Panama spent the decade from 2012 to 2021 marketing itself as the easiest path to legal residency in the Western Hemisphere. The Friendly Nations Visa — Visa de Países Amigos, FNV — opened to nationals of roughly 50 countries with no minimum investment, no income threshold, and a documentary economic-tie test most applicants satisfied with a stock-broker account and a notarised letter from a Panamanian lawyer's company. That programme ended on 20 August 2021, when President Laurentino Cortizo signed Decreto Ejecutivo 197 of 2021 and added three concrete economic requirements. Anything written about the FNV that does not lead with the 2021 reform is out of date.

Henley & Partners — Largest RBI/CBI advisory firm in the world

This article covers what the FNV actually requires after the 2021 reform, the three economic-qualification routes, the Qualified Investor Visa alternative for higher-tier capital, Panama's territorial-tax regime under Código Fiscal Article 694, the banking and KYC realities since Panama's 2018 entry to the OECD Common Reporting Standard, the application process step-by-step, and the path from provisional FNV through permanent residency to eventual naturalisation. It is written for prospective applicants doing diligence before they engage a Panamanian immigration lawyer — not for people who have already wired the qualifying funds. It does not cover the Pensionado visa (Panama's separate pensioner programme with its own income test) or the Reforestation Investor Visa, which are distinct categories administered under different legal instruments.

What the Friendly Nations Visa actually is in 2026

The Friendly Nations Visa is a Panamanian residency permit created originally by Decreto Ejecutivo 343 of 2012 under President Ricardo Martinelli, designed to attract nationals of countries with which Panama maintained "friendly, professional, economic and investment relations." The list of friendly nations expanded over the years from an initial 22 to the current count of approximately 50, covering most of the European Union, the United Kingdom, the United States, Canada, Australia, New Zealand, Japan, South Korea, Singapore, Hong Kong, Israel, South Africa, Brazil, Argentina, Chile, Uruguay, Mexico, and several others.

For the first nine years of the programme, the FNV's economic-tie requirement was famously light: an applicant needed only to demonstrate either professional ties (a Panamanian work permit or a directorship in a Panamanian company) or economic ties (typically a Panamanian corporation with a bank account or a stock-broker account). In practice, the Panamanian legal industry built a workflow around this — Panamanian counsel would incorporate a Panamanian S.A. for the applicant, open a corporate bank account with a modest deposit, and file the FNV application using the corporation itself as the qualifying economic tie. Total cost: USD $5,000-$8,000 in legal and incorporation fees, plus a few thousand dollars in initial bank deposits. No qualifying investment was required.

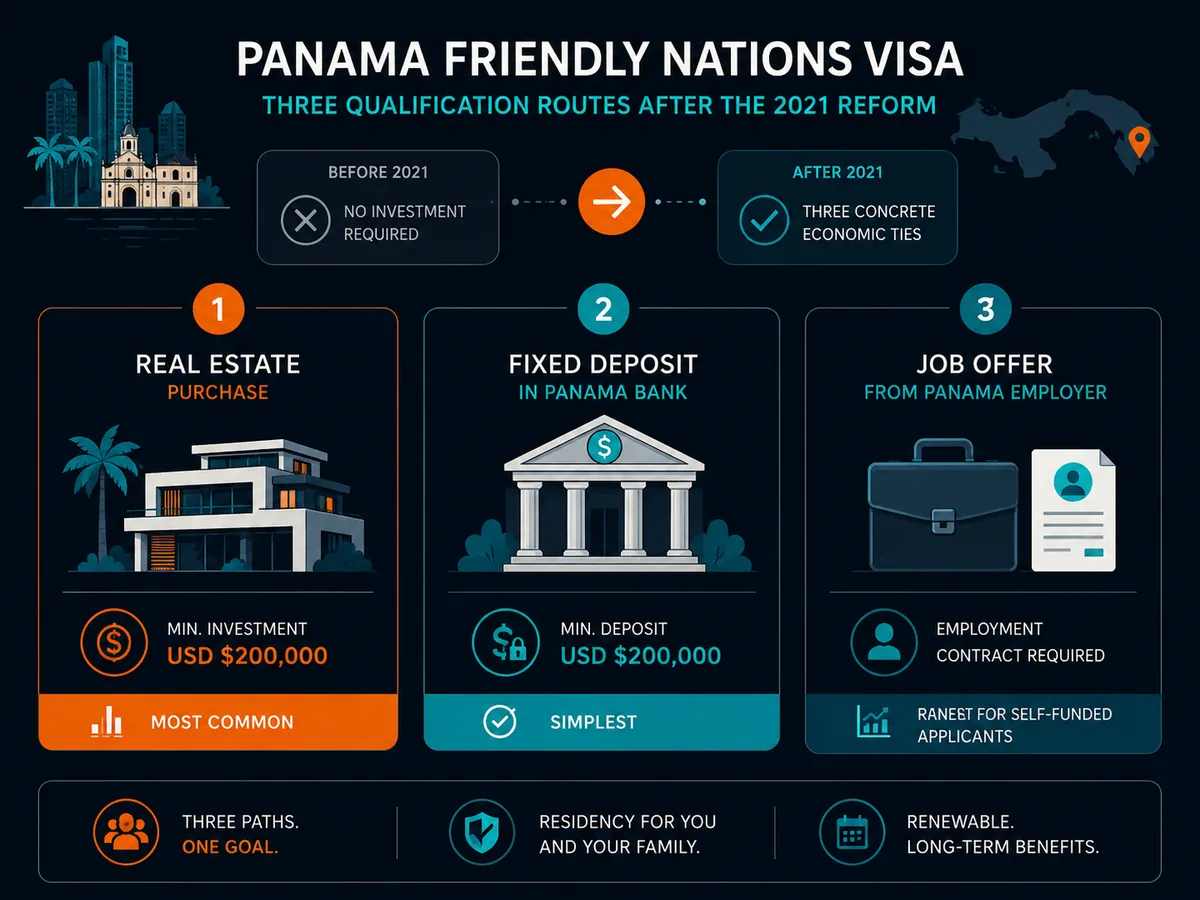

That route was eliminated by Decreto Ejecutivo 197 of 21 July 2021, gazetted in the Gaceta Oficial No. 29348-A and effective from 20 August 2021. Under the reformed framework, an FNV applicant must document one of three specific economic ties:

- A job offer from a Panamanian employer registered with the Caja de Seguro Social (CSS — the Panamanian social security institution), with the position justified as one not readily filled by a Panamanian national.

- A real-estate purchase in Panama with a registered title value of at least USD $200,000, held in the personal name of the applicant or via a Panamanian corporation whose shares are held directly by the applicant.

- A fixed-term bank deposit of at least USD $200,000 at a Panamanian bank, with a contractual hold of at least three years and the deposit account held in the personal name of the applicant.

The visa is issued initially as a two-year provisional residence permit rather than the immediate permanent residency the pre-reform FNV granted. After the two-year provisional period, holders apply to convert to permanent residency, subject to maintenance of the qualifying economic tie and continued good standing.

The Servicio Nacional de Migración (SNM) — Panama's federal migration authority — administers the FNV under the broader statutory umbrella of Ley 3 of 2008 (the Decreto Ley creating SNM) and the implementing Decreto Ejecutivo 320 of 2008 (the Reglamento Migratorio). The 2021 reform did not amend the statutory law; it changed the executive regulation that defines the FNV's specific evidentiary requirements.

Who this applies to — read this first

Eligibility for the FNV is restricted to nationals of the approximately 50 designated friendly countries. The downstream tax and reporting consequences depend almost entirely on the passport in your pocket. Read the segment that matches your situation before doing anything else.

US persons

Americans have historically been the largest single nationality applying for the FNV — a pattern dating to the original 2012 programme and continuing after the reform. The combination of geographic proximity (a three-hour flight from Miami), the use of US dollars as Panama's domestic currency, English-language legal infrastructure, and the territorial-tax regime on foreign-source income made Panama attractive to retirees and remote workers alike.

None of that reduces US tax exposure. Citizenship-based taxation under IRC §1 follows the passport. A US person who becomes a Panamanian resident continues to file Form 1040 annually, files FBAR on any Panamanian account whose aggregate maximum exceeds USD $10,000, and meets FATCA Form 8938 thresholds. Worse than Mexico or Portugal: because Panama exempts foreign-source income under its territorial regime, the foreign tax credit available against US tax is typically zero for a US-source retiree or remote-working consultant. The Panamanian residency is a lifestyle and legal-status arrangement, not a US tax-planning arrangement.

The US-Panama Tax Information Exchange Agreement of 2010 (TIEA, not a full income tax treaty) governs information exchange between the two tax authorities. Panama joined the OECD's Common Reporting Standard in 2018, meaning Panamanian banks now report on accounts held by tax residents of other CRS jurisdictions — including the United States via the FATCA framework that runs in parallel.

EU residents

EU, UK, Swiss, Norwegian and most European nationalities are on the FNV friendly-nations list and eligible to apply. The tax-side calculus differs from the US case in one important respect: EU member states operate residence-based tax systems, so leaving genuinely ends home-country tax exposure once the OECD-style tie-breaker tests under Article 4 of the Model Tax Convention are satisfied.

The headline traps are the exit-tax regimes applicable to substantial shareholders leaving certain EU jurisdictions. Germany's § 6 AStG treats the change of tax residency as a deemed disposal event for shareholdings above defined thresholds. France's exit tax under Article 167 bis CGI operates similarly. Spain's Modelo 720 imposes reporting obligations on foreign assets held by former residents in transition years. Panama's territorial regime captures none of these EU pre-departure events; an EU applicant should engage home-country counsel before triggering Panamanian residency rather than after.

CFC (controlled foreign corporation) rules in several EU jurisdictions — Germany's Außensteuergesetz, France's Article 209 B CGI, Spain's transparencia fiscal internacional — can attribute Panamanian holding-company income back to the EU shareholder regardless of Panamanian residency status, particularly during transition years when residency is contested.

Non-US, non-EU readers

Eligibility for the FNV varies by nationality. Approximately 50 nationalities qualify; the full list is published by SNM and updated periodically. Canadian, UK, Australian, New Zealand, Japanese, South Korean, Singaporean, Hong Kong, Israeli, South African, Brazilian, Argentine, Chilean, Uruguayan and Mexican nationals are all on the current list.

Nationals of non-friendly countries — including most African countries other than South Africa, most Asian countries other than the named exceptions, and most of the Middle East — cannot apply under the FNV. The available categories for non-friendly nationals are the Qualified Investor Visa under Decreto Ejecutivo 722 of 2020 (covered below), the Pensionado visa for retirees with qualifying lifetime pension income, the Self-Economic Solvency visa with a USD $300,000 fixed deposit, or various employment and business-investor categories with different thresholds.

The three FNV qualification routes (post-2021)

The reform decree's three routes are exclusive — an applicant qualifies on one of the three, with the documentary requirements specific to that route. The choice between them shapes the cost, timeline and ongoing maintenance burden of the residency.

Route 1 — Job offer from a Panamanian employer. The applicant must hold a written employment offer from a Panamanian company duly registered with the Caja de Seguro Social, with the position description and salary justified as one for which a Panamanian national was not readily available. The Ministerio de Trabajo's permiso de trabajo (work permit) is required in parallel — the FNV residency and the work permit are separate adjudications that proceed together. This route is least used by self-funded applicants because it requires a genuine Panamanian employer relationship with social-security registration and the corresponding payroll tax obligations.

Route 2 — Real-estate purchase of at least USD $200,000. The applicant must demonstrate ownership of Panamanian real property with a registered title value (valor catastral or transaction value, whichever is higher) of at least USD $200,000. The property must be held in the applicant's personal name or via a Panamanian S.A. whose shares are held directly. The title must be registered with the Registro Público de Panamá and free of disqualifying encumbrances. This is the route most foreign applicants use, particularly retirees and lifestyle movers who would purchase Panamanian property regardless of the visa requirement.

Route 3 — Fixed-term bank deposit of at least USD $200,000. The applicant must place USD $200,000 (or equivalent) in a time-deposit account at a Panamanian bank with a contractual hold of at least three years. The deposit account must be in the applicant's personal name (not corporate), and the bank must issue a certified letter confirming the deposit's terms and the hold period. The funds are not legally available to the applicant during the three-year hold — early withdrawal voids the visa qualification. This is the simplest route on paper and the most operationally difficult in practice, because the bank-account opening process for non-residents has become the most time-consuming step in the entire FNV journey (see "The banking challenge" below).

The alternative: Qualified Investor Visa (Decreto Ejecutivo 722/2020)

For applicants whose capital exceeds the FNV thresholds and who prefer immediate permanent residency rather than the two-year provisional period, the Qualified Investor Visa (Visa de Inversionista Calificado) is the parallel programme.

Created by Decreto Ejecutivo 722 of 15 October 2020 and effective from that date, the QIV was Panama's response to investment-migration competition from Portugal's then-active Golden Visa, Greece's Golden Visa, and the Caribbean citizenship-by-investment programmes. It grants permanent residency immediately, with no provisional period, in exchange for a higher minimum investment.

Three investment thresholds qualify:

- USD $300,000 in Panamanian real estate held in the applicant's personal name or via a Panamanian S.A. with direct shareholding. This threshold was scheduled to rise to USD $500,000 from October 2024 under transitional provisions — verify the current threshold with Panamanian counsel before structuring any purchase.

- USD $500,000 in securities listed on the Bolsa de Valores de Panamá (the Panamanian stock exchange), held through a Panamanian licensed broker.

- USD $750,000 in a fixed-term deposit at a Panamanian bank with a five-year contractual hold.

The QIV's qualifying funds must originate outside Panama and be wired through the Panamanian banking system to demonstrate source-of-funds compliance with Ley 23 of 2015, Panama's anti-money-laundering statute updated to meet FATF standards. The bank that receives the funds files a due-diligence acknowledgement with the SNM as part of the application package.

Unlike most Caribbean and EU investment-residency programmes, the QIV does not include a donation route. The full investment must be in qualifying assets, with the principal at the applicant's risk.

The QIV is open to all nationalities, not just the FNV friendly-nations list — a deliberate design choice to capture investor capital from jurisdictions excluded from the FNV.

Panama's territorial-tax regime

Panama operates one of the world's clearest territorial tax systems — and one whose practical application is more nuanced than the headline suggests.

The statutory authority is Article 694 of the Código Fiscal: "Es objeto del impuesto sobre la renta la renta gravable producida, de cualquier fuente, dentro del territorio de la República de Panamá." Income is subject to Panamanian income tax only when produced within Panamanian territory. Foreign-source income — including foreign salaries, foreign dividends, foreign capital gains, foreign rental income and foreign pensions — is exempt regardless of whether the income is remitted to Panama.

Resident individuals pay Panamanian income tax on Panama-source income at progressive rates:

| Annual taxable income (USD) | Marginal rate |

|---|---|

| Up to $11,000 | 0% |

| $11,000 - $50,000 | 15% on the excess over $11,000 |

| Above $50,000 | $5,850 fixed + 25% on the excess over $50,000 |

Source: Dirección General de Ingresos (DGI) 2026 schedule [source: verify current bracket figures from DGI before quoting in print].

The practical complication is the breadth of the "Panama-source" definition. Income from services rendered to a Panamanian client, even if the work is performed abroad, can be deemed Panama-source under DGI interpretive guidance. Income from intellectual property licensed for use in Panama is Panama-source. Trading executed on the Bolsa de Valores de Panamá generates Panama-source gains. Renting Panamanian real estate is Panama-source income regardless of the landlord's residency.

The "territorial paradise" framing collapses for any applicant whose income stream has Panamanian touchpoints. For a US-source-only retiree or a remote consultant invoicing non-Panamanian clients from Panamanian soil, the territorial regime delivers what it advertises. For an entrepreneur building Panamanian commercial operations, the territorial regime is largely irrelevant.

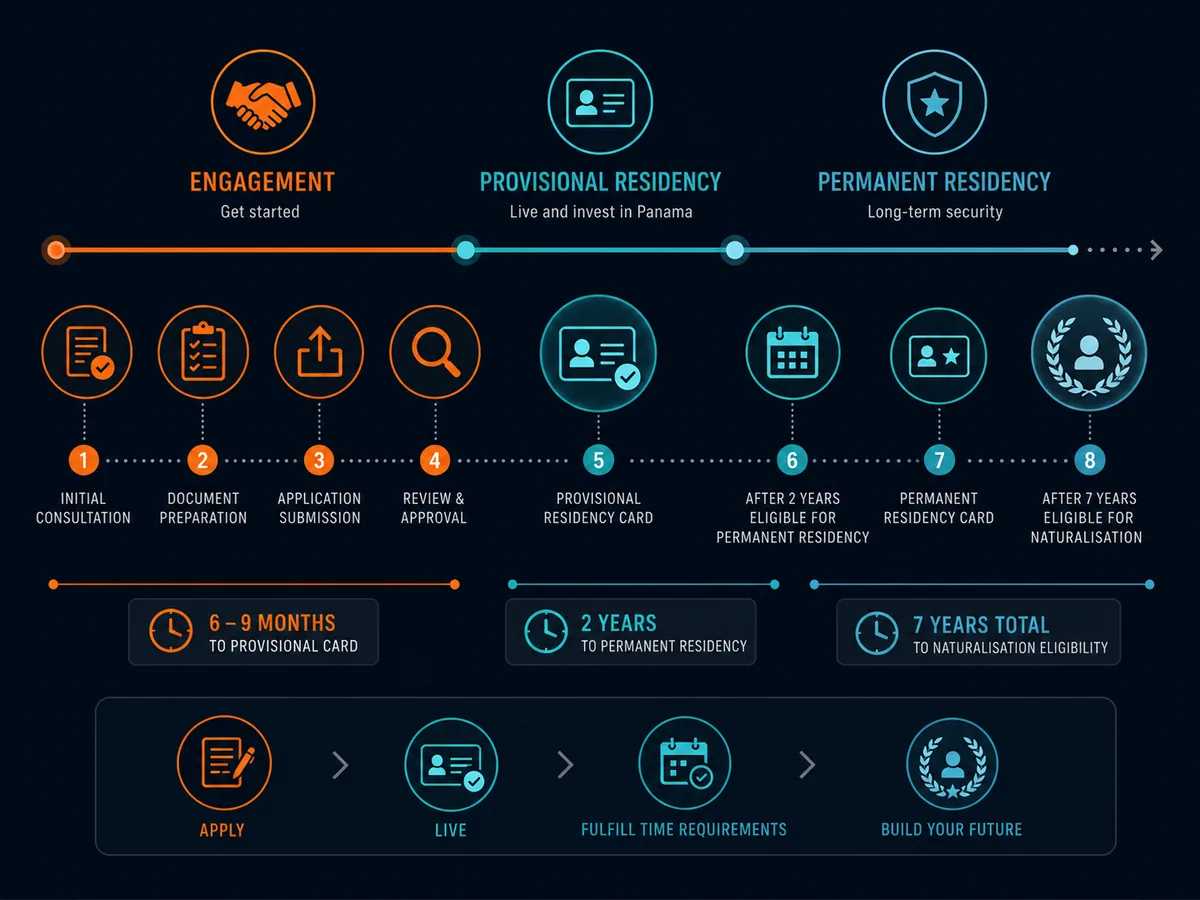

Application process step-by-step

The FNV application is filed in Panama by a Panamanian abogado idóneo (qualified attorney) acting under power of attorney. There is no consulate-route option for the FNV — unlike Mexico's Residente Temporal or Spain's NLV, the entire process happens in Panama after the applicant enters on a tourist visa (or visa-free for friendly nationalities).

Step 1 — Engage Panamanian immigration counsel. A Panamanian attorney is mandatory; the SNM does not accept FNV filings from self-representing foreign applicants. Counsel selection matters — the firms with the deepest SNM relationships process faster and recover better from documentary issues. Expect engagement fees of USD $4,000-$7,000 per principal applicant before disbursements.

Step 2 — Gather and apostille source documents. The standard documentary package:

- Passport with at least six months' validity, biographical page apostilled

- Apostilled criminal-record certificate from country of nationality and any country of residence over the past five years, with certified Spanish translation

- Apostilled marriage and birth certificates for any dependents, with certified Spanish translation

- Health certificate issued by a Panamanian licensed physician (obtained in Panama after arrival)

- Five passport photographs to SNM specification

- Evidence of the qualifying economic tie (real-estate title, fixed-deposit certificate, or employment contract — see the three routes above)

Step 3 — Enter Panama on tourist status. Friendly-nation passport holders enter visa-free for 180 days; the applicant must be physically present in Panama for the SNM filing and biometric capture.

Step 4 — File with the Servicio Nacional de Migración. Counsel files the documentary package at the SNM main office in Plaza Ágora, Panama City, with the relevant fees paid to the Tesoro Nacional. SNM issues a carné provisional (provisional ID card) valid for three to six months pending adjudication.

Step 5 — Receive the two-year provisional residency. SNM typically adjudicates within three to six months. On approval, the applicant returns to Panama for biometric capture and issuance of the physical cédula de residente (residency card), valid for two years from issuance.

Step 6 — Apply for permanent residency after the two-year period. Toward the end of the two-year provisional period, counsel files the conversion application demonstrating maintenance of the qualifying economic tie. SNM issues the permanent residency card on approval.

Step 7 — Apply for naturalisation after five further years. From the date of permanent residency, the applicant accrues the five-year residence clock toward naturalisation under Article 10 of the Constitution and the implementing provisions. Spanish-speaking and Latin American applicants qualify after three years.

End-to-end timeline from initial Panamanian arrival to physical residency card: six to nine months in 2026 conditions. The variance is driven mainly by document apostille turnaround in the applicant's country of nationality and Panamanian bank-account opening timelines.

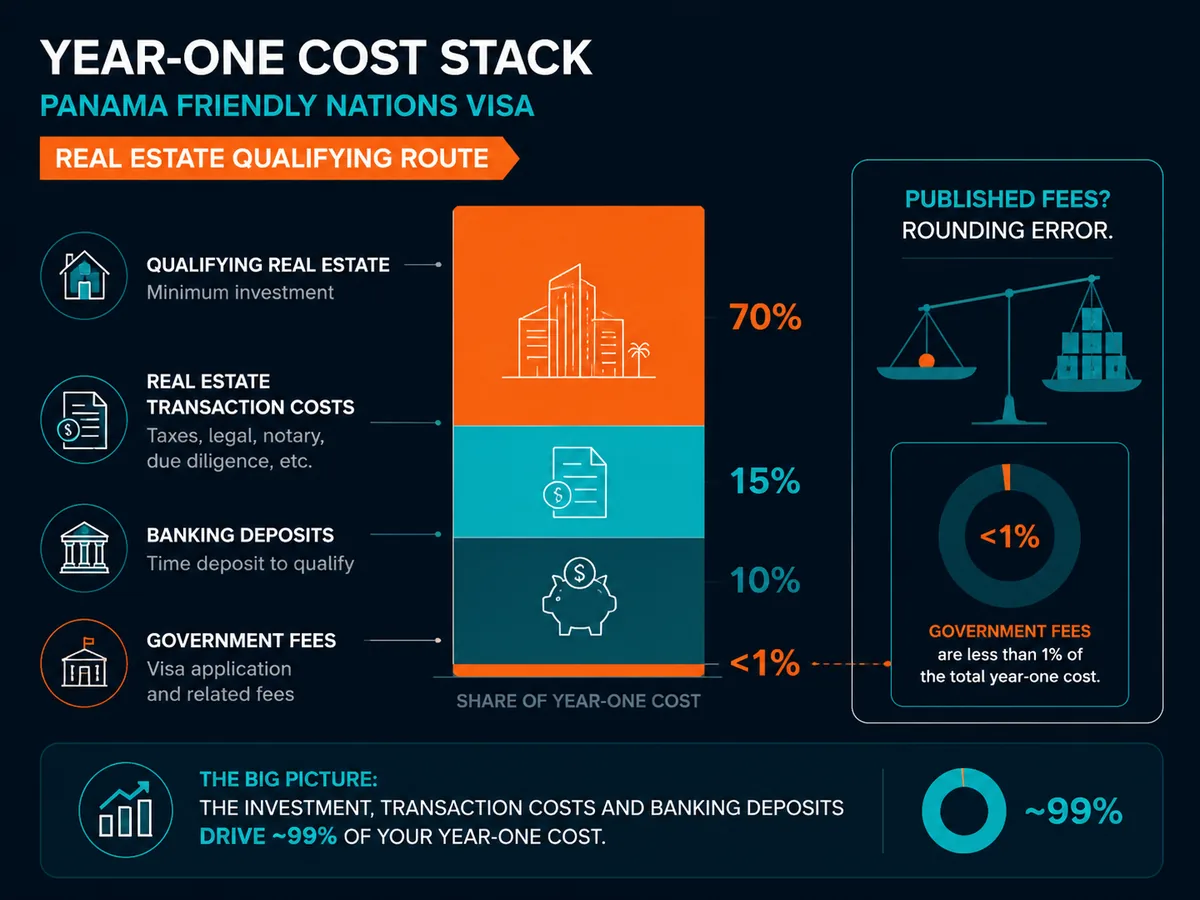

Real-cost stack (FNV via real estate)

The headline numbers are the qualifying investment plus government fees. The full year-one stack for the real-estate route is materially larger.

| Item | Cost (USD) | Notes |

|---|---|---|

| Qualifying real-estate purchase | $200,000+ | Registered title value; titled property only |

| Property transaction transfer tax | 2% of price | ITBI on real-estate transfer, paid at closing |

| Real-estate legal fees | $5,000 - $8,000 | Title search, escrow, registration with Registro Público |

| Immigration legal fees (principal) | $4,000 - $7,000 | Panamanian counsel, FNV filing through to permanent residency |

| Immigration legal fees (per dependent) | $1,500 - $3,000 | Spouse and minor children |

| SNM government fees | $250 + $800 deposit | Repatriation deposit (refundable on departure) plus filing fee |

| Tesoro Nacional fee | $250 | Treasury filing fee |

| Document apostilles | $300 - $500 | Criminal records, civil status documents |

| Certified Spanish translations | $200 - $400 | Mandatory for all foreign-language source documents |

| Panamanian bank account opening | $0 in fees | But $5,000 - $50,000 initial deposit at most banks |

| Health certificate (Panamanian physician) | $50 - $100 | Required Panama-side document |

| Cédula issuance fee | $50 | Physical residency card |

| US-side annual tax filing (US persons) | $1,500 - $3,500/year | Bright!Tax or equivalent expat CPA |

| Single applicant — real-estate route, excluding property | ~$11,500 - $20,500 | First year, excluding the $200k qualifying purchase |

| Family of three — real-estate route, excluding property | ~$15,500 - $27,500 | First year, excluding the $200k qualifying purchase |

For the financial infrastructure — wiring qualifying funds to Panama, paying Panamanian legal and closing fees in USD, multi-currency cards during the transition — most movers set up a Wise account before they leave their home country. For travel and gap-period health coverage in the months before Panamanian private insurance kicks in, SafetyWing covers the pre-permanent insurance layer.

The banking challenge

Panamanian bank-account opening for non-residents has become the most operationally difficult step in the FNV process, often more time-consuming than the SNM adjudication itself.

The historical context: the April 2016 Panama Papers leak of Mossack Fonseca's client records, followed by the OECD's grey-listing of Panama in 2016 and the Financial Action Task Force (FATF) grey-listing in 2019 (lifted in 2023), drove the Panamanian banking sector into an aggressive de-risking posture. Panama joined the OECD's Common Reporting Standard in 2018, with first reporting in 2019, and ratified the multilateral Convention on Mutual Administrative Assistance in Tax Matters the same year.

The practical consequences for FNV applicants in 2026:

- Initial deposits of USD $5,000 to $50,000 are standard at most Panamanian banks for new non-resident or new-resident accounts. The required deposit varies by bank and by client type (personal vs corporate, FNV applicant vs QIV applicant, US person vs other).

- Multiple in-person meetings are typically required. Most major Panamanian banks (Banco General, Banistmo, BAC Credomatic, Multibank, Global Bank) will not open accounts via electronic submission alone — the client must appear at the branch in person, in some cases multiple times.

- Extensive source-of-funds documentation is required under Ley 23 of 2015 compliance: bank statements from the home country covering 6-24 months, employment letters or business-ownership documentation, tax returns, and sometimes a banker's reference letter from the applicant's home-country bank.

- US persons face additional friction. Several Panamanian banks declined to onboard new US-person clients between 2019 and 2022 as they completed FATCA-compliance infrastructure build-out. The position has eased — most major banks now accept US persons — but extra documentation and longer onboarding remain the norm.

- Bank account opening typically requires the FNV provisional card already in hand, creating a chicken-and-egg problem for applicants whose qualifying route is the USD $200,000 fixed deposit. Counsel will sometimes negotiate conditional account opening with a designated bank, with the deposit held in escrow pending FNV approval.

The bank-account step is almost always the gating item that determines whether the overall timeline runs six months or twelve. Plan accordingly.

Comparison table

For prospective movers weighing Panama against the other Americas-residency programmes commonly considered:

| Programme | Minimum investment | Provisional duration | Path to permanent | Territorial tax | Best for |

|---|---|---|---|---|---|

| Panama FNV (real estate) | $200,000 property | 2 years | After 2-year provisional | Yes — foreign-source exempt | Friendly-nation lifestyle movers |

| Panama Qualified Investor | $300k property / $500k securities / $750k deposit | None — permanent immediately | Immediate | Yes — foreign-source exempt | Higher-tier capital, any nationality |

| Costa Rica Rentista | $60,000 deposit (24 months at $2,500/mo) | 2-year provisional | After 3 years | Yes — foreign-source exempt | Income-stream movers seeking nearby alternative |

| Mexico Residente Temporal | ~$1,700-$3,300/mo income or ~$30k savings | 1 year, renewable to 4 | After 4 years | No — worldwide for tax residents | Lower-capital lifestyle movers |

| Paraguay residency | $5,000 fixed deposit (formerly) — under reform 2024+ | None — permanent immediately under prior framework | Immediate under prior framework | Yes — foreign-source exempt | Lowest-cost Latin American residency [verify current 2026 rules] |

Panama's numbers compete favourably against Mexico on territorial tax and against Costa Rica on speed-to-permanent. Where it loses cleanly: the USD $200,000 qualifying investment floor (Mexico has none), the banking-de-risking friction (worst in the region), and the limited path benefits for US persons given citizenship-based taxation.

See the deeper pillars on Mexico Residente Temporal, Portugal D7 and countries with Golden Visa programmes for the comparable mechanics in each.

Path to permanent residency and citizenship

The FNV's two-year provisional period converts to permanent residency on application, subject to maintenance of the qualifying economic tie. The permanent residency card is then the foundation for the eventual naturalisation application.

Conversion to permanent residency. Toward the end of the two-year provisional period, counsel files the conversion application with SNM, demonstrating:

- Continued ownership of the qualifying real estate (Route 2) at registered value of at least USD $200,000, or

- Continued maintenance of the qualifying fixed deposit (Route 3) within the three-year hold period, or

- Continued employment with the Panamanian employer (Route 1) with CSS contributions current.

The permanent residency card is indefinite, requires no further renewal of the immigration status, and grants near-equivalent civil rights to Panamanian citizens with the exceptions of voting, certain political offices and restricted-zone property purchases (within the 10 km border-security buffer).

Naturalisation. Panamanian citizenship is governed by Article 10 of the Constitution and the implementing provisions of Law 8 of 2017. Naturalisation is available after:

- Five years of permanent residence for nationals of most countries, or

- Three years of permanent residence for nationals of Spanish-speaking Latin American countries and Spain.

The naturalisation application requires:

- Demonstrated Spanish-language proficiency (oral and written interview)

- Knowledge of Panamanian history, geography and civic structure

- A clean criminal record across all years of Panamanian residence

- Renunciation of prior citizenship in formal terms — though the practical enforcement of this requirement has historically been inconsistent for civil-law citizenships, and the constitutional position is best confirmed with current Panamanian counsel given periodic reform debate

The total clock from FNV provisional grant to naturalisation eligibility is therefore seven years for most nationalities (two years provisional + five years permanent + naturalisation processing), or five years for Spanish and Latin American applicants.

The traps

Banking de-risking is the bottleneck. The single most-common cause of FNV timeline blow-out in 2026 is the bank-account opening process. Several applicants have abandoned the FNV mid-process when no Panamanian bank would onboard them within a reasonable time. Engage counsel with established bank-relationship channels and budget twelve weeks minimum for the account opening alone.

The "Panama-source" definition is broader than the headline. The territorial-tax framing in marketing material implies a clean foreign/domestic split. The DGI's interpretive practice extends "Panama-source" to services rendered to Panamanian clients (regardless of where work is performed), royalties for IP used in Panama, and gains on Panama-Stock-Exchange securities. Applicants who plan to build Panamanian commercial operations should model the practical tax exposure with a Panamanian tax adviser before assuming territorial status delivers zero tax.

CRS reporting since 2018. Panama is a full participant in the OECD Common Reporting Standard. Panamanian financial accounts are reported annually to the account-holder's country of tax residence. The pre-2018 era when Panamanian banking offered de facto opacity to foreign tax authorities has been over for eight years. Any planning premised on Panamanian account secrecy is wrong on the facts.

OECD compliance scrutiny continues. Panama was on the FATF grey list from 2019 to 2023 and on EU non-cooperative jurisdiction lists at various points. The country has invested heavily in compliance infrastructure to exit these lists and remains under scrutiny. Periodic reform decrees can change documentary requirements with little notice — the 2021 FNV reform itself is the central example.

US persons gain nothing tax-wise without renunciation. The territorial regime exempts Panama from taxing foreign income, but Panama is not exempting US persons from US tax. Worldwide income remains taxable under US citizenship-based taxation, FBAR and FATCA reporting continue, and the foreign tax credit available against US tax is typically zero because no Panamanian tax was paid on the same income. The only mechanism that ends US tax obligation is formal renunciation under IRC §877A — covered in detail in the renouncing American citizenship pillar.

The three-year fixed-deposit hold is real. Route 3 applicants who chose the fixed-deposit qualifying route cannot access the USD $200,000 during the three-year hold period without voiding the FNV qualification. Treat the deposit as locked capital, not as available liquidity.

Naturalisation requires Spanish. Unlike the FNV and QIV, which can be processed entirely through English-speaking Panamanian counsel, naturalisation requires demonstrable Spanish-language proficiency in person. Applicants who do not invest in Spanish during the seven-year residency clock will fail at the final hurdle.

When to consult a professional

A handful of decision points genuinely justify paid help before acting:

- Panamanian immigration counsel is mandatory, not optional — the SNM does not accept self-filed FNV applications. Counsel selection matters; engage a firm with verifiable SNM filing volume and established bank-relationship channels.

- Cross-border tax planning before becoming a Panamanian resident. For EU residents, the exit-tax consequences in the departing jurisdiction can dwarf the cost of the FNV itself. For US persons, the question is whether eventual renunciation is the actual goal and what years of residence-building it requires.

- US expat tax filing. Non-optional from year one of Panamanian residency for US persons. Bright!Tax handles the FBAR + FATCA + FEIE stack for Americans in Latin America.

- Real estate due diligence. Panamanian title searches require local counsel; do not buy Panamanian real estate, particularly outside Panama City, without independent legal verification of the title chain.

- Comparative residency analysis. For applicants who are not yet certain Panama is the right jurisdiction, a comparative review against Caribbean CBI programmes, Portugal D7, Spain NLV, or Mexico Residente Temporal is worth the consultation fee.

For the higher-tier residency-and-citizenship advisory market, Henley & Partners handles Panama FNV and QIV alongside the broader citizenship-by-investment landscape. Latitude covers the same market with a Latin America-focused practice. For applicants whose interest leans toward Caribbean second-passport alternatives running in parallel to Panama residency, La Vida Golden Visas handles the Caribbean CBI advisory layer.

See our editorial policy on professional advice and our affiliate disclosure for how we handle service recommendations.## FAQ

What is the Panama Friendly Nations Visa?

The Friendly Nations Visa (Visa de Países Amigos, FNV) is a Panamanian residency category created under Decreto Ejecutivo 343 of 2012 and substantially rewritten by Decreto Ejecutivo 197 of 2021. It is open to nationals of roughly 50 countries with which Panama maintains friendly diplomatic, economic and professional ties. Since the August 2021 reform, the FNV no longer accepts the prior no-investment route. Applicants must instead document one of three economic ties to Panama: a job offer from a Panamanian employer registered with the Caja de Seguro Social, a real-estate purchase of at least USD $200,000, or a fixed-term bank deposit of at least USD $200,000 held for three years.

How much does the Panama Friendly Nations Visa cost in 2026?

The Panamanian government fees are modest — roughly USD $1,250-$1,800 in repatriation and immigration deposits paid to the Servicio Nacional de Migración and the Tesoro Nacional. The real cost stack runs much higher. The mandatory qualifying investment is USD $200,000 for the property or fixed-deposit routes. Panamanian immigration counsel typically charges USD $4,000-$7,000 per principal applicant, with USD $1,500-$3,000 per dependent. Add real-estate transaction legal fees of USD $5,000-$8,000 for the property route, document apostilles and certified Spanish translations of USD $300-$500, and the bank-account opening process, which alone can consume several months and require initial deposits of USD $5,000-$50,000 depending on the institution.

Can I still get Panama residency without buying property?

Yes, but not on the simplest historical FNV terms. Three current routes exist for non-investor applicants. The first is the FNV job-offer route — a genuine employment contract with a Panamanian employer registered with the Caja de Seguro Social. The second is the FNV fixed-deposit route — USD $200,000 placed in a three-year time deposit at a Panamanian bank. The third is the Short Stay Visa for Remote Workers under Decreto Ejecutivo 198 of 2021, which grants a nine-month stay, renewable once, for foreign nationals earning at least USD $36,000 per year (USD $48,000 for families) from non-Panamanian sources. The remote-worker visa does not lead to permanent residency.

Does Panama tax foreign-source income?

No — at least in principle. Panama operates a territorial tax system under Article 694 of the Código Fiscal: only income produced within Panamanian territory is subject to Panamanian income tax. Foreign-source income — including foreign salaries, foreign dividends, foreign capital gains and foreign pensions — is exempt regardless of whether the income is remitted to Panama. The practical complication is the breadth of the "Panama-source" definition. Income from services provided to a Panamanian client, even if the work is performed abroad, can be deemed Panama-source. Trading on the Panama Stock Exchange or invoicing through a Panamanian entity will also trigger local tax. A qualified Panamanian tax adviser is essential before structuring any business presence.

Does Panama residency end my US tax obligations?

No. The United States is the only OECD country other than Eritrea that taxes its citizens on worldwide income regardless of where they live. A US person who becomes a Panamanian resident continues to file Form 1040 annually, report worldwide income, file FBAR on Panamanian accounts whose aggregate maximum exceeds USD $10,000, and meet FATCA Form 8938 thresholds. Panama's territorial-tax exemption on foreign income means very little Panamanian tax is paid that could be used as a US foreign tax credit. The only mechanism that ends US tax obligations is formal renunciation of US citizenship under IRC §877A, which carries an exit tax for covered expatriates with average annual tax above USD $201,000 or net worth above USD $2 million.

When can I apply for Panamanian citizenship through the Friendly Nations Visa?

Permanent residency under the FNV is granted after the two-year provisional period. Panamanian naturalisation under Article 10 of the Constitution and Law 8 of 2017 then becomes available after five further years of permanent residence — seven years from the initial provisional grant in total. Citizens of Spain and Latin American countries qualify for naturalisation after only three further years of permanent residence. Applicants must demonstrate Spanish-language proficiency, knowledge of Panamanian history and geography, and complete an interview with the Ministerio de Gobierno. Panama recognised dual citizenship for naturalised Panamanians through a constitutional reform process, though the formal position is that naturalised citizens must renounce their prior citizenship — a rule rarely enforced in practice for civil-law citizenships but worth confirming with counsel.

Is there a Panama digital nomad visa?

Yes — the Short Stay Visa for Remote Workers, created by Decreto Ejecutivo 198 of 2021, parallel to the FNV reform decree. It grants a nine-month initial stay, renewable once for a further nine months, with no path to permanent residency. Applicants must prove foreign-source employment or freelance income of at least USD $36,000 per year for a single applicant or USD $48,000 for a family. The income cannot derive from any Panamanian source. The visa does not by itself create Panamanian tax residency, since the 183-day threshold is rarely reached within a single nine-month window if the holder maintains travel outside Panama. It is a short-stay product, not a residency replacement for the FNV or the Qualified Investor Visa.

What is the Panama Qualified Investor Visa?

The Qualified Investor Visa (Visa de Inversionista Calificado) was created by Decreto Ejecutivo 722 of 2020 to attract higher-tier capital that the post-reform FNV does not capture. It grants permanent residency immediately rather than the FNV's two-year provisional period. Three investment thresholds apply: USD $300,000 in Panamanian real estate (rising to USD $500,000 from October 2024 — verify current threshold before applying), USD $500,000 in securities listed on the Panamanian stock exchange, or USD $750,000 in a fixed-term deposit at a Panamanian bank held for five years. The funds must originate outside Panama and be wired through the Panamanian banking system. The QIV is administered by SENAFRONT-cleared Panamanian counsel and adjudicated by the Servicio Nacional de Migración.

Ready to act on this?

Henley & Partners — Largest RBI/CBI advisory firm in the world. Soveraine readers go to the front of the line through our partner link, and you fund independent editorial in the process.

Sources

- Decreto Ejecutivo 197 of 21 July 2021 (FNV reform) — Gaceta Oficial No. 29348-A — https://www.gacetaoficial.gob.pa/

- Decreto Ejecutivo 343 of 2012 (original FNV creation) — Gaceta Oficial — https://www.gacetaoficial.gob.pa/

- Decreto Ejecutivo 722 of 15 October 2020 (Qualified Investor Visa) — https://www.gacetaoficial.gob.pa/

- Decreto Ejecutivo 198 of 2021 (Short Stay Visa for Remote Workers) — https://www.gacetaoficial.gob.pa/

- Ley 3 of 2008 (creation of Servicio Nacional de Migración) — https://www.gacetaoficial.gob.pa/

- Ley 23 of 2015 (Panamanian AML statute) — https://www.gacetaoficial.gob.pa/

- Ley 8 of 2017 (naturalisation framework) — https://www.gacetaoficial.gob.pa/

- Constitución Política de la República de Panamá, Article 10 (nationality) — https://www.asamblea.gob.pa/

- Código Fiscal de Panamá, Article 694 (territorial income tax) — https://dgi.mef.gob.pa/

- Servicio Nacional de Migración (SNM) — https://www.migracion.gob.pa/

- Dirección General de Ingresos (DGI) — Ministerio de Economía y Finanzas — https://dgi.mef.gob.pa/

- Registro Público de Panamá (real-estate title registry) — https://www.registro-publico.gob.pa/

- Caja de Seguro Social (CSS) — http://www.css.gob.pa/

- US-Panama Tax Information Exchange Agreement (2010) — US Treasury — https://home.treasury.gov/policy-issues/tax-policy/treaties

- OECD Common Reporting Standard — Panama participation since 2018 — https://www.oecd.org/tax/automatic-exchange/

- OECD Convention on Mutual Administrative Assistance in Tax Matters — https://www.oecd.org/tax/exchange-of-tax-information/

- Financial Action Task Force — Panama mutual evaluation reports — https://www.fatf-gafi.org/

- IRC §877A (US expatriation tax) — https://www.law.cornell.edu/uscode/text/26/877A

- FinCEN BSA E-Filing (FBAR / Form 114) — https://bsaefiling.fincen.treas.gov/main.html

- IRS Form 8938 (FATCA reporting) — https://www.irs.gov/forms-pubs/about-form-8938