Long-term travel insurance is the one purchase nomads consistently get wrong. The market is dominated by three names — SafetyWing, World Nomads and WorldTrips — and a SERP full of affiliate reviews that rarely tell you which policy actually fits your passport, your tax residency or your medical history. This guide compares the main nomads travel insurance options for 2026, explains what each one covers and excludes, and flags the points where Americans, EU residents and everyone else need to read different fine print. It does not cover full international private medical insurance (IPMI) such as Cigna Global or Allianz Care — that is a separate product for a separate reader.

SafetyWing — Nomad insurance with recurring 364-day cookie

What nomads travel insurance actually is

Nomads travel insurance is a hybrid product that sits between standard holiday cover and full international health insurance. A standard travel policy assumes you have a home, you leave it for a defined trip, and you come back. A nomad policy assumes you do not — or that your "home" is wherever you happen to be sleeping this month.

In practice the category covers three different things, often sold as one:

- Emergency medical cover abroad — accidents, sudden illness, hospital admission, evacuation.

- Trip cover — cancellation, interruption, delays, lost baggage, theft of electronics.

- Liability and activity cover — third-party liability and (sometimes) adventure sports.

What it is not: it is not primary health insurance, it does not cover routine or preventive care, and it does not replace the residency-based public health cover you may be entitled to in your home country. If you need annual physicals, dental cleanings or ongoing chronic-condition management, you need IPMI, not a nomad travel policy.

Who this applies to — read your segment first

The right policy depends on where you are tax resident, where you are insured at home, and which country issued your passport. The product is global; the rules around it are not.

US persons — citizens and green-card holders

US persons can buy SafetyWing, World Nomads (US version, underwritten by Nationwide) and WorldTrips' Atlas Nomads. The catch is what these policies do not do at home. SafetyWing's Nomad Insurance provides limited cover for incidental trips back to the US — currently up to 30 days in any 90-day period, with a $250,000 lifetime cap on US treatment, per SafetyWing's plan description. It is not ACA-compliant and will not satisfy any state insurance mandate (California, Massachusetts, New Jersey, Rhode Island, DC and Vermont still impose them per Healthcare.gov).

US persons should also note: travel insurance has nothing to do with your tax filing obligations. You remain subject to citizenship-based taxation on worldwide income regardless of where you live or how you insure yourself (IRS Publication 54). FATCA and FBAR reporting on foreign financial accounts continue to apply.

EU freelancers and digital nomads

EU residents face an additional question: are you still covered by your home country's public system? If you remain tax resident in, say, Germany or France and your stay abroad is temporary, your European Health Insurance Card (EHIC) covers state-provided emergency care in other EU/EEA countries and Switzerland (European Commission, EHIC). It does not cover private hospitals, repatriation, or treatment outside the EU/EEA.

If you have broken tax residency — moved your centre of vital interests abroad, deregistered, lost your EHIC — you need genuine private cover. SafetyWing and World Nomads' European policies (underwritten by XL Insurance Company SE in Ireland) both work here. Be aware that several EU countries (Spain, Portugal, Netherlands) operate exit taxes on unrealised gains for departing tax residents; this is unrelated to insurance but often comes up in the same conversation. See the European Commission's exit taxation overview under the Anti-Tax Avoidance Directive.

Non-US, non-EU readers

This is the segment with the most flexibility. If you are tax resident in a territorial-tax jurisdiction (Panama, Paraguay, Georgia, Malaysia, UAE, Hong Kong) or have no current tax residency at all, you can buy any of the nomad policies without home-country complications. The decision is purely product-fit: subscription vs trip-based, medical-heavy vs trip-heavy.

You should still confirm that the policy is recognised by border officials in countries that require proof of insurance for entry (most Schengen states, parts of Latin America for digital nomad visas, and the UAE for some visa classes). SafetyWing and World Nomads both issue Schengen-compliant certificates on request.

How country of residence shapes the policy you can buy

Insurers sell different policy wordings to different markets because regulation requires it. Your country of residence at the moment of purchase determines:

- Which underwriter carries the risk — Nationwide for US-resident World Nomads buyers, XL Insurance Company SE for EU/UK residents, nib Travel Services for Australia and New Zealand.

- Which consumer-protection regime applies — the US has state insurance commissioners; the EU has the Insurance Distribution Directive (Directive 2016/97); the UK has the FCA.

- What "home" means in the contract — most policies define home as your country of residence and either exclude or limit cover there.

If you misstate your country of residence at purchase — a common shortcut for US persons trying to buy cheaper European versions — the policy is voidable. The insurer can refuse claims and refund the premium. Buy the version that matches the address on your tax filings or the country that issued your most recent residency permit.

Finding the right coverage for your next trip

Three product shapes dominate the nomads category in 2026. Each one suits a different traveller.

SafetyWing Nomad Insurance — the subscription

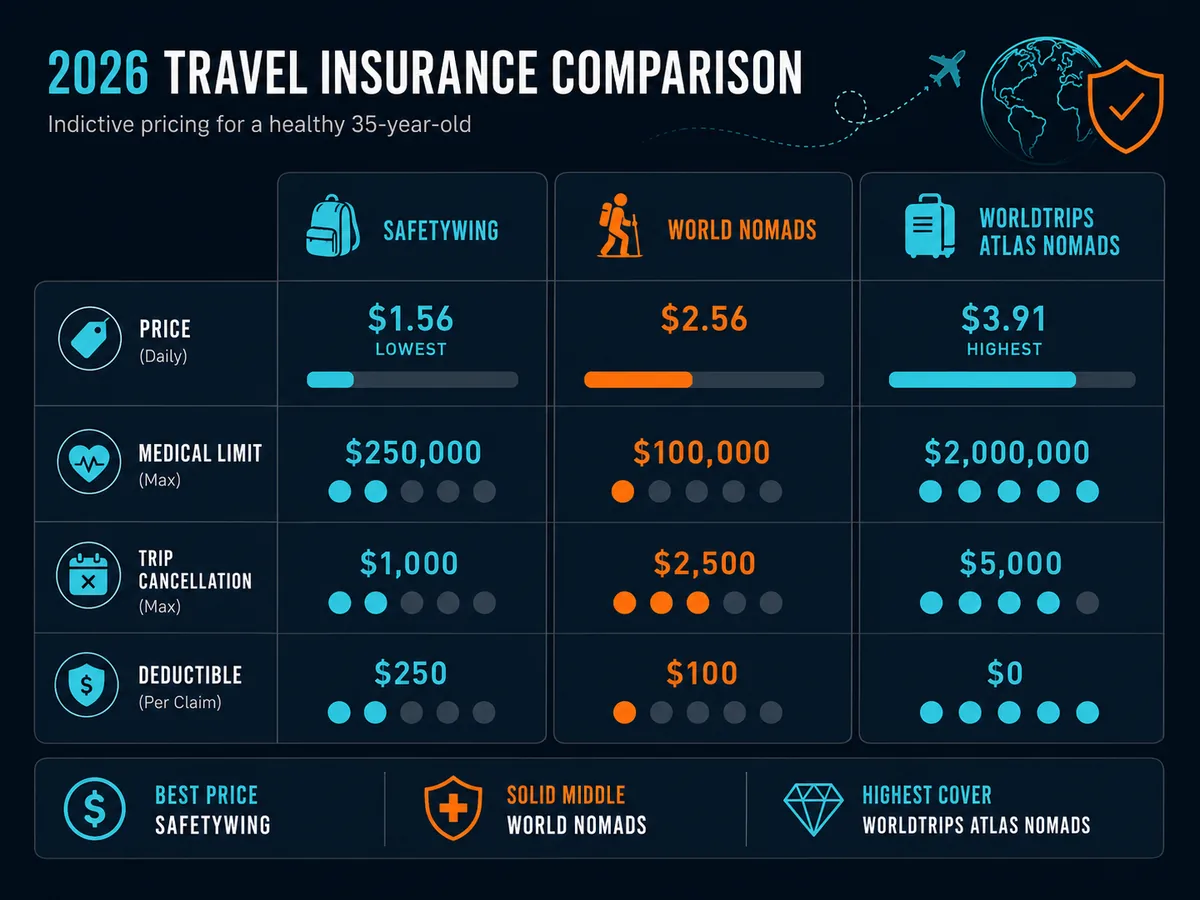

Sold as a 4-week auto-renewing subscription. Starts at $62.72 per 4 weeks for ages 10-39, with higher prices for older travellers, per SafetyWing's pricing page. Underwritten by Tokio Marine HCC.

Strengths: cheap for long stays, easy to start and stop, covers incidental home trips, includes COVID treatment as a regular illness.

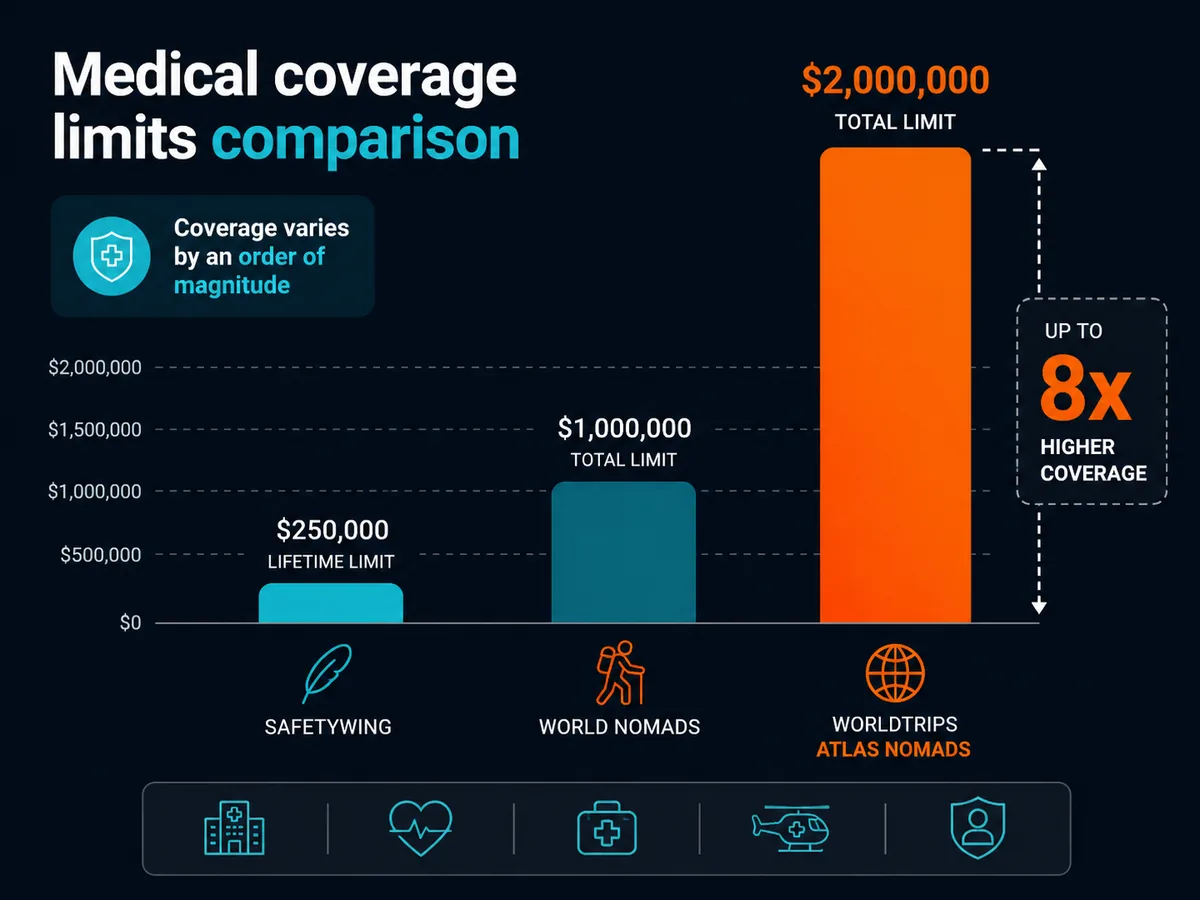

Weaknesses: low trip-cancellation cover ($5,000 limit on trip interruption only), low electronics cover, $250,000 lifetime medical limit, $250 deductible per certificate period. Not a replacement for full health insurance.

Best for: nomads with no fixed end date, low-value gear, and good baseline health.

World Nomads — the trip policy with adventure cover

Trip-based, with start and end dates. US version offers Standard and Explorer tiers, underwritten by Nationwide. Covers 200-plus adventure activities including trekking above 4,500m, scuba to recreational limits, and motorcycling with a valid licence (read the activity schedule carefully — limits differ by plan and country of residence).

Strengths: meaningful trip cancellation cover (up to $10,000 on Explorer), adventure-sports breadth, established claims infrastructure.

Weaknesses: more expensive per month than SafetyWing for long stays, must buy a new policy if you extend beyond 12 months, pre-existing conditions excluded without waiver.

Best for: travellers on trips of one to twelve months with non-refundable bookings and a willingness to do high-altitude or adventure activities.

WorldTrips Atlas Nomads — the higher-limit medical option

Atlas Nomads from WorldTrips is structured more like international medical cover, with higher medical maximums (up to $2 million depending on plan) and lower deductibles available. Underwritten by Lloyd's via WorldTrips' standard arrangement (verify on current WorldTrips' Atlas Nomads page).

Strengths: higher medical limits, optional add-ons, designed specifically for the work-abroad use case.

Weaknesses: less brand recognition for trip-cancellation claims, US-resident focus, fewer Schengen-friendly certificates by default.

Best for: longer-stay nomads who prioritise medical cover depth over trip protection.

Realistic costs and timelines

The table below shows representative 2026 prices for a healthy 35-year-old non-smoker with no pre-existing conditions, three months of cover, travelling outside the US.

| Product | Monthly cost (approx.) | Medical limit | Trip cancellation | Deductible / excess | Best fit |

|---|---|---|---|---|---|

| SafetyWing Nomad Insurance | $68 | $250,000 lifetime | None (interruption only, $5k) | $250 | Open-ended travel |

| World Nomads Standard (US) | $110-140 | $100,000 | $2,500 | $100 | Short trips, basic adventure |

| World Nomads Explorer (US) | $160-220 | $100,000 | $10,000 | $100 | Adventure + trip protection |

| WorldTrips Atlas Nomads | $130-200 | $1m-$2m | Up to $5,000 (varies) | $0-$2,500 selectable | Medical-heavy long stays |

Prices are indicative and change frequently. Always quote on the insurer's own site with your real age and itinerary. [source: TODO — capture live 2026 quotes from each provider for footnote]

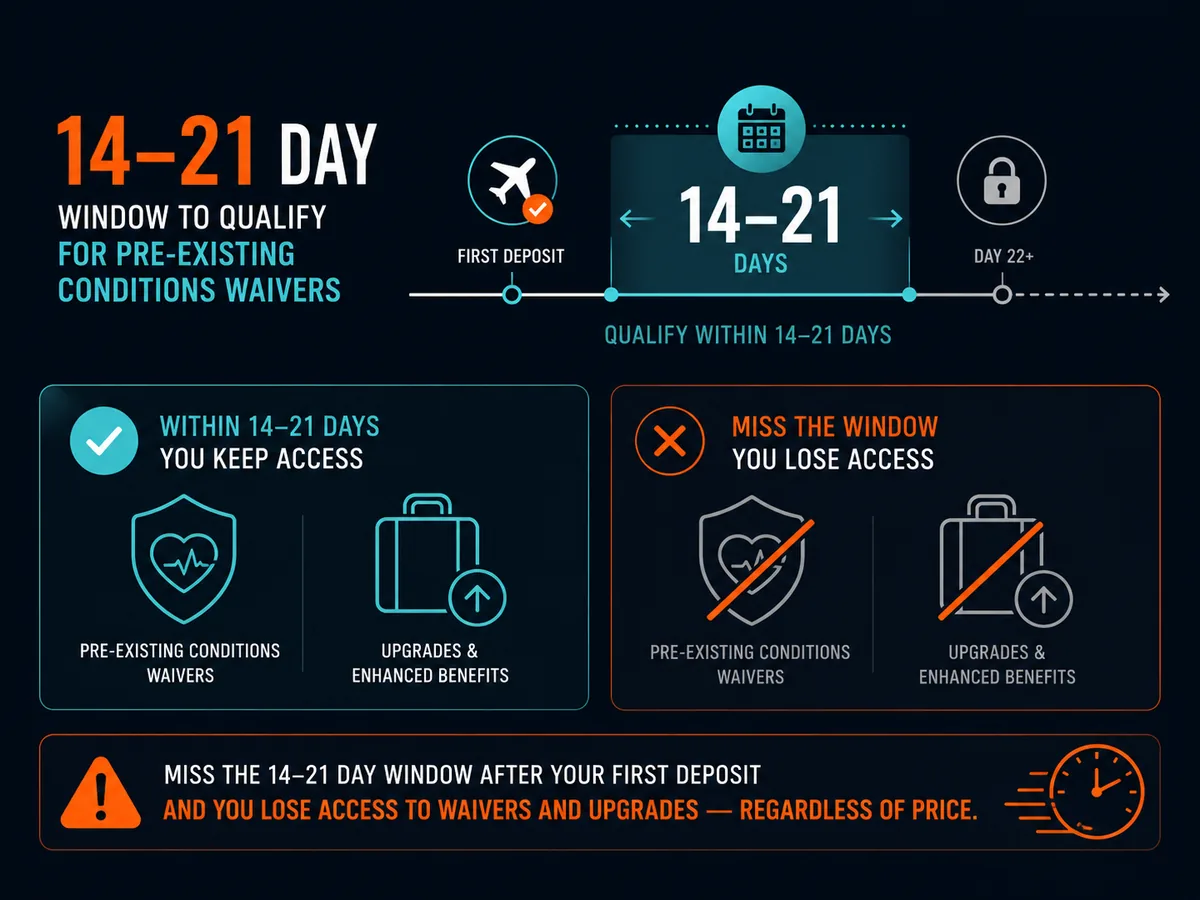

Timing matters more than price. Buy within 14 to 21 days of your first non-refundable booking to qualify for any pre-existing conditions waiver, cancel-for-any-reason upgrades or financial-default cover. Wait until departure week and you lose access to those features regardless of how much you pay.

Common mistakes and how to avoid them

Buying the wrong country version. Insurers price and underwrite by your country of residence. Buying the cheaper US version while resident in Germany — or vice versa — voids the contract at claim time. Use your real tax-residence address.

Treating nomad cover as health insurance. SafetyWing and World Nomads are emergency products. They do not pay for an annual GP visit, a planned dental crown or a routine blood panel. If you need that, you need IPMI or local private insurance in your host country.

Ignoring the pre-existing exclusion window. Most policies define pre-existing as any condition treated, medicated or advised on in the prior 90 to 180 days. A prescription you renewed three months ago counts. Disclose it; the underwriter decides.

Assuming adventure activities are included. Free climbing, scuba past 30m, motorcycle riding without a home-country licence, e-bikes above certain wattages — all commonly excluded. Read the activity schedule, not the marketing page.

Skipping the policy wording. The Product Disclosure Statement or Description of Coverage is 30-80 pages and contains everything that matters. Search it for "exclusion", "pre-existing", "high-risk", "war", "pandemic" and "home country" before you buy.

Letting it auto-renew without re-reading. SafetyWing's terms can change between renewals. Re-read the certificate annually.

Is World Nomads a good travel insurance

For the right reader, yes. It is a competent trip insurer with strong adventure-sports cover, a clean claims portal and underwriting from a financially solid carrier (Nationwide in the US). Independent reviews from NerdWallet and US News rate it well on flexibility and activity breadth, less well on medical limits and on customer service for disputed trip-cancellation claims.

It is not the right product if you want ongoing subscription cover with no end date (use SafetyWing), if you need primary health insurance abroad (use IPMI), or if your medical history includes recent active conditions you cannot get waived.

Will travel insurance cover kidney stones

It depends on whether the stone is a first occurrence or a recurrence. A first, sudden kidney stone attack during a covered trip is treated as acute illness and covered under emergency medical on SafetyWing, World Nomads and WorldTrips Atlas Nomads — subject to the deductible and policy limits.

A recurrence in someone with a history of kidney stones is a pre-existing condition. It is excluded unless you bought a policy with a pre-existing conditions waiver within the eligibility window (typically 14-21 days of initial trip deposit on US plans). Some EU policies allow declared pre-existing conditions for an extra premium; ask before you buy. Do not assume; do not omit. An undeclared history found in your medical records during claims review is the most common reason claims get denied.

Who is the most trusted travel insurance company

Trust splits by use case. For the nomad category specifically, the three most-cited names in independent reviews are SafetyWing (best for open-ended travel), World Nomads (best for trip-based adventure cover) and WorldTrips Atlas Nomads (best for higher medical limits). Trustpilot scores fluctuate; look at the underwriter's AM Best rating rather than the brand's review score. Nationwide (World Nomads US) holds an A+ rating; Tokio Marine HCC (SafetyWing's underwriter) holds A++. Both are financially strong.

If your reference for "most trusted" is legacy and balance sheet, the answer is the underwriter, not the brand. If your reference is community sentiment in nomad forums and Reddit, SafetyWing leads for monthly subscribers and World Nomads leads for short adventure trips.

When to consult a qualified professional

Buy insurance yourself; you do not need a broker for a standard nomad policy. Consult a professional in three situations:

- You have a complex medical history. A specialist insurance broker can place you with an underwriter willing to cover your conditions, often via full IPMI rather than nomad travel cover.

- You are changing tax residency. Speak to a tax adviser qualified in both your departure and destination jurisdictions before you move. Insurance is downstream of residency; get the residency right first.

- You are a US person planning long-term offshore life. Talk to a US-qualified cross-border tax adviser. Insurance does not change your filing obligations, but the structure of your work abroad — employee vs. contractor, sole proprietor vs. offshore company — interacts with the Foreign Earned Income Exclusion, the foreign tax credit and GILTI rules (IRC §951A) in ways that matter. No insurer can advise on this.

Soveraine is editorial, not regulated financial or legal advice. See our editorial policy, disclaimer and affiliate disclosure for how we work and how we are funded.

A note on the recommendations above

Soveraine has affiliate relationships with SafetyWing and World Nomads. We do not have one with WorldTrips at the time of writing — it is included because it is the best higher-medical-limit option in the category, not because it pays us. If you find a materially better alternative for your situation, buy it. Our rankings reflect editorial assessment, not commission rates.

Ready to act on this?

SafetyWing — Nomad insurance with recurring 364-day cookie. Soveraine readers go to the front of the line through our partner link, and you fund independent editorial in the process.

FAQ

Is World Nomads a good travel insurance

World Nomads is a credible trip-and-adventure insurer underwritten in the US by Nationwide and in Europe by XL Insurance Company SE. It works well for travellers on defined trips of up to a year who want adventure-sports cover and trip cancellation. It is not designed as ongoing health insurance for someone who has no fixed home base. Reviews on Trustpilot and consumer sites are mixed on claims handling — fast for straightforward medical claims, slower for complex trip-cancellation disputes. Read the Product Disclosure Statement for your country of residence before buying; coverage and limits differ materially between the US, UK, EU and Australian versions.

Will travel insurance cover kidney stones

Usually yes, if the kidney stone is a new, sudden onset during the trip and you have no prior history. Emergency treatment for a first-time attack falls under acute medical cover on SafetyWing, World Nomads and WorldTrips. If you have had kidney stones before, it counts as a pre-existing condition and is excluded unless you bought a policy with a pre-existing conditions waiver — typically only available if you insure within 14 to 21 days of your first trip deposit and insure the full trip cost. Always declare prior episodes; an undeclared history is the fastest way to have a claim denied.

Who is the most trusted travel insurance company

There is no single answer, because trust depends on what you need. For defined-trip cover with adventure activities, World Nomads has the longest brand history. For ongoing nomad health cover billed monthly, SafetyWing has the strongest reputation among long-term travellers. For higher medical limits and US-style health benefits abroad, WorldTrips' Atlas Nomads plan is rated well by independent reviewers including NerdWallet and US News. Check the underwriter rather than the brand: AM Best financial-strength ratings on the actual insurance carrier matter more than the marketing front-end.

What does World Nomads travel insurance cover

World Nomads covers overseas emergency medical and dental, emergency evacuation, trip cancellation and interruption, lost or stolen baggage, and 200-plus adventure activities depending on plan tier. The US Standard and Explorer plans are underwritten by Nationwide; the Explorer plan adds rental car damage, missed connections and higher limits. It does not cover routine check-ups, pregnancy beyond emergency complications, or pre-existing conditions unless a waiver applies. Cover ends when you return home or when your policy expires, whichever is first. The full benefit schedule is in the Description of Coverage on worldnomads.com — read it before you assume anything is included.

Does World Nomads insurance cover pre-existing conditions

Only