Most American "move to Portugal" guides skip the hard part: a US citizen who relocates to Portugal remains a US tax filer for life. The Portuguese visa, the Lisbon apartment, the eventual citizenship — none of that changes the IRS's reach. Citizenship-based taxation under the Internal Revenue Code follows the passport, not the postcode. Anyone planning the move who does not understand that mechanic is planning incompletely.

This is the Soveraine hub article for Americans relocating to Portugal in 2026. It covers the visa choice, the Portuguese tax mechanics, the US-side filing reality, the 1994 tax treaty, the citizenship timeline, the real cost stack, and the traps — including the post-Dec-2023 closure of the NHR regime and the AD government's pending proposal to extend naturalisation from five years to ten. It cross-links to the deeper Soveraine pillars on each individual visa, on the foreign tax credit mechanics, and on the bona fide resident test. It is written for prospective movers doing diligence before they commit, not for people already mid-application.

Bright!Tax — US expat tax filings (FBAR + FATCA + FEIE specialists)

Why Portugal — and why the calculus changed in 2023-2025

For the better part of a decade, Portugal was the easiest answer to the question "where in the EU can an American actually move?" The D7 was generous, the Golden Visa accepted real estate, and the non-habitual resident regime offered ten years of capped or zero tax on foreign-source income. Lisbon's English-friendly civil service, mild weather, and lower cost of living than London or Amsterdam made the pitch nearly self-marketing.

Three things changed between October 2023 and the end of 2025.

First, the Golden Visa real-estate route closed in October 2023 under Lei 56/2023. The Golden Visa survived as an investment programme but only via venture-capital funds, R&D contributions, donations, and capital transfers — not property purchase.

Second, the NHR tax regime closed to new applicants on 31 December 2023 under the 2024 State Budget Law (Lei n.º 82/2023). Its replacement, IFICI, is narrowly scoped to scientific research, certified R&D roles, and start-up innovation — covered in detail below. The "ten years of 0% tax in Portugal" pitch is dead for anyone who became tax resident from 1 January 2024 onward.

Third, AIMA — the Agência para a Integração, Migrações e Asilo that replaced SEF in October 2023 (aima.gov.pt) — inherited an appointment backlog it has not yet cleared. Residence-permit conversion appointments in some districts run six to eighteen months out.

Alongside these is the larger political shift. The Aliança Democrática (AD) government elected in March 2024 announced in mid-2025 a proposed reform to the Nationality Law (Lei 37/81) that would extend the naturalisation residency requirement from five to ten years for non-Portuguese-speaking applicants. As of June 2026 the reform is still in draft and has not been enacted, but US applicants should price the possibility into their planning.

Counter-current to all of this: US-citizen inbound migration to Portugal has continued rising through the post-pandemic years, with American demand visible in Lisbon and Porto property markets and in consular processing volumes. The EU's broader regulatory mood softened slightly on residence-by-investment after the Court of Justice's ruling against Malta's citizenship-by-investment programme in April 2025, which sharpened the legal distinction between residence permits (still permitted) and citizenship sales (now closed). Portugal's Golden Visa fund route remained on the residence side of that line and continues to operate.

The honest summary: Portugal is still a good move for many Americans, but it is no longer the special case it was in 2018-2022. The numbers need to be run fresh against Spain's nomad visa, Greece's NIN, Italy's impatriate regime, and Ireland's domicile mechanics.

Who this applies to — read this first

This guide is written for three audience segments, but US persons are the primary readers because the IRS-side mechanics dominate the move. Read the section that matches you.

US persons

Every section of this article applies to you. US citizenship-based taxation under IRC §1 and the worldwide-income rule mean your Form 1040 obligation does not end when you land in Lisbon. You file in the US every year, you file FBAR on foreign accounts above $10,000 aggregate, you watch for PFIC exposure on any European investment fund, and you coordinate Portuguese and US tax positions under the 1994 treaty. Soveraine's bona fide resident pillar covers the FEIE qualification mechanics; the foreign tax credit pillar covers FTC mechanics for the income types the FEIE does not shelter.

EU residents

EU, EEA and Swiss citizens do not need a Portuguese visa. Free movement under Directive 2004/38/EC gives you the right to reside on a registration certificate from the local municipality. The article is still useful for the tax sections, since Portuguese tax-residency rules apply to you the day you cross the 183-day threshold. For the broader non-dom landscape that you may already operate within, see non-dom meaning explained and non-doms.

Non-US, non-EU readers

If you hold a Canadian, UK, Australian, South African, Brazilian, or most Asian or African passports, the visa side of this article still applies — the D7, D8, Golden Visa and Tech Visa are open to you on the same terms as to Americans, and the AIMA process is the same. What differs is the home-country tax exit: your departure from a residence-based tax system can be clean, where an American's cannot. For the deeper nomad-visa-specific analysis, see the digital nomad visa Portugal pillar, written with non-US nomads as a primary audience.

The visa choice

Five routes are realistically available to an American moving to Portugal in 2026. The wrong choice wastes months and money.

D7 (passive income / retirement)

Built for retirees and people living off pensions, dividends, rental income or royalties. Income floor is one times the Portuguese minimum wage — €920 per month for 2026, about $1,000 — with family scaling of +50% for a spouse and +30% per child. Consulates expect a savings buffer of roughly €11,000 (~$12,000) in a Portuguese bank account. Processing 60-90 days at the consulate, plus the AIMA conversion. Best for retired Americans drawing Social Security, dividend income from a US portfolio, or rental income from US property. Deep dive: Portugal D7 visa.

D8 (digital nomad / remote work)

Built for active remote workers earning foreign-source income. Income floor is four times the Portuguese minimum wage — €3,680 per month for 2026, about $4,000 gross. Open to American employees of US companies, freelancers invoicing US or non-Portuguese clients, and owner-operators of US LLCs and S-corps. Processing comparable to D7. Best for mid-career Americans whose employer or freelance business lives in the US. Deep dive: digital nomad visa Portugal.

Golden Visa (post-2024 — investment fund only)

The investment residency programme that survived the October 2023 reform. The qualifying routes are: a €500,000 subscription in a Portuguese-regulated venture-capital or private-equity fund; a €500,000 contribution to research and development activities; a €250,000 donation to artistic production or cultural heritage; or €500,000 capital transfer to a Portuguese business creating jobs. The real-estate route is closed. Minimum stay is only seven days per year, making it the only Portuguese residence that does not require physical presence. Best for high-net-worth Americans wanting EU optionality without moving immediately. Deep dive: Portuguese Golden Visa.

Tech Visa (skilled work)

Routed through the IAPMEI Tech Visa certification scheme for employers in technology and innovation. The employer applies for certification; the employee then receives an expedited 30-day consular decision on a residence visa. Income floor tracks the qualifying employment contract. Best for American engineers, designers and product staff who can secure a job with a certified Portuguese employer before moving — small population in practice, but the fastest route when it fits.

D2 (entrepreneur)

The entrepreneur and self-employed visa under Article 89 of Lei 23/2007. Requires a viable Portuguese business plan, proof of capital sufficient to execute it, and either an established Portuguese company under the applicant's control or a credible plan to incorporate one. No fixed income floor, but consulates evaluate the business plan and personal financial standing. Best for Americans launching a Portuguese business or relocating an existing operation with a real Portuguese presence. Processing runs longer than D7 or D8 because of business-plan adjudication.

The wrong-visa rejection most often happens at the D7/D8 boundary — Americans pitching remote-work salary as "dividend income" routed through a US one-person LLC and applying for the D7. Consulates have wised up. If the income is active employment or freelance work, apply for the D8.

The tax mechanics — Portuguese side

Portugal taxes residents on worldwide income. Residency under Article 16 of the IRS Code (CIRS) is triggered when one of two tests is met: physical presence of more than 183 days in a 12-month period that includes time in the relevant tax year, or maintaining a habitual abode in Portugal at any point in the year — the centre of vital interests test, which catches people who spend less than 183 days but obviously live there.

Once resident, the personal income tax (IRS) applies on a progressive scale. The 2026 bands published by Autoridade Tributária e Aduaneira:

| Taxable income (€) | Marginal IRS rate |

|---|---|

| Up to 8,059 | 13.0% |

| 8,059 – 12,160 | 16.5% |

| 12,160 – 17,233 | 22.0% |

| 17,233 – 22,306 | 25.0% |

| 22,306 – 28,400 | 32.0% |

| 28,400 – 41,629 | 35.5% |

| 41,629 – 44,987 | 43.5% |

| 44,987 – 83,696 | 45.0% |

| Above 83,696 | 48.0% |

A solidarity surcharge of 2.5% applies between €80,000 and €250,000, and 5% above €250,000.

Capital gains on financial assets are generally taxed at a flat 28% for residents, with the option to aggregate into the progressive rate if it produces a lower outcome. Real-estate gains for non-residents are taxed at 28% on the full gain; residents may use the 50% inclusion rule for primary-residence gains and reinvestment rollover for replacement primary residences within the EU/EEA.

AIMI (Adicional ao IMI) — Portugal's wealth tax on real estate — applies on Portuguese-located property holdings above €600,000 per individual (€1.2 million per couple filing jointly), at 0.7% up to €1 million, 1% from €1 million to €2 million, and 1.5% above €2 million. Foreign real estate is outside its scope.

IFICI — the post-NHR regime under Article 58-A of the Tax Benefits Code (EBF), operationalised by Portaria 352/2024 — offers eligible new residents a flat 20% IRS rate on Portuguese-source employment and self-employment income and exemption on most foreign-source income for ten years. Eligibility is narrow: tenured researchers, qualified technical staff at IAPMEI- or AICEP-certified companies, highly qualified roles in R&D-investing companies, and specific roles in start-ups and innovation centres. For a typical retiree or remote-working American, IFICI does not apply. The default is ordinary IRS at the bands above.

The honest summary: an American couple drawing $120,000 a year from a US portfolio and moving to Lisbon under the D7 should plan for combined Portuguese IRS of roughly 30-40% on aggregate worldwide income, partially offset by foreign tax credits on the US side (covered next). The 0% pitch is dead.

The tax mechanics — US side

Becoming Portuguese tax resident does not end any US filing obligation. Every US citizen and lawful permanent resident files a Form 1040 every year, regardless of residence, and reports worldwide income.

The Foreign Earned Income Exclusion (FEIE) under IRC §911 shelters up to $130,000 of qualifying earned income for tax year 2025 (IRS Rev. Proc. 2024-40). It excludes salary, freelance income and self-employment earnings from US income tax, subject to either the bona fide residence test or the physical presence test. It does not exclude: pension income, Social Security, dividends, capital gains, rental income, or anything above the cap. Most Americans on the D7 — drawing precisely the kinds of passive income the D7 is built around — get little or no benefit from FEIE and must rely on the Foreign Tax Credit instead.

The Foreign Tax Credit (FTC) under IRC §901 gives a dollar-for-dollar credit against US tax for income tax paid to a foreign government on the same income. For an American resident in Portugal paying Portuguese IRS at 35-45% on a $150,000 portfolio income, FTC typically eliminates the US tax on that income at the federal level — though state-level exposure remains for Americans tax-domiciled in states like California or New York that do not recognise the FEIE or FTC at parity. Soveraine's foreign tax credit pillar walks through the basketing rules and the carryback/carryforward mechanics.

FBAR — the FinCEN Form 114 — is filed annually by any US person with foreign financial accounts whose aggregate maximum value exceeds $10,000 at any point in the calendar year. It is a reporting form, not a tax form; the penalty for non-filing is up to $10,000 per non-wilful violation per year and far more for wilful violations under 31 USC §5321.

FATCA Form 8938 — required by IRC §6038D — applies above higher thresholds: for unmarried filers living abroad, $200,000 on the last day of the year or $300,000 at any point in the year. Married filing jointly thresholds are double. It is filed with the Form 1040.

PFIC — the biggest trap. Almost every European mutual fund, Portuguese fundo de investimento, and ETF domiciled outside the US is a Passive Foreign Investment Company under IRC §1291-1298. The default §1291 treatment of PFIC gains is punitive: ordinary-income rates on gains spread across the holding period with interest charges that can exceed the gain. A QEF (Qualified Electing Fund) election or a mark-to-market election can mitigate this, but most Portuguese funds do not produce the annual PFIC Annual Information Statement that the QEF election requires. The practical rule for any American in Portugal: keep all investment assets in US-domiciled brokerage accounts (Schwab International, Interactive Brokers, Fidelity International where available). Use Portuguese banks only for current-account, bill-paying and rent purposes.

The US-Portugal tax treaty (1994)

The Convention Between the United States of America and the Portuguese Republic for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with Respect to Taxes on Income was signed in 1994 and entered into force in 1995. It is the operative treaty for any American resident in Portugal in 2026.

What it does. The treaty allocates taxing rights between the two countries to avoid double taxation on most categories of cross-border income. Headline provisions:

- Article 4 (Resident) — defines residency for treaty purposes and provides the tie-breaker rules when an individual is resident under both countries' domestic law: permanent home, then centre of vital interests, then habitual abode, then nationality, then mutual agreement.

- Article 10 (Dividends) — Portugal may tax dividends paid to a US resident at a maximum of 15% (5% for substantial holdings). The US may also tax those dividends, with credit for the Portuguese withholding under FTC mechanics.

- Article 11 (Interest) — generally taxed in the country of residence, with limited source-country withholding.

- Article 12 (Royalties) — capped at 10% in the source country.

- Article 20 (Pensions, Annuities, Social Security) — pensions and similar remuneration paid in respect of past employment are generally taxable only in the recipient's country of residence (so a Portuguese resident American draws their 401(k) into the Portuguese tax base, with US FTC). US Social Security paid to a Portuguese resident is taxable only in the United States under the treaty's specific Social Security carve-out.

- Article 24 (Relief from Double Taxation) — codifies the FTC mechanism that prevents double taxation in practice.

What it does not do. The treaty includes a saving clause at Article 1(3) — the standard provision in US treaties that allows the United States to continue taxing its citizens as if the treaty did not exist, with limited exceptions. For an American in Portugal, this means: the treaty does not let you stop filing US returns, does not exempt you from the US tax system, and does not eliminate FATCA or FBAR. It allocates and coordinates. It does not release.

The 1989 Totalisation Agreement. Separate from the income tax treaty is the US-Portugal Social Security Totalisation Agreement, signed in 1988 and effective from 1 August 1989. It coordinates which country's social-security system covers a worker who has paid into both, allowing periods of contribution to combine for benefit-eligibility purposes. For an American moving to Portugal on the D8 as an employee of a US company, the agreement permits a Certificate of Coverage (US Form 8463) to exempt them from Portuguese Segurança Social contributions for up to five years while remaining on US Social Security. For self-employed Americans, the rules are more nuanced; consult SSA international operations directly.

Citizenship timeline — and the reform pending

Portuguese citizenship under Article 6 of Lei 37/81 is open to any resident who has held a legal residence permit for at least five years, demonstrates A2-level Portuguese via the CIPLE language exam, holds a clean criminal record in Portugal and any country lived in for more than a year after age 16, and shows genuine connection to the Portuguese community. The five-year clock starts from the date the residence permit is issued, not from the visa or arrival date.

For an American on the D7 or D8, the practical sequence is therefore:

- Apply for the visa, receive it, enter Portugal — month 0.

- Attend AIMA appointment, receive two-year residence permit — month 6-18 depending on backlog.

- Renew the permit for three more years at year two — total five years of permit time.

- Apply for citizenship under Article 6 at year five from permit issuance.

- CIPLE A2 exam, criminal-record checks, application processing — typically 12-30 months from application to decision.

Total elapsed time from US departure to Portuguese passport: typically seven to eight years in practice, including processing delays.

Portugal allows dual citizenship, so American applicants do not need to renounce US citizenship to receive a Portuguese passport. The two are held in parallel.

The pending reform. In June 2025, the AD-led government announced a draft reform to Lei 37/81 that would extend the residence requirement to ten years for applicants from outside the CPLP (Comunidade dos Países de Língua Portuguesa) — meaning Americans, Britons, Canadians, Germans, and other non-Portuguese-speaking populations. CPLP nationals (Brazil, Mozambique, Angola, Cape Verde, São Tomé, Guinea-Bissau, East Timor) would retain a five-year threshold. As of June 2026 the reform has not been enacted into law and the five-year rule remains in force. The political question of whether existing residents at the time of any enactment would be grandfathered under the old rule is unresolved.

For US persons, the citizenship calculation has a tail-end consideration: the US exit tax under IRC §877A. An American who later acquires Portuguese citizenship and then chooses to renounce US citizenship is treated as a "covered expatriate" if average annual US income tax for the prior five years exceeds an inflation-adjusted threshold ($201,000 for 2025) or net worth exceeds $2 million. Covered expatriates pay a mark-to-market exit tax on the unrealised gain in all worldwide assets above an exclusion amount ($890,000 for 2025). Soveraine's renouncing American citizenship pillar covers the mechanics. The point is: a Portuguese passport is the entry ticket to renunciation, not renunciation itself.

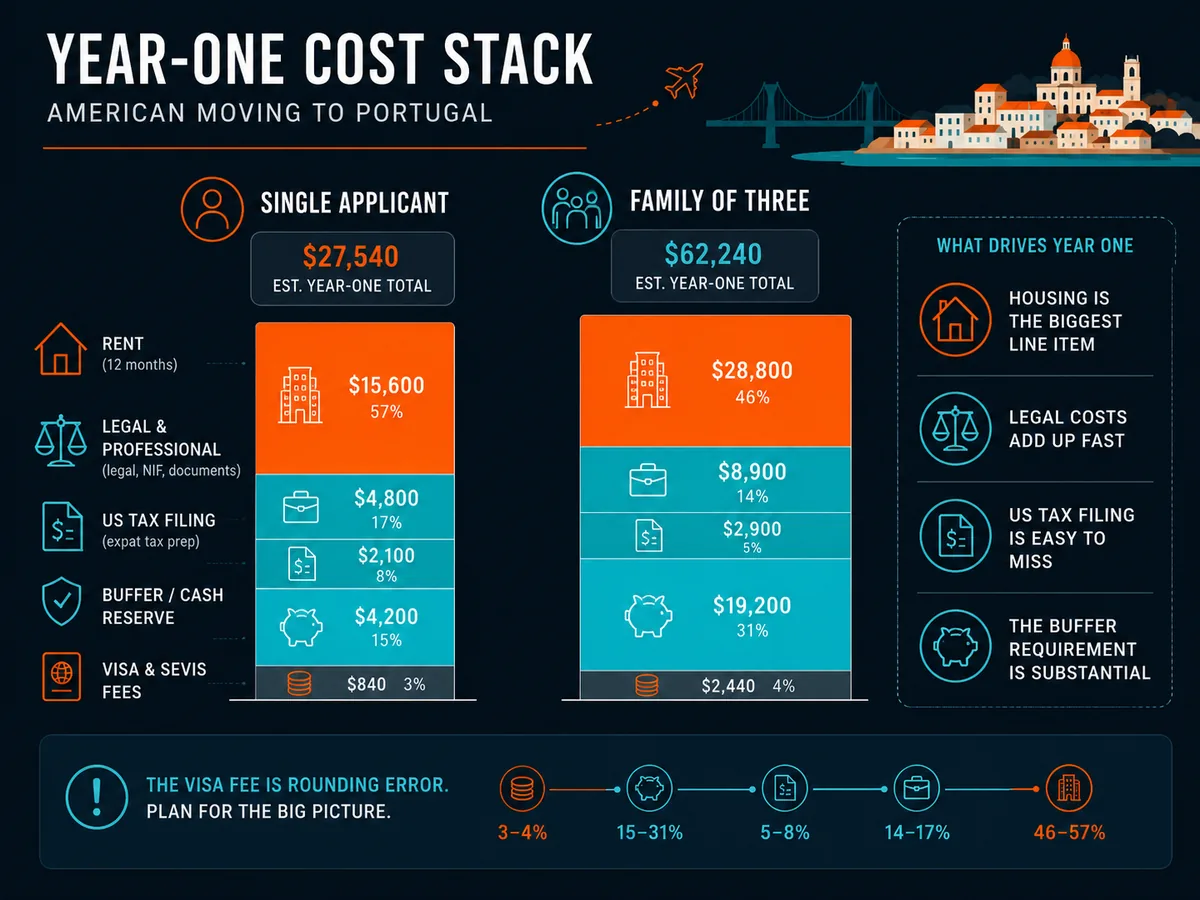

Real-cost stack (year 1)

The published government fees are modest. The real bill is the supporting cost stack, including the US-side dual-filing expense that follows Americans forever.

| Item | Cost (USD) | Notes |

|---|---|---|

| Consular visa fee | $100 per applicant | Roughly €90, varies slightly by consulate |

| AIMA residence permit fee | $185 per applicant | Roughly €170, payable at appointment |

| Document apostilles & translations | $400–$1,000 | FBI background check, state docs, translations |

| Legal/immigration counsel | $3,000–$8,000 | Family of three, full-service Portuguese firm |

| NIF + fiscal representative | $100–$280 | NIF free; representative annual fee while non-resident |

| Portuguese bank account | $0–$330 | Some banks charge non-residents; Millennium BCP and ActivoBank take Americans |

| Health insurance (12 mo. private, pre-SNS) | $550–$1,300 per person | Required for visa; supplement with SafetyWing for travel |

| Rent deposit + first 3 months | $3,500–$10,000 | Lisbon and Cascais higher; interior Portugal lower |

| Savings buffer (consular requirement) | ~$12,000 single, scaled for family | €11,000+ visible in Portuguese account |

| Shipping/movers from US | $4,000–$18,000 | 20-foot container Atlantic, contents-dependent |

| US-side annual tax filing | $1,500–$3,500/year | Bright!Tax, Greenback, or specialist CPA |

| Portuguese annual accountancy | $700–$1,700/year | Higher for self-employed |

| Single American applicant (DIY-leaning) | ~$18,000–$35,000 | Excluding savings buffer |

| Family of three with counsel | ~$30,000–$60,000 | Excluding savings buffer and shipping luxury items |

For the financial infrastructure — moving deposit money, paying Portuguese bills in euros while still earning in dollars, multi-currency accounts — most American movers set up a Wise account before they leave the US. For travel and gap-period health coverage in the months before SNS access, SafetyWing covers the pre-permanent insurance layer.

Visa comparison

The short answer to "which visa do I need?" for an American moving in 2026:

| Visa | Income / investment floor | Tax regime | Years to citizenship | Best for |

|---|---|---|---|---|

| D7 | €920/mo passive income (~$1,000) | Standard IRS (NHR closed) | 5 (10 if reform passes) | Retirees, dividend/pension income |

| D8 | €3,680/mo active foreign income (~$4,000) | Standard IRS (NHR closed) | 5 (10 if reform passes) | Remote employees and freelancers |

| Golden Visa | €250k donation / €500k fund | Standard IRS if resident | 5 (10 if reform passes) | HNW Americans wanting EU optionality |

| Tech Visa | Employment contract via IAPMEI-certified employer | Standard IRS; IFICI possible if eligible | 5 (10 if reform passes) | Engineers and product staff with a Portuguese job offer |

| D2 | Business plan + capital | Standard IRS | 5 (10 if reform passes) | Entrepreneurs incorporating in Portugal |

The choice is rarely close at the margin. Passive income + retirement → D7. Remote salary or freelance income → D8. Real money to invest, want optionality, do not need to move immediately → Golden Visa. Job offer with a certified Portuguese employer → Tech Visa. Real Portuguese business to build → D2.

For most American readers — retiring 55-70 year-olds with portfolios, 401(k)s, and Social Security — the answer is D7. For mid-career remote workers earning $50,000+ from US employers — D8. The other three are niche.

The traps

The PFIC trap is the single biggest American-specific failure. Walking into a Portuguese branch of Millennium BCP, BPI or Novo Banco and being offered a "balanced investment fund" is the start of years of punitive US tax filings. Keep all investment assets US-domiciled. Use Portuguese banks only for current-account purposes. This trap is large enough that Soveraine repeats it in every Portugal pillar.

The AIMA backlog. Residence-permit conversion appointments in some districts now run six to eighteen months out. The visa remains valid through the wait if the appointment is booked in time, but life without the residence card is friction-heavy: opening some Portuguese bank accounts becomes harder, SNS enrolment is delayed, some travel becomes complicated. Book the AIMA appointment the day you land in Portugal, not the week after.

Trying to relocate on the 90-day Schengen visa-waiver entry. US citizens enjoy 90 days in 180 visa-free entry to the Schengen area for tourism. This is not a relocation pathway. AIMA does not regularise visa-waiver entry into residence. Apply for the correct national long-stay visa from a Portuguese consulate in the US before moving. Trying to "fly in and figure it out" creates an out-of-status problem that takes months and significant legal cost to resolve, when it can be resolved at all.

Assuming NHR is still available. It is not, for anyone who became tax resident on or after 1 January 2024. Marketing pages, immigration-firm blog posts, and YouTube videos that still pitch "10 years of 0% tax in Portugal" are either out of date or wrong. Plan tax exposure on standard Portuguese rates unless you genuinely qualify for IFICI's narrow scope.

Forgetting state-level US tax. California, New Mexico, South Carolina and Virginia in particular tend to consider former residents tax-domiciled until they affirmatively establish a new domicile elsewhere. The federal FEIE does not bind state revenue agencies. Americans moving from these states should sever state ties (driver's licence, voter registration, vehicle registration, property tax exemptions) deliberately before the move, with a US-side CPA's guidance. The cleanest pre-move move for some Americans is a year in a no-state-tax state (Florida, Texas, Nevada, Tennessee, Washington, Wyoming, South Dakota, Alaska) before the international relocation.

Treating the US-Portugal treaty as an exit ticket. It is not. The saving clause preserves US taxation of US citizens regardless of treaty residence. The treaty allocates and prevents double taxation. It does not end the IRS relationship.

Banking refusals. Several Portuguese banks decline US-person account applications because FATCA compliance costs exceed the deposit value of an individual American customer. Millennium BCP and ActivoBank are the names that recur in 2026 as Americans-friendly. Plan to open in person on a Portuguese visit before the move, or use a relocation lawyer's bank contacts.

When to consult a professional

A handful of decision points justify professional help before acting:

- Tax planning before becoming Portuguese resident. Realising capital gains, restructuring a US LLC or S-corp, timing dividend distributions, contributing to a Roth before residency starts, executing Roth conversions — all decisions best made before the 183-day clock starts.

- US expat tax filing. Non-optional from year one. PFIC exposure alone justifies the fee. Bright!Tax and Greenback are the two most-cited specialists in Soveraine's reader correspondence.

- Estate planning across the US-Portugal divide. The US estate tax follows US-citizen domiciliaries on worldwide assets. Portuguese inheritance is governed by Regulation (EU) No 650/2012 (Brussels IV), which allows election of governing law. Coordinated planning matters for any American with material assets.

- Pre-renunciation analysis. Americans considering eventual renunciation after acquiring Portuguese citizenship need IRC §877A modelling years before the actual renunciation.

For travel-document tracking during the residency years, iVisa handles the visa-on-arrival paperwork most American Portuguese residents need for non-Schengen travel. For the broader second-passport conversation — including non-Portuguese options some Americans consider in parallel — Henley & Partners handles the citizenship-by-investment market end-to-end.

See our editorial policy on professional advice and our affiliate disclosure for how we handle service recommendations.

Ready to act on this?

Bright!Tax — US expat tax filings (FBAR + FATCA + FEIE specialists). Every American who moves to Portugal needs a US expat CPA from day one. Soveraine readers go to the front of the line through our partner link, and you fund independent editorial in the process.

FAQ

Can a US citizen just move to Portugal?

Not on the 90-day Schengen visa-waiver entry, which is for tourism only. To relocate, a US citizen needs a Portuguese national long-stay visa (D7, D8, Tech Visa, D2, or the post-2024 Golden Visa fund route) issued by a Portuguese consulate in the US before the move. Entering on the visa waiver and trying to convert in-country is one of the most common failure modes — AIMA does not regularise it. Apply for the correct visa from Washington, San Francisco, New York or another consulate covering your jurisdiction, then enter Portugal on that visa, then attend an AIMA appointment to convert it into a residence permit.

How much money do you need to move to Portugal from the US?

Realistic year-one budget for a single American applicant: $18,000–$35,000 covering visa fees, AIMA processing, document apostilles and translations, legal counsel, Portuguese health insurance, three to six months of rent and deposits, NIF and bank-account setup, US-side dual tax filing, and a savings buffer of roughly €11,000 (about $12,000) that the consulate expects to see. A family of three with legal representation typically runs $30,000–$60,000 in year one, before furniture and shipping.

Do Americans pay US taxes if they live in Portugal?

Yes. The United States taxes its citizens on worldwide income regardless of where they live — the only major country besides Eritrea to do so. An American resident in Portugal files a US Form 1040 every year on top of the Portuguese IRS return, claims the Foreign Earned Income Exclusion (up to $130,000 of earned income for 2025) or the Foreign Tax Credit, files FBAR (FinCEN Form 114) for foreign accounts above $10,000 aggregate, and files Form 8938 under FATCA above higher thresholds. The 1994 US-Portugal tax treaty avoids double taxation on most income types but does not end US filing obligations.

Is NHR still available for Americans moving to Portugal?

No. The non-habitual resident regime closed to new applicants on 31 December 2023 under Lei 82/2023. Anyone who became Portuguese tax resident from 1 January 2024 cannot apply. The replacement, IFICI (Incentivo Fiscal à Investigação Científica e Inovação), offers similar benefits — a flat 20% IRS rate on Portuguese-source professional income and exemption on most foreign-source income — but is narrowly scoped to scientific researchers, certified technical staff, and qualifying R&D and start-up roles. Most retirees, remote workers and ordinary American movers do not qualify.

How long until a US citizen can get Portuguese citizenship?

Currently five years of legal residence under Article 6 of the Nationality Law (Lei 37/81 as amended), starting from the date the residence permit is issued — not from the visa or arrival date. The AD-led government elected in 2024 proposed extending this to ten years for non-Portuguese-speaking applicants under a draft reform announced in June 2025. As of June 2026 the reform has not been enacted into law and the five-year rule remains in force, but applicants should plan for the possibility of a longer timeline. Portugal allows dual citizenship, so US citizens do not need to renounce — though Americans should weigh the US exit tax under IRC §877A before any later renunciation.

What is the PFIC trap for Americans in Portugal?

Almost every Portuguese and EU mutual fund, ETF, and "smart" investment account is a Passive Foreign Investment Company under US tax law (IRC §1291–1298). A US person who buys one owes punitive PFIC tax via Form 8621 — either the default §1291 method, which treats gains as ordinary income spread over the holding period with interest charges that can exceed the gain, or a mark-to-market or QEF election if available. The practical rule: keep all investment assets in US-domiciled brokerage accounts. Use Portuguese banks only for current-account and bill-paying purposes.

Does Portugal tax US Social Security and 401(k) distributions?

Under the 1994 US-Portugal tax treaty, US Social Security paid to a Portuguese tax resident is taxable only in the United States (Article 20). 401(k) and IRA distributions are more complex: the treaty generally permits Portugal to tax pension distributions paid to its residents (Article 20 paragraph 1), with a foreign tax credit available on the US side. The 1989 US-Portugal Totalisation Agreement coordinates Social Security contribution liability but does not change the income-tax treatment. Plan with a CPA who handles US-Portugal returns before drawing significant pension income.

What is the AIMA backlog and does it affect Americans?

AIMA — the Agency for Integration, Migration and Asylum that replaced SEF in October 2023 — has run a persistent appointment backlog since taking over, with residence-permit conversion appointments in some districts scheduled six to eighteen months out. It affects Americans the same as any other nationality. The visa remains valid through the wait if the appointment is booked in time, but life in limbo without the residence card is harder: banking, healthcare enrolment in the SNS, and some travel becomes friction-heavy. Book the AIMA appointment the day you land.

Sources

- US-Portugal Income Tax Treaty (1994) — IRS treaty documents — https://www.irs.gov/businesses/international-businesses/portugal-tax-treaty-documents

- IRS Publication 54 (Tax Guide for US Citizens and Resident Aliens Abroad) — https://www.irs.gov/publications/p54

- IRS Publication 519 (Tax Guide for Aliens) — https://www.irs.gov/publications/p519

- IRS Rev. Proc. 2024-40 (2025 inflation-adjusted FEIE) — https://www.irs.gov/pub/irs-drop/rp-24-40.pdf

- FinCEN BSA E-Filing (FBAR / Form 114) — https://bsaefiling.fincen.treas.gov/main.html

- IRS Form 8938 (FATCA reporting) — https://www.irs.gov/forms-pubs/about-form-8938

- IRC §911 (Foreign Earned Income Exclusion) — https://www.law.cornell.edu/uscode/text/26/911

- IRC §901 (Foreign Tax Credit) — https://www.law.cornell.edu/uscode/text/26/901

- IRC §1291–1298 (PFIC) — https://www.law.cornell.edu/uscode/text/26/1291

- IRC §877A (Expatriation tax) — https://www.law.cornell.edu/uscode/text/26/877A

- AIMA — Agência para a Integração, Migrações e Asilo — https://aima.gov.pt/

- Autoridade Tributária e Aduaneira (Portuguese Tax Authority) — https://www.portaldasfinancas.gov.pt/

- Lei 23/2007 (Portuguese foreigners' law) — https://dre.pt/dre/legislacao-consolidada/lei/2007-34536475

- Lei 37/81 (Portuguese Nationality Law) — https://dre.pt/dre/legislacao-consolidada/lei/1981-34530775

- Lei 82/2023 (2024 State Budget — NHR closure) — https://dre.pt/dre/legislacao-consolidada/lei/2023-82-220231229

- Lei 56/2023 (Mais Habitação — Golden Visa real-estate closure) — https://dre.pt/

- Portuguese national visas — official MNE portal — https://vistos.mne.gov.pt/en/national-visas/general-information

- US Social Security Administration — Portugal Totalisation Agreement — https://www.ssa.gov/international/Agreement_Pamphlets/portugal.html

- CJEU judgment on Malta citizenship-by-investment (Case C-181/23, April 2025) — https://curia.europa.eu/

- Regulation (EU) No 650/2012 (Brussels IV — succession) — https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=celex%3A32012R0650