The D7 is Portugal's residence visa for people who can support themselves from income earned outside the country — pensions, dividends, rental yield, royalties, or a remote salary that meets the threshold. It is the route most retirees and lower-budget movers take, and it remains open in 2026 despite the closure of the Golden Visa real-estate option and the old non-habitual resident tax regime.

La Vida Golden Visas — UK-based golden-visa specialist

This article covers what the D7 actually requires, what it costs, the tax exposure it triggers, and where the rules differ depending on your passport. It does not cover the Golden Visa (a separate investment route) or the D2 entrepreneur visa. It is written for prospective applicants doing diligence before they commit — not for people already in the application queue looking for paperwork shortcuts.

What the D7 visa is

The D7 is a national long-stay visa created under Article 61 of Law 23/2007 (the foreigners' law) and its implementing Decree-Law 84/2007. It permits a non-EU national with stable, recurring income to enter Portugal, then apply for a two-year residence permit through AIMA (the Agency for Integration, Migration and Asylum, successor to SEF since October 2023).

The two-year permit renews for three more years. After five years of legal residence, the holder can apply for permanent residence or Portuguese citizenship.

The D7 sits next to the D8 digital nomad visa (for active remote income above a higher threshold) and the Golden Visa (investment route, now limited to fund and capital-transfer options after the October 2023 reform). Knowing which route fits is the first decision — getting it wrong wastes six months at the consulate.

Who this applies to — and the parts that change by passport

The application paperwork is roughly the same for everyone. The tax and reporting consequences are not. Read the segment that matches your situation before doing anything else.

US persons (citizens and green-card holders)

US citizenship-based taxation does not stop at the Portuguese border. You continue to file a Form 1040 every year regardless of where you live, and you owe US tax on worldwide income. The Foreign Earned Income Exclusion (IRS Publication 54) shelters up to $130,000 of earned income in 2025 for qualifying residents, but it does not cover pension, dividend or rental income — exactly the income sources the D7 is built around.

FBAR (FinCEN Form 114) and FATCA (Form 8938) reporting kicks in on Portuguese bank accounts above the thresholds. Several Portuguese banks refuse US-person accounts entirely because of FATCA compliance costs. Plan to open an account in person with a bank that takes Americans — Millennium BCP and ActivoBank are the names that recur in 2026.

The US-Portugal tax treaty (full text via Treasury) provides foreign tax credit mechanics to avoid double taxation, but you will likely owe additional US tax on Portuguese-source income each year. Speak to a US-licensed CPA who handles expatriate returns before you move, not after.

EU freelancers and digital nomads

If you hold an EU passport, you do not need the D7 — free movement under Directive 2004/38/EC gives you the right to reside in Portugal on a registration certificate. Skip to the tax section.

If you are an EU resident on a non-EU passport, the D7 is open to you, but watch the exit-tax and CFC implications in your departing country. Most EU states treat a change of tax residency as a deemed disposal event for unrealised gains on substantial shareholdings — Germany's exit tax under § 6 AStG and France's exit tax under Article 167 bis CGI are the well-known examples.

The 183-day rule and "centre of vital interests" test under the OECD Model Tax Convention Article 4 will determine when you become Portuguese tax resident and cease to be resident in your home country. Treaty tiebreakers matter — getting both jurisdictions to agree you are no longer resident in the old one requires evidence, not just a flight booking.

Non-US, non-EU readers

Holders of Canadian, UK, Australian, South African, Brazilian, and most Asian passports have the cleanest path. Your home tax system is generally residence-based, so leaving genuinely ends your tax exposure (UK split-year treatment under SRT, Canada's departure-tax rules in T1243/T1244, Australia's residency tests).

CFC rules in your old country may still bite if you keep a foreign company, but for most retirees and remote workers, a clean break is achievable. This is the segment for whom the D7 works closest to how marketing materials describe it.

D7 income requirements

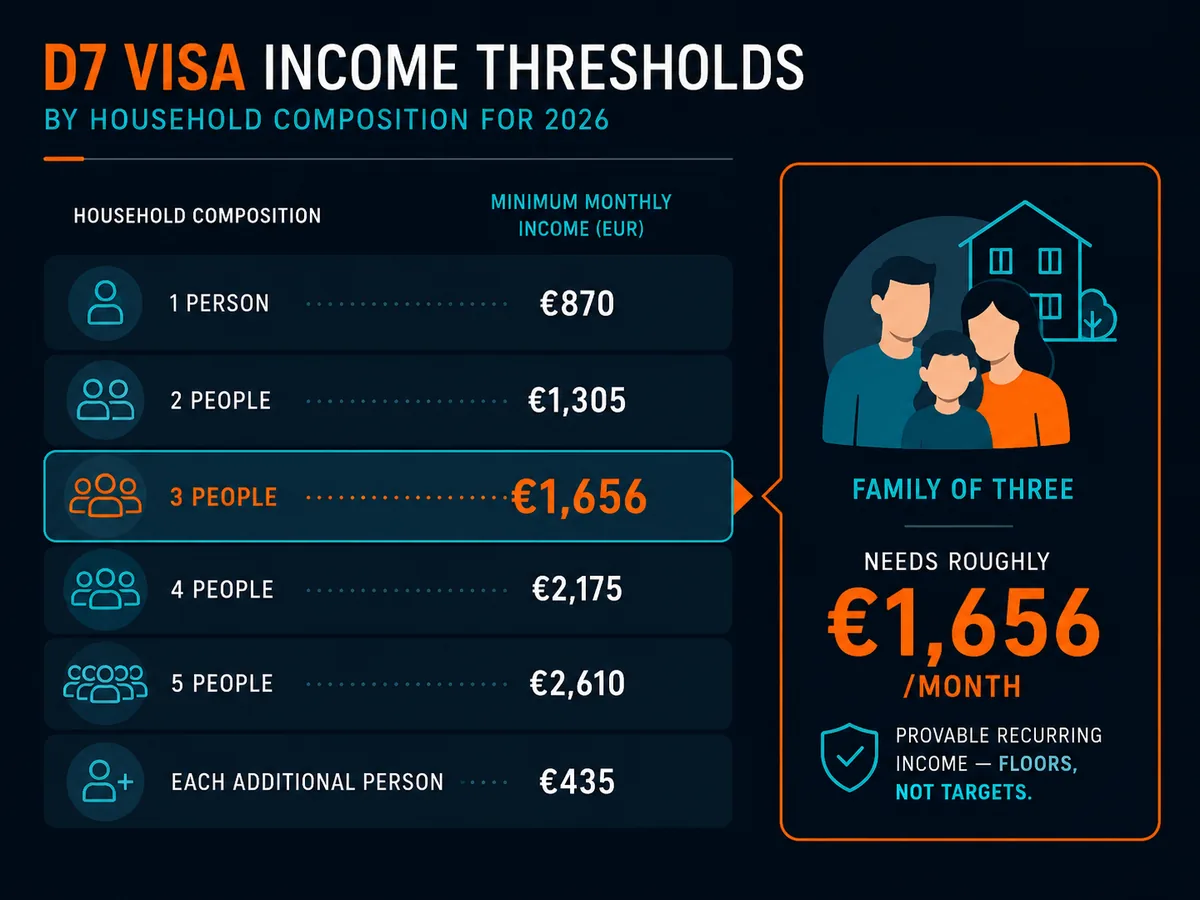

The income threshold is pegged to the Portuguese minimum wage, which rose to €870 per month for 2025 and is set to €920 per month for 2026 under the budget law. Consulates expect:

| Applicant | Monthly income | Annual equivalent |

|---|---|---|

| Main applicant | 100% (€920) | €11,040 |

| Spouse | +50% (€460) | +€5,520 |

| Each child | +30% (€276) | +€3,312 |

A family of three (two adults, one child) therefore needs roughly €1,656 per month of provable, recurring income, or just under €20,000 per year. These are floors, not targets. Consulates routinely approve applicants showing 1.5x to 2x the threshold and reject borderline cases. Aim higher than the minimum.

What counts as qualifying income:

- Government and private pensions

- Dividends from listed or private companies (with two to three years of history)

- Rental income from property you own

- Royalties and licensing income

- Annuities and structured payouts

- Interest from substantial deposits or bonds

What sits in a grey zone:

- Active remote-work salary — consulates increasingly route these to the D8

- Freelance / contractor income — same issue

- Cryptocurrency yield — rarely accepted without supporting documentation

The savings buffer is separate. Plan to show roughly 12 months of the threshold as liquid funds in a Portuguese bank account opened before submitting the application — around €11,040 for a single applicant, more for families.

Eligible dependants

Family reunification under Article 98 of Law 23/2007 allows the D7 holder to bring:

- Spouse or registered partner (including same-sex)

- Minor children of either spouse

- Adult children under 26 who are unmarried, financially dependent, and in education

- Dependent parents of either spouse (typically over 65, or younger if proven dependent)

- Minor siblings under legal guardianship

Each dependant files their own application but can be processed together with the main applicant or follow afterwards. Filing together is usually cheaper and faster.

Renewals and minimum stay

The initial D7 visa is valid for four months — long enough to enter Portugal and attend the AIMA appointment that converts it into a two-year residence permit. The two-year permit renews once for a further three years, then converts to permanent residence or supports a citizenship application.

The minimum stay rule under Article 85 of the foreigners' law: residence permit holders cannot be absent from Portugal for more than six consecutive months or eight months total within the two-year permit period. The D7 is not a backup residence to keep in your back pocket while living elsewhere — it requires real presence.

For most applicants, real presence also means crossing the 183-day Portuguese tax-residency threshold, which is the point at which Portugal taxes your worldwide income.

Application requirements and procedure

The standard document list:

- D7 visa application form — available from your nearest Portuguese consulate

- Passport valid for at least three months beyond the visa expiry, with two blank pages

- Two passport photographs to ICAO specification

- Proof of income — pension statements, dividend records, rental contracts, tax returns covering 12 months minimum

- Proof of accommodation in Portugal — 12-month rental contract, property deed, or notarised letter from host

- Portuguese bank account with the buffer funds deposited

- Criminal record certificate from every country you have lived in for more than one year since age 16, apostilled and translated

- Authorisation for AIMA criminal record check — a Portuguese-specific form

- Health insurance valid in Portugal until the residence permit appointment, then PB4 (treaty cover) or SNS registration

- NIF (Número de Identificação Fiscal) — Portuguese tax number, obtained through a fiscal representative if abroad

- Cover letter explaining the move and income sources

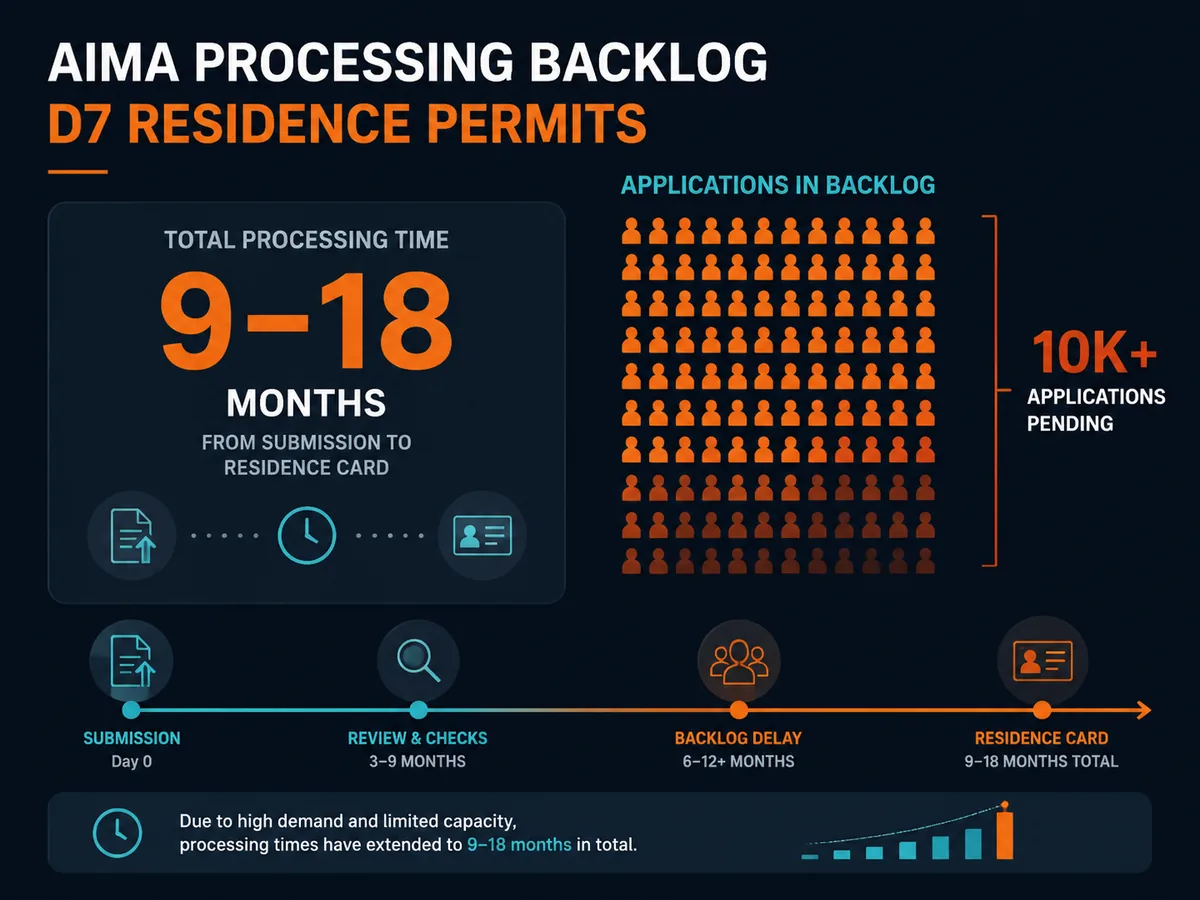

Submit at the consulate covering your jurisdiction. Processing runs 60-90 days for the visa itself, plus the AIMA appointment after arrival. Total elapsed time from initial submission to residence card in hand is now typically 9-18 months given the AIMA backlog [source: TODO — current AIMA processing-time statement].

The AIMA appointment is non-negotiable. Without it, the visa expires and you must start over.

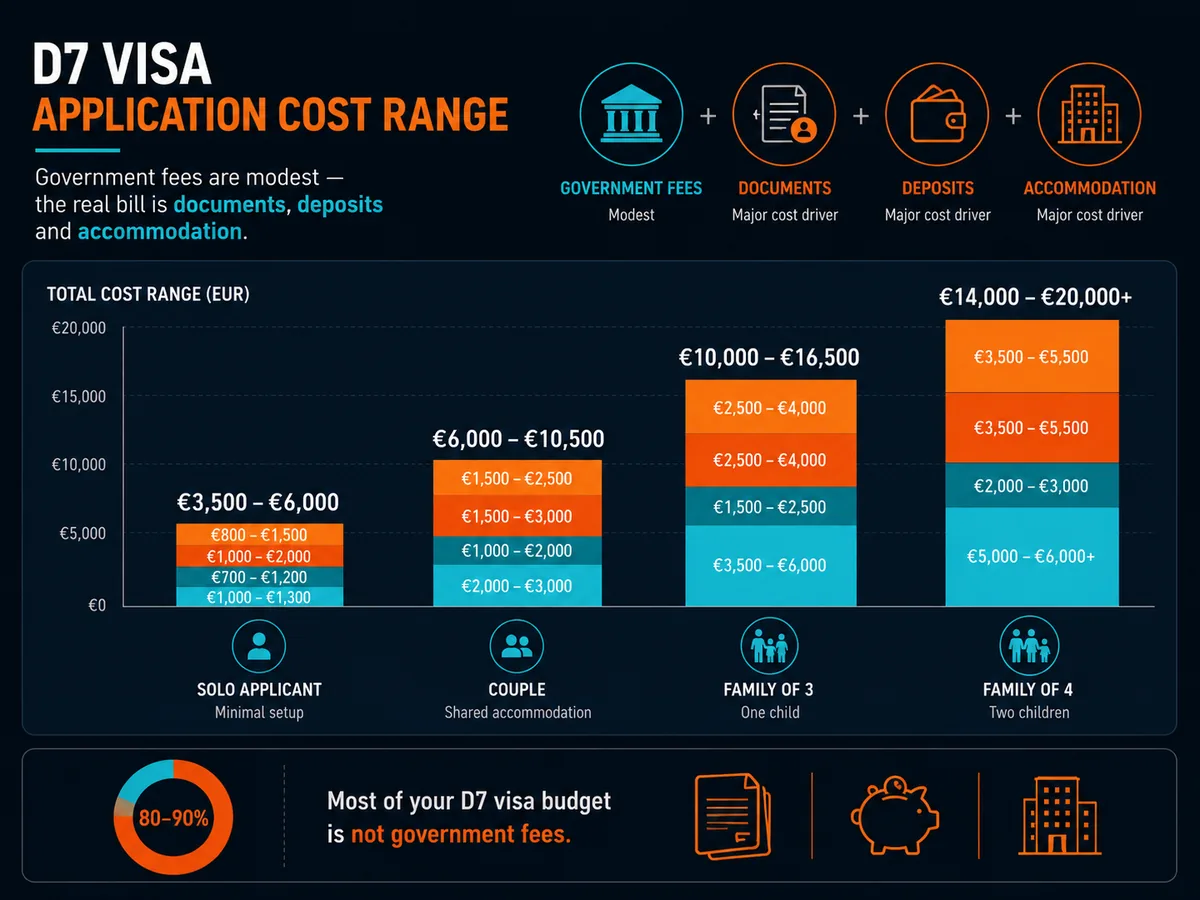

Realistic costs

The published government fees are modest. The real bill is the supporting cost stack.

| Item | Cost (€) | Notes |

|---|---|---|

| Consular visa fee | 90 | Per applicant |

| AIMA residence permit fee | ~170 | Per applicant, at the appointment |

| Document apostilles & translations | 300-800 | Varies by country of origin |

| NIF via fiscal representative | 100-250 | Annual fee if you stay non-resident initially |

| Criminal record certificates | 50-200 | Per jurisdiction |

| Portuguese bank account opening | 0-300 | Some banks charge non-residents |

| Health insurance (12 months) | 400-900 | Per applicant |

| Rental deposit + first month | 2,000-5,000 | Lisbon/Porto higher |

| Notarised lease (if required) | 50-150 | Some consulates require this |

| Legal / immigration support (optional) | 1,500-4,500 | Per family, full service |

| Total per single applicant (DIY) | ~3,200-7,500 | Excluding moving costs |

| Total per family of three (with lawyer) | ~8,000-15,000 | Excluding moving costs |

[source: TODO — verify current AIMA fee schedule from the official AIMA fees page]

A DIY application is genuinely possible if you read Portuguese reasonably well and can travel to the consulate. A lawyer is worth the spend if you have unusual income sources, a US passport (FATCA banking issues), or dependants with complex documentation.

Common mistakes

Showing one-off income. Three months of dividend payments is not "stable, recurring income". Build a 12-24 month track record before applying.

Renting on Airbnb for the proof-of-accommodation document. Consulates have wised up. You need a registered 12-month lease, ideally with the landlord's NIF and tax stamp, or a property deed in your name.

Forgetting the criminal record certificate from countries you only lived in briefly. Spent a year teaching English in Vietnam in 2018? You need a Vietnamese police certificate. Refusals on this point are common and cost months.

Assuming the old NHR tax regime still applies. It does not. The non-habitual resident scheme closed to new entrants on 31 December 2023 under the 2024 State Budget Law. The replacement IFICI scheme is narrow and aimed at scientific and technical workers — most D7 retirees and remote workers do not qualify. Plan your tax position on ordinary Portuguese rates, not NHR.

Using a US LLC or offshore company to "receive" the income. US persons: this does nothing for your US tax position and creates Portuguese reporting on the underlying entity. Non-US persons: Portuguese CFC rules under the CIT Code can attribute company income to you personally if the entity is in a low-tax jurisdiction. Take advice before structuring.

Missing the AIMA appointment. The visa is only the entry ticket. The residence permit is what you actually need. Book the appointment the day you arrive.

When to consult a qualified professional

The D7 application itself is administrative — most people can run it themselves if they read carefully. The places where professional advice pays for itself:

- Tax planning before you become Portuguese resident. Decisions about realising capital gains, restructuring company holdings, or timing dividend distributions are best made before the 183-day clock starts.

- US persons on FATCA, FBAR, GILTI and PFIC exposure. A US expat CPA is non-optional. Portuguese investment funds are PFICs under US rules — buying one without advice is expensive.

- Exit tax in your departing country. EU departures in particular need a tax lawyer in the old jurisdiction.

- Complex family situations — non-marital partners, children from previous relationships, dependent parents in third countries.

A Portuguese immigration lawyer typically charges €1,500-€4,500 for a full family D7 service. A US expat CPA runs $1,500-$3,500 per year for the ongoing return. Both are cheaper than the alternative.

See our editorial policy on professional advice and our affiliate disclosure for how we handle service recommendations.

FAQ

Who is eligible for the D7 visa in Portugal?

Any non-EU, non-EEA, non-Swiss national over 18 who can show stable, recurring passive or remote income above the Portuguese minimum wage threshold (€920 per month in 2026), proof of accommodation in Portugal, a clean criminal record, and valid health insurance. Pensions, dividends, rental income, royalties and remote-work salary are the typical income sources accepted by consulates. Dependants — spouse, minor children, dependent parents and dependent adult children in education — can be added under family reunification rules set out in Law 23/2007.

How much money do you need in the bank for a D7 visa?

There is no single statutory savings figure, but consulates expect to see roughly 12 months of the minimum wage saved as a buffer — about €11,040 for the main applicant in 2026, plus 50% for a spouse (€5,520) and 30% per child (€3,312). This sits on top of the monthly income requirement. Some consulates ask for more, particularly Washington and London. Show the funds in a Portuguese bank account opened before applying — a step every successful applicant takes.

What are the disadvantages of the D7 visa?

Three real downsides. First, the minimum stay rule: you cannot be outside Portugal for more than six consecutive months or eight non-consecutive months in any two-year permit period. Second, tax residency — spending 183+ days a year in Portugal makes you tax resident on worldwide income, and the old non-habitual resident regime closed to new entrants in 2024. Third, AIMA processing backlogs have pushed residence-permit appointments to 12-18 months in some districts.

Is Portugal still welcoming American expats?

Yes, but the regime has tightened. The D7 remains open to Americans and consulates in Washington, San Francisco and New York continue to process applications. What changed: the non-habitual resident tax regime closed to new arrivals after 31 December 2023, replaced by the narrower IFICI scheme aimed at scientific and technical workers. Property prices in Lisbon and Porto have risen sharply, and the Golden Visa real-estate route closed in October 2023. American applicants should also budget for FATCA-driven banking friction.

What is the difference between the D7 and D8 visa?

The D7 is for passive income — pensions, dividends, rental income, royalties. The D8, introduced in October 2022, targets remote workers earning active employment or freelance income from foreign clients. The D8 requires roughly four times the minimum wage (around €3,680 per month in 2026) versus the D7's one times minimum wage. If your income is salary from a foreign employer or active freelance work, the D8 is the correct route — consulates have started refusing D7 applications based on remote-work income.

Does the D7 visa lead to Portuguese citizenship?

Yes, on the same timeline as other residence routes. After five years of legal residence under the D7, you can apply for permanent residence or Portuguese citizenship under Article 6 of the Nationality Law. Citizenship requires A2-level Portuguese (the CIPLE exam), a clean criminal record in Portugal and any country where you lived after age 16, and proof of genuine connection to the community. Portugal allows dual citizenship, so most applicants do not need to renounce their original nationality.

Ready to act on this?

La Vida Golden Visas — UK-based golden-visa specialist. Soveraine readers go to the front of the line through our partner link, and you fund independent editorial in the process.

Sources

- Law 23/2007 (Portuguese foreigners' law), consolidated text — https://dre.pt/dre/legislacao-consolidada/lei/2007-34536475

- Portuguese national visas — official portal — https://vistos.mne.gov.pt/en/national-visas/general-information/type-of-visa

- IRS Publication 54 (Tax Guide for US Citizens and Residents Abroad) — https://www.irs.gov/publications/p54

- FinCEN BSA E-Filing (FBAR / Form 114) — https://bsaefiling.fincen.treas.gov/main.html

- IRS FATCA summary (Form 8938) — https://www.irs.gov/businesses/corporations/summary-of-fatca-reporting-for-us-taxpayers

- Directive 2004/38/EC (EU citizens' free movement) — https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=celex%3A32004L0038

- OECD Model Tax Convention — https://www.oecd.org/tax/treaties/oecd-model-tax-convention-available-products.htm

- France exit tax — Article 167 bis CGI — https://www.legifrance.gouv.fr/codes/article_lc/LEGIARTI000041464977

- UK Statutory Residence Test (RDR3) — https://www.gov.uk/government/publications/rdr3-statutory-residence-test-srt

- Portuguese Tax Authority portal — https://info.portaldasfinancas.gov.pt/

- US Treasury — tax treaty information — https://home.tre