The non-lucrative visa is Spain's residence permit for non-EU citizens who can support themselves without working. It is the path most retirees, financially independent households and passive-income earners take into Spain. It is not — despite a great deal of internet folklore — a route for remote workers, freelancers or anyone running an active business. This guide covers the 2026 income thresholds, the document set Spanish consulates actually require, the tax bill that comes with Spanish residence, and how the answers differ depending on whether you hold a US, EU or third-country passport. We will not cover the digital nomad visa, golden visa (abolished in April 2025) or the autónomo route except where they intersect.

La Vida Golden Visas — UK-based golden-visa specialist

What the non-lucrative visa actually is

The non-lucrative visa — visado de residencia no lucrativa — is governed by the Spanish Immigration Law (Ley Orgánica 4/2000) and the implementing regulation Royal Decree 557/2011, specifically Articles 46 to 51 [source: TODO — link to BOE consolidated text of RD 557/2011]. It grants an initial one-year residence permit, renewable for two-year periods, on the condition that the holder does not engage in any lucrative activity in Spain.

The Spanish Foreign Ministry's consular network describes it bluntly: a visa "to reside in Spain without carrying out any gainful (work or professional) activity, provided that the applicant has sufficient and guaranteed means" (Consulate General of Spain in Los Angeles). That single sentence carries the entire structure: passive means, no work, renewable.

After five years of continuous residence you can convert to long-term EU residence. After ten you can apply for citizenship, with shorter tracks for certain nationalities. The visa requires you to spend more than 183 days per calendar year in Spain to renew — which makes you a Spanish tax resident by default.

Who this applies to — and who it doesn't

The non-lucrative visa is open to non-EU/EEA/Swiss nationals. EU citizens do not need it; they register under the EU free-movement regime.

The audience that fits cleanly: retirees with pension income, individuals living off investment portfolios, rental-property owners with foreign income, and households with substantial liquid savings who intend to spend at least a few years in Spain before deciding next steps.

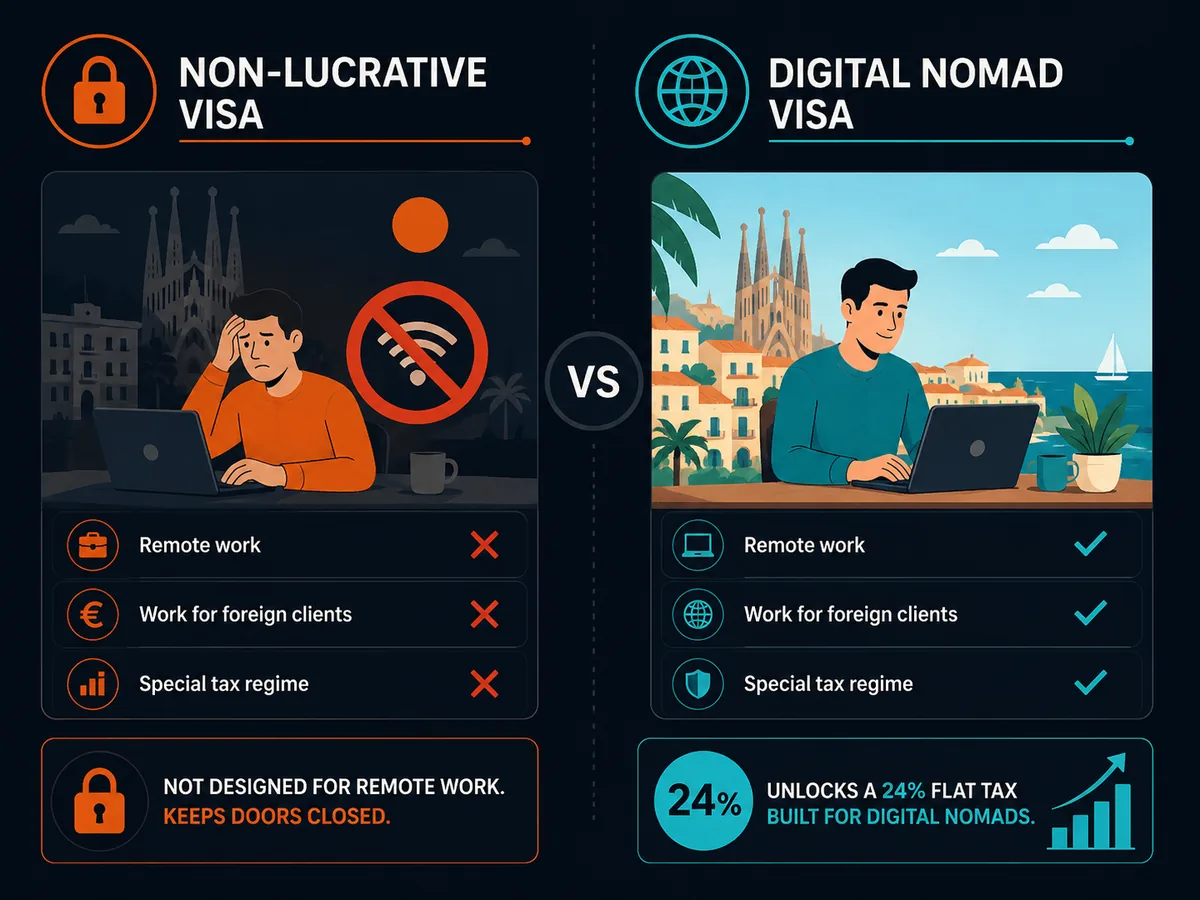

The audience that does not fit: anyone planning to work remotely for a foreign employer, anyone running a business (whether incorporated abroad or not), freelancers with active clients, and short-stay visitors who want to dodge the 90/180 Schengen rule. For remote workers, the correct route is the digital nomad visa created by the 2023 Startup Law (Ley 28/2022), which carries a Beckham-style 24% flat tax option (Ley 28/2022, BOE).

US persons

US citizens and green-card holders carry citizenship-based taxation with them. Becoming a Spanish tax resident does not end your US filing obligations — you continue to file Form 1040, FBAR (FinCEN 114) for foreign accounts over $10,000 aggregate, and Form 8938 where thresholds are met (IRS, FBAR reference guide). The US–Spain double tax treaty allows foreign tax credits, so you generally pay the higher of the two rates — which is almost always the Spanish rate.

EU freelancers and digital nomads

If you are already an EU citizen, you do not need this visa. If you are an EU tax resident moving from another member state, watch for exit taxes (Spain's article 95 bis applies in reverse from your departure state) and for whether your home state will assert residence under the 183-day rule or the centre-of-vital-interests test in your bilateral treaty.

Non-US, non-EU readers

This is the cleanest segment. Your home country likely uses residence-based or territorial taxation, so leaving it for Spain ends your tax exposure there (subject to formal deregistration). The non-lucrative visa simply moves you into the Spanish system without the overlay of US citizenship-based tax or EU exit-tax friction.

Required documents

Each consulate publishes a checklist. The Los Angeles, Washington DC and London consulates are the most thorough. Expect:

- National visa application form, signed.

- Form EX-01 (residence application), signed.

- Form 790-052, the fee payment form.

- Valid passport with at least one year of validity and two blank pages.

- Two recent passport photographs, white background.

- Proof of residence in the consular district (utility bill, driver's licence, lease).

- Criminal record certificate from every country you have lived in for the past five years, issued within the last three months, apostilled under the 1961 Hague Convention and translated into Spanish by a sworn translator (Hague Apostille Section).

- Medical certificate stating you are free of diseases listed in the International Health Regulations 2005, issued within the last three months.

- Private health insurance from a provider authorised to operate in Spain, full coverage, no co-pays, no deductibles, no waiting periods. Travel insurance does not qualify.

- Proof of financial means — bank statements, pension award letters, brokerage statements, rental contracts.

For dependants: marriage certificate, birth certificates, and proof that the financial means cover them too. All foreign civil documents must be apostilled and sworn-translated.

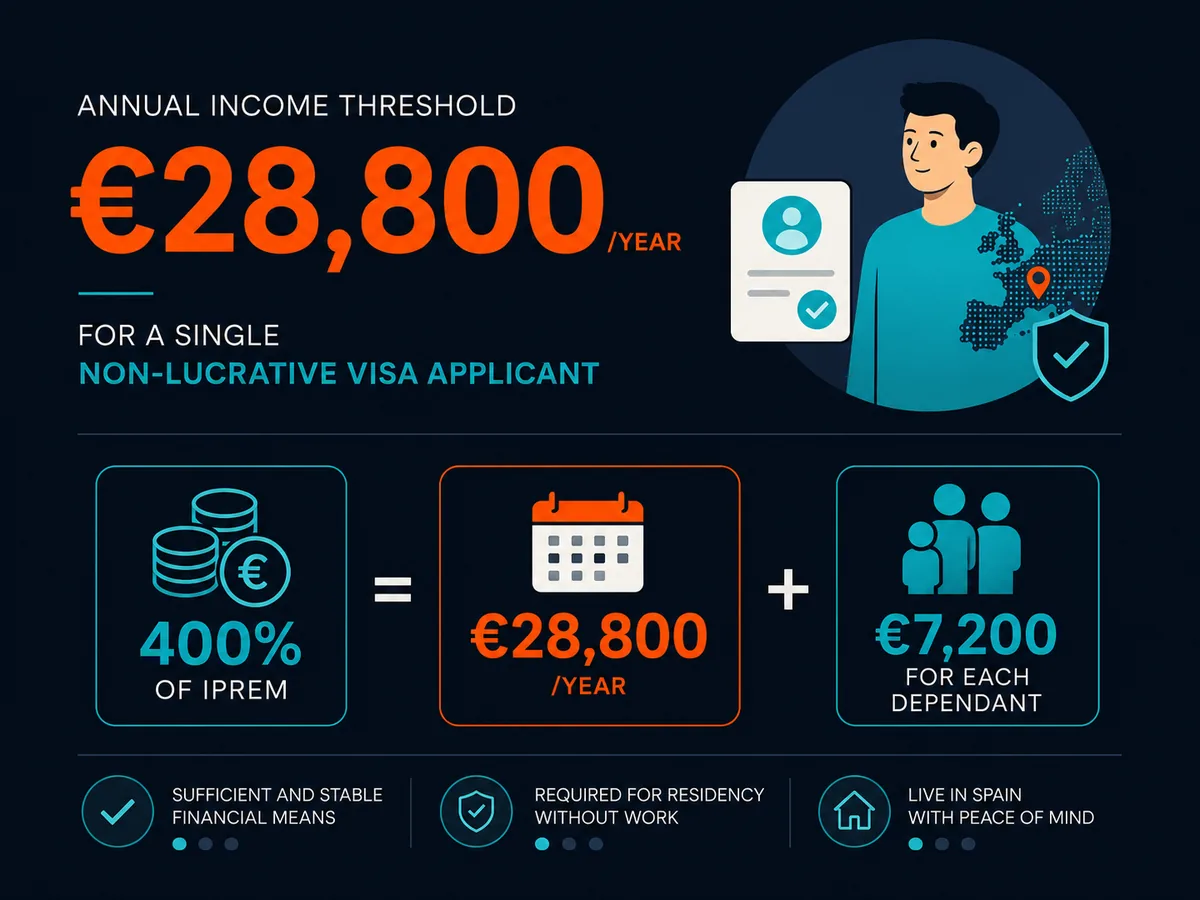

Income and savings thresholds for 2026

The income test is anchored to the IPREM — the Indicador Público de Renta de Efectos Múltiples — which is reset by the annual State Budget Law. The non-lucrative visa requires 400% of IPREM for the main applicant and 100% for each additional family member.

The IPREM for 2024 was €600/month (€7,200/year) and was carried into 2025 by extended budget [source: TODO — confirm 2026 IPREM figure from BOE once Ley de Presupuestos Generales del Estado is published]. Applied to that base:

| Household | Monthly minimum | Annual minimum |

|---|---|---|

| Main applicant (400% IPREM) | €2,400 | €28,800 |

| + 1 dependant (100%) | €600 | €7,200 |

| + 2 dependants | €1,200 | €14,400 |

| Couple + 2 children | €4,200 | €50,400 |

These are minimums. Consulates routinely expect a comfortable margin — bank balances showing 12 to 24 months of cover, not just the headline annual figure. Immigrant Invest and several Spanish immigration law firms report consulates rejecting applications that hit the threshold exactly but show no buffer (Immigrant Invest).

Procedure: application to TIE card

The end-to-end process has three phases.

Phase 1 — Consular application

File at the Spanish consulate with jurisdiction over your legal residence. You cannot pick a more lenient consulate. Some consulates require appointments booked months in advance; the BLS visa-services contractor handles intake for several US consulates (BLS Spain Visa, Los Angeles).

Submit in person. Biometric data is collected. The consulate forwards the file to the Subdelegación del Gobierno in the Spanish province where you intend to live. Decision: typically one to three months. The visa is then placed in your passport and is valid for 90 days of entry.

Phase 2 — Entry and empadronamiento

Enter Spain within the visa window. Within 30 days of arrival, register at your local town hall (the empadronamiento) and apply for the Foreigner Identity Card (TIE) at the relevant Oficina de Extranjería. You will need a NIE (foreigner identity number), proof of address, and the visa itself.

Phase 3 — Renewal cycle

The initial card is valid for one year. The first renewal grants two years. The second renewal grants another two years. At five years you qualify for long-term residence. Each renewal requires fresh proof of means, continued health insurance and evidence of more than 183 days physically present in Spain during the prior period.

Realistic costs, fees and timeline

Government fees are modest. The professional and compliance costs are not.

| Item | Cost (EUR equivalent) | Notes |

|---|---|---|

| Consular visa fee | €80–€140 | Varies by reciprocity; US applicants pay around $140 [source: TODO — current US consular fee from MAEUEC] |

| TIE card fee | ~€16 | Tasa modelo 790-012 |

| Apostille (US) | $20–$50 per document | State Secretary of State |

| Sworn translation | €40–€80 per page | Spain-registered traductor jurado |

| FBI background check | $18 + handling | IdentoGO channeler |

| Private health insurance | €1,200–€3,000 per adult per year | Sanitas, Adeslas, DKV most commonly accepted |

| Immigration lawyer (optional) | €1,500–€3,500 | Per applicant, end-to-end |

| Total first-year cash outlay (single applicant, with lawyer) | €4,500–€7,500 | Excluding required income |

Timeline from decision to TIE in hand is typically four to seven months.

Taxes once you become resident

Spending more than 183 days in Spain in a calendar year, or having your main centre of economic interests there, makes you a Spanish tax resident under Article 9 of the Personal Income Tax Law (Ley 35/2006) [source: TODO — link to consolidated LIRPF Art. 9]. Tax residents pay IRPF on worldwide income.

The general scale, combining state and autonomous-community rates, runs from roughly 19% to 47–50% in 2025 depending on the region. Savings income (dividends, interest, capital gains) is taxed on a separate scale: 19% up to €6,000, 21% to €50,000, 23% to €200,000, 27% to €300,000, and 28% above €300,000 [source: TODO — confirm 2026 savings scale from Agencia Tributaria].

Wealth tax (Impuesto sobre el Patrimonio) applies above a state minimum of €700,000 of net assets, with a €300,000 main-residence allowance. Madrid effectively bonifies it to zero; Andalucía does the same. Catalonia, Valencia, the Balearics and most other regions impose it. The state Solidarity Tax on Large Fortunes catches residents of zero-tax regions on assets above €3 million (Agencia Tributaria — wealth tax).

The Beckham regime — the impatriate flat 24% on Spanish-source income — is not available to non-lucrative visa holders. It requires moving to Spain because of an employment contract or director appointment.

Tax for US persons

US citizens remain subject to US taxation on worldwide income regardless of residence (IRS Publication 54). The 1990 US–Spain treaty, modernised by the 2013 protocol that entered into force in November 2019, allocates taxing rights and provides foreign tax credits (US Treasury — Spain treaty documents). Practical points:

- Social Security: taxable only in Spain under Article 20, but the US saving clause means US citizens still report it on Form 1040 and credit Spanish tax paid.

- Roth IRAs: Spain does not recognise the US tax treatment. Distributions and internal growth may be taxable in Spain.

- Mutual funds and ETFs: US-domiciled funds held by Spanish residents are treated as PFIC-adjacent under Spanish rules and, separately, EU regulations restrict purchases. Many US brokers will close accounts of Spanish-resident clients.

- FBAR and Form 8938 filings continue.

Tax for EU citizens already in another member state

Moving from one EU state to Spain triggers tax-residence change in both. Your departure state may apply exit tax on unrealised gains (France, Germany, the Netherlands all do). Spain itself applies an exit tax under Article 95 bis LIRPF on residents with portfolios above €4 million who leave after ten years of residence — relevant for the back-end, not the front-end.

Tax for non-US, non-EU readers

The simplest case. Confirm formal deregistration from your home tax authority, document the date your Spanish residence begins, and from that point you are inside the Spanish system. Treaty relief depends on whether Spain has a bilateral treaty with your home state (list maintained by Agencia Tributaria).

Can you work remotely on this visa

Officially, no. The visa explicitly prohibits lucrative activity, and Spanish immigration lawyers are increasingly cautious. The Madrid-based firm Pellicer & Heredia notes that "the non-lucrative visa is incompatible with any work activity, including remote work for foreign companies" (Pellicer Heredia).

In practice, several consulates have historically approved applicants who had remote income, and many holders quietly continue remote work. The risk surfaces at the two-year renewal, when tax filings reveal employment income. The clean answer for remote workers is the digital nomad visa under the 2023 Startup Law, which permits the activity and offers the 24% flat rate.

Common mistakes

Filing at the wrong consulate. Consular jurisdiction is strict. Applications filed outside the district where you legally reside are rejected on intake.

Travel insurance instead of resident health insurance. Travel policies have deductibles and coverage caps. Consulates want full-coverage Spanish private insurance from a provider operating in Spain — Sanitas, Adeslas, DKV, Asisa.

Stale criminal records. The FBI background check, the UK ACRO certificate or equivalents must be issued within three months of application, apostilled, and translated. Many applicants get the document, then queue for an apostille appointment, then for sworn translation, and the original expires.

Underestimating the savings buffer. Hitting the 400% IPREM line exactly leaves no margin. Consulates want comfort.

Disclosing remote employment intentions. If you say in your cover letter that you plan to continue your remote job, expect refusal. The cleaner course — and the more honest one — is to apply for the visa designed for the activity you plan to do.

Assuming the visa stops at the consulate. Many applicants do not realise the empadronamiento-NIE-TIE chain inside Spain has its own 30-day clock.

Ignoring tax planning before arrival. The day you become Spanish resident, your worldwide tax base reorganises. Capital gains, IRA conversions, sales of appreciated property and business exits are far cheaper to execute as a non-resident.

When to consult a qualified professional

Before any material action, talk to:

- A Spanish immigration lawyer in the province where you will live, for document review and consulate-specific quirks.

- A tax advisor qualified in both your home jurisdiction and Spain, ideally six to twelve months before relocation, to model your post-move tax exposure and to identify pre-arrival actions.

- For US persons, a US CPA with Spain experience — the cross-border PFIC, Roth, Social Security and trust questions are not optional reading.

This article is journalism, not tax or legal advice. The non-lucrative visa is a YMYL decision: it affects your tax filings, your investment access, your healthcare and your right to return to work. Pay the professional fees once. See our editorial policy and disclaimer for how we research these pieces and what they are not.

Ready to act on this?

La Vida Golden Visas — UK-based golden-visa specialist. Soveraine readers go to the front of the line through our partner link, and you fund independent editorial in the process.

FAQ

Do you have to pay taxes in Spain with a non-lucrative visa?

If you spend more than 183 days in Spain in a calendar year, or your centre of economic interests is there, you become a Spanish tax resident and owe Spanish tax on your worldwide income. The non-lucrative visa effectively forces this outcome because it requires residence of more than 183 days per year to renew. Residents file IRPF, pay savings-income tax on dividends and capital gains, and may owe wealth tax depending on the autonomous community. Spain has double tax treaties with the US and most EU states, so foreign tax already paid is generally credited.

How do I get a non-lucrative visa for Spain?

Apply in person at the Spanish consulate covering your legal residence — not where you happen to be. Core documents: national visa form, passport with two years' validity, criminal record certificate from every country you have lived in for the past five years (apostilled and translated), private Spanish health insurance with no co-pay and full coverage, medical certificate, and proof of income or savings meeting 400% of IPREM plus 100% for each dependant. Consulate decisions take one to three months. You then enter Spain within the visa window and register your TIE card within 30 days.

Can I work remotely on a non-lucrative visa in Spain?

The Spanish government's official position is that the non-lucrative visa prohibits any work activity, including remote work for a foreign employer. In practice consulates have approved applicants with foreign passive income and ignored remote employment, but several have started rejecting applications where remote work is disclosed. If you intend to work remotely, the digital nomad visa created under the 2023 Startup Law is the correct vehicle — it is designed for it and grants access to a 24% flat tax regime. Using the non-lucrative visa as a workaround is a legal risk at renewal.

What happens after 5 years on a non-lucrative visa?

After five years of continuous legal residence in Spain you can apply for long-term EU residence, which removes the income-proof requirement and grants rights close to those of Spanish citizens except for voting and public-sector employment. After ten years of legal residence you can apply for Spanish citizenship — reduced to two years for nationals of Ibero-American countries, Andorra, the Philippines, Equatorial Guinea, Portugal and for Sephardic