Non-doms — short for non-domiciled individuals — were, until April 2025, one of the most distinctive features of the UK tax code. The status let long-term UK residents shelter foreign income and gains from British tax in exchange for a flat charge. It is now gone, replaced by a four-year residency-based regime. This article explains what the rules were, what replaced them, how the change affects readers of different nationalities, and where comparable regimes still exist in Europe and beyond. It does not cover UK inheritance tax in depth — that reform deserves its own piece — and it is not a substitute for advice from a chartered tax adviser.

Henley & Partners — Largest RBI/CBI advisory firm in the world

What is a non-dom

A non-dom was a person tax resident in the UK whose domicile, under English common law, lay elsewhere. Domicile is not citizenship and not residency. It is the country a person treats as their permanent home — the place they intend to return to, or where their father was domiciled when they were born.

Because the UK taxes residents on worldwide income by default, the practical use of non-dom status was the remittance basis: an election to pay UK tax only on UK-source income and on foreign income actually brought into the UK. Foreign income left abroad was untaxed in the UK, regardless of whether it was taxed elsewhere.

The regime traced back to 1799, when William Pitt the Younger introduced income tax to fund the Napoleonic Wars and exempted overseas colonial income from UK taxation. It survived, with modifications, for 226 years.

Who this applies to

The audience for this article splits three ways, and the practical takeaways differ sharply.

US persons

If you hold a US passport or a green card, the UK non-dom regime — old or new — never freed you from US tax. The United States taxes its citizens and lawful permanent residents on worldwide income regardless of where they live, under 26 U.S.C. § 1 and § 61. You still file Form 1040 every year. You still file FBAR (FinCEN Form 114) if your aggregate foreign accounts exceed $10,000 at any point in the year, and Form 8938 under FATCA if thresholds are met. The Foreign Earned Income Exclusion (IRS Publication 54) and foreign tax credits can reduce double taxation, but they do not eliminate filing obligations. Renunciation of citizenship — with the associated exit tax under IRC § 877A — is the only complete exit.

For US persons, the UK reform mainly changes UK-side planning, not US-side liability.

EU freelancers and digital nomads

EU tax residents are generally taxed on worldwide income once they meet residency tests — typically 183 days plus the "centre of vital interests" test under most double tax treaties modelled on the OECD Model Convention, Article 4. Most EU member states operate CFC (controlled foreign company) rules under the Anti-Tax Avoidance Directive (ATAD), and several — including France, Germany, the Netherlands and Spain — apply exit taxes on unrealised gains when you leave.

For this group, the relevant question is rarely "can I become a UK non-dom" but "is there a continental equivalent I can use without triggering my home country's exit tax." The answer is sometimes yes (see Italy and Portugal below), but the sequencing matters.

Non-US, non-EU readers

This is the segment with the most flexibility. If you hold, say, a South African, Indian, Singaporean or Australian passport and are not currently tax resident in a country with aggressive exit rules, the menu of options is wider. Several territorial-tax jurisdictions and special regimes — including the new UK FIG regime — are open to you without the home-country complications that bind US and EU readers.

What is a non-dom under the old rules

Under the regime that ran until 5 April 2025, claiming the remittance basis worked like this. You filed a UK Self Assessment return and ticked the relevant boxes on the SA109 supplementary pages. You then paid UK tax on:

- All UK-source income and gains, in full.

- Foreign income and gains only to the extent you remitted them to the UK.

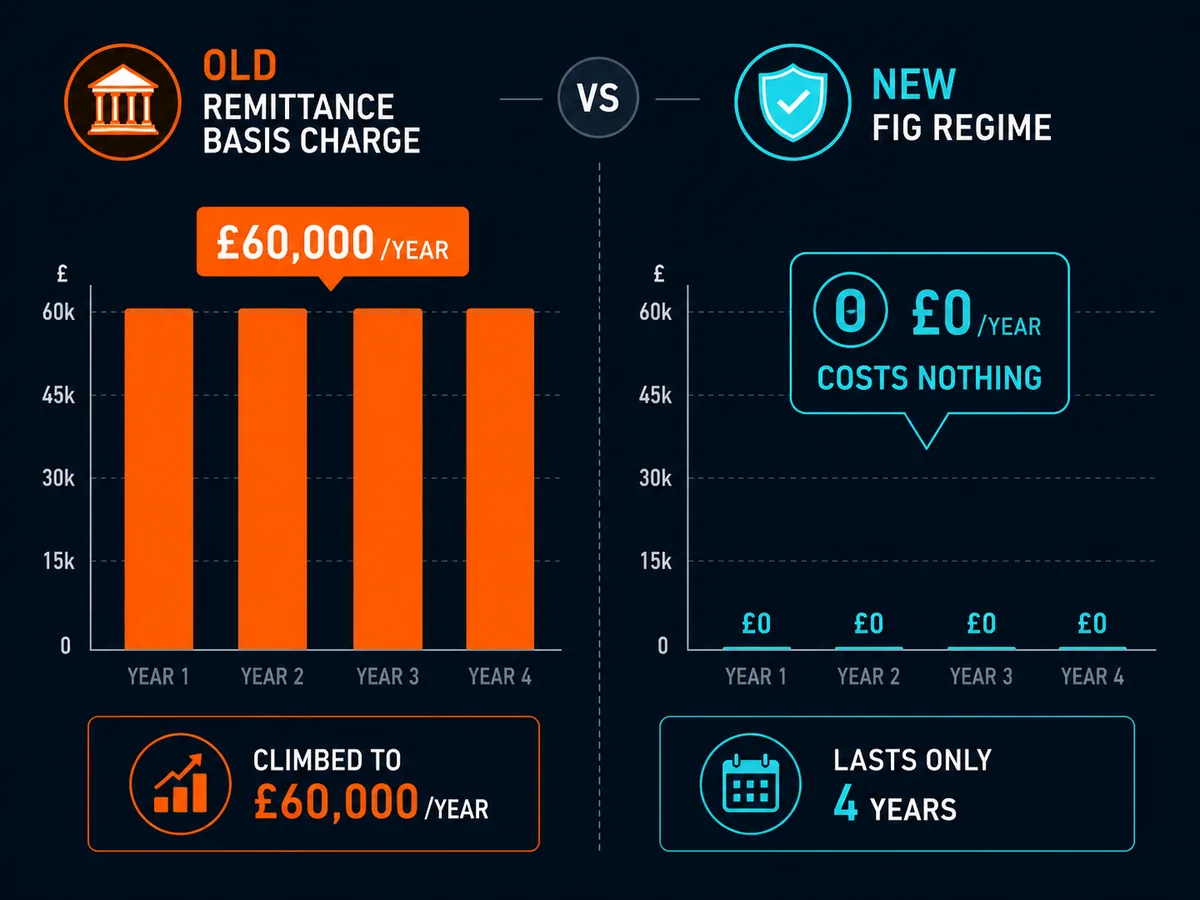

The cost climbed with tenure. From HMRC's published guidance:

- First seven of the last nine UK tax years: free, but you lost your personal allowance and CGT annual exemption.

- Seven of the last nine: £30,000 Remittance Basis Charge (RBC).

- Twelve of the last fourteen: £60,000 RBC.

- Fifteen of the last twenty: deemed domicile — full worldwide taxation, no election available.

The RBC was the price of admission, not a tax on the foreign income itself. For someone with £2m of untaxed offshore investment income, paying £60,000 to keep it outside the UK net was straightforward arithmetic.

How the non-dom rules are changing

In the Spring Budget 2024, the previous Conservative government announced the abolition of the regime. The incoming Labour government confirmed and tightened the reform in the Autumn Budget 2024. The legislation took effect on 6 April 2025.

The headline changes, drawn from HMRC's Reforming the taxation of non-UK domiciled individuals policy paper:

- Remittance basis abolished for income and gains arising on or after 6 April 2025.

- Foreign Income and Gains (FIG) regime introduced for new arrivals: 100% relief on foreign income and gains for the first four UK tax years of residence, provided the individual was non-resident for the prior ten tax years.

- Temporary Repatriation Facility (TRF): a window allowing former remittance-basis users to bring previously sheltered foreign income and gains into the UK at reduced rates — 12% in 2025/26 and 2026/27, rising to 15% in 2027/28.

- Rebasing of foreign assets to 5 April 2017 values for CGT purposes, available to qualifying former non-doms.

- Inheritance tax moved to a residence-based system: a "long-term resident" — broadly someone UK resident in at least ten of the previous twenty tax years — is liable to UK IHT on worldwide assets.

The FIG regime is, in international comparison, quite generous for its four years and quite limited beyond them. There is no equivalent to the old fifteen-year runway.

How do you become a non-dom now

You do not become a non-dom under the new regime — the legal category no longer determines income tax treatment. You can, however, qualify for the FIG four-year relief by meeting two tests:

- You become UK tax resident under the Statutory Residence Test (HMRC RDR3).

- You were not UK tax resident in any of the ten consecutive tax years immediately before your year of arrival.

That is it. There is no fee, no application, no domicile analysis. You claim FIG relief on your Self Assessment return for each of the four qualifying years. You lose your personal allowance and CGT annual exemption for any year you claim, just as remittance-basis users did.

After four years, you are taxed on worldwide income and gains like any other UK resident, subject to relief under double tax treaties.

What were the current rules for non-dom status

For the avoidance of doubt — and because much of the SERP still indexes pre-reform commentary — the current rules (tax year 2025/26 onwards) are:

- No remittance basis.

- FIG regime available to qualifying new arrivals for four years.

- TRF available to former remittance-basis users until 5 April 2028.

- Worldwide taxation for everyone else, on an arising basis.

- Residence-based IHT after ten of twenty years of UK residence.

The status "non-dom" persists as a common-law concept for some non-tax purposes (such as succession in certain estates), but it no longer drives UK income tax, capital gains tax or — from April 2025 — inheritance tax.

How many non-doms are there and who are they

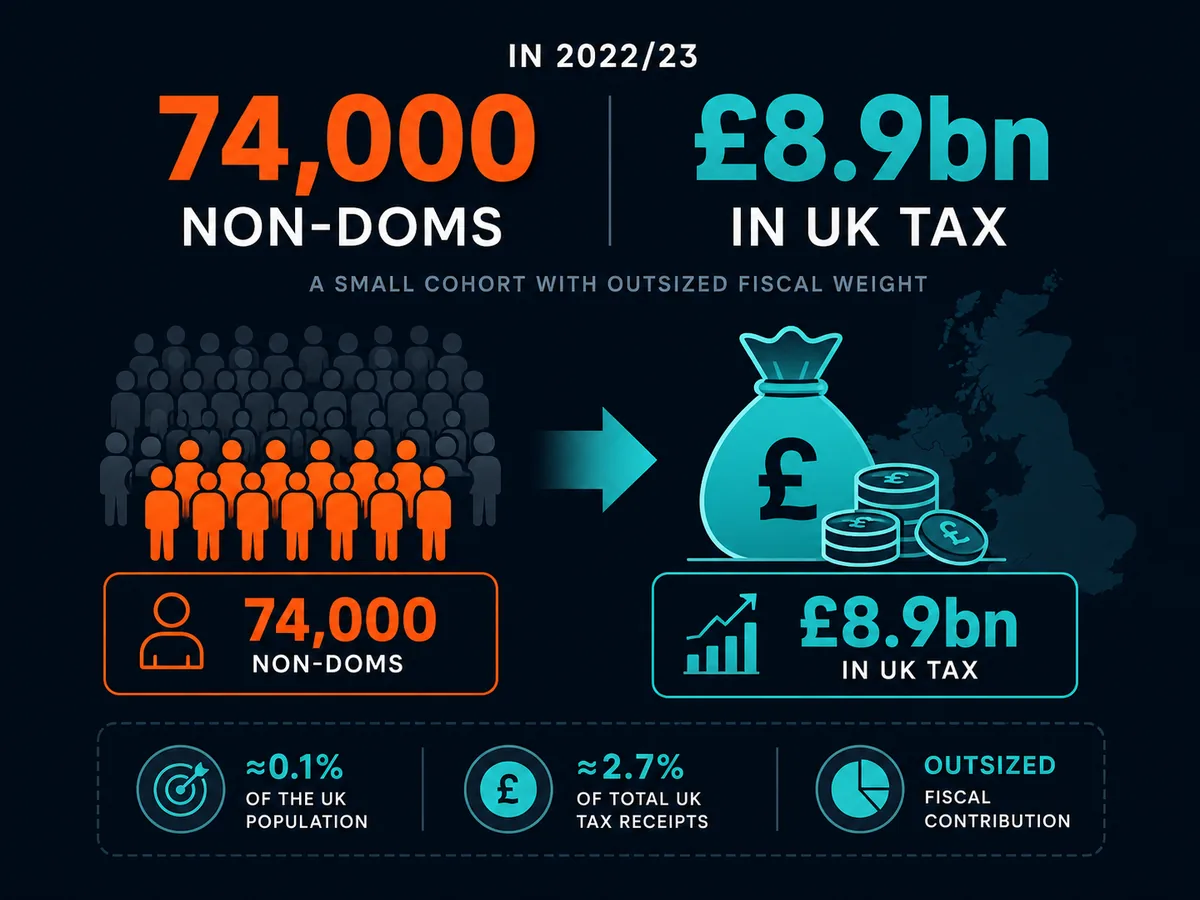

HMRC's most recent published statistics on non-domiciled taxpayers recorded approximately 74,000 individuals claiming non-domiciled status in the 2022/23 tax year, contributing around £8.9bn in UK taxes. Roughly 37% of non-doms lived in London, and the largest source countries were India, the United States, France, Italy and Germany.

Research from the LSE's International Inequalities Institute and the University of Warwick found that around one in five top earners in finance had claimed non-dom status at some point, and that the regime was heavily concentrated in a small number of postcodes — Kensington, Westminster, the City.

Whether the population has fallen materially since April 2025 is contested. Oxford Economics estimated a higher departure rate than the Office for Budget Responsibility's 12% assumption. The Treasury's projected revenue gain of £12.7bn over five years depends on those assumptions holding. The true number will not be clear until 2026/27 returns are filed.

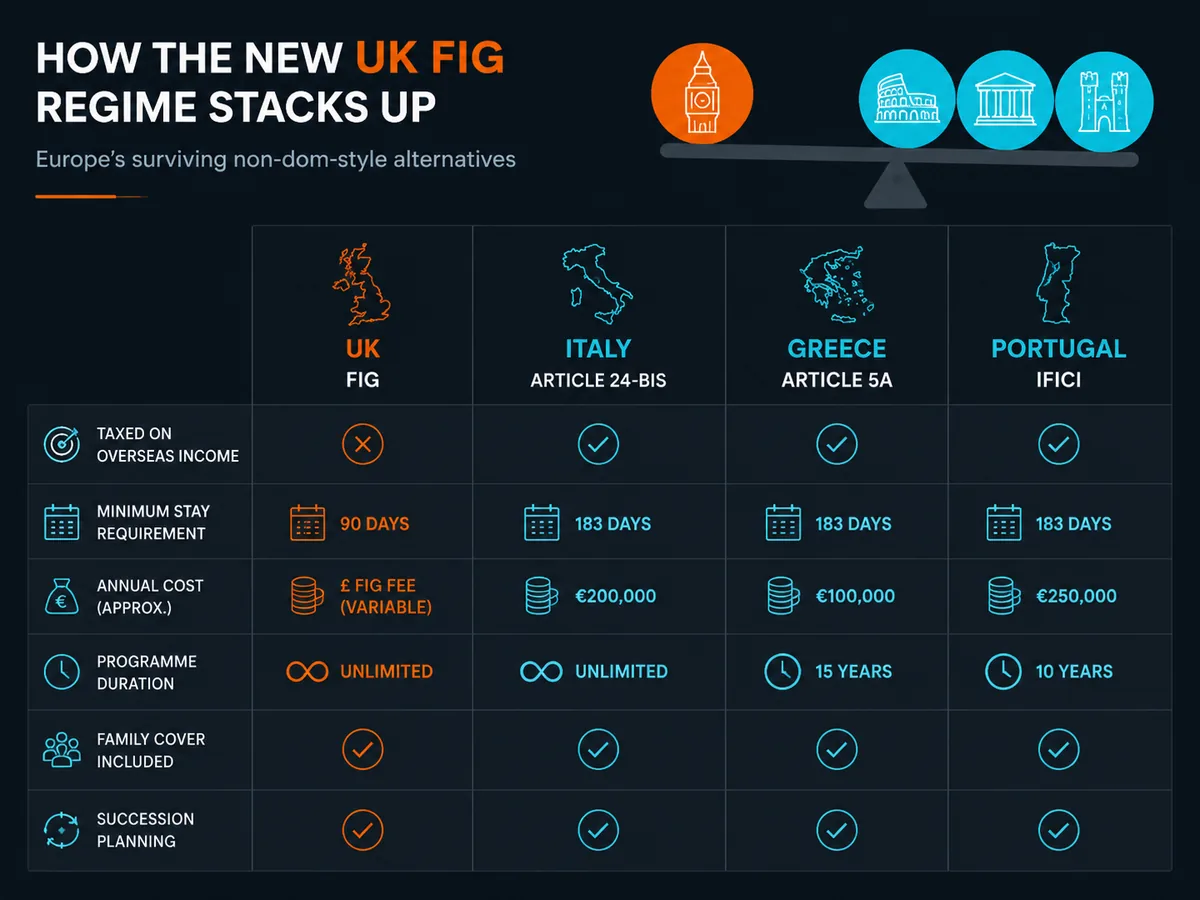

Comparable regimes still open

For readers considering alternatives to the UK, three European regimes deserve mention. None replicates the old non-dom system exactly, and each carries trade-offs.

Italy — flat tax for new residents

Italy's Article 24-bis flat tax regime charges a €200,000 flat annual tax on all foreign-source income, irrespective of amount (raised from €100,000 in August 2024). It runs for up to fifteen years. The applicant must not have been Italian tax resident in nine of the prior ten years. Family members can be added for €25,000 each.

This is the closest current European analogue to the old UK regime, and it is where a significant number of departing non-doms have reportedly gone.

Portugal — NHR 2.0 (IFICI)

Portugal's original Non-Habitual Resident regime closed to new applicants in 2024. Its replacement, the Incentivised Tax Status for Scientific Research and Innovation (IFICI), offers a 20% flat rate on qualifying Portuguese-source professional income and exemption on most foreign income for ten years — but only to applicants in specified high-skilled professions (research, technology, certain engineering and academic roles). It is narrower than NHR and not a direct non-dom substitute.

Greece — €100,000 flat tax

Greece offers a non-dom regime under Article 5A of the Income Tax Code: a flat €100,000 annual tax on foreign income for up to fifteen years, with a €20,000 supplement per family member. The applicant must invest at least €500,000 in Greek real estate, business or securities within three years.

Realistic costs, fees and timeline

| Regime | Annual cost | Duration | Residency requirement | Investment required |

|---|---|---|---|---|

| UK FIG (new, from 2025) | £0 | 4 years | 10 prior years non-resident | None |

| UK non-dom (pre-2025) | £0–£60,000 | Up to 15 years | None | None |

| Italy Art. 24-bis | €200,000 | Up to 15 years | 9 of 10 prior years non-resident | None |

| Greece Art. 5A | €100,000 | Up to 15 years | 7 of 8 prior years non-resident | €500,000 |

| Portugal IFICI | Variable (20% on PT income) | 10 years | 5 prior years non-resident | None, but profession-restricted |

Sources: HMRC, Agenzia delle Entrate, AADE Greece, Portuguese Tax Authority.

Timelines for setup are typically two to six months once you have a tax adviser engaged, a residence permit in hand (where required for non-EU applicants), and an opening tax ruling or election filed. For Italy, the optional advance ruling from the Agenzia delle Entrate adds three to four months but is recommended to confirm eligibility before you move.

Common mistakes and how to avoid them

Confusing residency with domicile. Under the old UK regime, many readers assumed that moving abroad changed their domicile. It did not, unless they also abandoned all UK ties and intended to live in the new country indefinitely. The new regime sidesteps this trap by using residency only.

Triggering an exit tax on the way out. For French, German, Dutch and Spanish residents, leaving with substantial unrealised gains can crystallise a tax bill before you have set foot in your new country. Check your home jurisdiction's exit-tax rules under ATAD before booking the moving van.

Assuming a US passport gets a pass. It does not. No European regime overrides US worldwide taxation. The FIG regime, the Italian flat tax and the Greek €100,000 election all reduce local tax. They do not reduce US tax. You will likely owe the US the difference, subject to foreign tax credits.

Banking the remittance basis without tracking remittances. Under the old UK regime, mixed accounts containing pre- and post-residence funds were a documentation nightmare. Many non-doms paid more tax than necessary because they could not prove which money was "clean capital". If you are using the TRF window, get your records straight before designating funds.

Treating provider marketing as legal advice. Several relocation firms publish guides that conflate "what HMRC has said it will accept" with "what the statute actually permits." They are not always the same. Read the underlying HMRC policy paper and the Finance Act 2025 before relying on any third-party summary.

When to consult a qualified professional

Anything involving a six- or seven-figure move between tax systems is not a DIY project. You should engage:

- A chartered tax adviser (CTA) or solicitor in your departing country, to model the exit position.

- A dottore commercialista, steuerberater, expert-comptable or equivalent in your destination, to confirm the local treatment and file any advance rulings.

- For US persons, a US-qualified CPA or enrolled agent with international experience, because no European adviser will handle your 1040, FBAR or Form 8938.

Disclosure: Soveraine does not provide tax advice. We link to professional bodies and primary sources; we do not have an affiliate relationship with any of the tax authorities cited. See our editorial policy, disclaimer and affiliate disclosure for how we handle commercial relationships.

Ready to act on this?

Henley & Partners — Largest RBI/CBI advisory firm in the world. Soveraine readers go to the front of the line through our partner link, and you fund independent editorial in the process.

FAQ

Who are non-doms?

Until April 2025, a non-dom was a UK tax resident whose permanent home — their domicile — was treated under English common law as being outside the UK. Domicile is a separate concept from residency: you can live in London for years and still be domiciled in, say, India or South Africa if that is where your father was domiciled when you were born and you intend to return there eventually. The status mattered because non-doms could elect the remittance basis, paying UK tax only on UK-source income and foreign income they brought into the country.

What does it mean to be non-domiciled?

Being non-domiciled means HMRC accepts that your long-term permanent home is somewhere other than the UK, even though you currently live there. Domicile follows the rules in English common law: you acquire a domicile of origin at birth (usually your father's), and to change it you must move to a new country and demonstrate the intention to live there indefinitely. Non-dom status was never automatic — you claimed it on a Self Assessment return, and HMRC could challenge it. From 6 April 2025, the concept no longer drives UK income tax treatment.

How long can non-doms stay in the UK?

Under the old regime, non-doms could remain UK resident indefinitely, but the remittance basis charge climbed with time: £30,000 a year after seven of the last nine tax years, £60,000 after twelve of fourteen. After fifteen years of UK residence in the last twenty, they were treated as deemed domiciled and taxed on worldwide income. Under the new FIG regime from April 2025, the relief lasts only four years from the date you become UK tax resident, provided you were non-resident for the previous ten.

Are non-doms leaving the UK?

Some are. Reports from advisers including Oxford Economics and Henley & Partners suggest a meaningful outflow of high-net-worth individuals during 2024 and 2025, with Italy, the UAE, Switzerland and Monaco the most cited destinations. Exact numbers are disputed — the Office for Budget Responsibility assumed a 12% departure rate when costing the reform, while industry groups argue the real figure is higher. The honest answer: it is too early to know the net fiscal impact, and government estimates and lobby-group estimates differ by an order of magnitude.

How does domicile differ from residency?

Residency is about where you physically live and is tested mostly by day counts and ties — in the UK, via the Statutory Residence Test. Domicile is about where your permanent home is in a deeper, common-law sense: where you intend to end up. You have one domicile at a time but can be tax resident in several countries simultaneously. Most countries use only residency to decide who pays tax on worldwide income. The UK was unusual in using domicile as a parallel concept, and that quirk is what the 2025 reform removed.

How do you become a non-dom now?

You do not — at least not in the old sense. From 6 April 2025, the remittance basis was abolished and replaced with the FIG regime, which is residency-based, not domicile-based. To qualify, you must become UK tax resident after at least ten consecutive years of non-residence. You then get four tax years of relief on fore