Monaco is the most famous 0% personal income tax jurisdiction in Europe, and one of the most misrepresented. The headline rate is real — there has been no personal income tax on Monégasque residents since the Sovereign Ordinance of 1869. What the headline omits is that the route in costs upward of €1 million in year one before the keys turn, that the principality's most-cited residency country (France) is contractually excluded from the tax benefit, and that the €500,000 bank deposit so often quoted is a bank policy, not a statute. This guide walks through what Monaco actually delivers, who it works for, what it costs, and the traps that catch readers who shop on the headline alone. It is written for three audiences in parallel: US persons, EU residents (especially French nationals), and readers based in the rest of the world.

Henley & Partners — Largest RBI/CBI advisory firm in the world

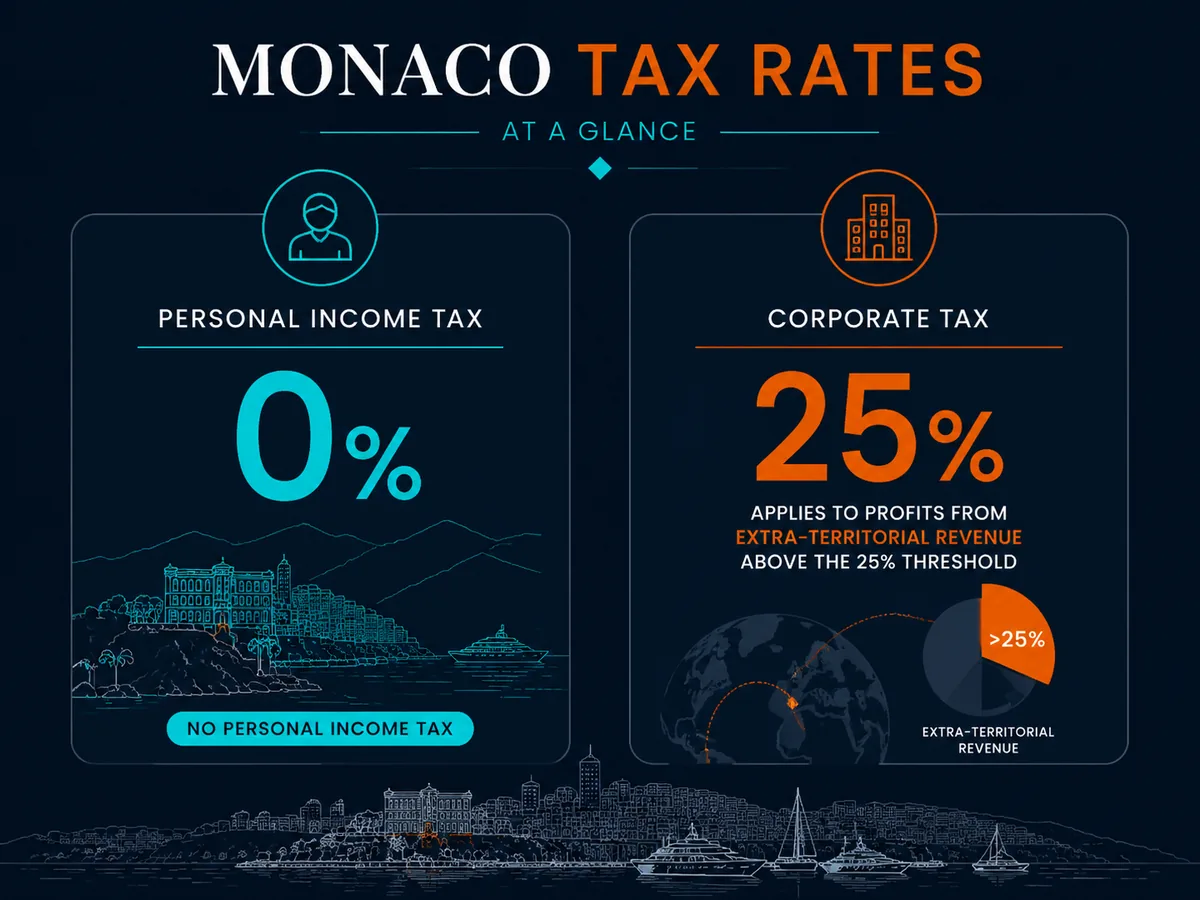

What Monaco's tax regime actually is

Monaco's personal tax regime is older than most of its competitors' constitutions. The Sovereign Ordinance of 1869, issued by Prince Charles III, abolished personal income tax on Monégasque residents. The principle has held without interruption ever since and is summarised on the official portal of the Monégasque government's Direction des Services Fiscaux.

For an individual resident in Monaco, the rate card is short:

- Personal income tax: 0% on wages, business income and investment income, for all nationalities except French citizens covered by the 1963 convention.

- Capital gains tax: 0% on share disposals, securities and real estate (subject to standard VAT rules on commercial property).

- Wealth tax: none.

- Inheritance and gift tax: 0% for transfers in the direct line — between spouses, from parents to children, and to grandchildren. Rates rise for collateral and unrelated heirs (8% siblings, 10% uncles/aunts and nieces/nephews, 13% other relatives, 16% unrelated parties) under Law No. 580 of 29 July 1953 and subsequent amendments.

- Annual property tax on residences: none.

- Council tax / habitation tax: none.

- VAT: 20% under a customs union agreement with France, mirroring the French rate.

Companies are a different story. Under the Franco-Monégasque Tax Convention of 18 May 1963 — which still governs much of cross-border taxation between the two states — Monégasque companies that earn more than 25% of their revenue from outside Monaco are subject to a 25% corporate tax (Impôt sur les Bénéfices, ISB) administered by the Direction des Services Fiscaux. Companies earning less than 25% of revenue extra-territorially are exempt. Industrial, commercial and self-employed professional activities also fall within ISB scope under the 1963 convention as amended in 2018 (Government of Monaco: Business taxation).

In plain terms: Monaco is 0% for the individual; 25% for the international company; and 20% for everyone at the checkout. The headline applies cleanly to a wealthy individual living on investment income or a salary from a Monaco-resident employer, and applies poorly to a remote founder running a global SaaS through a Monaco entity.

The French citizen exception

The single most important sentence in any honest article about Monaco tax residency: moving to Monaco does not reduce French tax for French nationals.

The rule is set in Article 7 of the Franco-Monégasque Tax Convention of 18 May 1963. French nationals who transferred their residence to Monaco on or after 13 October 1962 remain subject to French income tax on their worldwide income, with their tax assessed under French rules as if they were resident in France. The same applies to French nationals who were resident in Monaco on 13 October 1962 but cannot prove five years of continuous residence in Monaco prior to that date.

Two narrow exceptions survive:

- French nationals born in Monaco before 13 October 1962 who were resident in Monaco on that date and can prove the five-year residence requirement. This is a small, ageing cohort.

- Their direct descendants by inheritance in some readings, although the French tax administration applies this narrowly.

The convention was renegotiated and updated in 2001 and most recently amended in 2014 (in force 2016), tightening exchange of information and substance verification (French Senate: bilateral convention texts). Successive reforms have closed the gaps that allowed earlier carve-outs.

The practical result. A French citizen who moves from Paris to Monaco and obtains a Monégasque carte de séjour pays:

- French income tax on worldwide income at the standard French progressive scale up to 45%, plus the exceptional contribution of 3% to 4% on high incomes.

- French social charges where applicable.

- No Monégasque income tax (which is moot because Monaco does not levy any on individuals).

For a French CEO earning €1 million, the move saves nothing on income tax. It may still serve lifestyle, succession or family reasons — but it is not a tax move. Any agent who pitches Monaco residency to a French national as a tax optimisation is selling a product the law does not deliver.

Who this applies to — read this first

Monaco's relevance changes more sharply by nationality than almost any other residency. Read the section for your passport.

US persons

US citizens and green-card holders are taxed on worldwide income regardless of where they live, under IRC §1 and IRC §61. Monaco's 0% rate does not pause that. A US person resident in Monaco still files Form 1040, still files FBAR (FinCEN 114) on Monégasque bank accounts above $10,000 in aggregate (FinCEN), and still files Form 8938 under FATCA above the relevant thresholds (IRS Form 8938).

The available reliefs are the foreign earned income exclusion of $130,000 for tax year 2025 under IRC §911 (IRS Rev. Proc. 2024-40) plus the foreign housing exclusion. These are real but capped. The bigger problem for high-income Americans is that Monaco's 0% rate generates no foreign tax credit — there is no Monégasque tax paid that can be credited against US tax on amounts above the FEIE cap, on passive income, or on capital gains. A US founder selling a company while resident in Monaco pays full US capital gains tax with no offset.

Monaco is therefore most useful to a US person who is at or below the FEIE cap on earned income and who is moving primarily for lifestyle. For high earners, it offers no marginal benefit over a higher-tax European base unless and until they renounce citizenship under IRC §877A. Engage a specialist — Bright!Tax, Greenback or MyExpatTaxes — before signing a Monégasque lease.

EU residents — especially French nationals

For French citizens, see the section above. Monaco does not deliver income tax savings.

For other EU citizens — Italian, German, Spanish, Belgian, Dutch — Monaco can work if the move is clean. The break with the home tax residency must be genuine under that state's domestic rules and under the OECD Model Tax Convention Article 4 tiebreaker. Spain applies an exit tax on unrealised capital gains for departing taxpayers above thresholds under Article 95 bis of the Personal Income Tax Law. The Netherlands imposes a conserverende aanslag on substantial shareholdings. Germany applies the Außensteuergesetz §6 exit charge on shareholders of 1% or more in domestic corporations. Italy's "trasferimento all'estero" rules tax latent gains on qualifying participations.

Beyond exit tax, EU exit substance is scrutinised. Holding a Monégasque carte de séjour while leaving a permanent home, family and economic interests in Milan or Munich invites a tax-residency redetermination under the treaty tiebreaker — and Italy and Germany both run active programmes targeting "false Monégasques."

Non-US, non-EU readers

This is the cleanest fit. UK nationals — especially after the abolition of the non-domicile remittance basis in April 2025 under the Finance Act 2025 reforms — increasingly look at Monaco as a successor base, because the new UK Foreign Income and Gains regime offers only four years of relief before worldwide UK tax kicks in. Middle Eastern wealth uses Monaco for European access combined with Schengen mobility. Asian, Latin American and African HNW families use it for succession planning given the 0% inheritance tax in the direct line.

For this segment, Monaco delivers as advertised — provided the substance is built, the home country residency is cleanly severed, and the capital is in place.

The qualification — what you actually need

There is no single statute that codifies a "Monaco residency programme" in the way Portugal's golden visa or the UAE's free zones do. Residency is granted on a case-by-case basis by the Direction de la Sûreté Publique, Service des Étrangers, under Sovereign Ordinance No. 3.153 of 19 March 1964 on the conditions of entry and stay of foreigners. The published procedure is set out by the Monégasque Service Public for foreigners settling in Monaco.

Four conditions, in practice:

1. Accommodation in Monaco. The applicant must provide proof of a place to live in the principality — either a residential lease of at least 12 months in their own name, ownership of a residential property, or designated accommodation by a spouse, parent, child, or sibling who is already a Monaco resident. Hotel rooms, short-term rentals and "virtual offices" do not qualify. The lease must be registered with the Service du Cadastre.

2. Sufficient financial resources. The applicant must demonstrate ability to live in Monaco without becoming a public charge. The accepted forms of proof are:

- a bank deposit at a Monaco-licensed bank, with the widely-applied de facto minimum of €500,000 (not codified in statute, but referenced consistently by the Monégasque banking association and applied by CFM Indosuez, CMB Monaco, Andbank Monaco, Banque Havilland and other licensed institutions);

- proof of professional income at sufficient level (employment contract with a Monaco-resident employer, or business ownership);

- a combination of pension income, investment income and assets that the bank attests cover Monégasque living costs.

The €500,000 figure functions as the practical floor. Some banks set higher thresholds — €1 million is common at the wealth-management tier — and the deposit is returnable: it is the applicant's own money held in their own account, not a fee.

3. Clean criminal record. Apostilled police clearance certificates from every country the applicant has resided in for more than six months over the past five years. For US citizens this means an FBI Identity History Summary, apostilled by the US Department of State. For UK citizens, an ACRO Police Certificate. Original documents in French translation (sworn).

4. Health insurance. Private health insurance cover is mandatory for the duration of the carte de séjour. Monaco's CCSS social security applies only to those employed by a Monaco-registered employer. Private cover suitable for residency applications typically runs €3,000 to €10,000 per year depending on age and coverage level — Cigna Global and Allianz Care issue compliant policies.

The application process

Six steps, in order. Skipping or reversing any of them adds months.

Step 1 — Secure accommodation. A 12-month residential lease, signed and registered with the Service du Cadastre. Available rental stock is limited, agents charge a fee equivalent to one month's rent, and refundable deposits run three months. Some landlords require proof of funds before showing units.

Step 2 — Open a Monaco bank account and transfer the deposit. This is the longest single step, typically two to four months. Monégasque banks operate full KYC under Law No. 1.362 of 3 August 2009 on combating money laundering, as amended. The bank conducts source-of-funds verification on every euro of the deposit. Cryptocurrency-derived funds, opaque trust structures and complex corporate flows extend the process substantially. La Vida and Henley & Partners maintain introductions at the major banks; using an introducer is the norm.

Step 3 — Assemble the documentation set. Passport, birth certificate (apostilled, translated), marriage certificate where applicable, apostilled police certificates from the past five years' residences, bank attestation of the deposit, residential lease, health insurance certificate, CV, two passport photographs, and the application form.

Step 4 — Submit the application. Filing is in person at the Direction de la Sûreté Publique, Service des Étrangers, accompanied by payment of the residence permit fee. The file is reviewed for completeness and then forwarded for security and police checks.

Step 5 — Interview. The applicant attends a personal interview at the Service des Étrangers. The interview covers residency intent, source of income, ties to Monaco, family situation, and travel patterns. It is conducted in French (translator permitted). The applicant should expect to be asked why Monaco and to demonstrate a coherent answer.

Step 6 — Carte de séjour issuance. On approval, the first card issued is a carte de séjour temporaire, valid for one year. It is renewable annually for the first three years. After three years of continuous residence, it converts to a carte de séjour ordinaire, valid for three years and renewable. After ten years of continuous residence as a Monaco resident, the holder qualifies for a carte de séjour privilégiée, valid for ten years and renewable. Naturalisation is theoretically available after ten years post-majority residence under Law No. 1.155 of 18 December 1992 but is granted at the discretion of the Sovereign Prince and rarely approved.

End-to-end timeline from a clean start: six to twelve months.

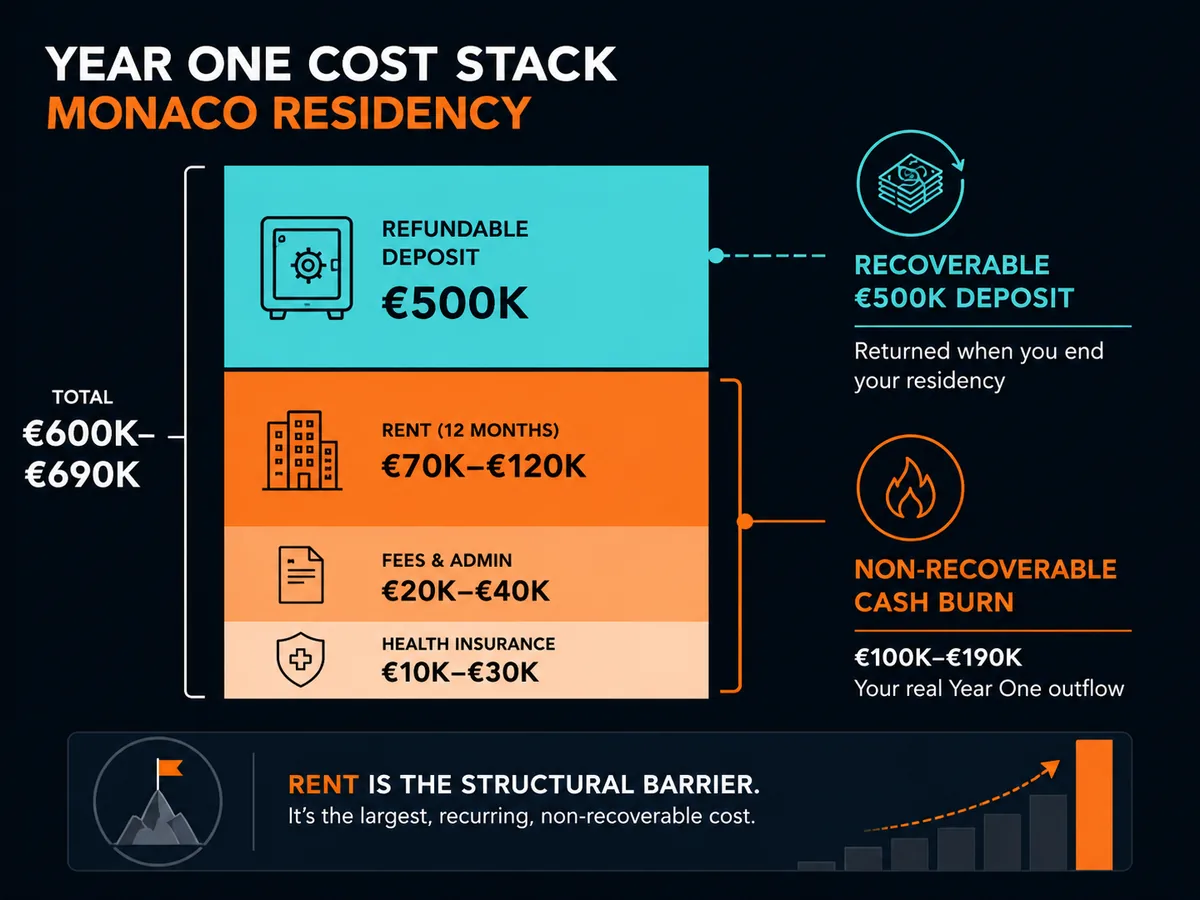

Real costs — year one breakdown

Monaco's marketing emphasises 0% tax. Honest accounting emphasises the cost of acquisition.

| Line item | Year one cost (EUR) | Notes |

|---|---|---|

| Rent — 1-bed apartment | €60,000 – €100,000 | €5–8k/month, agency fee +1 month, deposit +3 months refundable |

| Refundable bank deposit | €500,000+ | Applicant's own money in own account; returnable |

| Legal and immigration fees | €15,000 – €30,000 | Local attorney or specialist firm, including bank introductions |

| Apostilles, translations, certificates | €3,000 – €5,000 | Police certificates, birth/marriage certificates, sworn translations |

| Residency permit fees | €200 – €500 | Per the Direction de la Sûreté Publique published fee schedule |

| Private health insurance | €3,000 – €10,000 | Age- and coverage-dependent; mandatory |

| Furniture and setup | €20,000 – €40,000 | Long-stay apartments typically unfurnished in Monaco |

| Bank account opening (non-deposit) | €1,000 – €3,000 | KYC processing, signature certifications |

| Tax residency certificate (issued by Direction des Services Fiscaux) | €0 – €500 | Issued on request once residency is in place |

| Cash burn excluding refundable deposit | €100,000 – €190,000 | First-year out-of-pocket cost |

| Total committed in year one | €600,000 – €690,000 | Including the €500k deposit |

Sources: Knight Frank Wealth Report 2025 (Monaco prime residential rent index); Direction des Services Fiscaux; local practitioner fee surveys.

Rent is the largest non-refundable line and the structural barrier. Monaco's residential market has ranked first in the world by price per square metre in Knight Frank's Prime International Residential Index for over a decade, with average prime sale prices above €52,000 per square metre and prime rents averaging €5,500 per square metre per year. A modest two-bedroom apartment listing at €12,000 per month is normal, not high.

For a couple looking at family-suitable accommodation (two-bedroom, secondary school nearby), realistic year-one rent rises to €120,000–€200,000. The €1 million headline cost cited in the opening paragraph is the conservative estimate for a family setup that meets standard Monégasque residency expectations.

Comparison table

How Monaco stacks up against the other established European-adjacent residencies for HNW individuals.

| Jurisdiction | Personal income tax | Minimum entry cost | Deposit required | Days/yr required | EU/Schengen access | Best for |

|---|---|---|---|---|---|---|

| Monaco | 0% (except French nationals) | €600k+ year one (€500k refundable) | €500,000 at Monaco bank | 183 in practice | Schengen via French border | UHNW seeking 0% with European base |

| UAE (Dubai) | 0% | USD 5k–12k + free-zone licence | None | 90 with home/business, 183 otherwise | None | Founders wanting banking + 0% personal |

| Andorra | 10% above €40k | €600k investment (property/securities) | €50,000 (refundable with AFA) | 183 | None (Schengen via France/Spain land border only) | Mid-tier earners seeking Pyrenean lifestyle |

| Switzerland (lump-sum) | Negotiated; CHF 250k–1M+ annual | CHF 250k+ annual lump-sum tax | None statutory | 183 | Schengen | Wealthy individuals wanting Swiss base and treaty network |

| Cyprus (non-dom) | 0% on dividends/interest for 17 years | EUR 300k investment for residency, lower for non-dom | None | 60 (special regime) | EU member | Mid-cap entrepreneurs needing EU passport route |

Sources: Government of Monaco taxes, UAE Federal Tax Authority, Andorra Govern: residency, Swiss Federal Tax Administration on lump-sum taxation, Cyprus Tax Department.

Monaco's advantage is the combination of 0% personal income tax, full Schengen mobility through the French border, the strength of Monégasque private banks, and a small physical footprint that is easy to evidence as a real home. The price for those advantages is the highest cost-of-entry in the table.

The traps

The French citizen exception. Already covered above. It is worth flagging twice because it disqualifies the largest single nationality of would-be applicants. If you hold a French passport and are not part of the pre-1957 carve-out, Monaco does not solve your French tax bill.

The €500,000 is a bank policy, not a statute. Many readers expect the figure to be a published government threshold. It is not. It is the de facto floor applied by the Monégasque banks under their own KYC and substance policies, coordinated through the Monaco Association for Financial Activities (AMAF). Banks can and do set higher thresholds, and they can reject applicants whose source of funds is not robust regardless of the amount. There is no formal appeal.

The 1963 Convention applies more broadly than people think. Beyond the French citizen rule, the convention also governs corporate taxation, inheritance between Monaco residents and French residents, and reciprocal exchange of information. Amendments in 2010 (in force 2011) and 2014 (in force 2016) have progressively tightened substance and reporting requirements. A Monaco-based company doing more than 25% of revenue with French clients can find itself subject to French corporate tax in addition to or in place of Monégasque ISB (French Ministry of Finance: international tax conventions).

The six-month rule and substance audits. Holding the carte de séjour is not the same as being a tax resident. The Direction de la Sûreté Publique expects physical presence in Monaco for at least six months per year, and Direction des Services Fiscaux will not issue a tax residency certificate without it. Renewal interviews probe travel patterns, utility consumption, mobile phone usage and bank activity. The penalty for being detected as a "paper Monégasque" is non-renewal of the card.

OECD CRS reporting. Monaco has participated in the Common Reporting Standard since 2017 and exchanges financial account information annually with over 100 partner jurisdictions, including every EU member state, the UK, Australia and most of the OECD. A French, German or Italian tax resident with a Monégasque account is reported to their home tax authority within the following year. The US does not participate in CRS but operates FATCA through an intergovernmental agreement with Monaco signed in 2016.

Monaco's housing market is the real barrier. Rent ranks first globally in Knight Frank's index. New residential development is constrained by physical territory of 2.08 km² and is dominated by ultra-prime towers like Tour Odéon and Mareterra. Many would-be residents qualify financially but cannot secure suitable accommodation because supply is fully absorbed by existing residents and the new-build pipeline is reserved years in advance. Working with an established broker — Astons, Knight Frank Monaco, Savills Monaco — is effectively required.

Naturalisation is not on offer. Monégasque citizenship after ten years of residence is theoretically possible but in practice extremely rare. Long-term residents typically remain on the carte de séjour privilégiée indefinitely. The principality also discourages dual citizenship for naturalised Monégasques, which deters most candidates who would otherwise qualify.

The 25% corporate tax catches international businesses. A founder relocating a SaaS or digital services business to Monaco expecting 0% on company profits is reading the wrong rate. Where more than 25% of revenue is sourced outside Monaco, ISB at 25% applies. The clean structure for international business is usually to keep the operating company offshore (UAE, Singapore, Hong Kong) and use Monaco as personal residence — but the substance question then becomes whether the offshore company can be argued to be managed from Monaco. This is exactly the territory where Henley & Partners, Latitude and a cross-border tax counsel earn their fees.

Final CTA## FAQ

Is Monaco really a 0% income tax country?

Yes, for personal income tax on individuals who are not French nationals. Since the Sovereign Ordinance of 1869, Monaco has levied no personal income tax on residents — no tax on salaries, no tax on investment income, no tax on capital gains. There is also no wealth tax and no inheritance tax for direct heirs (spouses, parents, children). Companies generating more than 25% of revenue outside Monaco pay a 25% corporate tax under the 1963 Franco-Monégasque tax convention. Property taxes are minimal and there is no annual property tax on residential homes. The exception that swallows the rule for one nationality: French citizens who became resident in Monaco after 1957 remain liable for French income tax.

How much money do you need to become a Monaco resident?

The widely cited bank deposit threshold is €500,000 at a Monaco-licensed bank, although the figure is not codified in statute — it is the de facto minimum applied by the major Monégasque banks (CFM Indosuez, CMB Monaco, Banque Havilland, Andbank Monaco) under their KYC and onboarding policies. On top of the deposit, an applicant must prove accommodation in Monaco, which in practice means a residential lease of at least 12 months or property ownership. A small one-bedroom apartment rents for €5,000 to €8,000 per month. Year-one cash burn excluding the returnable deposit is typically €100,000 to €150,000.

Why do French citizens still pay French tax in Monaco?

Under Article 7 of the Franco-Monégasque Tax Convention of 18 May 1963, French nationals who established residence in Monaco on or after 13 October 1962 remain subject to French income tax on their worldwide income as if they were French residents. The carve-out applies to French citizens born in Monaco before that date and their descendants, who escape French taxation. The convention was renegotiated in 2010 with effect from 2011, tightening the definition of residence and reporting. For an ordinary French passport holder, moving to Monaco delivers no income tax saving — France continues to tax them.

Do US citizens benefit from Monaco's 0% tax?

No. The United States taxes its citizens and lawful permanent residents on worldwide income regardless of where they live, under IRC §1 and §61. A US person resident in Monaco still files Form 1040 every year, still files FBAR (FinCEN 114) on Monégasque bank accounts above $10,000 in aggregate, and still files Form 8938 under FATCA where the threshold is met. The foreign earned income exclusion of $130,000 for tax year 2025 is available under §911 if the bona fide residence or physical presence test is met, but Monaco's 0% personal rate provides no foreign tax credit to offset US tax above the cap, because there is no Monégasque tax paid to credit.

How long does it take to get Monaco residency?

From a clean start to the first carte de séjour, plan on six to twelve months. Securing a long-term lease takes one to three months, opening a Monaco bank account and transferring the deposit takes two to four months of KYC, and the residency application itself with the Direction de la Sûreté Publique takes three to six months from filing to issuance. The first card issued is a carte de séjour temporaire, valid for one year and renewable annually for three years. After three years it converts to a carte de séjour ordinaire valid for three years, renewable. After ten years of continuous residence the holder qualifies for a carte de séjour privilégiée valid for ten years.

Do I have to live in Monaco full time?

To maintain residency status the Direction de la Sûreté Publique expects genuine residence — in practice, physical presence in Monaco for at least six months per calendar year, plus continued occupation of a Monégasque address. Random checks include utility consumption, mobile phone usage in Monaco, and banking activity. To obtain a Monégasque tax residency certificate for use under double tax treaties, the bar is higher and the principality applies an OECD-style centre of vital interests test. Holding the card without living there is the most common reason for non-renewal.

Is Monaco still on any tax haven blacklist?

Monaco was removed from the OECD list of uncooperative tax havens in 2009 after committing to information exchange standards, and is not currently on the EU list of non-cooperative jurisdictions for tax purposes. Monaco participates in the Common Reporting Standard and exchanges financial account information annually with over 100 partner jurisdictions, including all EU member states. This means a German, Spanish or Italian tax resident who opens a Monaco account is reported to their home tax authority within the following year. Privacy is not a benefit of Monégasque banking in 2026.

Can I get Monégasque citizenship after residency?

Naturalisation in Monaco is rare and entirely discretionary by the Sovereign Prince. The statutory minimum is ten years of continuous residence after the age of 18 under Law No. 1.155 of 18 December 1992, but in practice applications are rarely approved and the principality grants only a small number of naturalisations per year. Most long-term residents remain on the carte de séjour privilégiée indefinitely. The country also does not generally permit dual citizenship for naturalised Monégasques, which deters many applicants who would otherwise qualify.

Ready to act on this?

Henley & Partners — Largest RBI/CBI advisory firm in the world. Soveraine readers go to the front of the line through our partner link, and you fund independent editorial in the process.

Sources

- Government of Monaco — Direction des Services Fiscaux, taxes overview. https://en.gouv.mc/Policy-Practice/The-Economy/Taxes

- Government of Monaco — Business taxation. https://en.gouv.mc/Policy-Practice/The-Economy/Taxes/Business-Taxation

- Service Public Particuliers Monaco — Foreigners settling in Monaco. https://en.service-public-particuliers.gouv.mc/Foreigners/Settling-in-Monaco

- Franco-Monégasque Tax Convention of 18 May 1963 (as amended). https://www.impots.gouv.fr/international-particulier/conventions-internationales

- Sovereign Ordinance No. 3.153 of 19 March 1964 — Conditions of entry and stay of foreigners. https://journaldemonaco.gouv.mc/

- Law No. 1.155 of 18 December 1992 on Monégasque nationality. https://journaldemonaco.gouv.mc/

- Law No. 1.362 of 3 August 2009 on combating money laundering and terrorist financing. https://www.amaf.mc/

- Monaco Association for Financial Activities (AMAF). https://www.amaf.mc/

- Knight Frank Wealth Report 2025 — Prime International Residential Index. https://www.knightfrank.com/wealthreport

- OECD Common Reporting Standard. https://www.oecd.org/tax/automatic-exchange/

- OECD Model Tax Convention on Income and on Capital. https://www.oecd.org/tax/treaties/model-tax-convention-on-income-and-on-capital-condensed-version-20745419.htm

- US Treasury — FATCA Intergovernmental Agreement with Monaco (2016). https://home.treasury.gov/policy-issues/tax-policy/foreign-account-tax-compliance-act

- IRS Rev. Proc. 2024-40 — Annual inflation adjustments. https://www.irs.gov/pub/irs-drop/rp-24-40.pdf

- IRC §911 — Citizens or residents of the United States living abroad. https://www.law.cornell.edu/uscode/text/26/911

- IRC §877A — Tax responsibilities of expatriation. https://www.law.cornell.edu/uscode/text/26/877A

- FinCEN — Report of Foreign Bank and Financial Accounts (FBAR). https://www.fincen.gov/report-foreign-bank-and-financial-accounts

- IRS Form 8938 — Statement of Specified Foreign Financial Assets. https://www.irs.gov/forms-pubs/about-form-8938

- UK Government — Changes to the taxation of non-UK domiciled individuals (Finance Act 2025). https://www.gov.uk/government/publications/changes-to-the-taxation-of-non-uk-domiciled-individuals

- EU Council — EU list of non-cooperative jurisdictions for tax purposes. https://www.consilium.europa.eu/en/policies/eu-list-of-non-cooperative-jurisdictions/

- French Senate — Bilateral conventions. https://www.senat.fr/