Italy is not a zero-tax jurisdiction. What it offers is a flat annual tax on foreign-source income — currently €200,000 for new applicants, €100,000 for those grandfathered in before August 2024 — paired with a two-year Investor Visa that converts into a long-term residence permit. The combination is the European Union's most distinctive pull for high-net-worth individuals, and since the UK abolished the non-dom regime in April 2025 it has become the headline destination for departing London money.

The 2024 change matters more than most press coverage acknowledges. Anyone who transferred Italian tax residence on or before 9 August 2024 pays the original €100,000 substitute tax. Anyone whose residence transfer takes effect from 10 August 2024 onwards pays €200,000 — doubled by Decree-Law 113/2024 (Morri Rossetti & Franzosi summary). A further increase to €300,000 is being debated in the draft 2026 Budget Law. This article explains both the visa and the tax regime as one editorial piece, because in practice most users need both.

Henley & Partners — Largest RBI/CBI advisory firm in the world

The two regimes — what "Italian Golden Visa" actually means

Most search traffic for "Italian Golden Visa" conflates two legally separate programmes. Confusing them is the first mistake.

Investor Visa for Italy (visto per investitori). Created by Article 1, paragraphs 148–149 of Law 232/2016, operated by the Ministry of Enterprises and Made in Italy. It is an immigration product: a two-year residence visa for non-EU citizens who commit one of four qualifying investments. EU citizens do not need it.

Regime for new residents (regime dei neo-residenti). Introduced by the 2017 Budget Law as Article 24-bis of the TUIR (DPR 917/1986), amended by Decree-Law 113/2024. It is a tax product: an optional annual substitute tax on all foreign-source income, open to anyone transferring Italian tax residence who meets the prior non-residency test, regardless of nationality.

A non-EU HNW moving from London to Milan will typically use both. An EU citizen moving from Paris uses only the flat tax — freedom of movement covers immigration. Different agencies, different elections.

The €100,000 / €200,000 flat-tax regime (Article 24-bis TUIR)

The legal basis is Article 24-bis of Presidential Decree 917/1986, inserted by the 2017 Budget Law (Law 232/2016) and most recently amended by Decree-Law 113/2024. The Agenzia delle Entrate publishes the official guidance on its English-language portal for new residents.

Who qualifies

Three conditions, all required:

- Italian tax residence. You must transfer tax residence to Italy under Article 2 of the TUIR. From 1 January 2024, that is met if for more than 183 days you (a) have your domicile in Italy (main place of personal and family relationships), (b) have habitual residence in Italy, or (c) are registered in the Anagrafe.

- Prior non-residency. You must not have been Italian tax resident in at least nine of the ten tax periods preceding the first year of the option.

- Election. You exercise the option on your Italian tax return (Modello Redditi PF) for the first qualifying year, or in advance via an optional ruling (interpello) to the Agenzia delle Entrate.

Italian citizens returning home after a long absence qualify on the same terms as foreign nationals — relevant for many Italian-American and Italian-Argentine families.

What it covers

The substitute tax applies to all foreign-source income of the elector, regardless of amount, whether or not brought into Italy, and across all categories — interest, dividends, royalties, foreign employment income, foreign rental income, foreign pensions, and capital gains on non-qualifying foreign shareholdings.

Italian-source income is taxed normally. Rental income from an Italian villa, dividends from an Italian company, employment income earned in Italy, capital gains on Italian assets — these fall outside the substitute tax and are subject to ordinary IRPEF rates (23%–43% plus regional and municipal additions).

Two carve-outs in Article 24-bis itself: - Capital gains from the sale of qualified shareholdings in foreign companies realised in the first five years of the option are excluded and taxed under ordinary rules. - The regime exempts the elector from the foreign asset reporting obligation (Quadro RW) and from wealth taxes on foreign real estate (IVIE) and foreign financial assets (IVAFE).

What it costs

For applicants whose residence transfer takes effect: - On or before 9 August 2024: €100,000 per year for the elector, €25,000 per year per qualifying family member added under Article 433 of the Italian Civil Code (spouse, children, parents, in-laws). - From 10 August 2024 onwards: €200,000 per year for the elector, €25,000 per family member.

Payment is due by the IRPEF balance deadline (30 June following the tax year). Failure to pay terminates the option for that and subsequent years.

Duration

The option runs for a maximum of fifteen tax periods including the first. It can be revoked at any time; revocation is final. The clock starts in the year residence is transferred.

How to apply

The ruling is optional but heavily recommended. The Agenzia delle Entrate publishes a dedicated instruction form and procedure for the interpello. The ruling confirms eligibility in advance and prevents the most expensive error in the regime: making the move and electing, only to be told three years later that the prior-residency test was not met.

The Investor Visa — four tiers

The Investor Visa is operated through the investorvisa.mise.gov.it portal, managed by the Ministry of Enterprises and Made in Italy. Non-EU citizens — and only non-EU citizens — can apply by committing to one of four qualifying investments. The investment must be made within three months of entering Italy on the visa, and held for the duration of the residence permit.

| Tier | Investment | Notes |

|---|---|---|

| Innovative start-up | €250,000 | In an Italian innovative start-up registered in the special section of the company register |

| Limited company | €500,000 | In an Italian limited company already incorporated and operating |

| Philanthropic donation | €1,000,000 | A non-refundable donation supporting projects of public interest in culture, education, immigration management, scientific research, restoration of cultural or natural heritage |

| Italian government bonds | €2,000,000 | Italian government securities (BOTs, BTPs, CCTs, CTZs) with a residual maturity of at least two years |

Source: Investor Visa for Italy portal and the underlying Article 26-bis of Legislative Decree 286/1998 (the Consolidated Immigration Act).

The process

Two-stage approval:

- Nulla osta from the Investor Visa Committee. Online application via the portal with passport, CV, proof of available funds, criminal record certificate, and a no-objection declaration from the target entity (tiers 1, 2 and 3). The Committee's statutory deadline is 30 days from a complete application; 25–35 days is typical.

- Consular visa application. Once the nulla osta is issued, the applicant has six months to apply at the Italian consulate. The visa is issued within a few weeks.

The applicant then has two years to enter Italy. On entry, the visa converts within eight days into a residence permit (permesso di soggiorno per investitori) at the local Questura.

From visa to citizenship

The pathway, assuming continuous compliance:

- Years 0–2: Initial Investor Visa residence permit.

- Year 2–5: First renewal — three-year permit, investment must be maintained.

- Year 5: Eligibility for the EU long-term residence permit (permesso di soggiorno UE per soggiornanti di lungo periodo), which is independent of the underlying investment. Requires stable income, accommodation, A2 Italian and no criminal convictions.

- Year 10: Eligibility for Italian citizenship by naturalisation under Article 9 of Law 91/1992. Requires ten years of continuous legal residence, B1 Italian, integration evidence. Discretionary. Processing: 24–36 months.

The Investor Visa is a long road to citizenship — not a shortcut. The "Italian Golden Passport" framing is misleading; Malta's old CBI and Caribbean CBI programmes delivered passports in 6–18 months.

Who this applies to — read this first

The audience splits three ways, and the practical takeaways diverge sharply.

US persons

If you hold a US passport or green card, the Article 24-bis regime is significantly less attractive than the headlines suggest. The US taxes citizens and LPRs on worldwide income under 26 U.S.C. § 1 and § 61. The Italian substitute tax does not change that. You still file Form 1040, FBAR, and Form 8938.

The harder question is foreign tax credit treatment. The substitute tax is a single annual lump sum, not an item-by-item income tax. Whether it qualifies for credit under IRC § 901 is contested, with no Revenue Ruling on point. Most US-Italian practitioners conclude the FTC is limited or denied for the substitute tax — meaning a US person pays €200,000 to Italy and substantially full US tax on the same foreign income. The flat tax becomes a €200,000 surcharge.

Model the position with a US-side CPA before electing. See our Foreign Earned Income Exclusion piece for the more useful US-side tool.

EU residents

This is the segment for which Italy was designed. The 2024 increase to €200,000 was a direct response to the volume of UK non-doms — many of them EU and Commonwealth nationals — relocating after the April 2025 abolition of the remittance basis. EU citizens skip the Investor Visa (freedom of movement covers entry); the relevant question is the nine-of-ten-year non-residency test.

Two traps. EU exit taxes: France, Germany, the Netherlands and Spain apply them on unrealised gains on substantial shareholdings when residents leave, under ATAD. Sequence the restructure before the move, not after. Treaty residence tiebreakers: under OECD Model Article 4, retaining a permanent home and centre of vital interests in your origin country can keep you resident there despite the Italian election. Cut home-country ties properly.

Non-US, non-EU readers

The cleanest fit. A South African, Indian, Singaporean, Brazilian or Emirati national with no residual exit-tax exposure can use the Investor Visa for residence and Article 24-bis to cap Italian tax on foreign income. For UHNW families with $50m+ in foreign portfolios, €200,000 a year is a rounding error. For applicants in the $3–10m range, the maths is closer — model it before committing.

Total first-year fees outside the substitute tax — visa, legal, accountancy — typically run €30,000–€80,000. See the cost table below.

Real costs and timeline

| Item | Typical cost (EUR) | Notes |

|---|---|---|

| Investor Visa nulla osta application | €0 | The portal application itself is free; criminal records and translations cost €200–€600 |

| Italian consular visa fee | €116 | Standard long-stay visa fee, varies by jurisdiction |

| Residence permit issuance (electronic) | €100–€200 | Plus the standard €76 postal kit and €30.46 revenue stamp |

| Legal fees for the visa + flat-tax application package | €10,000–€30,000 | Italian law firm or specialist boutique |

| Tax ruling (interpello) drafting | €5,000–€15,000 | Recommended even if not strictly required |

| Annual dottore commercialista filings | €5,000–€15,000 | Higher for elaborate offshore structures |

| Annual substitute tax (post-Aug 2024) | €200,000 | Plus €25,000 per family member added |

| Annual substitute tax (pre-Aug 2024, grandfathered) | €100,000 | Same family extension cost |

| Time to nulla osta | 30 days (statutory) / 25–35 days (typical) | From a complete application |

| Time from nulla osta to visa | 2–8 weeks | Depends on consulate workload |

| Time to permanent residence (EU long-term) | 5 years of legal residence | Plus A2 Italian and stable income |

| Time to citizenship eligibility | 10 years of legal residence | Plus B1 Italian, integration evidence |

| Citizenship decision processing | 24–36 months after application | Per the Ministry of the Interior |

Sources: Agenzia delle Entrate, Investor Visa for Italy, Italian Ministry of the Interior and a survey of three Italian law firms' published fee schedules.

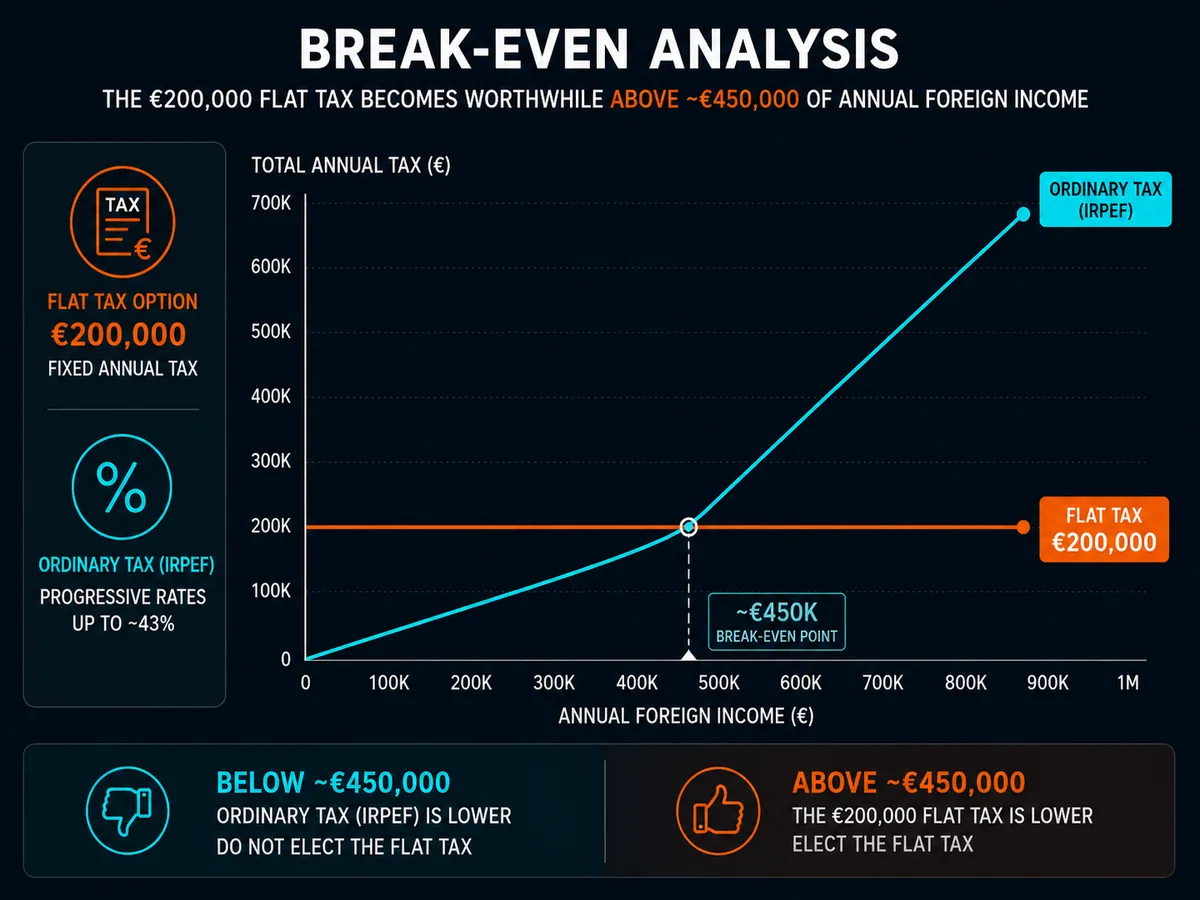

The honest summary: at €200,000 a year, the regime is no longer the bargain it was at €100,000. The break-even against ordinary Italian taxation — IRPEF at up to 43% plus a regional surcharge of 1.23–3.33% and a municipal surcharge of up to 0.9% — is foreign income of approximately €450,000–€500,000 per year. Below that, paying ordinary tax is cheaper.

The 2024 changes

The August 2024 doubling was the largest amendment since 2017:

- 9 August 2024. The Council of Ministers approves Decree-Law 113/2024 ("Omnibus"), raising the Article 24-bis substitute tax from €100,000 to €200,000 for residence transfers after entry into force.

- 10 August 2024. Published in the Gazzetta Ufficiale; takes immediate effect. The €100,000 rate is closed to new applicants.

- 7 October 2024. The decree is converted into Law 143/2024, confirming €200,000 in primary legislation.

- Late 2025. The draft 2026 Budget Law proposes a further increase to €300,000 for new applicants (Arletti Partners analysis). Still in parliamentary passage as of mid-2026.

Grandfathering. Individuals who validly elected before 10 August 2024 continue at €100,000 for the remainder of their fifteen-year window. The family extension stays at €25,000. Pre-existing electors are unaffected by any future increase.

The Meloni government's stated rationale was equity — the original figure had not been indexed. The practical effect has narrowed the cost gap with the old UK £60,000 Remittance Basis Charge, though Italy's fifteen-year duration still beats the UK's four-year FIG window.

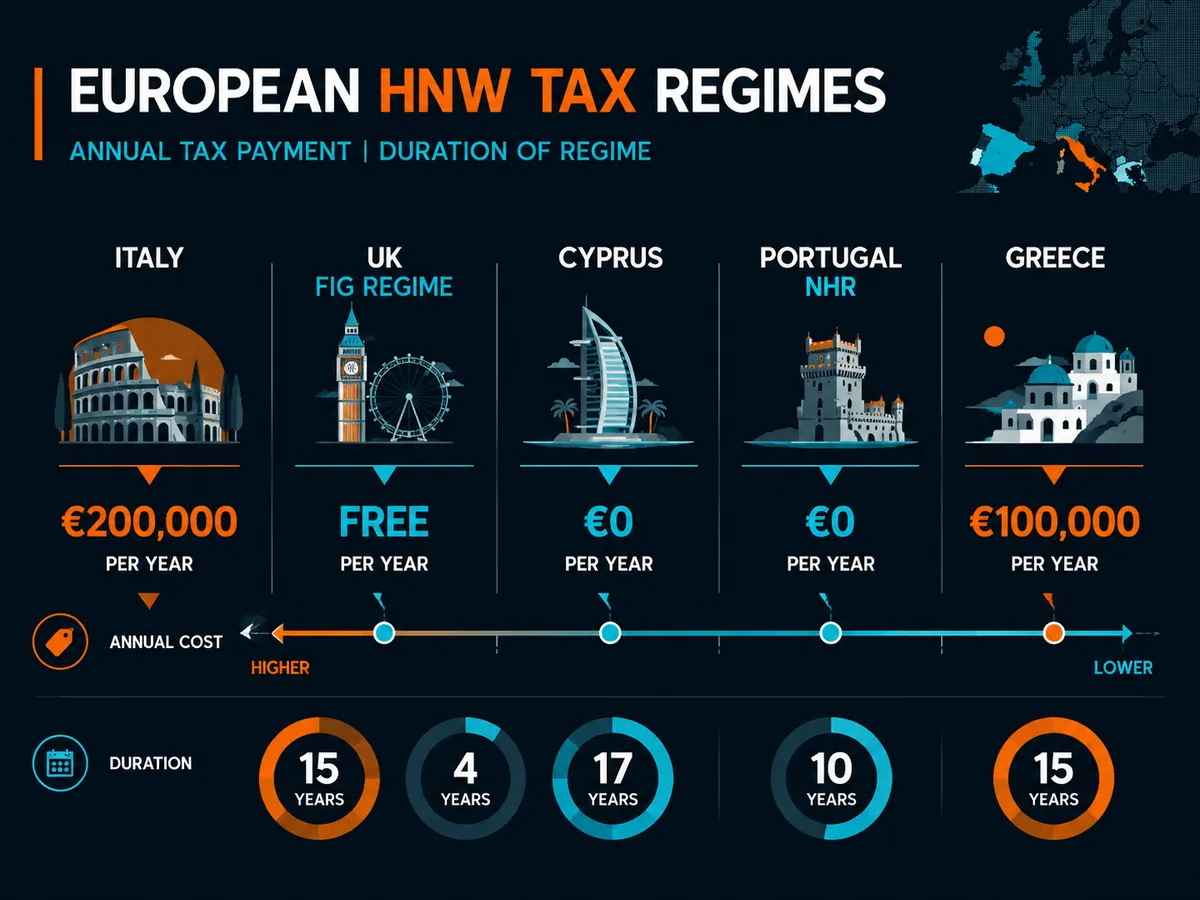

Comparison table

Italy's place in the European HNW landscape, as of mid-2026:

| Country | Regime | Annual tax | Duration | Residency requirement | Family extension |

|---|---|---|---|---|---|

| Italy (Art. 24-bis, post-Aug 2024) | Substitute tax on foreign income | €200,000 | 15 years | 183 days + domicile in Italy | €25,000 per member |

| Italy (Art. 24-bis, grandfathered) | Substitute tax on foreign income | €100,000 | 15 years from election | 183 days + domicile in Italy | €25,000 per member |

| UK (pre-Apr 2025 non-dom) | Remittance basis | £0 – £60,000 RBC | Up to 15 years | UK Statutory Residence Test | None |

| UK (FIG, from Apr 2025) | Foreign Income and Gains relief | £0 | 4 years | 10 prior years non-resident | None |

| Cyprus (non-dom) | Domicile-based exemption on most foreign income | €0 (plus 2.65% GHS) | 17 years | 60 or 183 days | None |

| Portugal (IFICI / NHR 2.0) | 20% on PT prof. income; foreign exempt | Variable | 10 years | 5 prior years non-resident | None (profession-restricted) |

| Greece (Art. 5A) | Substitute tax on foreign income | €100,000 | 15 years | 7 of 8 prior years non-resident | €20,000 per member |

Sources: Agenzia delle Entrate, HMRC, Cyprus Tax Department, Portuguese Tax Authority, AADE Greece.

For a deeper treatment of the UK side, see our non-doms pillar.

The gotchas

Italian tax residency is broader than 183 days. Article 2 of the TUIR, as amended from 1 January 2024, treats you as resident if for more than 183 days you have domicile in Italy (main personal and family relationships), habitual residence, or Anagrafe registration. The 2024 amendment narrowed domicile to a personal/family test, but the net is still wider than a day-count. You can become resident sooner than planned if your family arrives ahead of you.

Treaty tiebreakers can pull you back. Most Italian treaties follow OECD Model Article 4: permanent home, centre of vital interests, habitual abode, nationality. A French citizen who moves to Milan but keeps a Paris apartment with family still in France may find France retains taxing rights despite the Italian election.

CFC rules apply. Italy's CFC regime under Article 167 TUIR (ATAD) attributes profits of low-tax foreign subsidiaries to the Italian resident shareholder. Article 24-bis does not exempt CFC income — a meaningful carve-out that catches crypto and trading entities held through Cayman, BVI or UAE structures. An advance ruling is essential.

CRS reporting is unchanged. Italy participates fully in the Common Reporting Standard. Foreign banks still report your accounts to your country of tax residence — now Italy. The Quadro RW exemption applies only to your return, not to foreign banks' obligations.

The investment must be maintained. For Investor Visa holders, selling the start-up stake, redeeming the BTPs early, or winding down the philanthropic project triggers permit revocation at the year-2 or year-5 renewal.

Substance matters at year 10. No statutory minimum days under Article 24-bis, but at the citizenship stage ten years of continuous legal residence is interpreted strictly. Long absences break continuity. Most successful applicants spend at least 180 days a year in Italy.

When to consult a professional

The minimum competent team for an Italian Golden Visa relocation:

- A dottore commercialista experienced in Article 24-bis to draft the interpello and handle annual filings.

- An Italian immigration lawyer to manage the nulla osta and residence permit conversion.

- A tax adviser in your departing country to model the exit and avoid triggering home-country exit tax or treaty residence.

- For US persons, a US cross-border CPA — no Italian adviser will handle your 1040, FBAR or 8938, and the FTC question needs US-side judgement.

Soveraine does not provide tax advice and has no commercial relationship with the Agenzia delle Entrate or any Italian government body. See our editorial policy, disclaimer and affiliate disclosure.

Ready to act on this?

Henley & Partners — Largest RBI/CBI advisory firm in the world, with a long-standing Italian practice. Soveraine readers go to the front of the line through our partner link, and you fund independent editorial in the process.

FAQ

What is the Italian Golden Visa?

The phrase "Italian Golden Visa" is shorthand for two distinct programmes that the Italian government runs in parallel. The first is the Investor Visa for Italy, a two-year residence visa available to non-EU citizens who commit one of four qualifying investments — €250,000 in an innovative Italian start-up, €500,000 in an Italian limited company, €1 million as a philanthropic donation, or €2 million in Italian government bonds. The second is the Article 24-bis flat-tax regime for new residents, which applies an annual substitute tax to all foreign-source income. The two are legally separate; you can use one without the other, and most HNW relocators use both.

How much is the Italy flat tax for new residents?

It depends on when you became Italian tax resident. Individuals who transferred residence on or before 9 August 2024 are grandfathered at the original €100,000 per year. Anyone whose residence transfer takes effect from 10 August 2024 onwards pays €200,000 per year — the figure was doubled by Legislative Decree 113/2024. In both cases, qualifying family members can be added for €25,000 each per year. The regime is optional, runs for a maximum of fifteen tax periods, and replaces ordinary Italian income tax on foreign-source income only. Italian-source income is taxed normally.

How long does the Italian Investor Visa last?

The initial Investor Visa is issued for two years. On entry, it is converted into an Italian residence permit. The permit can be renewed for an additional three years, and further three-year renewals are available as long as the qualifying investment is maintained. After five years of legal residence you can apply for an EU long-term residence permit (permesso di soggiorno UE per soggiornanti di lungo periodo). After ten years of continuous legal residence you become eligible to apply for naturalisation as an Italian citizen, subject to language and integration requirements. The Investor Visa is residence-by-investment, not citizenship-by-investment.

Does the Italy flat tax help US citizens?

Only at the Italian end. The US taxes its citizens and lawful permanent residents on worldwide income regardless of where they live, under 26 U.S.C. § 1 and § 61. Electing the Article 24-bis substitute tax in Italy does not reduce your US filing obligations, your FBAR or FATCA reporting, or — usually — the US tax you owe. Because the substitute tax is not an income tax on each item of foreign income, the foreign tax credit treatment for US persons is contested. Most US practitioners conclude that paying €200,000 to Italy and the regular US bill on top makes the regime far less attractive than for a non-US client. Speak to a cross-border CPA before electing.

Who qualifies for the Article 24-bis flat-tax regime?

Three tests must be met. First, you must transfer your tax residence to Italy under the rules of Article 2 of the TUIR — broadly, 183 days plus domicile or habitual residence in Italy. Second, you must not have been Italian tax resident in at least nine of the ten tax periods preceding your move. Third, you must exercise the option on your Italian tax return for the first qualifying year, or in advance through the optional ruling procedure with the Agenzia delle Entrate. The regime is available to Italian citizens returning home after a long absence, not only to foreign nationals — a distinction that matters for the Italian diaspora.

What is the difference between the Italian Investor Visa and the flat-tax regime?

They serve different functions. The Investor Visa is an immigration product: it gives non-EU citizens the right to live in Italy in exchange for a qualifying investment held for the life of the permit. The flat-tax regime is a tax product: it caps the Italian tax on all your foreign-source income at a single annual figure. EU citizens do not need the Investor Visa — they have freedom of movement — but they can still elect the flat tax. Non-EU citizens typically need both: the visa to establish residence, the flat tax to make the move financially attractive. Each is governed by separate statute and administered by different ministries.

How does Italy's flat tax compare with the UK non-dom regime?

The UK abolished the remittance basis for non-doms on 6 April 2025 and replaced it with the four-year FIG regime, which costs nothing but lasts only four tax years. Italy's Article 24-bis costs €200,000 a year for new applicants but runs for up to fifteen tax periods. For someone with foreign income above roughly €1.5–2 million per year, Italy is now cheaper than the UK was at the £60,000 Remittance Basis Charge plus tax on remitted funds. For someone with foreign income under that threshold, the FIG regime's four-year window may be more attractive. Italy is the destination most cited by departing UK non-doms, though the cost has narrowed the gap considerably.

Is the Italian flat tax going to increase again?

Possibly. The draft 2026 Italian Budget Law, published in late 2025, includes a proposal to raise the Article 24-bis substitute tax from €200,000 to €300,000 for new applicants transferring residence after the law enters force. The proposal is not yet enacted and the figure may change during parliamentary passage. Existing electors at €100,000 or €200,000 would continue to be grandfathered at their original rate under the proposal as drafted. Anyone considering the regime should monitor the legislative timetable carefully and consider whether to move and elect before the new rate takes effect.

Sources

- Agenzia delle Entrate — New Residents (English portal). https://www.agenziaentrate.gov.it/portale/web/english/non-resident-/new-residents

- Investor Visa for Italy — Ministry of Enterprises and Made in Italy. https://investorvisa.mise.gov.it/

- Investor Visa for Italy — Phase 1, getting your visa. https://investorvisa.mise.gov.it/index.php/en/investor-visa-how-it-works/2-non-categorizzato/21-phase-1-getting-your-investor-visa-for-italy

- Normattiva — DPR 917/1986 (TUIR), Article 24-bis. https://www.normattiva.it/

- Decree-Law 113/2024 ("Omnibus") — converted into Law 143/2024.

- Morri Rossetti & Franzosi — Flat tax on foreign income of new residents doubled to €200,000. https://morrirossetti.it/en/insight/publications/flat-tax-on-foreign-income-of-new-residents-doubled-to-200-000.html

- Arletti Partners — New increase of the flat tax in the 2026 draft Budget Law. https://arlettipartners.com/new-increase-of-the-flat-tax-in-the-2026-draft-budget-law/

- HMRC — Reforming the taxation of non-UK domiciled individuals. https://www.gov.uk/government/publications/tax-changes-for-non-uk-domiciled-individuals/reforming-the-taxation-of-non-uk-domiciled-individuals

- OECD — Model Tax Convention on Income and on Capital. https://www.oecd.org/tax/treaties/model-tax-convention-on-income-and-on-capital-condensed-version-20745419.htm

- EU Anti-Tax Avoidance Directive (ATAD). https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32016L1164