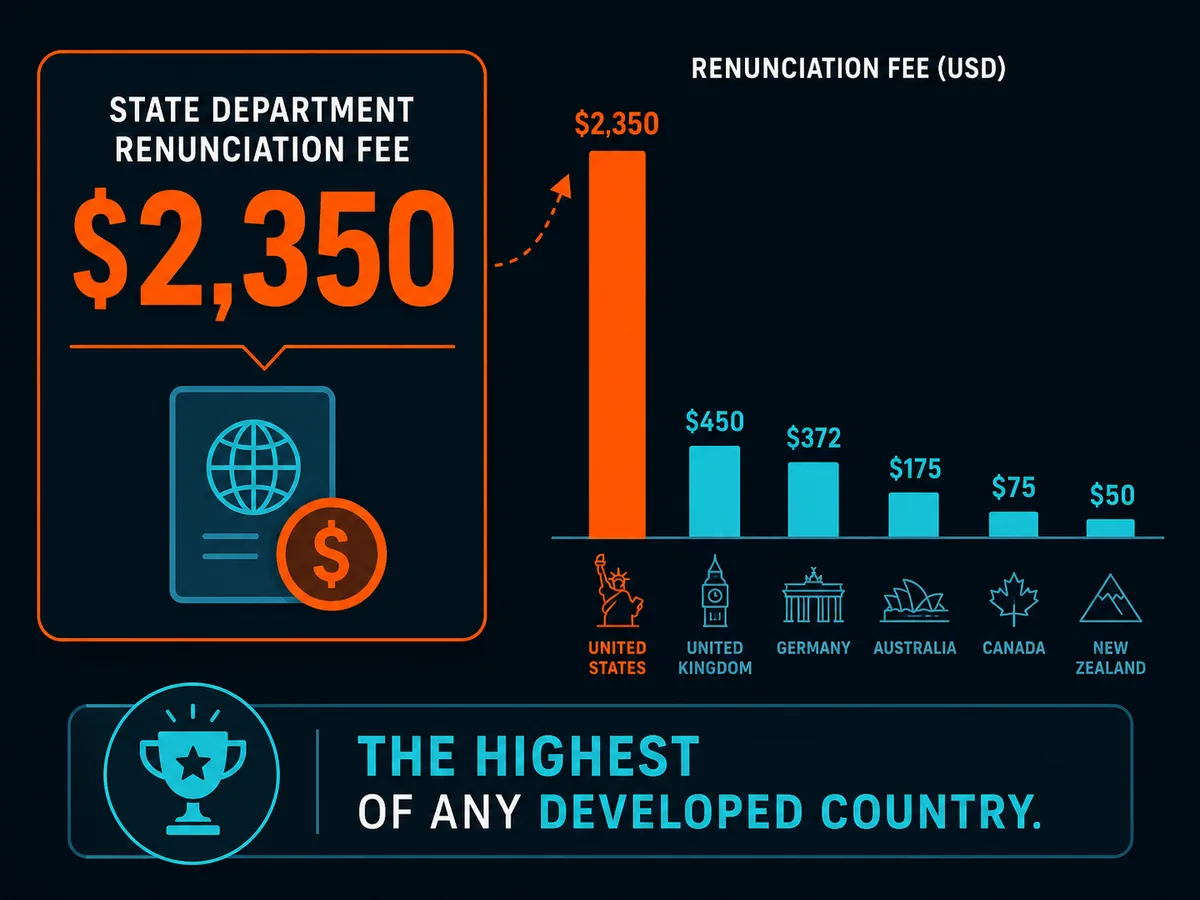

At the appointment you will sign Form DS-4080 (Oath of Renunciation), Form DS-4081 (Statement of Understanding) and Form DS-4079 (Request for Determination). You pay the USD 2,350 fee at the appointment. The consular officer takes your US passport, cancels it and returns it to you. The post then sends the file to the State Department's Office of Legal Affairs in Washington for approval.

Step 5: Wait for the CLN

Approval currently takes three to twelve months from the oath date, depending on the post and case complexity. Your loss of nationality is effective from the oath date — not the CLN approval date — for both nationality and tax purposes.

Step 6: File the final US tax return

The year after the oath, you file a dual-status return covering the period you were still a citizen, plus Form 8854 (Initial and Annual Expatriation Statement). Form 8854 is where you certify five years of compliance and, if applicable, calculate the exit tax. Failing to file it is a USD 10,000 penalty under IRC § 6039G and, more importantly, leaves you classified as a covered expatriate by default regardless of your actual financial situation.

How you may lose US citizenship without formal renunciation

Renunciation under § 1481(a)(5) is the cleanest route, but it is not the only one. The same statute lists six other expatriating acts, all of which require the act plus the intent to relinquish nationality:

- Obtaining naturalisation in a foreign state after age 18 (§ 1481(a)(1))

- Taking an oath of allegiance to a foreign state (§ 1481(a)(2))

- Serving in the armed forces of a foreign state engaged in hostilities against the US, or as a commissioned officer (§ 1481(a)(3))

- Accepting employment with a foreign government if you are a national of that state or take an oath (§ 1481(a)(4))

- Making a formal written renunciation during a state of war (§ 1481(a)(6))

- Committing treason or attempting to overthrow the US government (§ 1481(a)(7))

"Relinquishment" in everyday usage refers to claiming § 1481(a)(1) through (4) after the fact, typically by appearing at a consulate years after a foreign naturalisation and asking for a CLN back-dated to that date. This used to be a tax-planning route — Form 8854 and the exit tax only apply to expatriations on or after 17 June 2008 under the HEART Act. For naturalisations before that date, relinquishment can sidestep the exit tax entirely. The USD 2,350 fee was extended to relinquishment cases in 2015, so the cost is now identical.

What happens when you renounce or lose US citizenship

The immediate consequences are administrative. Your US passport is cancelled. You can no longer enter the United States as a citizen, vote in federal elections, work for the US government or receive consular protection abroad.

The downstream consequences are financial and personal.

Tax filing ends — but only after the final return. Your worldwide income tax obligation ends on the oath date. The IRS treats you as a non-resident alien from that day forward, taxed only on US-source income under IRC § 871 and any applicable treaty.

Estate and gift tax to US persons. If you are a covered expatriate, gifts and bequests from you to a US citizen or resident are subject to a special transfer tax under IRC § 2801 at the highest estate or gift tax rate. This applies indefinitely. Your US-citizen children inherit less, net of tax, than they would have if you had remained a citizen.

Banking. The picture improves abroad and worsens in the US. Foreign banks that have refused or restricted your accounts under FATCA generally accept former citizens once you produce the CLN. US banks are unaffected — you can still hold US accounts as a non-resident alien — but you may face new W-8BEN requirements and treaty-based withholding.

Social Security. Earned retirement benefits continue under the rules in SSA Publication 05-10137, subject to non-resident alien withholding (30 percent on 85 percent of benefits, often reduced by treaty). SSI stops. Medicare cannot be used outside the US, which for most renunciants is moot anyway.

Travel back to the US. Former citizens enter as foreign nationals. Most use the Visa Waiver Program if their new passport qualifies, or a B1/B2 visitor visa. The so-called Reed Amendment (8 U.S.C. § 1182(a)(10)(E)) theoretically bars former citizens who renounced for tax avoidance reasons, but it has effectively never been enforced because the State Department has not published implementing regulations.

The exit tax: the part most people underestimate

The mark-to-market exit tax under IRC § 877A applies to "covered expatriates". You are a covered expatriate if you meet any one of three tests on the day before expatriation:

- Net worth test. Worldwide net worth of USD 2 million or more.

- Tax liability test. Average annual net US income tax for the five preceding years above USD 206,000 for 2025 expatriations (indexed annually — confirm the current figure with IRS Form 8854 instructions).

- Compliance test. Failure to certify five years of US tax compliance on Form 8854.

If you are a covered expatriate, your worldwide assets are deemed sold at fair market value on the day before expatriation. Gain above an exclusion amount (USD 890,000 for 2025, indexed) is taxed at ordinary capital gains rates. Deferred compensation, specified tax-deferred accounts and interests in non-grantor trusts are taxed under separate, harsher regimes — IRAs are treated as fully distributed on the day before expatriation.

The compliance test is the trap. A person worth USD 300,000 who fails to file Form 8854 properly becomes a covered expatriate by operation of law, with all the § 2801 transfer tax consequences that flow from it, even though they have no actual exit tax to pay.

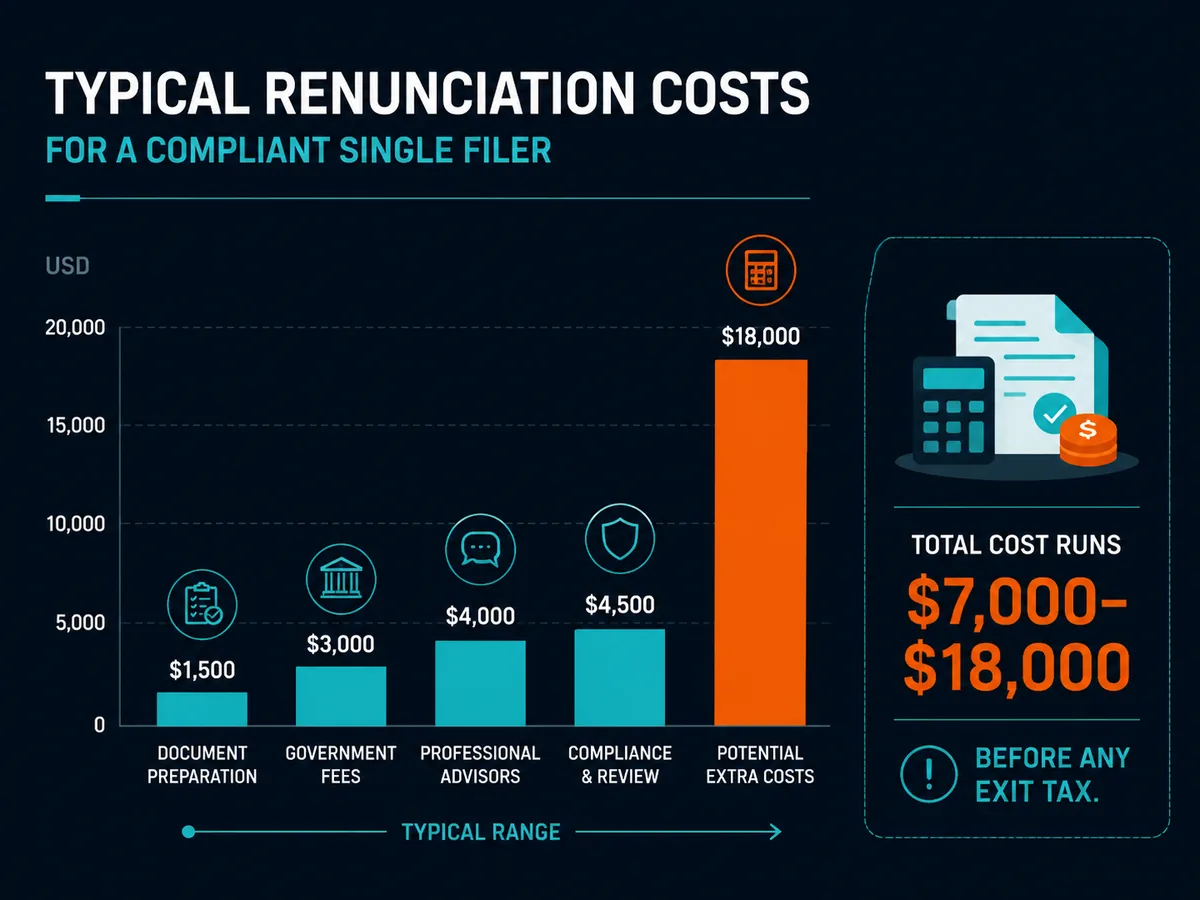

What renouncing American citizenship actually costs

The State Department fee is the smallest line item. Here is a realistic 2026 budget for a straightforward case — single filer, no business interests, fully tax-compliant, net worth under USD 2 million.

| Item | Cost (USD) | Notes |

|---|---|---|

| State Department renunciation fee | 2,350 | Fixed since 2014. Paid at appointment. source |

| Five years of back tax returns (if needed) | 2,000–6,000 | Cross-border CPA fees |

| Streamlined Filing Procedure (if applicable) | 3,000–8,000 | Three returns + six FBARs + statement |

| Form 8854 preparation | 1,500–4,000 | Required even with no exit tax |

| Final dual-status return | 1,000–2,500 | Year of expatriation |

| Second citizenship acquisition | Varies wildly | Naturalisation by residency: filing fees only. Investment programmes: USD 130,000+ |

| Travel to consulate (if not local) | 500–3,000 | Some applicants travel to less busy posts |

| Subtotal for compliant single filer | ~7,000–18,000 | Excluding any actual exit tax |

| Exit tax (covered expatriates) | 0–7 figures | Mark-to-market on net worth above USD 890,000 exclusion |

For a covered expatriate with a concentrated equity position or a successful private company, the exit tax is the dominant cost. Pre-expatriation planning — gifting to a non-US spouse below annual exclusion thresholds, accelerating Roth conversions, restructuring trust interests — can materially reduce the bill but requires lead time of years, not weeks.

How long it takes in 2026

From decision to CLN in hand, plan for 18 to 36 months in most cases:

- Second-passport acquisition: 6 months (citizenship by investment, fastest route) to 5+ years (residency-based naturalisation in most EU countries).

- Tax catch-up via Streamlined Procedure: 3 to 9 months from engagement to filed package.

- Consular appointment wait: 1 to 14 months depending on post.

- CLN approval after oath: 3 to 12 months.

- Final tax filings: filed the year following the expatriation year.

The expatriation date for tax purposes is the oath date, not the CLN date — useful to know because it means you can act on the basis of having expatriated before the certificate arrives.

Common mistakes and how to avoid them

Renouncing before securing a second passport. Statelessness is a serious legal problem. Consular officers may decline to take the oath, but if they accept it, you cannot undo it.

Skipping Form 8854. The form must be filed even if no exit tax is owed. Skipping it makes you a covered expatriate by default and triggers a USD 10,000 penalty.

Assuming relinquishment back-dates the tax exit. Only relinquishment based on a pre-17 June 2008 expatriating act sidesteps the 877A regime. A foreign naturalisation in 2023 with intent to relinquish does not get you out of the exit tax.

Underestimating the IRA and 401(k) treatment. Specified tax-deferred accounts are deemed distributed on the day before expatriation for covered expatriates. The income tax — and 10 percent penalty if under 59½ — falls due immediately on the full account value.

Forgetting about US-citizen children. If a covered expatriate later gifts or bequeaths to US-citizen children, § 2801 transfer tax applies. Many renunciants restructure inheritance plans toward non-US beneficiaries or charitable structures before expatriating.

Treating the exit tax as the only US connection that ends. US-source income — dividends from US stocks, rent from US real estate, capital gains on US real property under FIRPTA — remains taxable. A former citizen with a US brokerage account is still a US taxpayer on that account, just under the non-resident alien rules.

When to consult a qualified professional

For anyone with a net worth above USD 1 million, a foreign company, a non-trivial retirement account, or any tax non-compliance in the past five years, this is not a do-it-yourself project. The cost of getting Form 8854 wrong, or of failing to plan around § 877A, is an order of magnitude larger than the cost of competent advice.

Look for a US tax attorney or CPA who handles expatriation cases routinely — not as a side line — and who works with a cross-border counterpart in your country of residence. The home-country side

Ready to act on this?

Greenback Expat Tax — Streamlined Procedure + amnesty + standard US expat returns. Soveraine readers go to the front of the line through our partner link, and you fund independent editorial in the process.