Mexico hosts roughly 1.6 million resident Americans — the largest concentration of US citizens living abroad of any country in the world, per US State Department consular registration data. The legal scaffolding under which most of them live is the Residente Temporal visa, a one- to four-year residence permit issued by Mexican consulates abroad under the 2011 Ley de Migración. It is the standard non-pensioner route into Mexico, and since 2023 it has quietly become harder to obtain at several US consulates — the statutory floor has not moved, but consulate-level discretion on income multipliers has tightened in San Diego, Houston, Los Angeles and Washington in particular.

Bright!Tax — US expat tax filings (FBAR + FATCA + FEIE specialists)

This article covers what the Residente Temporal actually requires, the income thresholds the consulates are applying in 2026, the application process step-by-step, the Mexican tax-residency rules under LISR Article 9 that operate independently of immigration status, and the US-side filing reality that follows every American to Mexico. It is written for prospective applicants doing diligence before they commit — not for people already in the consulate queue. It does not cover the Visa de Visitante por Razones Humanitarias or work-permit applications routed through Mexican employer sponsorship, which are separate procedures with different evidentiary thresholds.

What Residente Temporal actually is

The Residente Temporal is a national long-stay visa created under Articles 52(VII) and 54 of the Ley de Migración, the statutory framework Mexico enacted in May 2011 to consolidate its previous patchwork of FM2/FM3 categories. It permits a foreign national over 18 to enter and reside in Mexico for an initial one-year period, renewable for one, two, or three additional years up to a total of four years. After the four-year cap — or after two years if the holder is married to a Mexican citizen or has a Mexican child — the status converts (on application) to Residente Permanente.

The visa is granted on one of three legal bases:

- Economic solvency (solvencia económica) — proof of passive or active income above the consulate's threshold, or of savings above the alternative threshold. This is the route most non-Mexican-family applicants use.

- Family unity — a Mexican spouse, parent or child anchors the application. Income thresholds are typically waived or reduced.

- Employer sponsorship — a Mexican company with INM registration sponsors the applicant for a specific role, with a work permit (permiso para trabajar) bundled in.

The visa is issued as a 180-day single-entry stamp in the passport at the consulate. After entering Mexico, the holder has 30 calendar days to attend the local INM office and complete the canje — the exchange of the consular sticker for a physical Residente Temporal card (TRT). Miss the 30-day window and the entire process restarts at the consulate.

Work authorisation is not automatic on Residente Temporal. An applicant who wants to work legally in Mexico — for a Mexican employer, as a freelancer issuing Mexican invoices, or as a self-employed professional — must request the permiso para trabajar either at the canje appointment or via a separate INM filing thereafter. Income from foreign-source remote work paid into foreign accounts generally does not require the permit, but the line is fact-sensitive and worth confirming with a Mexican immigration lawyer in marginal cases.

Who this applies to — read this first

The visa itself is open to any non-Mexican over 18. The downstream tax and reporting consequences depend almost entirely on the passport in your pocket. Read the segment that matches your situation before doing anything else.

US persons

This is the primary audience for this article. Mexico is the largest single destination for US persons living abroad, and the proximity, US-Mexico Totalisation Agreement (in force since 1 October 2024), and treaty network make the move administratively cleaner than most. None of that ends your US tax obligations. Citizenship-based taxation under IRC §1 follows the passport — you continue to file a Form 1040 every year, file FBAR on any Mexican peso account whose aggregate maximum value exceeds USD $10,000, watch for PFIC exposure on any Mexican FIBRA or investment fund, and coordinate Mexican ISR and US federal positions under the 1993 treaty's foreign tax credit mechanics.

The Medicare problem is acute: US Medicare does not cover services received in Mexico, with narrow exceptions for emergencies near the border. Retirees relocating to Mexico need private Mexican health insurance, IMSS voluntary enrolment, or a hybrid arrangement — see the expat health insurance pillar.

EU residents

EU, Schengen and most European citizens receive a 180-day Forma Migratoria Múltiple on arrival in Mexico — visa-free entry for tourism or short stays. To live in Mexico long-term, the same Residente Temporal route applies as for Americans, filed at a Mexican consulate in the country of legal residence. The tax-side consequences differ in one important respect: EU member states operate residence-based tax systems, so leaving genuinely ends the home-country tax exposure once the OECD-style tie-breaker tests are satisfied. Watch the exit-tax rules in the departing country — Germany's § 6 AStG and France's exit tax under Article 167 bis CGI in particular treat the change of tax residency as a deemed disposal event for substantial shareholdings.

Non-US, non-EU readers

Canadian, UK, Australian, Brazilian, Argentine, and most Asian-passport holders take the same Residente Temporal route via consulate filing in the country of legal residence. Canadians and Britons receive the same 180-day tourist permit on arrival as Americans and Europeans. Brazilian and most Latin American applicants benefit from the CPLP-style preferences at the naturalisation stage — two years' residence rather than five — but the Residente Temporal route and thresholds are the same. Consulate processing times in non-Western jurisdictions are typically longer (six to twelve weeks rather than two to four), and original document requirements stricter.

The income thresholds (2026)

This is the section that almost every other guide gets wrong by quoting a single dollar figure.

Mexican consular guidance pegs the solvencia económica threshold to the Unidad de Medida y Actualización (UMA), an indexed unit published annually by the Instituto Nacional de Estadística y Geografía (INEGI). The UMA replaced the minimum wage as the indexing reference in 2016 to decouple social-benefit thresholds from wage policy.

The 2026 UMA values published by INEGI:

| Period | UMA value (MXN) |

|---|---|

| Daily | 113.14 (2025 base — verify 2026 update) |

| Monthly | 3,439.46 |

| Annual | 41,273.52 |

[source: verify 2026 UMA publication from INEGI before quoting in print]

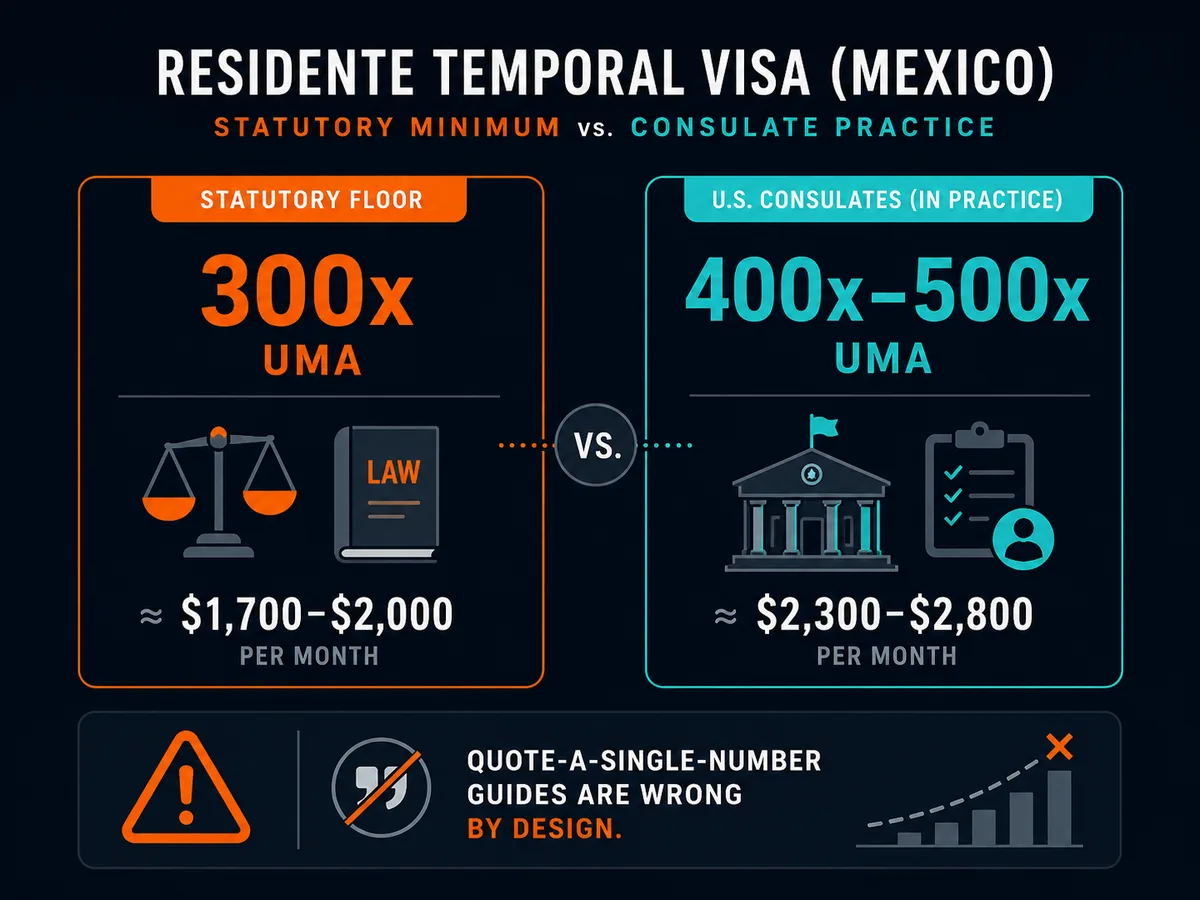

The statutory formula applied by Mexican consulates under the published Lineamientos Generales para la Expedición de Visas:

- Economic solvency via income: monthly average income across the last six months of bank statements of at least 300 × monthly UMA — roughly MXN 31,000–34,000 per month, or approximately USD $1,700–$2,000 at June 2026 exchange rates.

- Economic solvency via savings: average balance across the last twelve months of bank or investment statements of at least 5,000 × monthly UMA — roughly MXN 515,000–570,000, or approximately USD $30,000–$33,000.

That is the statute. What individual consulates actually accept is a different question, and this is where almost every prospective applicant gets caught off-guard.

Consulate-level discretion has tightened materially since 2023. The 300x statutory minimum is now a floor that several high-volume US consulates — San Diego, Houston, Los Angeles, San Francisco, Washington — treat as inadequate, applying their own internal thresholds of 400x to 500x UMA for income (roughly USD $2,700–$3,300 per month) and proportionally higher savings figures. The Toronto, Vancouver, Madrid and London consulates have generally remained closer to the statutory floor. Consulates in smaller US cities and in Latin America vary widely.

There is no public schedule of which consulate applies which multiplier. The only reliable approach is to check the consulate's published Requisitos page directly the week before applying, ideally call the consulate to confirm, and budget evidentiary cushion of at least 50% above the published number.

Application process — step by step

The full process from decision to TRT card in hand typically runs three to six months, depending on consulate appointment availability and INM canje processing in the destination Mexican state.

Step 1 — Gather documents. The standard set required by the Secretaría de Relaciones Exteriores consular network:

- Passport valid at least six months beyond application

- Solicitud de visa form (downloadable from the consulate page)

- Recent passport photograph to ICAO specification

- Original and copy of the last six months' bank or investment statements (income route) or last twelve months (savings route)

- For family-unity applications: apostilled and translated marriage, birth or parental certificates

- Original criminal record certificate from country of residence, apostilled and translated to Spanish (some consulates only)

- Proof of legal residence in the country of consulate filing (residence card, utility bill, lease)

- Payment of the consular visa fee — currently USD $54 (2026)

Step 2 — Book the consulate appointment. Mexican consulates use the MEXITEL appointment system. In 2026, wait times at high-demand US consulates run four to twelve weeks. Most consulates do not accept walk-ins; the appointment is non-negotiable.

Step 3 — Attend the in-person interview. The applicant must appear in person — no proxies, no mailed applications. The consular officer reviews documents, conducts a short interview (usually in Spanish or English; assume Spanish), and either issues a decision on the spot or requests additional documents. If approved, the visa sticker is affixed to the passport within two to ten working days.

Step 4 — Receive the 180-day single-entry visa. The consulate-issued sticker is valid for a single entry within 180 days. Use it to travel to Mexico — by air, land or sea. Present the visa at the port of entry and request the Forma Migratoria Múltiple marked "Canje" rather than the standard tourist box, indicating intent to exchange.

Step 5 — File the canje within 30 calendar days. This is the most-failed step in the entire process. Within 30 calendar days of entering Mexico, present at the Instituto Nacional de Migración office in the city where you plan to reside. The canje filing requires:

- Original passport with the visa and FMM

- Completed Formato Básico form

- Proof of Mexican address (utility bill, lease, hotel reservation)

- CURP (issued at canje appointment if not previously held)

- Payment of the INM canje fee — currently around MXN 5,500 (~USD $325)

- Two passport photographs (one front, one right profile, white background)

Step 6 — Receive the Residente Temporal card (TRT). INM processes the canje and issues the physical TRT card within 30-60 working days. Until the card is in hand, the applicant cannot exit Mexico without a permiso de salida — leaving without it cancels the application.

Mexican tax residency — different from immigration residency

This is the section most applicants skip and most regret.

Holding a Residente Temporal card does not automatically make you a Mexican tax resident. Conversely, not holding one does not exclude you from Mexican tax residency if you trigger the substance test. Mexican tax residency is determined entirely under Article 9 of the Ley del Impuesto Sobre la Renta (LISR), independent of migration status.

LISR Article 9 deems a natural person Mexican tax resident when either of two tests is met:

- The person has established a permanent home (casa habitación) in Mexico. If the person also maintains a home in another country, residency falls to whichever jurisdiction is the centre of vital interests (centro de intereses vitales).

- The centre of vital interests is in Mexico, defined to include: (a) more than 50% of total income in the relevant calendar year derived from Mexican sources, or (b) the principal centre of professional activities is located in Mexico.

The practical effects:

- A US retiree on Residente Temporal who lives full-time in San Miguel de Allende but draws 100% of income from US Social Security and US-based portfolio dividends generally is not Mexican tax resident under LISR Article 9 — neither the home test nor the income test triggers cleanly, because the income is foreign-sourced and the casa habitación analysis depends on tie-breaker mechanics.

- A US remote worker on Residente Temporal who lives full-time in Mexico City and earns 100% of income from a US employer is closer to the line. The casa habitación test almost certainly triggers; the income-source carve-out within the centre-of-vital-interests test offers some shelter, but Mexican tax authorities (SAT) have authority to challenge.

- A US digital entrepreneur who incorporates a Mexican S.A. de C.V. and operates from Mexico is clearly Mexican tax resident — the principal centre of professional activity is in Mexico regardless of where individual clients sit.

Once Mexican tax resident, the individual files an annual ISR return at progressive rates running from 1.92% at the bottom band to 35% above MXN 4,511,707 (roughly USD $260,000) for 2025, with capital gains on financial assets generally taxed at a 10% flat rate for Mexican-source gains. Foreign-source dividends, interest and gains are taxed at the same progressive scale, with foreign tax credit available against tax paid in the source jurisdiction.

The "I have a Residente Temporal card but I'm not Mexican tax resident" position is workable — many Americans operate it successfully — but it depends on careful documentation: retained US tax filings, US driver's licence, US mailing address, US-domiciled investment accounts, and the ability to demonstrate that any Mexican home is not the casa habitación in the LISR Article 9 sense.

US tax implications

Becoming a Mexican resident — for immigration purposes, tax purposes, or both — does not end any US filing obligation. Every US citizen and lawful permanent resident files a Form 1040 every year, reports worldwide income, and faces the full FBAR / FATCA / PFIC compliance stack.

The headline points specific to Mexico:

The 1993 US-Mexico Income Tax Treaty (full text via IRS), as amended by protocols in 2002, allocates taxing rights and provides foreign tax credit mechanics. The treaty's Article 4 tie-breaker mirrors the OECD Model — permanent home, then centre of vital interests, then habitual abode, then nationality, then mutual agreement. Pension distributions and social security are addressed in Article 19, with primary taxation generally allocated to the country of residence. The treaty includes a standard saving clause preserving US taxation of US citizens regardless of treaty residence.

The US-Mexico Totalisation Agreement (SSA reference) entered into force on 1 October 2024, after a decades-long ratification delay. It coordinates Social Security contribution liability between the two systems and allows Americans seconded to Mexico by US employers to remain on US Social Security via a Certificate of Coverage for up to five years, exempt from Mexican IMSS contributions on the same earnings.

FEIE — the Foreign Earned Income Exclusion under IRC §911 — shelters up to $130,000 of qualifying earned income for tax year 2025 if the bona fide residence or physical presence test is met. Useful for remote-working Americans on Residente Temporal who genuinely live in Mexico; useless for retirees drawing passive income.

FTC — the Foreign Tax Credit under IRC §901 — provides dollar-for-dollar credit for Mexican ISR paid on the same income. For Americans who become Mexican tax resident and pay Mexican ISR at the higher progressive bands, the FTC typically eliminates US federal tax on the same income.

FBAR — FinCEN Form 114 — required annually for any US person with Mexican bank accounts whose aggregate maximum value exceeds USD $10,000 at any point in the calendar year. Mexican peso accounts at BBVA, Santander, Banorte, HSBC México and similar all count.

Form 8938 under FATCA — required above the higher thresholds in IRC §6038D: $200,000 on the last day of the year or $300,000 at any point for unmarried filers living abroad, double for married filing jointly.

PFIC — the Mexican-specific trap. Mexican mutual funds (fondos de inversión) and the publicly-traded FIBRAs (Fideicomisos de Infraestructura y Bienes Raíces — the Mexican equivalent of US REITs) are almost universally classified as Passive Foreign Investment Companies under IRC §1291-1298. A US person who buys a FIBRA — including the popular FIBRA Uno, FIBRA Macquarie, FIBRA Prologis — owes punitive PFIC tax via Form 8621. The default §1291 method applies ordinary-income rates on gains spread across the holding period with interest charges that can exceed the gain itself. The practical rule for any American in Mexico: keep all investment assets in US-domiciled brokerage accounts. Use Mexican banks only for current-account and bill-paying purposes.

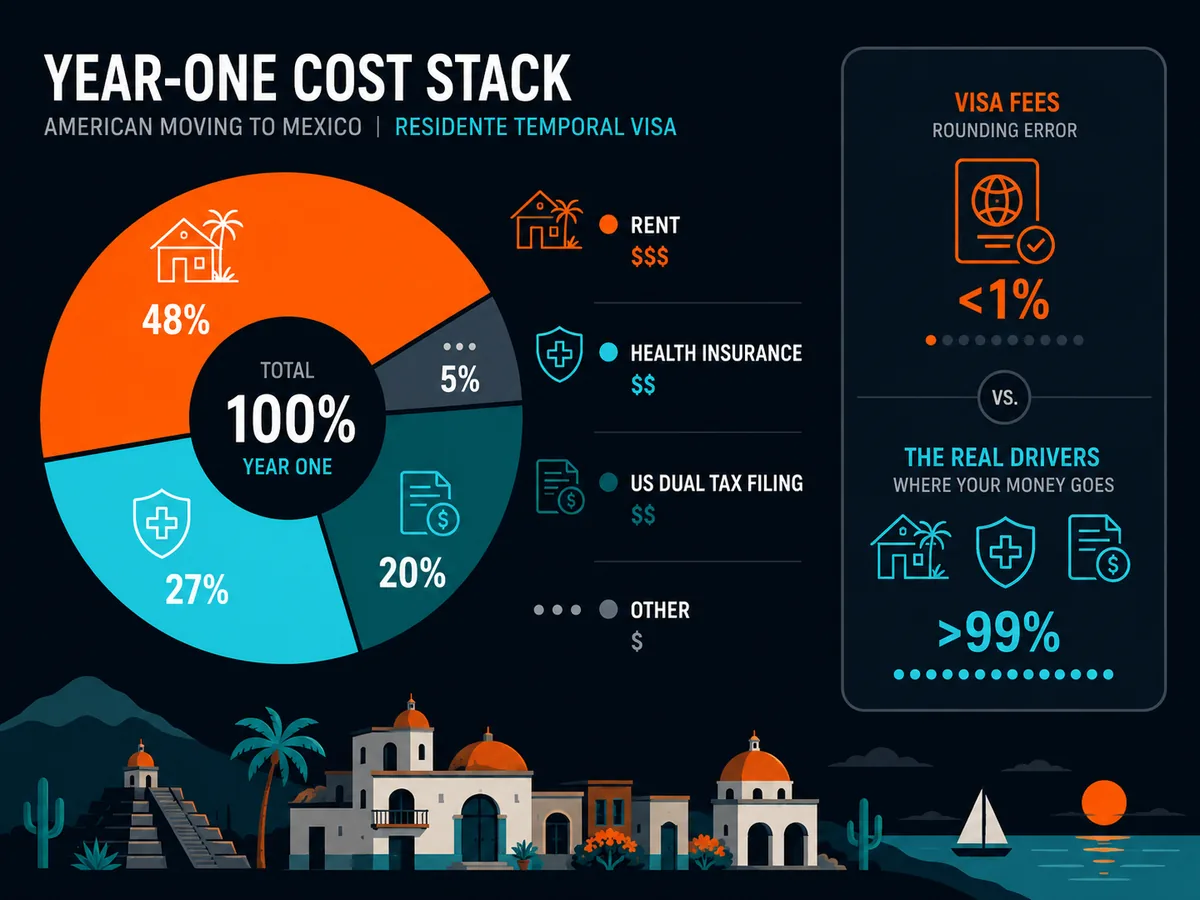

Real-cost stack (year 1)

The visa fees themselves are modest. The full cost stack for the first year on the ground is materially larger.

| Item | Cost (USD) | Notes |

|---|---|---|

| Consular visa fee | $54 per applicant | 2026 SRE schedule |

| INM canje fee (Residente Temporal card) | ~$325 per applicant | MXN ~5,500 at 2026 FX |

| Document apostilles & translations | $200–$500 | FBI background check, state docs, certified Spanish translation |

| Legal/immigration facilitator (optional) | $500–$2,000 | Many DIY successfully; family or complex cases benefit |

| CURP registration | $0 | Issued at canje appointment |

| RFC (tax ID) registration | $0 | Free at SAT office; some hire gestor for ~$50 |

| Mexican bank account opening | $0 | Requires TRT card or temporary RFC; hardest step for non-residents |

| Health insurance (12 mo. private) | $1,200–$3,500 per person | IMSS voluntary annual cost ~MXN 12,000 for 60-yr-old; private higher |

| Rent deposit + first month | $1,500–$5,000 | CDMX, San Miguel, Mérida higher; smaller cities lower |

| Shipping/movers from US | $3,000–$15,000 | 20-foot container; menaje de casa import requires Residente Temporal |

| US-side annual tax filing | $1,500–$3,500/year | Bright!Tax, Greenback or specialist CPA |

| Mexican annual accountancy | $400–$1,200/year | Higher if filing as tax resident with foreign income |

| Single American applicant (DIY-leaning) | ~$8,000–$18,000 | First year, excluding shipping |

| Family of three with counsel | ~$15,000–$30,000 | First year, excluding shipping luxury items |

For the financial infrastructure — moving deposit money, paying Mexican utility bills in pesos while still earning in dollars, multi-currency cards — most American movers set up a Wise account before they leave the US. For travel and gap-period health coverage in the months before IMSS or private Mexican insurance kicks in, SafetyWing covers the pre-permanent insurance layer.

The "digital nomad" question

Mexico has no specific digital nomad visa. This surprises applicants who have read about Portugal's D8, Spain's DNV under the 2023 Startup Law, or Italy's nomad visa published in April 2024. Mexico's federal government has not enacted equivalent legislation despite repeated reports of imminent action.

In practice, remote workers in Mexico use one of three routes:

- Residente Temporal via economic solvency — the standard four-year path described above. Active remote-work income paid into a US bank account generally satisfies the income test at most consulates. This is the route for anyone planning to stay more than 180 days at a stretch.

- 180-day Forma Migratoria Múltiple on entry — US, Canadian, EU and most Western passport holders receive 180 days on arrival. Provided the stay genuinely is temporary and the casa habitación / centre-of-vital-interests tests are not triggered, no Mexican tax residency arises. The trap: serial 180-day stays with brief border runs accumulate. Mexican border authorities have wide discretion to refuse re-entry on the FMM Canje request or to reduce the duration granted on subsequent entries. Several published cases of "Mexico nomads" being denied entry after multiple back-to-back stays surfaced in 2024-2025.

- The Mexico City coworking-visa workaround — informal arrangements with employer-sponsored visas brokered through Mexican relocation firms. These are work-permit visas under Article 52(IV), not nomad visas, and carry the same Residente Temporal four-year cap. They suit a narrow population.

For the broader nomad-visa landscape, see the digital nomad visas pillar, which covers the global comparison including Mexico's structural absence from the formal-nomad-visa map.

Path to Permanente and citizenship

The Residente Temporal four-year clock converts cleanly to permanent residence under defined statutory rules.

Conversion to Residente Permanente. Under Article 55 of the Ley de Migración, eligibility for Permanente arises after:

- Four years on Residente Temporal, or

- Two years on Residente Temporal if married to a Mexican citizen or in legal concubinage with a Mexican national, or

- At any time for retirees meeting the (higher) direct-Permanente income thresholds — generally 500x UMA monthly income, plus residency-history evidence, or

- At any time for parents of Mexican-citizen children.

Permanente status is indefinite, requires no renewal, includes automatic work authorisation, and grants near-equivalent rights to Mexican citizens with the exceptions of voting, certain political offices, and restricted-zone real-estate ownership within 50km of the coast or 100km of borders (the fideicomiso trust workaround handles this).

Naturalization. Mexican citizenship is governed by the Ley de Nacionalidad. Under Article 20, naturalisation is available after five years of legal residence in any combination of statuses. The five-year clock reduces to two years for:

- Nationals of Spanish-speaking Latin American countries, Spain, Portugal, the Philippines or Belize

- Applicants married to a Mexican citizen

- Applicants with a Mexican-born child

- Applicants who have made distinguished cultural, scientific or industrial contributions to Mexico

Mexico recognised dual citizenship in the March 1998 constitutional reform. A US citizen who naturalises as Mexican is not required to renounce US citizenship; the two passports are held in parallel.

The §877A trap for US persons. A US citizen who later acquires Mexican citizenship and then chooses to renounce US citizenship is treated as a "covered expatriate" under IRC §877A if average annual US income tax for the prior five years exceeds an inflation-adjusted threshold ($201,000 for 2025) or net worth exceeds $2 million. Covered expatriates pay a mark-to-market exit tax on the unrealised gain in all worldwide assets above an exclusion amount ($890,000 for 2025). Soveraine's renouncing American citizenship pillar covers the mechanics. The point: Mexican naturalisation is the entry ticket to renunciation, not renunciation itself.

Comparison with peer residency programmes

For prospective movers weighing Mexico against the other passive-income / retirement residency programmes commonly considered:

| Programme | Monthly income floor | Savings alternative | First-stay duration | Path to permanent | Path to citizenship |

|---|---|---|---|---|---|

| Mexico Residente Temporal | ~USD $1,700-$3,300 (consulate-dependent) | ~USD $30,000-$55,000 | 1 year | 4 years (2 if married to MX) | 5 years (2 if Latin American or married to MX) |

| Portugal D7 | ~USD $1,000 (€920) | ~USD $12,000 (€11,000) | 4 months → 2-year permit | 5 years | 5 years |

| Spain NLV | ~USD $2,900 (400% IPREM) | ~USD $35,000 | 1 year → 2-year renewals | 5 years | 10 years (2 for Latin Americans) |

| Panama Friendly Nations | $1,000/mo or $5k deposit | Property option $200k+ | 2-year provisional | 2 years | 5 years |

| Costa Rica Rentista | $2,500/mo for 24 months | $60,000 deposit | 2-year provisional | 3 years | 7 years |

Mexico's numbers compete favourably against Spain and Costa Rica on income threshold, against Portugal on speed-to-permanent-without-language-requirement, and against Panama on civil-society stability and consular network. Where it loses cleanly: the lack of a formal digital-nomad track, the consulate-multiplier uncertainty, and the absence of any Portugal-NHR-equivalent tax incentive for new arrivals.

See the deeper pillars on Portugal D7, non-lucrative visa Spain, and zero-percent-tax residencies for the comparable mechanics in each.

The traps

Consulate-multiplier discretion. The statutory floor of 300x UMA is one thing; what your particular consulate actually accepts is another. The single most-common cause of refusal in 2025-2026 is documenting to the 300x minimum at a consulate that has internally adopted 400-500x. Build evidentiary cushion of 50%+ above the published number; budget for resubmission if the first attempt fails on income grounds.

The 30-day canje window. The single most-common cause of post-approval failure is missing the canje window. The visa is a 180-day single-entry sticker. Once you enter Mexico, the 30 calendar days to file at INM are running whether you have unpacked the boxes or not. Book the INM appointment in your destination city before flying to Mexico wherever possible.

RFC and CURP are gating identifiers. Almost everything in Mexico — opening a bank account, signing a utility contract, registering a vehicle, signing a lease longer than 11 months, importing menaje de casa — requires either an RFC (federal taxpayer ID) or CURP (general population identifier). Get both at the canje appointment. Trying to operate in Mexico without them is months of friction.

PFIC exposure on FIBRAs. The FIBRAs — FIBRA Uno, FIBRA Macquarie, FIBRA Prologis and their peers — look like attractive Mexican real-estate investment trusts to a US investor newly resident in Mexico. They are PFICs under US tax law and produce punitive Form 8621 filings. Stay out of them. Use US-domiciled REITs if you want the same exposure.

The casa habitación tax-residency trigger. US persons who become Residente Temporal but want to avoid Mexican tax residency face the casa habitación test under LISR Article 9. Owning a Mexican house, signing a long lease as the named tenant, and registering Mexican utility accounts in your name all build the case for Mexican tax residency. The strategies for managing this — corporate ownership, shorter leases, careful CFDI documentation — are fact-sensitive and worth a session with a cross-border tax adviser before the first INM appointment.

The §877A renunciation tax. Americans pursuing Mexican naturalisation as a route to eventual US renunciation should run the §877A exit-tax model years before acting. The mark-to-market exit tax is calculated on unrealised gains in all worldwide assets above the exclusion. For a US person with appreciated real estate, deferred-comp accounts, or private business equity, the exit tax can run into seven figures and is owed in the year of renunciation regardless of liquidity.

Banking refusals. Mexican banks generally accept US persons (FATCA-compliance costs are lower than in some EU countries because Mexico has its own large US-person customer base) but require Mexican proof of residence, RFC, and an in-person appointment. Plan to open the account after the canje, not before — most banks will not open accounts for tourist-permit holders.

When to consult a professional

A handful of decision points genuinely justify paid help before acting:

- Cross-border tax planning before becoming Mexican resident. Decisions about realising capital gains, restructuring a US LLC or S-corp, timing Roth conversions, and managing the casa habitación analysis are best made before the first INM appointment.

- US expat tax filing. Non-optional from year one. PFIC exposure on Mexican investment funds alone justifies the fee. Bright!Tax handles the FBAR + FATCA + FEIE stack for Americans in Mexico.

- Real estate in the restricted zone. The fideicomiso trust required for foreigner ownership within 50km of the coast or 100km of borders is a specialised Mexican legal product; do not buy beach property without local counsel.

- Pre-renunciation analysis. Americans considering eventual US renunciation after acquiring Mexican citizenship need IRC §877A modelling years in advance.

For travel-document tracking during the residency years, iVisa handles the visa-on-arrival paperwork most Mexican residents need for non-Mexico travel. For the broader second-passport conversation that some Americans pursue in parallel, Henley & Partners handles the citizenship-by-investment market end-to-end.

See our editorial policy on professional advice and our affiliate disclosure for how we handle service recommendations.

Ready to act on this?

Bright!Tax — US expat tax filings (FBAR + FATCA + FEIE specialists). Every American who moves to Mexico needs a US expat CPA from year one — PFIC exposure on Mexican FIBRAs and the LISR Article 9 residency analysis alone justify the spend. Soveraine readers go to the front of the line through our partner link, and you fund independent editorial in the process.

FAQ

What is a Mexico temporary resident visa?

The Residente Temporal is a Mexican long-stay visa created under Articles 52(VII) and 54 of the Ley de Migración (2011). It permits a foreign national to live in Mexico for an initial year, renewable in one- to three-year increments up to a four-year total. It is granted on three bases: economic solvency (passive income or savings), family unity (Mexican spouse, parent or child), or employer sponsorship. After four years on Temporal — or two years if married to a Mexican citizen — the holder is eligible to convert to Residente Permanente.

How much income do you need for the Mexico temporary resident visa?

The statutory floor is set at 300 times the Mexico City UMA (Unidad de Medida y Actualización) of provable monthly income across the last six months — roughly USD $2,000-$2,200 per month at 2026 exchange rates. In practice, individual Mexican consulates apply their own multipliers ranging from 300x to 500x UMA, so the real number an applicant is asked for can be USD $2,700-$3,300 per month depending on which consulate processes the file. The savings alternative is 5,000 times UMA across the last twelve months, roughly USD $33,000-$36,000.

Can I apply for the Mexico temporary resident visa from inside Mexico?

No. Article 41 of the Reglamento de la Ley de Migración requires the initial Residente Temporal application be filed at a Mexican consulate in the applicant's country of legal residence — not at INM offices inside Mexico. Entering Mexico on a 180-day tourist permit (Forma Migratoria Múltiple) and trying to convert to Residente Temporal inside the country is not permitted. The narrow exceptions — family-unity applications with Mexican spouses or children — still require formal INM filings, not consulate workarounds.

Does Mexico tax US Social Security and 401(k) distributions?

The US-Mexico Income Tax Treaty (1993, amended 2002) generally allocates pension and Social Security taxation to the country of residence under Article 19. A US person who becomes Mexican tax resident under LISR Article 9 typically reports 401(k), IRA and Social Security distributions on the Mexican return, with foreign tax credit available against US tax. The saving clause preserves US taxation of US citizens regardless of Mexican residence — the treaty allocates and prevents double taxation but does not end Form 1040 filing.

Is there a Mexico digital nomad visa?

Mexico has no specific digital nomad visa equivalent to Portugal's D8 or Spain's DNV. Remote workers use one of two routes: the standard Residente Temporal via economic solvency (active foreign-source income generally accepted by most consulates) or the 180-day tourist permit on entry, which US, EU and most Western passport holders receive on arrival for short stays. The latter creates no Mexican tax residency in most cases but provides no path to long-term status or eventual Permanente.

How long does it take to get a Mexico temporary resident visa?

Three to six months end-to-end is realistic. Consulate processing of the initial visa runs two to six weeks once the appointment is held. The visa is issued as a 180-day single-entry stamp in the passport. After entering Mexico, the applicant has 30 calendar days to file the canje (exchange) at the local INM office, which then issues the physical Residente Temporal card (TRT) within 30-60 days. Missing the 30-day window invalidates the visa and requires restarting at the consulate.

Can I get Mexican citizenship through the temporary resident visa?

Yes, on the standard timeline. After four years on Residente Temporal — or two years if married to a Mexican — the holder converts to Residente Permanente under Article 55 of the Ley de Migración. After five years of legal residence in any status, naturalization is available under Article 20 of the Ley de Nacionalidad. Two years suffices for nationals of Spanish-speaking Latin American countries, Spain, Portugal, or those married to a Mexican citizen. Mexico has recognised dual citizenship since the March 1998 constitutional reform, so US citizens are not required to renounce.

What is the difference between Residente Temporal and Residente Permanente?

Residente Temporal is granted for up to four years total and requires periodic renewal. Work authorisation is permitted only if specifically requested and approved (permiso para trabajar). Residente Permanente is indefinite, requires no renewal, includes automatic work authorisation, and grants near-equivalent rights to Mexican citizens except for political rights and certain restricted property rights. The Permanente status is the prerequisite for naturalisation. Most applicants pass through Temporal first; direct Permanente is reserved for retirees meeting higher income thresholds, holders of Mexican family ties, or refugees.

Sources

- Ley de Migración (Mexico, 2011 as amended) — Cámara de Diputados consolidated text — https://www.diputados.gob.mx/LeyesBiblio/pdf/LMigra.pdf

- Reglamento de la Ley de Migración — https://www.diputados.gob.mx/LeyesBiblio/regley/Reg_LMigra.pdf

- Ley del Impuesto Sobre la Renta (LISR, Article 9 — tax residency) — https://www.diputados.gob.mx/LeyesBiblio/pdf/LISR.pdf

- Ley de Nacionalidad (Mexico) — https://www.diputados.gob.mx/LeyesBiblio/pdf/LNaci.pdf

- Instituto Nacional de Migración (INM) — https://www.inm.gob.mx/

- Secretaría de Relaciones Exteriores — consular network — https://www.gob.mx/sre

- INEGI — Unidad de Medida y Actualización (UMA) — https://www.inegi.org.mx/temas/uma/

- Servicio de Administración Tributaria (SAT) — https://www.sat.gob.mx/

- US-Mexico Income Tax Treaty (1993, amended 2002) — IRS treaty documents — https://www.irs.gov/businesses/international-businesses/mexico-tax-treaty-documents

- US-Mexico Social Security Totalisation Agreement — SSA — https://www.ssa.gov/international/Agreement_Pamphlets/mexico.html

- MEXITEL consulate appointment system — https://mexitel.sre.gob.mx/

- IRC §911 (Foreign Earned Income Exclusion) — https://www.law.cornell.edu/uscode/text/26/911

- IRC §901 (Foreign Tax Credit) — https://www.law.cornell.edu/uscode/text/26/901

- IRC §1291-1298 (PFIC) — https://www.law.cornell.edu/uscode/text/26/1291

- IRC §877A (Expatriation tax) — https://www.law.cornell.edu/uscode/text/26/877A

- FinCEN BSA E-Filing (FBAR / Form 114) — https://bsaefiling.fincen.treas.gov/main.html

- IRS Form 8938 (FATCA reporting) — https://www.irs.gov/forms-pubs/about-form-8938

- IRS Publication 54 (Tax Guide for US Citizens and Residents Abroad) — https://www.irs.gov/publications/p54

- US State Department — Mexico country information — https://travel.state.gov/content/travel/en/international-travel/International-Travel-Country-Information-Pages/Mexico.html

- US Embassy in Mexico — https://mx.usembassy.gov/