Form 8802 is one of the most misunderstood IRS forms. It is not a tax return, it does not change what you owe, and on its own it produces nothing useful. What it does is start a process: file Form 8802, pay the user fee, wait, and — if the IRS agrees you are a US tax resident — you receive Form 6166, a one-page wet-signature letter on US Treasury letterhead. Form 6166 is the document foreign payers, banks and tax authorities actually want to see. Without it, US-source-equivalent income paid into your account from abroad is generally withheld at the statutory non-treaty rate — frequently 25-30% — recoverable only through the foreign country's slow refund process. This article is a tactical reference: what the two forms do, who can request them, how to apply, what it costs, what it takes, and the most common reasons applications are rejected.

Bright!Tax — US expat tax filings (Form 8802, FBAR, FATCA, FEIE specialists)

What Form 8802 and Form 6166 actually are

These are two different forms. Conflating them is the most common error in this whole area.

Form 8802 — Application for United States Residency Certification — is a request to the IRS for confirmation of your US tax-resident status for a specific calendar year. Filed under Revenue Procedure 2018-50, it carries a user fee and on its own does nothing in the outside world. See the IRS About Form 8802 page.

Form 6166 — Certification of U.S. Tax Residency — is the result. A one-page letter on US Treasury letterhead, signed in original ink by an IRS official, stating that for the calendar year in question the named taxpayer filed (or will file) as a US tax resident. See the IRS Form 6166 page.

Form 6166 is the document foreign payers, banks and tax authorities want to see. Form 8802 is the paperwork that produces it.

Who this applies to — read this first

Only US tax residents can validly request Form 6166. The form does not create residency; it documents it.

US persons

This is the audience Form 8802 is built for. Three categories qualify:

- US citizens — including those living abroad. US citizenship is treated as residency-equivalent for treaty purposes under most US tax treaties.

- Lawful permanent residents (green-card holders) — file Form 1040 on worldwide income while holding LPR status and can request Form 6166.

- Resident aliens meeting the substantial presence test — non-citizens meeting the day-count rules in IRC §7701(b) (generally 183 weighted days). You must compute the days and be ready to defend the calculation.

US persons file 1040 (or 1120 / 1065 / 1041 for entities and pass-throughs) and have a legitimate path to Form 6166. Everything in this guide is aimed at them.

EU residents

You cannot request a US Form 6166 if you are not a US tax resident. The form certifies US residency for US treaty positions — it has no application to your own tax life. If you need a residency certificate to give to a foreign payer (a US client, a German publisher, a Japanese licensee), request your own country's equivalent:

- United Kingdom — Certificate of Residence from HMRC, via GOV.UK.

- France — Attestation de résidence fiscale via the Impôts.gouv.fr online portal.

- Germany — Bescheinigung in Steuersachen from the local Finanzamt.

- Spain — Certificado de residencia fiscal a efectos de Convenio from the Agencia Tributaria.

- Italy — Certificato di residenza fiscale from the Agenzia delle Entrate.

The reason to read this article anyway: many EU residents pick up Form 8802 / 6166 terminology from US-centric SEO and waste time trying to file it. You cannot. The forms above do, in your country, what Form 6166 does in the US.

Non-US, non-EU readers

Same logic. Request a tax residency certificate from your own jurisdiction — UAE Federal Tax Authority, Singapore IRAS, Australia ATO, and so on. Form 8802 is not for you unless you are also a US citizen or LPR. If you are a US citizen living in, say, Dubai, you can and should use Form 6166 to obtain treaty benefits in third countries with US treaties.

When you need Form 6166

Form 6166 is a documentary requirement attached to specific cross-border situations. It is not something to obtain "just in case" — a stale Form 6166 has no value. You need it when:

- Royalty payments from abroad. A US author with a German publisher, a US musician licensing to a UK label, a US software firm licensing to a Japanese distributor. Statutory withholding is often 15-30%; treaties (Article 12) cut it to 0-10% with Form 6166 on file.

- Dividend distributions. From a foreign-domiciled company to a US shareholder. Treaty Article 10 reduces typical 15-30% withholding to 5-15%.

- Interest payments. Treaty Article 11 frequently reduces or eliminates cross-border interest withholding for US-resident payees.

- Pension and annuity income from foreign sources. Treaty Article 17 or 18 allocates taxing rights, usually requiring Form 6166 to claim the position with the foreign payer.

- Service income subject to foreign withholding. Treaty articles for "Business Profits" or "Independent Personal Services" override withholding with Form 6166 as evidence.

- Foreign bank and brokerage onboarding. Some EU banks — particularly in Germany and France — request Form 6166 as part of FATCA/CRS compliance when opening accounts for US persons.

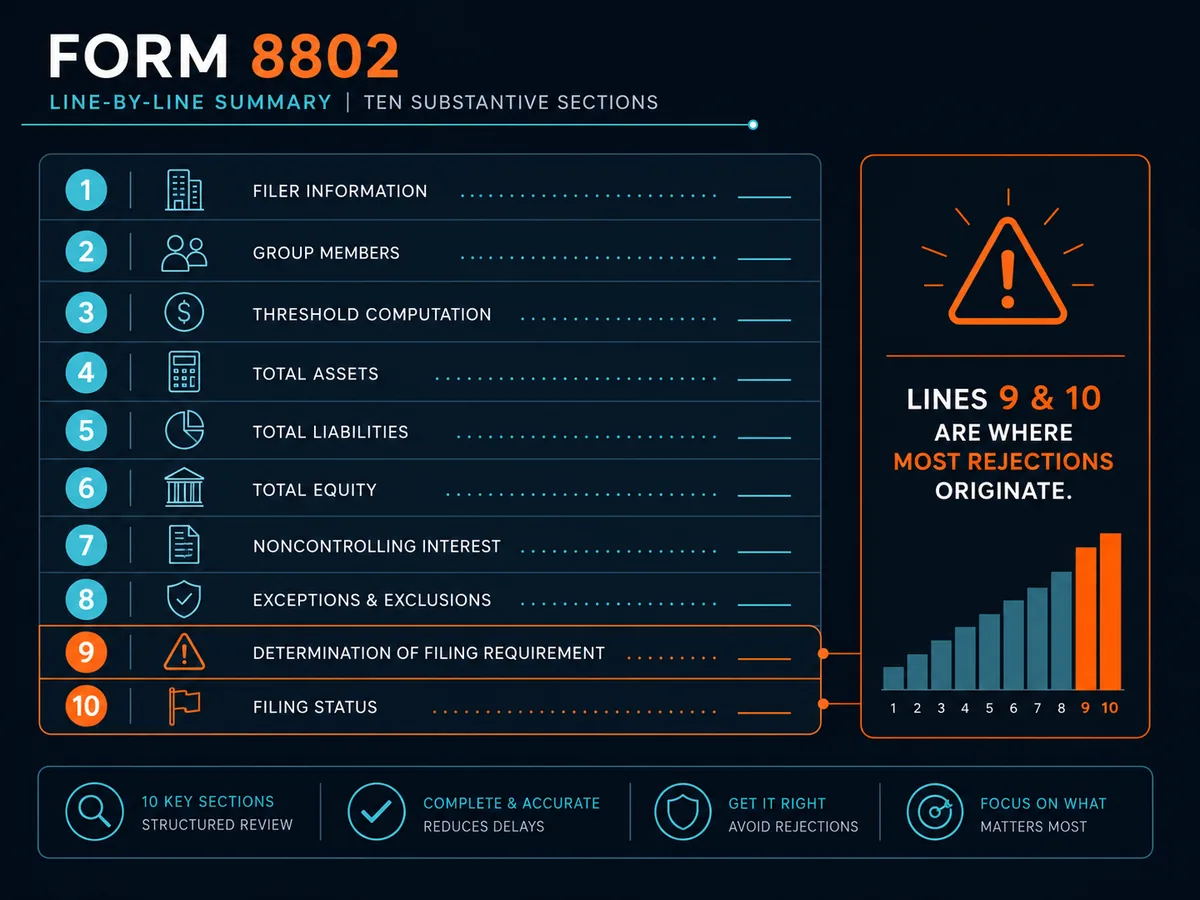

The Form 8802 application — line by line

Form 8802 has ten substantive lines plus the perjury declaration. Confirm the current revision at the IRS Form 8802 page before filing.

- Line 1 — Calendar year. One year per application.

- Line 2 — Applicant name and TIN. Must match the most recent US tax return exactly. Mismatches with IRS records are a leading cause of return-without-action.

- Line 3a — US mailing address. Where Form 6166 will be mailed.

- Line 3b — Foreign address. Required if the applicant lives abroad.

- Line 4 — Applicant type. Individual, corporation, partnership, trust, estate, disregarded entity, etc. The wrong box voids the application.

- Line 5 — Tax return filed. The US return covering the year (1040, 1120, 1065, 1041, 990). The IRS cross-references this against its records.

- Line 6 — Basis of residency. Citizenship, LPR status, substantial presence, or domestic place-of-organisation.

- Line 7 — Country or countries. Multiple countries can be requested on a single Form 8802 under one fee — you receive a separate Form 6166 for each.

- Line 8 — Tax period. Usually the calendar year on Line 1; fiscal year for non-calendar filers.

- Line 9 — Penalties-of-perjury statements. The most error-prone section. The required wording varies by applicant type; paraphrasing invalidates the form.

- Line 10 — Perjury declaration. Signature, title and date — under penalties of perjury per IRC §7206.

User fee and processing time

Under Rev. Proc. 2018-50 the user fee is USD $85 per application for individuals (including sole proprietors and disregarded-entity owners filing in their own name) and USD $185 for non-individual applicants — corporations, partnerships, trusts, estates and others. [source: TODO — confirm 2026 user fee against the current IRS instructions, which may supersede the 2024-2025 figures.]

The fee is paid through Pay.gov before Form 8802 is mailed. Pay.gov issues a confirmation number that goes on Form 8802 itself. A missing or unmatched confirmation is the single most common reason applications are returned.

The IRS advertises a 45-day turn-around once a complete application is received. The realistic window is 60 to 90 days, longer for first-time applicants with a thin US filing history, applicants whose 1040 for the requested year has not yet been filed, and substantial-presence applicants. Many cross-border practitioners file in January for the upcoming calendar year so Form 6166 is in hand before mid-year foreign payments.

Where to send Form 8802

Per the current instructions, the mailing addresses are:

Mail: Internal Revenue Service, Philadelphia, PA 19255-0625 Private delivery (FedEx, UPS, DHL): Internal Revenue Service, 2970 Market Street, BLN# 3-E08.123, Philadelphia, PA 19104

A fax option exists for some applicant types — confirm against the current Form 8802 instructions before using it. E-filing is not available to individuals. The standard path for an individual or single-entity applicant is mail with an original ink signature.

The "perjury statement" trap

Line 9 is where competent applications go wrong most often. The IRS provides exact wording for each applicant category in the instructions — use it verbatim.

- US citizen — "I am a U.S. citizen and have filed (or will file) a Form 1040 with the IRS for the year requested."

- LPR — equivalent attestation, plus a statement that you have not claimed non-resident treaty status with another country (which would terminate LPR status for US tax purposes).

- Substantial-presence resident alien — must include a computation of US days under the formula in IRC §7701(b). Wrong day-count = bounced form.

- Entities — corporations, partnerships, trusts, estates and disregarded entities each have their own required language plus signatory authority requirements.

Misstatement on Line 9 is a perjury offence under IRC §7206(1) — up to three years in prison and a $100,000 fine. Get the exact wording from the current instructions and copy it.

A worked example — German royalty payment

A US-citizen author receives a EUR 50,000 royalty advance from a German publisher in 2026.

Without Form 6166, the publisher applies the statutory royalty withholding on a non-resident author — 15.825% (15% plus the 5.5% Solidaritätszuschlag). Withholding: EUR 7,912. The author receives EUR 42,088 and must reclaim the rest through a non-resident German tax filing — months of paperwork in German, often with a tax-advisor fee that eats into the recovery.

With Form 6166, Article 12 of the US-Germany income tax treaty reduces royalty withholding to 0%. The publisher pays the full EUR 50,000. The income is fully taxable in the US at the author's US rates — no foreign tax credit needed, no refund process, no cashflow lag.

The economic value in this single transaction: roughly EUR 7,900 of immediate cash plus six to twelve months of avoided foreign administration. Against an $85 user fee, the math is not subtle. The same analysis runs through UK royalties under the US-UK treaty, Japanese royalties under the US-Japan treaty, and most other US tax treaties.

Renewal and duration

Form 6166 certifies residency for a single calendar year. There is no multi-year option — to maintain coverage you file a new Form 8802 each year. The application can be filed as early as 1 December of the prior year (per Rev. Proc. 2018-50).

A single Form 8802 can request multiple countries for the same year and applicant under one user fee — you receive a separate Form 6166 for each country listed on Line 7. You can also request multiple copies for the same country if foreign payers each require their own original.

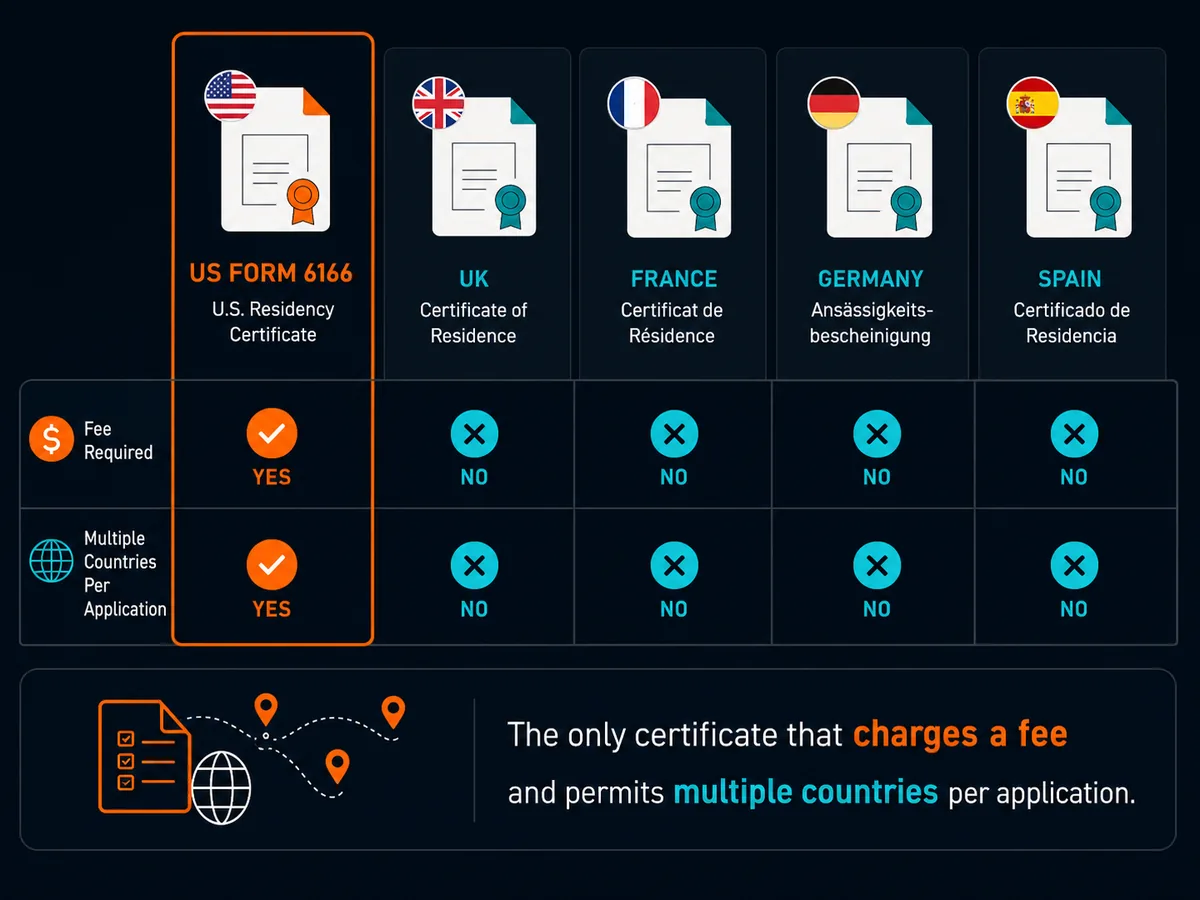

Comparison — US Form 6166 vs European residency certificates

| Document | Country | Issuing authority | Fee | Typical processing | Wet-signature original | Multi-country per request |

|---|---|---|---|---|---|---|

| Form 6166 | USA | IRS, Philadelphia | USD $85 (individual) / $185 (entity) | 45-90 days | Yes | Yes — one application, multiple countries |

| Certificate of Residence | UK | HMRC | Free | 15-30 working days | Yes (or digital, depending on partner) | No — one per country per request |

| Attestation de résidence fiscale | France | DGFiP / Impôts.gouv.fr | Free | 15-30 days online | Yes (PDF with seal accepted in most treaty contexts) | No |

| Bescheinigung in Steuersachen | Germany | Local Finanzamt | Free | 2-6 weeks | Yes | No |

| Certificado de residencia fiscal | Spain | Agencia Tributaria | Free | 1-20 days | Yes | No |

The US is an outlier in three respects: it charges a fee, it has the longest processing window, and it permits multiple countries per application. Practitioners moving clients between US and EU systems should plan timelines accordingly.

The most common rejection reasons

The IRS routinely returns Form 8802 applications without processing when any of the following are present. There is no formal appeal for a return-without-processing — you refile and lose your place in the queue.

- Missing or unmatched Pay.gov receipt. The fee must be paid before mailing, and the confirmation number must appear on the form in the right field.

- Wrong applicant type on Line 4. A single-member LLC owned by an individual files in the individual's name — the LLC is disregarded and not the applicant.

- Missing TIN or name mismatch. SSN/EIN and name must match IRS records exactly.

- Substantial-presence applicants with no day computation. Saying "I meet the substantial presence test" is not enough — Line 9 requires the calculation.

- Year not yet filed without conditional language. If the 1040 for the requested year has not yet been filed, the application must include the "have filed or will file" wording.

- Wrong perjury statement. Using citizen wording for an LPR (or vice versa) is treated as a defective application.

- Filing too early. Form 8802 can be filed from 1 December of the prior year — earlier is returned.

- Outdated form version. Old revisions are returned without comment; use the current form from the IRS website.

What Form 6166 is not

A few clarifying negatives, because the SERP for "US tax residency certificate" is full of misleading copy:

- Not a tax residency status. Form 6166 documents a residency you must already have under US tax law — it is evidentiary, not constitutive.

- Not a treaty position by itself. The foreign country still applies its own domestic law. Form 6166 supplies the documentary basis for a treaty claim; it does not adjudicate one.

- Not a substitute for W-8BEN. Form W-8BEN is what a non-US person gives a US payer. Form 6166 is the opposite direction — a US person to a foreign payer. Not interchangeable.

- Does not waive treaty disclosure on the US return. Treaty-based positions on Form 1040 may still require Form 8833 under Treas. Reg. §301.6114-1. Form 6166 covers the foreign side, not the US side.

When to use a preparer

A competent US expat CPA prepares Form 8802 as a stand-alone for roughly USD 150-400, or bundled into an annual expat return. The cost-benefit against a returned application — and the lost processing time that costs — favours professional preparation in most cases other than the simplest single-country US-citizen filing.

Use a preparer when:

- You are an LPR with prior treaty-claim history in another country.

- You are a substantial-presence applicant.

- You are filing for an entity — especially a partnership or trust where signatory authority is non-obvious.

- You need Form 6166 for multiple countries simultaneously.

- A previous Form 8802 has been returned without processing.

For straight US-citizen, single-country, current-year applications, careful self-preparation works — read the instructions front to back, pay the fee on Pay.gov first, and copy the Line 9 wording verbatim.

Greenback, MyExpatTaxes and Bright!Tax all offer Form 8802 preparation as an a-la-carte service. Compare on country experience first, price second. If you are also moving money between the US and the country requesting Form 6166, Wise is our default reference for multi-currency receiving accounts. See our affiliate disclosure on how we pick partners.

Ready to act on this?

Bright!Tax prepares Form 8802 applications routinely for US expats receiving foreign royalty, dividend and service income. Soveraine readers go to the front of the line through our partner link, and you fund independent editorial in the process.

FAQ

What is IRS Form 8802 used for?

Form 8802 is the application form a US taxpayer files with the IRS to request Form 6166 — a wet-signature letter from the IRS certifying that the applicant is a US tax resident for treaty purposes. Form 8802 itself is not a tax return and does not change what you owe. Its only function is to start the IRS's residency-certification process so a foreign payer, bank or tax authority will apply your treaty withholding rate instead of the statutory 30%.

What is the difference between Form 8802 and Form 6166?

Form 8802 is the application; Form 6166 is the result. You file Form 8802 with the IRS, pay the user fee, and — if approved — receive Form 6166 in the mail. Form 6166 is the document foreign payers actually want to see. It is a one-page letter on US Treasury letterhead with an original signature confirming that, for a specific calendar year, you filed as a US tax resident. Confusing the two is the single most common mistake among first-time applicants.

How much does Form 8802 cost?

The user fee is USD $85 for an individual applicant and USD $185 for non-individual applicants (corporations, partnerships, trusts, estates), per the IRS Form 8802 instructions. The fee is paid through Pay.gov before the form is mailed; the payment confirmation number must be entered on Form 8802 itself. One user fee covers a single application, which can request certifications for the same year, the same applicant, and multiple countries.

How long does the IRS take to process Form 8802?

The IRS advertises a 45-day processing window once a complete application is received. In practice, 60 to 90 days is more realistic, and first-time applicants without a US filing history can wait longer while the IRS validates the underlying residency claim. File Form 8802 well before the foreign deadline you need Form 6166 for — many practitioners file in January for the entire upcoming year.

Can a non-US person get Form 6166?

No. Form 6166 certifies US tax residency. It is only available to taxpayers who can validly assert that status — US citizens, lawful permanent residents, and resident aliens who meet the substantial presence test. If you are a tax resident of France, the UK, Germany or anywhere else, you do not request Form 6166; you request the equivalent certificate from your own tax authority (for example HMRC's Certificate of Residence, France's Attestation de résidence fiscale, or Germany's Bescheinigung in Steuersachen).

Does Form 6166 cover multiple years?

No. Each Form 6166 certifies residency for a single calendar year. A new Form 8802 must be filed each year you need a fresh certificate. The single application can, however, request certifications for multiple countries within the same calendar year and can request multiple original copies of the same certificate at no extra per-copy fee, subject to the limits in the Form 8802 instructions.

What happens if I don't have Form 6166?

The foreign payer is generally required by its own tax law to withhold at the statutory non-treaty rate — frequently 15-30% for dividends, royalties and interest. You can usually claim that withholding back later through the foreign country's tax-refund process, but that takes months to years, requires foreign-language filings, and ties up cash in the meantime. Form 6166 prevents the problem at source.

Is Form 8802 the same as a W-8BEN?

No. Form W-8BEN (for individuals) and W-8BEN-E (for entities) are forms a non-US person gives to a US payer to claim treaty benefits on US-source income. Form 8802 is the opposite direction: a US person applying to the IRS for a certificate to give to a foreign payer to claim treaty benefits on foreign-source income. The two forms operate at opposite ends of the same treaty machinery.

Sources

- IRS — About Form 8802, Application for U.S. Residency Certification: https://www.irs.gov/forms-pubs/about-form-8802

- IRS — Form 6166, Certification of U.S. Tax Residency: https://www.irs.gov/individuals/international-taxpayers/form-6166-certification-of-us-tax-residency

- IRS — Revenue Procedure 2018-50 (Form 8802 user fee and procedures): https://www.irs.gov/pub/irs-drop/rp-18-50.pdf

- Internal Revenue Code §894 — Income affected by treaty (Cornell LII): https://www.law.cornell.edu/uscode/text/26/894

- Internal Revenue Code §1441 — Withholding of tax on nonresident aliens (Cornell LII): https://www.law.cornell.edu/uscode/text/26/1441

- Internal Revenue Code §1442 — Withholding of tax on foreign corporations (Cornell LII): https://www.law.cornell.edu/uscode/text/26/1442

- Internal Revenue Code §7701(b) — Definition of resident alien and nonresident alien (Cornell LII): https://www.law.cornell.edu/uscode/text/26/7701

- Internal Revenue Code §7206 — Fraud and false statements (Cornell LII): https://www.law.cornell.edu/uscode/text/26/7206

- Treasury Regulation §301.6114-1 — Treaty-based return positions (eCFR): https://www.ecfr.gov/current/title-26/chapter-I/subchapter-A/part-301/section-301.6114-1

- IRS — About Form W-8 BEN: https://www.irs.gov/forms-pubs/about-form-w-8-ben

- IRS — About Form 8833 (treaty-based return position disclosure): https://www.irs.gov/forms-pubs/about-form-8833

- US Treasury — US Model Income Tax Convention (2016): https://home.treasury.gov/policy-issues/tax-policy/treaties

- US Treasury — US-Germany Income Tax Treaty (Protocol 2006, in force 2007): https://home.treasury.gov/system/files/131/Treaty-Germany-TE-12-9-2010.pdf

- US Treasury — US-UK Income Tax Treaty: https://home.treasury.gov/system/files/131/Treaty-UK-TE-7-19-2002.pdf

- UK HMRC — How to apply for a certificate of residence: https://www.gov.uk/guidance/get-a-certificate-of-residence

- Pay.gov — IRS user fee payment portal: https://www.pay.gov/