"Pay zero tax on crypto" is the most over-promised phrase in the digital-asset corner of the personal-finance internet. The accurate version is narrow. A handful of jurisdictions exempt private long-term holdings entirely. A smaller handful tax personal capital gains at zero across the board. A US citizen cannot reach zero through residency alone because the United States taxes on citizenship. And from 2027 onwards the OECD's Crypto-Asset Reporting Framework closes most of the informational gaps that made aggressive structures defensible in 2020. This guide covers the legitimate routes, the traps that destroy them, and the reporting regime that is about to overlay the whole conversation. It is written for three audiences in parallel — US persons, EU residents and freelancers, and readers based in the rest of the world.

Bright!Tax — US expat tax filings (FBAR + FATCA + Form 8949 + 1099-DA specialists)

How crypto is taxed by default

Before any zero-tax route is plausible, the baseline matters. Most jurisdictions worldwide classify crypto-assets as property rather than currency, which means a disposal is a taxable event and the gain or loss is measured against the asset's cost basis at the moment of disposal. The IRS set this position in Notice 2014-21 and has reiterated it in every subsequent piece of guidance, including the 2024 final regulations on digital-asset broker reporting under Treasury Decision 10000.

HMRC takes the same property characterisation in its Cryptoassets Manual, as does the German Bundesministerium der Finanzen in its 10 May 2022 circular, updated in March 2025. The Portuguese Autoridade Tributária e Aduaneira classifies crypto-asset gains under three separate income categories depending on activity (AT crypto guidance).

The taxable surface is wider than most newcomers expect. The IRS, HMRC and most EU revenue authorities treat the following as separate taxable events:

- Spot trades — selling crypto for fiat is a disposal at fair market value on the trade date.

- Crypto-to-crypto swaps — swapping ETH for SOL is two disposals, not a deferral.

- Spending crypto — using crypto to pay for goods or services is a disposal of the crypto at fair market value, separate from any sales tax or VAT due on the purchase.

- Staking rewards — taxable as ordinary income at fair market value on receipt, then capital gain or loss on later disposal (IRS Rev. Rul. 2023-14).

- Mining — ordinary income on receipt, plus self-employment tax in the US if conducted as a trade or business.

- NFT mints, sales and royalties — same property regime, with additional complexity around collectibles tax rates.

- DeFi yield — taxable as ordinary income on accrual in most jurisdictions; the precise trigger is unsettled in many.

A small group of countries treats crypto as currency rather than property — El Salvador after the 2021 Bitcoin Law, the Central African Republic briefly in 2022 — and a separate small group classifies disposals as miscellaneous or other income rather than capital gains (Japan applies progressive rates up to 55% under the National Tax Agency's crypto FAQ). The currency treatment is rare; the property treatment is the global default.

Who this applies to — read this first

The phrase "pay zero tax on crypto" lands very differently depending on the passport and residency of the reader. Three positions, three answers.

US persons

For US citizens and green-card holders, there is no residency route to zero. The US taxes worldwide income on citizenship under IRC §1 and IRC §61, and capital gains are not excluded by the foreign earned income exclusion. A US person abroad still files Form 1040 with Schedule D and Form 8949 for every disposal, still answers "Yes" to the digital-asset question on page 1 of Form 1040, still files FBAR (FinCEN 114) if foreign exchange accounts exceed $10,000 in aggregate at any point in the year (FinCEN), and from 1 January 2025 receives Form 1099-DA from US-regulated brokers reporting gross proceeds, with cost basis reporting phasing in from 2026 under the 2024 broker regulations.

The only US-side path that meaningfully reduces capital gains exposure on crypto is Puerto Rico's Act 60 for genuine bona fide residents under IRC §937 — and even that exempts only gains accrued after the move, never built-in gains brought in from elsewhere. The IRS confirmed this in Notice 2021-46 and audits the residency test actively.

EU residents

For an EU tax resident the answer turns on the member state. Germany's §23 EStG carve-out makes long-term private crypto disposals exempt. Portugal's post-2023 regime exempts disposals held over 365 days but charges 28% on short-term disposals. Italy moved from a 26% capital gains rate to a 42% headline rate from 2026 under the 2025 Budget Law before partial retreat to 33%. The Netherlands taxes deemed yield on Box 3 wealth annually, regardless of realisation, under the transition regime in place to 2028. France applies a flat 30% prélèvement forfaitaire unique on disposals by individuals under Article 150 VH bis CGI.

The relevance for EU readers is that "zero crypto tax in the EU" is a country-specific question, not a regional one, and the OECD Article 4 tiebreaker can pull a paper resident of a low-tax member state back into the high-tax state of origin if family, home and economic interests remain there (OECD MTC).

Non-US, non-EU readers

Readers outside the US and EU have the widest planning surface. Most home jurisdictions tax on residence, accept a clean break when residence is shifted, and apply CFC rules only above thresholds that solo crypto investors rarely cross. The UAE, Singapore (for individuals without a trading business), Cayman, Bermuda, Bahamas, Monaco, Vanuatu and Brunei tax personal capital gains at zero. Territorial systems — Paraguay, Panama, Costa Rica, Hong Kong, Malaysia — exempt foreign-source disposals for residents who structure their exchange accounts and counterparties offshore. The structural risks for this segment are CFC rules in the country of departure (UK, Australia, Canada, South Africa), exit taxes on unrealised gains in some states, and the CARF reporting that will flow from 2027 regardless of where the wallet lives.

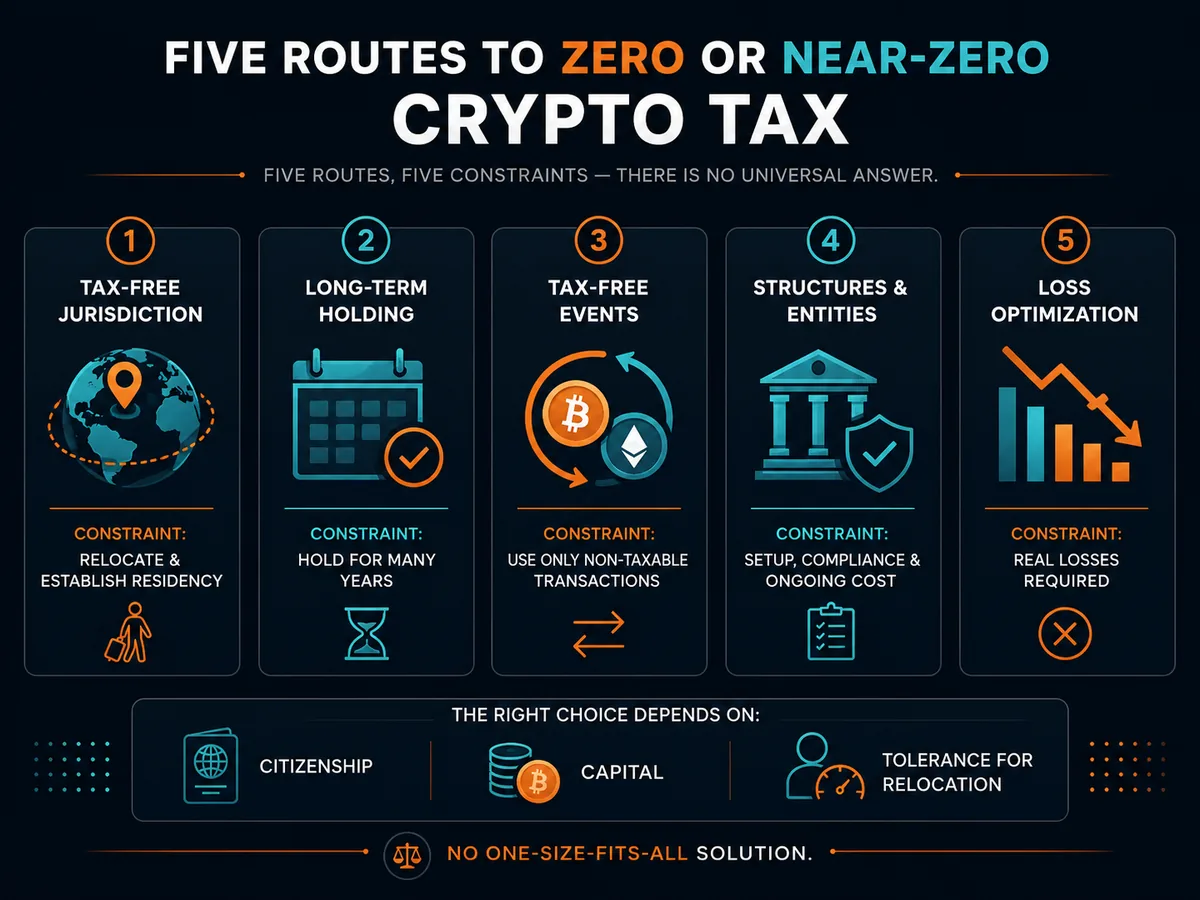

The legitimate zero-tax routes

Five routes account for almost every legitimate zero-tax outcome on a crypto disposal. They are distinct, the gotchas are different, and combining them clumsily generally produces a worse result than picking one and executing it cleanly.

Holding-period exemption — Germany §23 EStG

The cleanest exemption in the developed world. Under §23 of the Einkommensteuergesetz, a private sale of "other economic goods" — which the BMF circular of 10 May 2022 confirms includes cryptocurrencies — is exempt from personal income tax if the asset is held for more than 12 months between acquisition and disposal. A taxpayer who bought BTC in March 2024 and sold in April 2025 owes nothing on the gain.

The exemption covers spot sales, crypto-to-crypto swaps, and spending — any disposal of the long-held asset. Below the 12-month threshold, the gain is taxed at the taxpayer's marginal personal income tax rate up to 45%, but only if total private disposals in the year exceed an annual allowance of €1,000 (raised from €600 from 2024 under the Wachstumschancengesetz).

Mechanics. Hold the asset more than 12 months. Sell from a private wallet — the exemption applies to private holdings only, not to commercial trading. Maintain transaction records sufficient to evidence the acquisition date and cost basis; the FIFO method is the BMF default.

Gotchas. The 12-month exemption is the part that survived. The original §23 statute included an extended 10-year holding period for assets used to generate income — a reading that previously caught coins used in staking or lending. The BMF's March 2025 update confirmed that for individuals staking through proof-of-stake networks in a non-commercial capacity, the 12-month period continues to apply, ending years of uncertainty. The exemption fails entirely if the activity is recharacterised as commercial trading — high frequency, leverage, professional infrastructure — in which case gains fall under §15 EStG as business income with full progressive taxation and trade tax.

Territorial-tax residency plus offshore exchange — Paraguay and Panama

Paraguay and Panama both apply territorial taxation: only locally sourced income is taxed; foreign-source income is exempt for residents. A Paraguayan or Panamanian tax resident who sells crypto through an offshore exchange to an offshore counterparty, with funds routed to an offshore account, generates foreign-source income that is not within the Paraguayan or Panamanian tax net.

The Paraguayan personal income tax of 10% applies only to Paraguayan-source income under the Ley 6380/2019 and the Servicio de Tributación administrative guidance. Panama's Article 694 of the Fiscal Code defines Panamanian-source income narrowly. Neither country has specific crypto disposal rules — the position is derived from the source rules.

Mechanics. Establish tax residency. Paraguay's residency process is administered through the Dirección General de Migraciones and produces a cédula de identidad within months; the tax residency certificate requires SET registration and demonstrated economic substance. Panama's Friendly Nations Visa requires a USD 200,000 investment or local employment since the 2021 reform. Use exchanges incorporated outside Paraguay or Panama and counterparties outside both countries.

Gotchas. Both countries have thin treaty networks, so a tiebreaker dispute with a high-tax country of origin is resolved under that country's domestic law, not a treaty. Both are within the CARF perimeter — Panama signed the multilateral competent authority agreement on the Crypto-Asset Reporting Framework and will begin exchanging from 2027. A Paraguayan residency that is not backed by substantial physical presence is brittle if the country of origin claims continuing residency.

UAE residency plus a UAE tax residency certificate

The United Arab Emirates levies zero personal income tax under Federal Tax Authority guidance, which applies equally to crypto disposals by individuals. The 9% corporate tax introduced in 2023 under Federal Decree-Law No. 47 of 2022 applies to business profits above AED 375,000 but does not reach private investment activity by individuals.

Mechanics. Establish a free-zone company, obtain an investor visa, complete biometrics, and receive the Emirates ID. Apply to the FTA for a tax residency certificate once eligible under Cabinet Decision No. 85 of 2022 — the 90-day route is available for individuals with permanent place of residence and economic interests in the UAE; otherwise 183 days. The TRC is the document required by foreign banks, exchanges and tax authorities to recognise the UAE as the country of tax residency.

Gotchas. The 9% corporate tax does reach a crypto trading business — high-frequency disposals through a UAE free-zone company exceed the small-business relief threshold of AED 3 million revenue available under Ministerial Decision No. 73 of 2023. Free-zone qualifying income remains at 0% only under the Article 18 substance test, which requires real activity in the zone. The 9% does not reach personal disposals — but if the FTA recharacterises a flurry of personal trades as a business, the line moves. The UAE is a CARF signatory and will report to other CARF jurisdictions from 2027.

Puerto Rico Act 60 — for US persons only

Puerto Rico's Act 60, codified as the Incentives Code Law 60-2019, reduces tax on Puerto Rico-source capital gains for bona fide residents of the territory to 0% on gains accrued after the move under the Individual Resident Investor Decree (formerly Act 22).

Mechanics. Meet the three-part bona fide residence test under IRC §937 and Treasury Regulation §1.937-1 — a 183-day presence test, a tax home test, and a closer connection test. Apply for the Individual Resident Investor decree with the Department of Economic Development and Commerce. Pay an annual government fee of USD 5,000 and an annual charitable contribution requirement of USD 10,000 (raised from USD 5,000 in 2022). Purchase real property in Puerto Rico within two years.

Gotchas. Built-in gains on crypto acquired before establishing Puerto Rico residency remain federally taxable at US rates (IRS Notice 2021-46). The IRS opened a Puerto Rico Act 60 compliance campaign in 2021 and the Government Accountability Office has flagged enforcement gaps that Treasury is closing. Residency must be real — the "snowbird" pattern of a few months a year, a Manhattan apartment kept open, and a Florida driver's licence retained will fail the closer-connection test on audit. US-source income, including most US-based business income, remains US-taxable.

El Salvador Bitcoin residency

El Salvador adopted the Bitcoin Law in 2021 making Bitcoin legal tender alongside the US dollar, and in 2023 amended its Digital Assets Issuance Law to exempt Bitcoin from capital gains and income tax for natural and legal persons holding the asset as legal tender. The country offers a Freedom Visa granting permanent residency and a path to citizenship for individuals investing 1 BTC or USDT equivalent.

Mechanics. Apply for residency under the relevant immigration category, obtain a DUI (Documento Único de Identidad), file Salvadoran tax returns as a resident, and conduct disposals while resident. The Ministerio de Hacienda has not published detailed implementation guidance for non-Bitcoin crypto-assets, and the Bitcoin exemption is the headline.

Gotchas. El Salvador's IMF programme renegotiated in late 2024 walked back several Bitcoin Law provisions — acceptance by private merchants is now voluntary rather than mandatory, and tax payments in Bitcoin are no longer accepted. The Bitcoin-specific exemption survived the renegotiation; the framework around it did not. Banking infrastructure is thin compared to UAE or Panama. The country is a CARF signatory.

The traps

Most of the popular "0% crypto" advice fails for one of five reasons. Each of these has wrecked plans that looked tidy on paper.

The German exemption resets if recharacterised. A holder who runs a small node, lends through Aave, or runs a Liquidity Provider position can find that the activity is treated as commercial under §15 EStG rather than private under §23, with the 12-month exemption falling away and the entire portfolio reclassified. The 2025 BMF circular is more permissive than the 2022 version, but the line is not bright. A precautionary written ruling from the local Finanzamt is cheap insurance for any holder approaching the threshold of "professional."

Portugal is no longer the free lunch. Until the 2023 reform, Portuguese tax authorities took the position that crypto gains by individuals were not within any income category and therefore untaxed. The 2023 State Budget changed that. Gains on assets held less than 365 days are now taxed at 28% as capital gains under Category G of the IRS code; gains on assets held 365 days or more are exempt under AT guidance. Holders who relocated to Portugal in 2020 or 2021 expecting the old regime to persist now face a tax wedge on any short-term activity.

UAE free-zone non-qualifying income hits 9%. A free-zone company that derives income from mainland UAE counterparties, or whose income fails the substance test in Article 18 of the Decree-Law, loses qualifying status and pays the standard 9% corporate tax on profits above AED 375,000. The mistake commonly made is treating a free-zone licence as an automatic 0% wrapper — the activity must qualify and the substance must be real (FTA guidance on qualifying income).

Exchange withdrawals trigger KYC and source-of-funds review. Every regulated exchange, in every CARF or CRS jurisdiction, runs anti-money-laundering screening on fiat withdrawals above bank-level thresholds. A clean tax position with an unclear source-of-funds document is still going to slow down a withdrawal. Receipts, wallet history, and acquisition records matter even when the disposal itself is tax-exempt.

CRS and CARF extend reporting to crypto. The Common Reporting Standard has covered traditional financial accounts since 2017. The Crypto-Asset Reporting Framework extends the same logic to crypto-asset service providers from 2027. A French tax resident with a Bahamian exchange account does not have privacy from France for long.

Comparison table

| Country | Long-term holding rate | Short-term rate | Residency required | CARF participant | Best for |

|---|---|---|---|---|---|

| Germany | 0% after 12 months (§23 EStG, private holdings) | Marginal up to 45% above €1,000 allowance | Yes — full German tax residency | Yes (via EU DAC8) | Long-term private holders with one-year discipline |

| Portugal | 0% after 365 days | 28% under Category G | Yes — 183 days or habitual residence | Yes (via EU DAC8) | EU-passport holders with long-term holdings |

| United Arab Emirates | 0% personal | 0% personal | Yes — 90 or 183 days per Cabinet Decision 85 | Yes — first exchanges 2027 | Active traders willing to relocate |

| Puerto Rico (Act 60) | 0% on post-move gains | 0% on post-move gains | Yes — IRC §937 three-part test | US/PR territory; outside CARF | US persons with the substance to defend bona fide residency |

| Paraguay | 0% on foreign-source disposals (territorial) | 0% on foreign-source disposals | Yes — SET registration plus presence | Yes — first exchanges 2027 | Low-cost paper home with thin treaty needs |

| Panama | 0% on foreign-source disposals (territorial) | 0% on foreign-source disposals | Yes — 180 days plus Friendly Nations Visa | Yes — committed for 2027 | USD banking with territorial regime |

| El Salvador | 0% on Bitcoin specifically | 0% on Bitcoin specifically | Yes — Freedom Visa or standard residency | Yes — committed | Bitcoin maximalists comfortable with frontier banking |

| Cayman Islands | 0% personal | 0% personal | Yes — Certificate of Permanent Residence requires investment | Yes — among earliest CARF adopters | Capital above USD 2.4m investment threshold |

Sources: German BMF March 2025 circular, Portuguese AT crypto guidance, UAE Federal Tax Authority, Puerto Rico DDEC, Paraguay SET, Panama DGI, OECD CARF jurisdictions list.

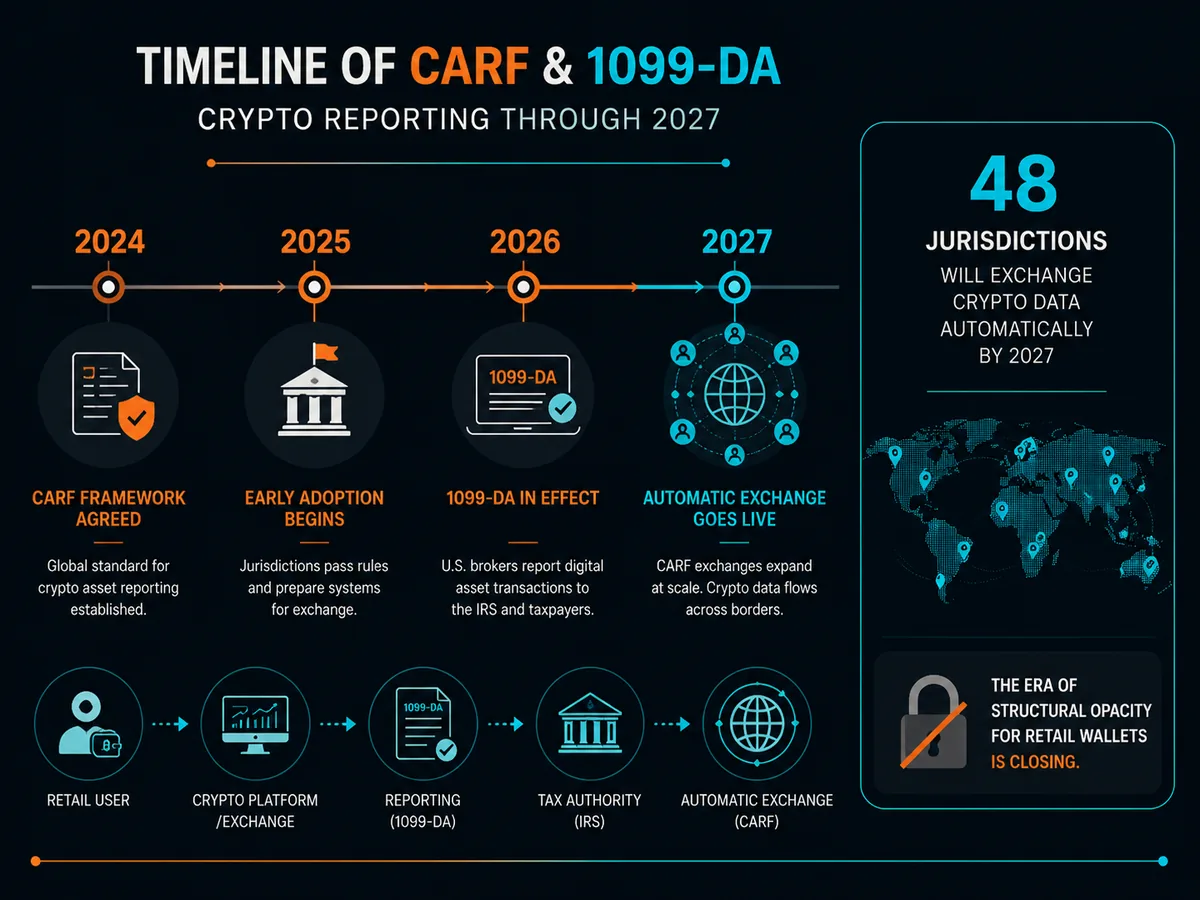

OECD CARF and CRS — the closing window

The single largest structural change to crypto tax planning is not a rate change in any one country. It is the OECD's Crypto-Asset Reporting Framework, agreed in 2022 and incorporated into amendments to the Common Reporting Standard in 2023. CARF puts in place, for crypto, the same automatic exchange of information regime that the CRS put in place for traditional financial accounts in 2017.

Under CARF, "reporting crypto-asset service providers" — centralised exchanges, brokers, certain wallet providers, and crypto ATM operators — are required to collect tax residency information from users, perform due diligence on existing and new accounts, and report to the local tax authority on an annual basis. Reportable information includes user identity (name, address, date of birth, tax identification number), aggregate fair-market-value transfers in and out, and aggregate fair-market-value disposals. The local tax authority then forwards the information to the user's country of tax residency through the OECD's Common Transmission System.

Forty-eight jurisdictions signed the multilateral competent authority agreement at the November 2023 OECD meeting committing to first exchanges by 2027 covering data from calendar year 2026. The signatories include the European Union (implemented through DAC8), the United Kingdom, Australia, Singapore, the UAE, the Cayman Islands, the Bahamas, Bermuda, Liechtenstein and Switzerland. The United States did not sign CARF but operates parallel reporting through Form 1099-DA from 1 January 2025 — gross proceeds for tax year 2025, cost basis reporting from tax year 2026 — covered by the 2024 broker regulations.

The practical effect is straightforward. A taxpayer holding a Bahamian exchange account in 2026 should expect the Bahamian authorities to report that account to the taxpayer's country of tax residency in 2027 and every year thereafter. A reporting position that depends on the home country not knowing about the account is no longer durable. Reporting positions that depend on a clean legal exemption — German §23, Portuguese 365-day, UAE personal — survive unchanged because they are documented and correct on the merits.

What this isn't

This article is not tax-evasion guidance. The five routes above are public-record exemptions and residency regimes available under the published law of the jurisdictions concerned. The distinction matters because the bad version of this conversation — hiding assets, falsifying source-of-funds documents, structuring transactions to defeat reporting — produces criminal exposure in every jurisdiction discussed and, increasingly, automatic detection through CARF.

It is not advice to renounce US citizenship. Renunciation under INA §349(a)(5) is the only route that stops US citizen tax filing entirely, but it triggers the IRC §877A exit tax on covered expatriates — a deemed sale of all worldwide assets, including crypto, at fair market value on the day before expatriation, with the first $890,000 of gain excluded for 2024 (indexed annually by the IRS). The decision is legally irreversible, costs USD 2,350 in State Department fees, and forfeits visa-free re-entry rights. It is a life decision with tax consequences, not a tax-planning move.

It is not a recommendation of any specific exchange as a tax-avoidance tool. Exchanges are operational infrastructure — they execute trades, custody assets, and now report to tax authorities. They do not change the tax character of a disposal. A clean German §23 exemption is exempt whether the trade was on Coinbase, Kraken, Bitstamp or a peer-to-peer transfer. The exchange's CARF reporting status changes how the disposal is reported, not whether it is taxable.

When to consult a professional

The crypto layer of cross-border tax planning is unsettled enough that a written opinion from a specialist is usually cheaper than the wrong assumption. Talk to a qualified advisor — and to two of them, one on the side of departure and one on the side of arrival, not one alone — before you act if any of the following apply:

- You are a US person holding more than ~USD 250,000 of crypto and considering Puerto Rico Act 60.

- You hold long-term positions in Germany and are unsure whether your staking or lending activity remains "private" under the 2025 BMF circular.

- You moved to Portugal under the old regime and have realised short-term gains since 1 January 2023.

- You are operating a free-zone company in the UAE with crypto trading activity above AED 3 million revenue.

- You are considering a Paraguayan or Panamanian residency without intending to spend substantial time there.

- You hold cryptoassets in centralised exchanges in jurisdictions that will begin CARF reporting in 2027.

Specialist US expat tax filers — Bright!Tax, Greenback Expat Tax — handle Form 8949, Schedule D, FBAR and the new 1099-DA reconciliation for US persons. Cross-border residency advisors at Henley & Partners handle the relocation side, free-zone formation partners such as SPC Free Zone handle UAE incorporation, and multi-currency banking providers such as Wise Business handle the operational rails — none of them are substitutes for a tax opinion.

For Soveraine's view on how we choose and disclose any service mentions, see our editorial policy and affiliate disclosure. We do not currently recommend a single crypto tax provider — the right choice depends heavily on country, holding pattern and the complexity of on-chain activity.

Ready to act on this?

Bright!Tax — US expat tax filings (FBAR + FATCA + Form 8949 + 1099-DA specialists). US persons with crypto positions still file every year regardless of residency; Soveraine readers go to the front of the line through our partner link, and you fund independent editorial in the process.

Sources

- IRS — Frequently Asked Questions on Virtual Currency Transactions. https://www.irs.gov/individuals/international-taxpayers/frequently-asked-questions-on-virtual-currency-transactions

- IRS — Notice 2014-21 (initial virtual currency guidance). https://www.irs.gov/pub/irs-drop/n-14-21.pdf

- IRS — Rev. Rul. 2023-14 (staking rewards). https://www.irs.gov/pub/irs-drop/rr-23-14.pdf

- IRS — About Form 1099-DA. https://www.irs.gov/forms-pubs/about-form-1099-da

- Treasury — 2024 Final Regulations on Digital Asset Broker Reporting (TD 10000). https://www.federalregister.gov/documents/2024/07/09/2024-14004/gross-proceeds-and-basis-reporting-by-brokers-and-determination-of-amount-realized-and-basis-for

- IRC §877A — Tax responsibilities of expatriation. https://www.law.cornell.edu/uscode/text/26/877A

- IRC §911 — Citizens or residents of the United States living abroad. https://www.law.cornell.edu/uscode/text/26/911

- IRC §937 — Bona fide residence in a US territory. https://www.law.cornell.edu/uscode/text/26/937

- FinCEN — Report of Foreign Bank and Financial Accounts (FBAR). https://www.fincen.gov/report-foreign-bank-and-financial-accounts

- HMRC — Cryptoassets Manual. https://www.gov.uk/hmrc-internal-manuals/cryptoassets-manual

- Bundesministerium der Finanzen — Crypto circular, 10 May 2022. https://www.bundesfinanzministerium.de/Content/DE/Downloads/BMF_Schreiben/Steuerarten/Einkommensteuer/2022-05-10-einzelfragen-zur-ertragsteuerrechtlichen-behandlung-von-virtuellen-waehrungen-und-von-sonstigen-token.html

- Bundesministerium der Finanzen — Crypto circular update, 6 March 2025. https://www.bundesfinanzministerium.de/Content/DE/Downloads/BMF_Schreiben/Steuerarten/Einkommensteuer/2025-03-06-einzelfragen-zur-ertragsteuerrechtlichen-behandlung-von-virtuellen-waehrungen-und-von-sonstigen-token.html

- §23 EStG — Private disposal transactions. https://www.gesetze-im-internet.de/estg/__23.html

- Autoridade Tributária e Aduaneira — Código do IRS (crypto guidance under Categories E, G, B). https://info.portaldasfinancas.gov.pt/pt/informacao_fiscal/codigos_tributarios/irs/Pages/codigo-do-irs.aspx

- UAE Federal Tax Authority. https://tax.gov.ae/en/

- UAE Cabinet Decision No. 85 of 2022 — Tax residency for natural persons. https://mof.gov.ae/

- UAE Federal Decree-Law No. 47 of 2022 — Corporate tax. https://mof.gov.ae/corporate-tax/

- OECD — Crypto-Asset Reporting Framework. https://www.oecd.org/tax/automatic-exchange/crypto-asset-reporting-framework/

- OECD — Common Reporting Standard. https://www.oecd.org/tax/automatic-exchange/

- EU — Council Directive (EU) 2023/2226 (DAC8). https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32023L2226

- El Salvador — Ley Bitcoin (Decreto No. 57). https://www.asamblea.gob.sv/sites/default/files/documents/decretos/171117063-36C4-4D9F-B6E0-A2C2EC9C9FF4.pdf

- Puerto Rico — Incentives Code Law 60-2019. https://www2.pr.gov/agencias/dddec/Pages/InitiativeActs.aspx

- IRS — Notice 2021-46 (Puerto Rico Act 60 built-in gains). https://www.irs.gov/pub/irs-drop/n-21-46.pdf