"Non-dom" is one of the most misused phrases in international tax. It is not a country. It is not a visa. It is not zero tax. It is a category of taxpayer in a small number of common-law jurisdictions whose foreign-source income is taxed on a remittance basis rather than on the worldwide arising basis used by most of the world. The UK — the country that invented the modern concept — abolished its non-dom regime from 6 April 2025. This article explains what the term actually means, what survives after the UK exit, and why so much of the SERP is still indexing the pre-2025 rules.

Henley & Partners — Largest RBI/CBI advisory firm in the world

What "non-dom" actually means

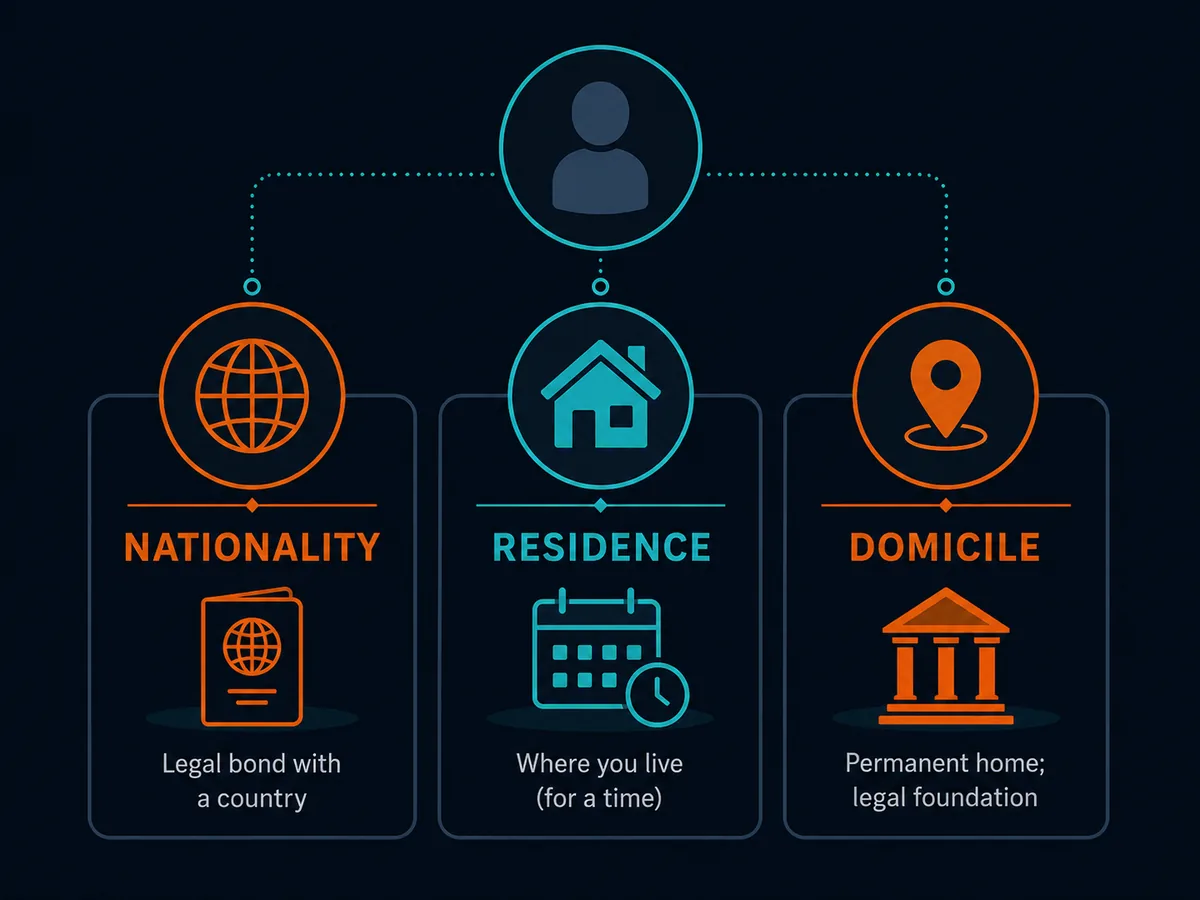

A non-dom is a person who is tax resident in one country while remaining, under that country's common-law rules, domiciled in another. Domicile is not residence, not citizenship, and not nationality. It is the country a person treats as their permanent home — the place they intend to return to or remain in indefinitely.

The concept comes from English common law, where domicile has three forms:

- Domicile of origin — acquired at birth, traditionally from one's father (mother's, if parents unmarried). It never disappears; it can only be displaced.

- Domicile of choice — acquired by moving to a new country with the intention to live there indefinitely. Abandon the new country without forming an intent to live in a third, and the domicile of origin revives.

- Domicile of dependence — applied to minors and, historically, to married women.

Because the test for changing a domicile of choice is intentional rather than mechanical, a person can live abroad for decades while remaining domiciled at home. HMRC's RDR1 manual — the 200-page reference text that governed UK practice until 2025 — devoted dozens of pages to the evidential question of when, exactly, a person's domicile had moved.

The practical use of non-dom status, where it exists, is the remittance basis: a method of taxing foreign income and gains only when the money is actually brought into the country of residence. Money left abroad in foreign bank accounts, foreign portfolios or foreign property sits outside the local tax net. Money wired home, used to pay a local credit card, or used to buy local property becomes a remittance and is taxed in the year of remittance.

This contrasts with the default arising basis used by almost every country in the world, under which foreign income is taxed in the year it accrues, regardless of where the money sits.

Who this applies to — read this first

The audience for "non dom meaning" splits three ways, and the relevance differs sharply across the three. Reading the section that matches your situation first will save you time on the rest of the article.

US persons

If you hold a US passport or a green card, the term "non-dom" in foreign income tax law has almost no relevance to your US filing. The United States taxes its citizens and lawful permanent residents on worldwide income regardless of residence, under 26 U.S.C. §1 and §61. Whether you are domiciled in Texas, Cyprus or the Cayman Islands, you still file Form 1040 every year, you still file FBAR (FinCEN Form 114) on aggregate foreign accounts over $10,000, and you still file Form 8938 above the FATCA thresholds.

The word "domicile" does appear in the US tax code, but in a specific and limited sense. Under IRC §2001 and the regulations at §7701(b) and Treas. Reg. §20.0-1(b), domicile determines exposure to US estate and gift tax for non-citizens. A non-US citizen domiciled in the US is taxed on worldwide assets at death; a non-US citizen non-domiciliary is taxed only on US-situs assets. For income tax, US citizens and green-card holders are taxed by citizenship and lawful status, not by domicile.

If you are a US person becoming Cyprus, Irish, Maltese or Greek non-dom, the local relief reduces your foreign tax bill. Your US position is unchanged, and the foreign tax credit (IRC §901) on a reduced foreign tax will produce a smaller credit — meaning your overall liability can fall less than the brochure suggests.

EU residents

Most EU member states are civil-law jurisdictions that recognise only residence, not domicile, as the basis of personal tax liability. The concept of non-dom has no domestic meaning in France, Germany, Spain, Italy, the Netherlands or the Nordic countries. Residence is tested under the relevant code — typically 183 days plus a "centre of vital interests" tiebreaker under OECD Model Tax Convention, Article 4 — and worldwide taxation follows automatically.

Two practical implications:

- Civil-law countries with special regimes (Italy's flat tax, Greece's Article 5A, Portugal's old NHR and current IFICI) are sometimes described as "non-dom regimes" in media coverage. They are not non-dom regimes in the legal sense; they are special resident regimes with a flat or reduced tax on foreign income. The exception is Greece's Article 5A, which is technically structured as a non-dom election.

- Exit taxes under the EU Anti-Tax Avoidance Directive (ATAD) can crystallise unrealised gains on the way out of France, Germany, the Netherlands or Spain. Plan the exit sequencing before claiming any foreign non-dom regime, because the trip itself can be the most expensive tax event in the chain.

Non-US, non-EU readers

This is the group for whom non-dom status, where it survives, is most usable. South African, Indian, Australian, Singaporean, Hong Kong, UAE and Commonwealth-passport readers face neither US-style citizenship-based taxation nor EU-style exit-tax rules. Cyprus, Ireland, Malta and Greece are all open to them subject to the relevant immigration permission, and the choice between regimes turns on practical factors — banking access, real estate prices, school options, time-zone fit — rather than on home-country tax constraints.

The UK abolition — what changed in April 2025

For 226 years, from William Pitt the Younger's introduction of income tax in 1799 until 5 April 2025, the UK operated a remittance-basis system for non-domiciliaries. From 6 April 2025, that system is gone.

The legislation is in the Finance (No. 2) Act 2025, and the policy detail in HMRC's Reforming the taxation of non-UK domiciled individuals paper. The headline changes:

- The remittance basis is abolished for foreign income and gains arising on or after 6 April 2025.

- A new Foreign Income and Gains (FIG) regime offers 100% UK tax relief on foreign income and gains for the first four UK tax years of residence, for individuals who were non-UK resident for the prior ten consecutive tax years. It is residency-based — domicile is no longer the trigger.

- A Temporary Repatriation Facility (TRF) allows former remittance-basis users to bring previously sheltered foreign income and gains into the UK at reduced rates — 12% in tax years 2025/26 and 2026/27, rising to 15% in 2027/28.

- Inheritance tax moves from a domicile-based to a residence-based test. A "long-term resident" — broadly someone UK resident in at least 10 of the previous 20 tax years — is liable to UK IHT on worldwide assets, with a tail period after departure.

- The old £30,000 / £60,000 Remittance Basis Charges and the 15-year deemed domicile rule for income tax are gone.

Why this triggered the visible HNW outflow from London in late 2024 and 2025 is straightforward arithmetic. For a non-dom with substantial offshore investment income, paying a £60,000 RBC to keep that income outside the UK tax net was a small price. Switching to worldwide taxation on the arising basis turns the same person into a top-rate UK taxpayer on the full foreign return. Industry advisers — Henley & Partners among them — reported a meaningful shift of clients to Italy, the UAE, Switzerland, Monaco, Cyprus and Dubai through 2024 and early 2025.

The Office for Budget Responsibility, in its October 2024 Economic and Fiscal Outlook, assumed a 12% departure rate among affected non-doms when costing the reform at roughly £12.7bn over five years. Industry research (Oxford Economics, commissioned by Foreign Investors for Britain) estimated a higher departure rate. As with most behavioural-response assumptions in tax policy, the truth will not be visible until 2026/27 self-assessment returns are filed and HMRC publishes its non-domiciled taxpayers statistics for the post-reform years.

What's left after the UK exit

Four European jurisdictions still operate meaningful non-dom or remittance-style regimes for individuals. None replicates the old UK system exactly, and each has its own qualification rules, costs and edge cases. The legal basis in each case is set out in the country's own tax code — the links below go to the relevant authority.

Cyprus non-dom

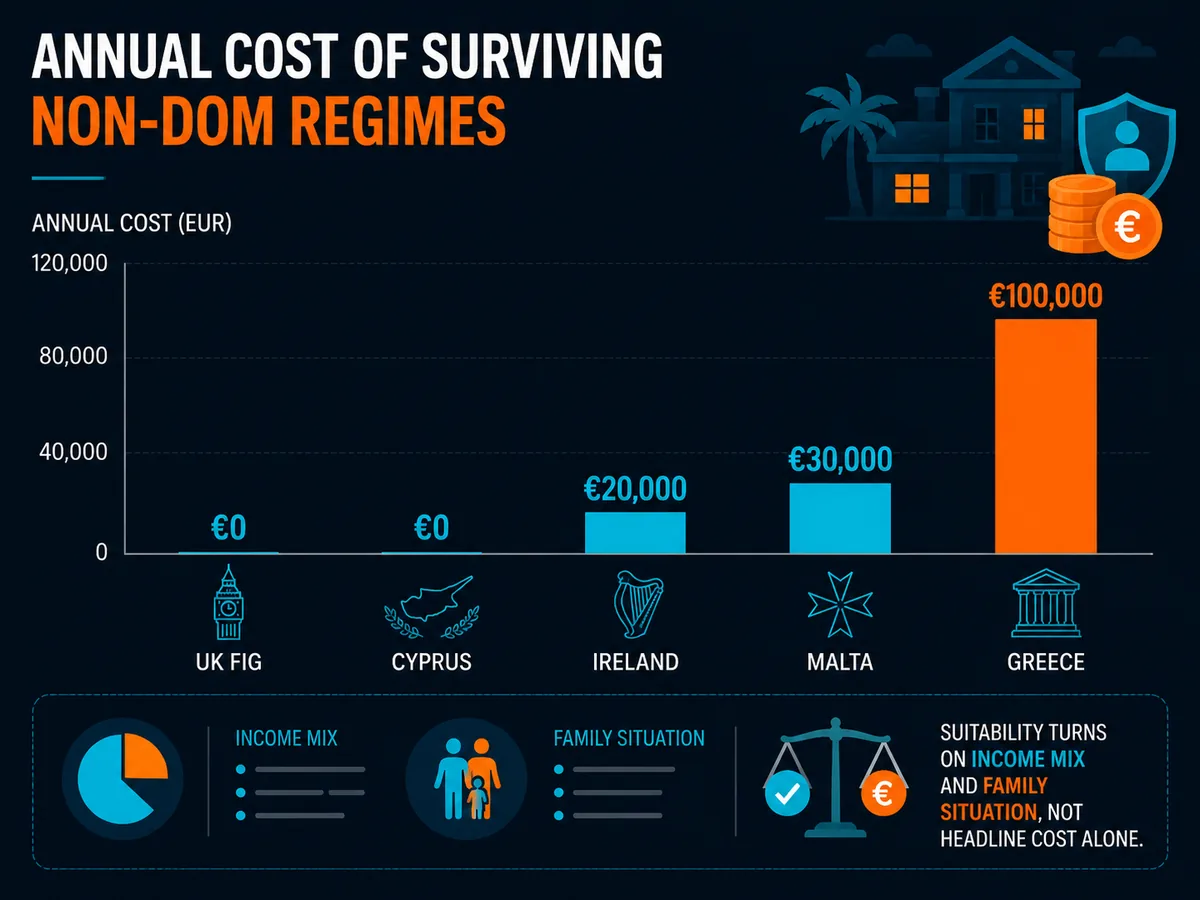

Cyprus introduced its non-dom regime in 2015. A Cyprus tax resident classified as non-domiciled is exempt from the Special Defence Contribution (SDC), which would otherwise apply at 17% on dividends, 17% on most interest and 3% on rental income. The exemption lasts up to 17 years from the year residence is established.

A person qualifies if they have not been Cyprus tax resident for at least 17 of the prior 20 years and is not Cypriot-domiciled of origin. Tax residency itself can be established by the 183-day rule or — uniquely in the EU — the 60-day rule: 60 days in Cyprus, no other tax residence, business or employment ties to the island, and a permanent residence (owned or rented). See the Cyprus Ministry of Finance — Tax Department.

Exempt: dividends, interest, capital gains on most securities. Not exempt: employment income (taxed at progressive rates up to 35%, though a 50% exemption for income over €55,000 may apply for new arrivals), Cyprus-source rental, and gains on Cyprus immovable property. Standard social insurance and GeSY contributions still apply.

Ireland non-dom

Ireland never closed its non-dom regime — the remittance basis remains available under sections 71 and 73 of the Taxes Consolidation Act 1997. An Irish tax resident who is non-domiciled is taxed on Irish-source income in full and on foreign income only to the extent it is remitted to Ireland. There is no fixed expiry.

One cost layer matters: the Domicile Levy of €200,000 per year, payable by individuals who are Irish-domiciled with worldwide income over €1m, Irish property over €5m, and Irish income tax under €200,000. It targets HNW Irish-domiciled emigrants rather than non-doms directly, but sets the political tone of the regime. See Revenue — Domicile.

Foreign income and gains not remitted are exempt. Irish-source income and indirect remittances (paying off a foreign credit card used in Ireland counts) are not.

Malta non-dom

Malta operates a remittance basis for resident non-doms under the Income Tax Act, Chapter 123 of the Laws of Malta. A minimum annual tax of €5,000 applies to resident non-doms with foreign income of at least €35,000, whether or not remitted (introduced 2018). Capital gains on foreign assets are not taxable in Malta even if remitted. See Commissioner for Tax and Customs.

Exempt: foreign-source income not remitted to Malta, all foreign capital gains. Not: Malta-source income, foreign income remitted to Malta, and gains on Malta-situs assets. Standard rates on Malta-source income reach 35%.

Greece HNW non-dom (Article 5A)

Greece introduced an Article 5A regime in 2019 for HNW non-doms. An eligible individual elects to pay a flat €100,000 annual tax on all foreign-source income, with no further Greek income tax on foreign income regardless of amount. The regime lasts up to 15 years, with family members added for €20,000 each per year.

Qualification requires the applicant was not Greek tax resident in 7 of the prior 8 years and commits to invest at least €500,000 in Greek real estate, business or securities within three years. See AADE — Article 5A guidance. Greek-source income remains taxable at standard progressive rates.

How non-dom interacts with US tax filing

For a US person electing non-dom status in any of the four jurisdictions above, the IRS's position is uncomplicated and rarely advantageous. The US taxes worldwide income on an arising basis. Foreign non-dom relief reduces the foreign tax actually paid, which in turn reduces the foreign tax credit available under IRC §901. The net US position can be similar to or worse than living in a high-tax jurisdiction, depending on the income mix.

Specific issues to model with a cross-border CPA: PFIC rules under IRC §1297 on non-US mutual funds and ETFs (including those held inside a Cyprus or Malta brokerage), where Form 8621 and the excess-distribution mechanics can make ordinary investing punitive; Subpart F and GILTI under §951–§951A, which pull profits from a controlled foreign corporation back into the US shareholder's income regardless of distribution; and the exit tax under IRC §877A, which applies to long-term green-card holders who renounce LPR status — run the numbers before giving up the card.

The bona fide residence test under §911 (covered in our bona fide resident pillar) can exclude up to $130,000 of qualifying earned income for tax year 2025 (IRS Rev. Proc. 2024-40). It does not exclude passive income, capital gains or any income above the cap. Becoming a Cyprus non-dom does not make a US person a non-US taxpayer.

Comparison — what survives in 2026

The five remaining regimes, side by side. Sources: HMRC, Cyprus MoF, Irish Revenue, Malta CFR, AADE Greece.

| Regime | Foreign income treatment | Minimum / flat tax | Maximum duration | Residency requirement |

|---|---|---|---|---|

| UK FIG (from 6 Apr 2025) | 100% relief on foreign income & gains, then full worldwide taxation | None | 4 years | 10 prior years non-resident |

| Cyprus non-dom | Exempt from SDC on dividends, interest, rental | None | 17 years | 60-day or 183-day rule |

| Ireland non-dom | Remittance basis on foreign income & gains | None (€200k Domicile Levy only for HNW Irish-domiciled) | Indefinite | Standard Irish residency tests |

| Malta non-dom | Remittance basis (capital gains exempt even if remitted) | €5,000/year (if foreign income ≥ €35k) | Indefinite | Ordinary residence in Malta |

| Greece Art. 5A | Foreign income covered by flat tax | €100,000/year + €20k per family member | 15 years | 7 of prior 8 years non-resident, €500k investment |

The traps — where the meaning of "non-dom" stops being clean

The status looks portable on paper. In practice, three layers of rules turn what looks like a clean offshore election into a fight on multiple fronts.

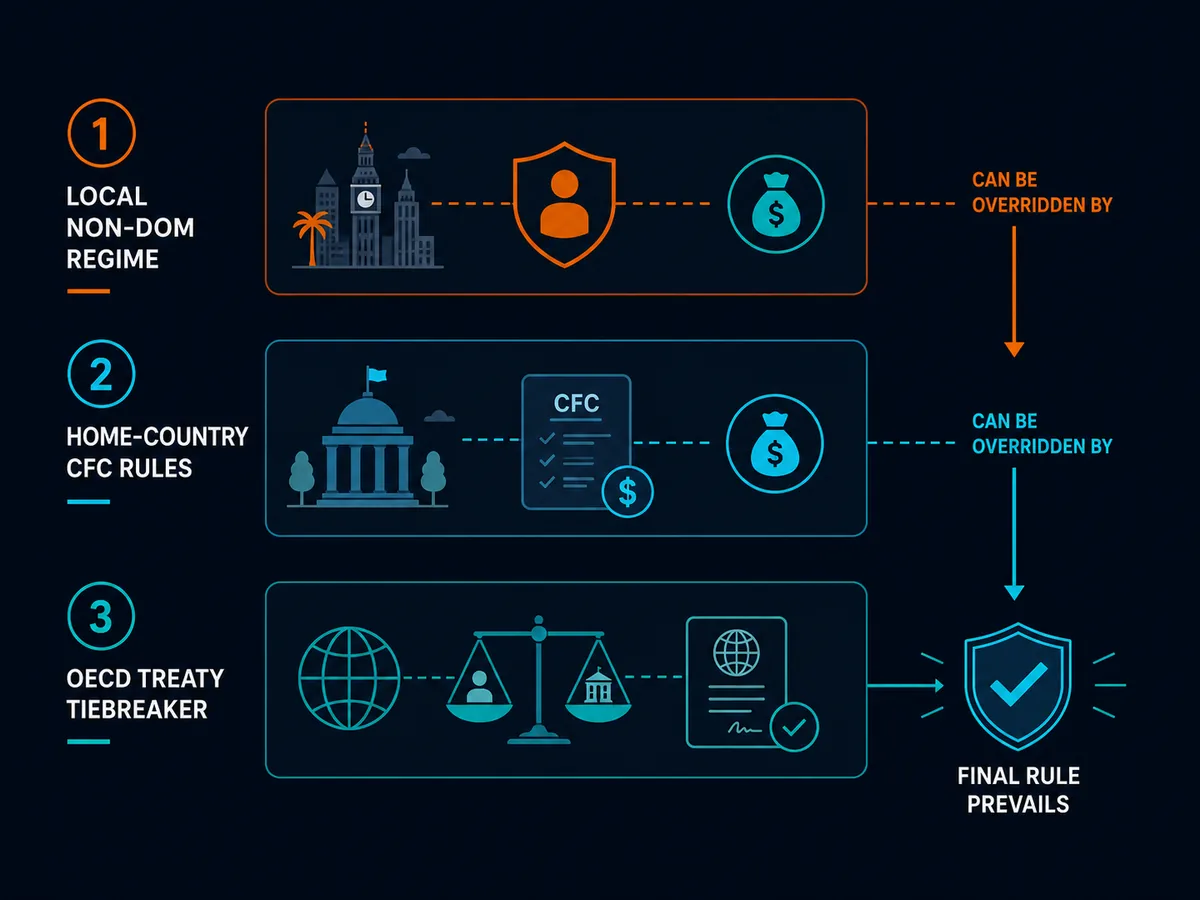

Substance requirements. The Cyprus 60-day rule sounds light until the practical substance is in view: it requires a permanent residence (owned or rented), business or employment ties to Cyprus, and no other country of tax residence. Without those, the day-count alone does not establish Cyprus residency, and the non-dom relief evaporates. Malta and Ireland both rely on the "ordinary residence" concept, with its own evidential expectations.

Home-country CFC rules. EU member states implementing ATAD and the UK's CFC regime under TIOPA 2010 can pull profits from a non-dom's Cyprus or Maltese holding company back into the home-country tax base if substance is thin and effective rates fall below the threshold. The destination-country non-dom regime does not prevent this — only genuine business activity does.

OECD treaty tiebreaker. A person resident in two countries simultaneously is treated by their treaty network as resident in only one, under Article 4(2) of the OECD MTC: permanent home, centre of vital interests, habitual abode, nationality. A Cyprus non-dom who keeps a London family home and commutes weekly may find HMRC arguing — under the UK-Cyprus DTT — that the centre of vital interests is still in the UK.

CRS reporting unchanged. The OECD Common Reporting Standard (CRS) requires participating jurisdictions to exchange financial-account information annually. Becoming a Cyprus non-dom does not hide a Cyprus brokerage account from prior or remaining tax residences. Non-dom relief is a taxation mechanism; CRS is a reporting mechanism.

Mixed-fund problems. Under the old UK rules, remittance-basis users routinely paid more tax than necessary because offshore accounts mixed pre-residence "clean capital" with post-residence income. The same problem applies in Ireland, Malta and Cyprus where the remittance mechanic survives. Segregated accounts and contemporaneous records matter from day one.

When to talk to a professional

Anything involving a meaningful move between tax systems is not a DIY exercise. The advisers needed are usually a chartered tax adviser (CTA) or solicitor in the departing country to model the exit position; a local tax adviser in the destination — a chartered accountant in Ireland, a dottore commercialista equivalent in Malta, a Cyprus-qualified tax adviser, or a Greek-qualified accountant familiar with Article 5A; for US persons, a US-qualified CPA or enrolled agent with cross-border experience (no European adviser will sign your 1040, FBAR or 8938); and for families, a succession lawyer in both jurisdictions — domicile drives intestate succession in many common-law countries, and abolishing the income-tax meaning of non-dom in the UK has not changed the succession-law meaning.

Soveraine does not provide tax, legal or financial advice. The links in this article go to primary statutory and tax-authority sources; read them directly before relying on any provider summary. See our editorial policy, disclaimer and affiliate disclosure.

For the country-by-country comparison — Italy, Portugal IFICI, and others alongside the four covered here — see our companion pillar on non-doms, which takes the destination-by-destination view rather than the conceptual one above.

Ready to act on this?

Henley & Partners — Largest RBI/CBI advisory firm in the world. Their tax-residency planning team handles exactly the cross-border domicile and remittance-basis questions this article frames. Soveraine readers go to the front of the line through our partner link, and you fund independent editorial in the process.

FAQ

What does "non-dom" actually mean?

"Non-dom" is short for non-domiciled, a term from English common law adopted by a handful of countries — historically the UK, and still Ireland, Cyprus, Malta, India and others. It describes a tax resident whose permanent home, in the legal sense of domicile, lies in another country. The practical effect, where the regime survives, is that foreign-source income is taxed only when remitted to the country of residence rather than on a worldwide arising basis. It is not a country, not a visa, and not a zero-tax status.

Is non-dom status the same as residency?

No. Residency is where you currently live, tested by day counts and ties. Domicile is where, under common-law rules, you have your permanent home — typically inherited from your father at birth (a "domicile of origin") and changeable only by moving abroad with the intent to live there indefinitely (a "domicile of choice"). You can be a UK or Irish resident and a non-dom at the same time. Most civil-law countries — France, Germany, Spain, Italy — recognise only residency, so the concept has no domestic meaning there.

Is the UK non-dom regime really abolished?

Yes. From 6 April 2025, the remittance basis of taxation for non-doms was abolished by the Finance Act 2025, following the Autumn Budget 2024. It was replaced by the Foreign Income and Gains (FIG) regime, a four-year residency-based relief for new arrivals who were non-resident for the prior ten tax years. Inheritance tax also shifted from a domicile-based to a residence-based test. The common-law concept of domicile still exists for succession purposes, but it no longer drives UK income, capital gains or inheritance tax.

Where can I still claim non-dom status in 2026?

Four jurisdictions in Europe still operate meaningful non-dom or remittance-style regimes: Cyprus (17-year exemption on dividends, interest and capital gains for individuals classified as non-dom), Ireland (remittance basis on foreign income for non-doms, with a €200,000 Domicile Levy for high earners), Malta (remittance basis with a minimum annual tax of €5,000 for resident non-doms), and Greece (a flat €100,000 annual tax on worldwide foreign income for HNW non-doms under Article 5A, for up to 15 years).

Does non-dom status reduce US tax for Americans?

No. The United States taxes its citizens and lawful permanent residents on worldwide income regardless of residence or domicile (IRC §1 and §61). Becoming a non-dom in Cyprus or Greece reduces the local tax bill, not the US one. Foreign tax credits and the foreign earned income exclusion may offset double taxation, but Form 1040, FBAR and Form 8938 filing obligations continue. "Domicile" in US tax law affects estate and gift tax under §2001 and §7701(b), not income tax.

What is the remittance basis?

The remittance basis is a method of taxing foreign income only when it is brought — remitted — into the country of residence. Money left in foreign bank accounts, foreign investments or foreign property is outside the local tax net. Money transferred to the country, used to pay credit cards there, or used to buy assets there is taxable on remittance. It originated in 18th-century British colonial tax practice and survives in Ireland, Malta and (in modified form) Cyprus, alongside Article 5A in Greece.

What is the difference between domicile and nationality?

Nationality is your legal citizenship, granted by a state. Domicile is a common-law concept of permanent home, independent of citizenship. A British national can be domiciled in India; an Indian national can be domiciled in England. Tax law in most countries treats them as wholly separate concepts. The US is unusual in linking worldwide income tax to citizenship rather than residence or domicile; the UK was unusual until 2025 in linking certain reliefs to domicile rather than residence.

Why did the UK abolish the non-dom regime?

The Conservative government announced abolition in the Spring Budget 2024 to broaden the tax base, and the incoming Labour government confirmed and tightened it in the Autumn Budget 2024. HM Treasury projected revenue of around £12.7bn over five years, on the assumption of a 12% departure rate for affected individuals (Office for Budget Responsibility, October 2024). Industry estimates of departure are higher. The honest position: the long-run fiscal effect will not be known until 2026/27 returns are filed.

Sources

- HMRC — RDR1: Residence, domicile and the remittance basis (reference manual). https://www.gov.uk/government/publications/residence-domicile-and-remittance-basis-rules-uk-tax-liability

- HMRC — Changes to the taxation of non-UK domiciled individuals (policy paper). https://www.gov.uk/government/publications/changes-to-the-taxation-of-non-uk-domiciled-individuals

- Office for Budget Responsibility — Economic and Fiscal Outlook, October 2024. https://obr.uk/efo/economic-and-fiscal-outlook-october-2024/

- Cyprus Ministry of Finance — Tax Department. https://www.mof.gov.cy/mof/tax/taxdep.nsf

- Irish Revenue — Domicile guidance. https://www.revenue.ie/en/jobs-and-pensions/tax-residence/domicile.aspx

- Commissioner for Tax and Customs, Malta (CFR). https://cfr.gov.mt/

- AADE — Independent Authority for Public Revenue, Greece (Article 5A). https://www.aade.gr/en

- OECD Model Tax Convention on Income and on Capital (condensed version). https://www.oecd.org/tax/treaties/model-tax-convention-on-income-and-on-capital-condensed-version-20745419.htm

- EU Anti-Tax Avoidance Directive (ATAD). https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32016L1164

- OECD Common Reporting Standard. https://www.oecd.org/tax/automatic-exchange/common-reporting-standard/

- Internal Revenue Code §1, §61, §877A, §901, §911, §1297, §2001, §7701. https://www.law.cornell.edu/uscode/text/26