The FBAR is one of the most consequential US filing obligations almost nobody outside the United States has heard of — and one many Americans abroad discover only after a foreign bank asks them to sign a W-9. This guide covers who has to file FinCEN Form 114, what counts as a reportable account, the $10,000 threshold, the deadline, the penalties for missing it, and how the rules apply differently depending on your passport. Nothing here is tax advice. The FBAR is a YMYL topic where a wrong move can cost five figures, and a qualified cross-border accountant is cheaper than a penalty notice.

Bright!Tax — US expat tax filings (FBAR + FATCA + FEIE specialists)

What is the FBAR

The FBAR — Report of Foreign Bank and Financial Accounts, formally FinCEN Form 114 — is a US Treasury filing required of any US person whose foreign financial accounts had a combined value exceeding $10,000 at any time during the calendar year. It is administered by the Financial Crimes Enforcement Network (FinCEN), a bureau of the Treasury, not by the IRS, although the IRS enforces it.

The legal basis sits in the Bank Secrecy Act of 1970, codified at 31 U.S.C. § 5314 and implemented through 31 CFR § 1010.350. The FBAR is filed electronically through the BSA E-Filing System. There is no paper-filing option for individuals in routine cases.

It is an informational report. It does not, by itself, generate any tax. It simply tells Treasury where your money is held outside the United States.

Who this applies to — by nationality

This article splits readers into three groups because the FBAR question has three different answers.

US persons — citizens, green-card holders, US tax residents

The FBAR applies to you in full, regardless of where you live. The United States is one of two countries that taxes on the basis of citizenship rather than residency (the other is Eritrea), and Treasury reporting follows the same logic. A US citizen who has lived in Berlin for 20 years and has never set foot in the IRS's jurisdiction in adulthood still files an FBAR every year if their German, French and Swiss accounts crossed $10,000 in aggregate.

"US person" for FBAR purposes, per FinCEN's instructions for FinCEN Form 114, includes:

- US citizens, including dual nationals

- US lawful permanent residents (green-card holders), even if they live abroad

- Individuals who meet the IRS substantial presence test

- Entities formed under US law — LLCs, corporations, partnerships, most trusts and estates

Single-member LLCs file their own FBAR if they hold foreign accounts, even though they are disregarded for income-tax purposes. This catches a lot of solo founders by surprise.

EU freelancers and digital nomads who are not US persons

If you are an EU citizen, resident, or freelancer with no US passport, no green card, and no substantial US presence, the FBAR does not apply to you. Your reporting obligations sit with your country of tax residence. France has its own foreign-account reporting (the 3916 form). Germany requires foreign-account disclosure on the Anlage AUS. Spain has Modelo 720, with its own substantial penalties for omission.

EU readers should care about the FBAR for two reasons: if you marry a US person, joint accounts become reportable; and if you take a green card for US work, you inherit the obligation the day it issues.

Non-US, non-EU readers

If you hold a passport from a territorial-tax jurisdiction — Singapore, the UAE, Panama, Paraguay, Georgia, Malaysia under MM2H — and you are not a US person, you have no FBAR obligation. Foreign-account reporting in your home country may still apply, but the FinCEN regime does not reach you. Where the FBAR matters to this audience is when advising US-person clients, partners, or co-founders: any account on which a US person has signature authority is reportable by that US person, even if the funds belong to a non-US entity.

What counts as a foreign financial account

The reportable account list is broader than most people assume. Per 31 CFR § 1010.350 and the IRS FBAR Reference Guide, reportable accounts include:

- Bank accounts (checking, savings, time deposits)

- Securities and brokerage accounts

- Mutual funds and pooled investment vehicles

- Foreign-issued life insurance with cash value

- Foreign-issued annuities

- Commodity futures and options accounts

- Foreign pension and retirement accounts (with narrow exceptions for certain treaty-protected plans)

Cryptocurrency held in self-custody wallets is not currently reportable on the FBAR, per FinCEN Notice 2020-2. Crypto held on a foreign exchange is a grey area: FinCEN has signalled it will issue rules bringing virtual-currency accounts within FBAR scope, but as of publication that rule is not final. [source: TODO — confirm current status of FinCEN proposed rule on virtual currency FBAR reporting]

Accounts you do not report:

- US-based accounts, even if they hold foreign currency

- Accounts of an international financial institution where the US government is a member

- Correspondent or nostro accounts

- Accounts held in a US military banking facility

A foreign-issued credit card with no positive balance ability is not a financial account. A Wise multi-currency account held in your name, by contrast, is.

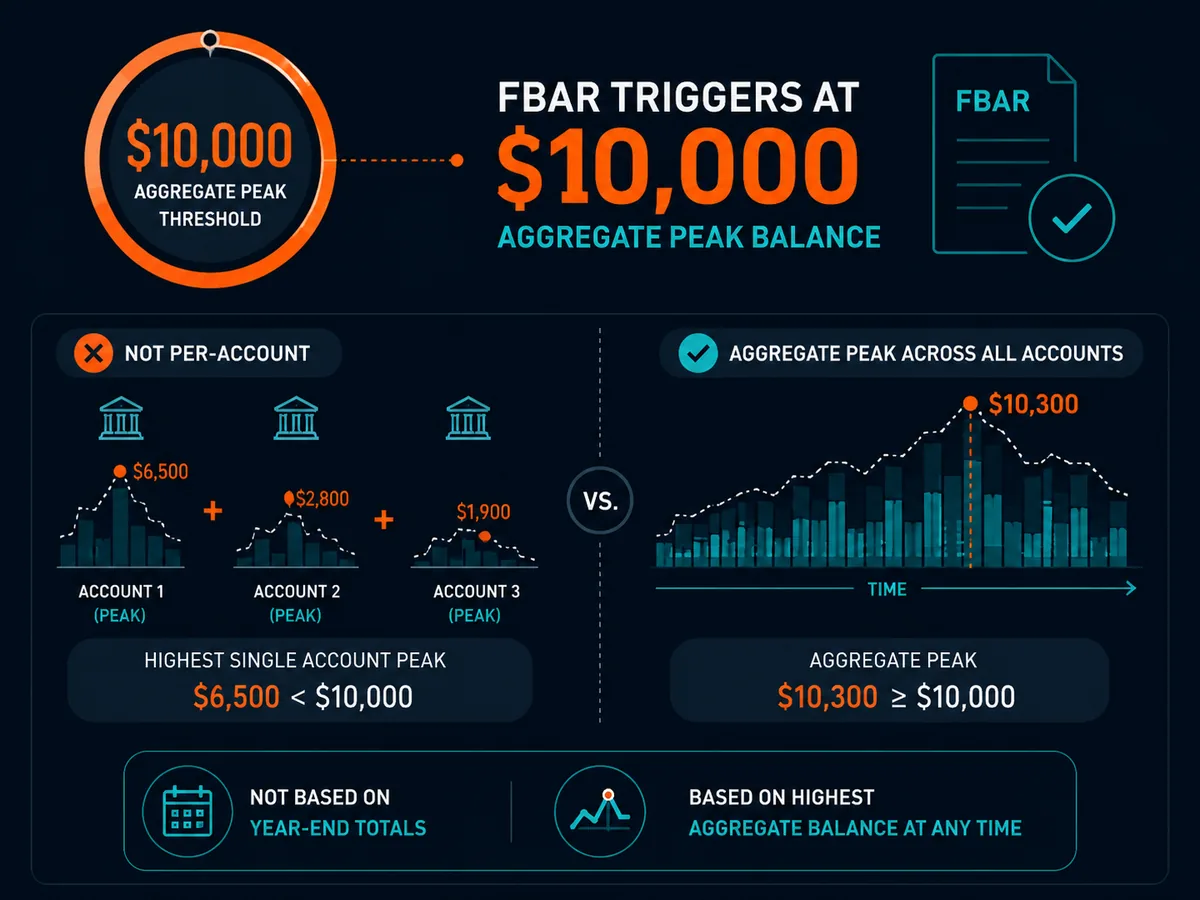

The $10,000 threshold — what actually triggers filing

The threshold is the aggregate maximum balance across all your foreign accounts at any single point during the calendar year. Two facts trip people up:

It is aggregate, not per account. Six accounts holding $2,000 each on the same day cross the line.

It is the peak, not the year-end. A wire of $30,000 that landed in your Singapore account on a Tuesday and left for a property purchase on Wednesday is enough. The account peaked at $30,000; the FBAR is due.

You report the maximum value of each account during the year, in US dollars, using the Treasury Financial Management Service year-end exchange rates (or a verifiable rate if Treasury does not publish one for that currency).

Who is required to file an FBAR

To restate the core rule cleanly: you file an FBAR if all three are true.

- You are a US person (see above).

- You had a financial interest in or signature authority over one or more foreign financial accounts.

- The aggregate maximum value of those accounts exceeded $10,000 at any time during the calendar year.

"Financial interest" includes accounts you own directly, accounts owned by an entity in which you hold more than 50% of the voting power or value, and accounts held by certain trusts where you are grantor or beneficiary. "Signature authority" means you can dispose of assets in the account by communicating directly with the institution — even if the money is not yours. Employees who can sign on a corporate account abroad have an FBAR obligation, though some narrow employee exemptions apply for officers of SEC-registered entities.

Do I need to report a foreign bank account with less than $10,000

If — and only if — the combined balance of every foreign account you hold (or sign on) stayed under $10,000 for every single day of the year, you do not file. If you held $9,500 in one account for 364 days but it briefly hit $11,000 on December 30 after a transfer, you file.

A common misconception: people assume the test is per account. It is not. A $4,000 balance in one country plus an $8,000 balance in another, on the same day, triggers the obligation.

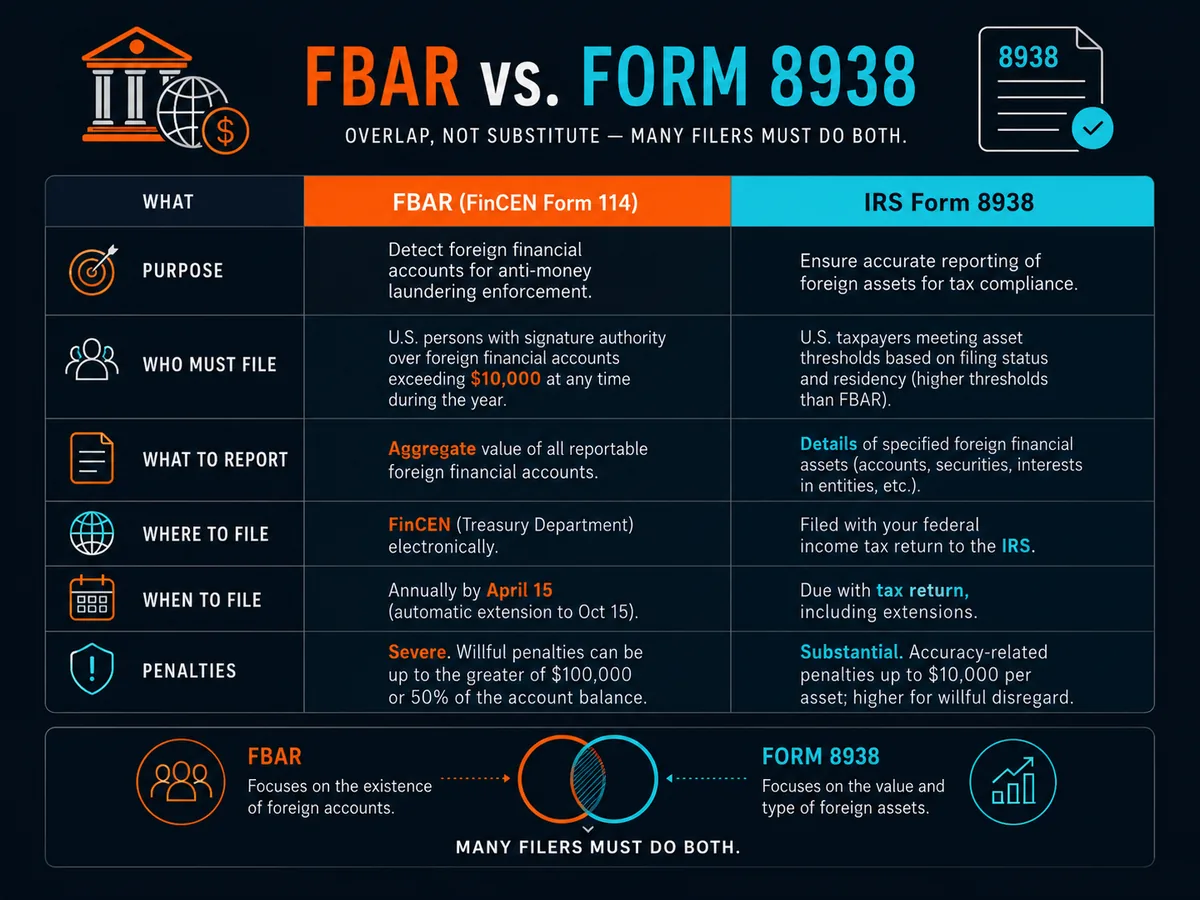

Note also: the FBAR threshold ($10,000) is different from the Form 8938 threshold ($50,000 single / $100,000 married filing jointly for US residents, with higher thresholds for taxpayers abroad). Form 8938 is filed with your Form 1040 under FATCA, per IRS instructions for Form 8938. The two forms overlap but neither replaces the other. Many filers must do both.

What happens if you don't file an FBAR

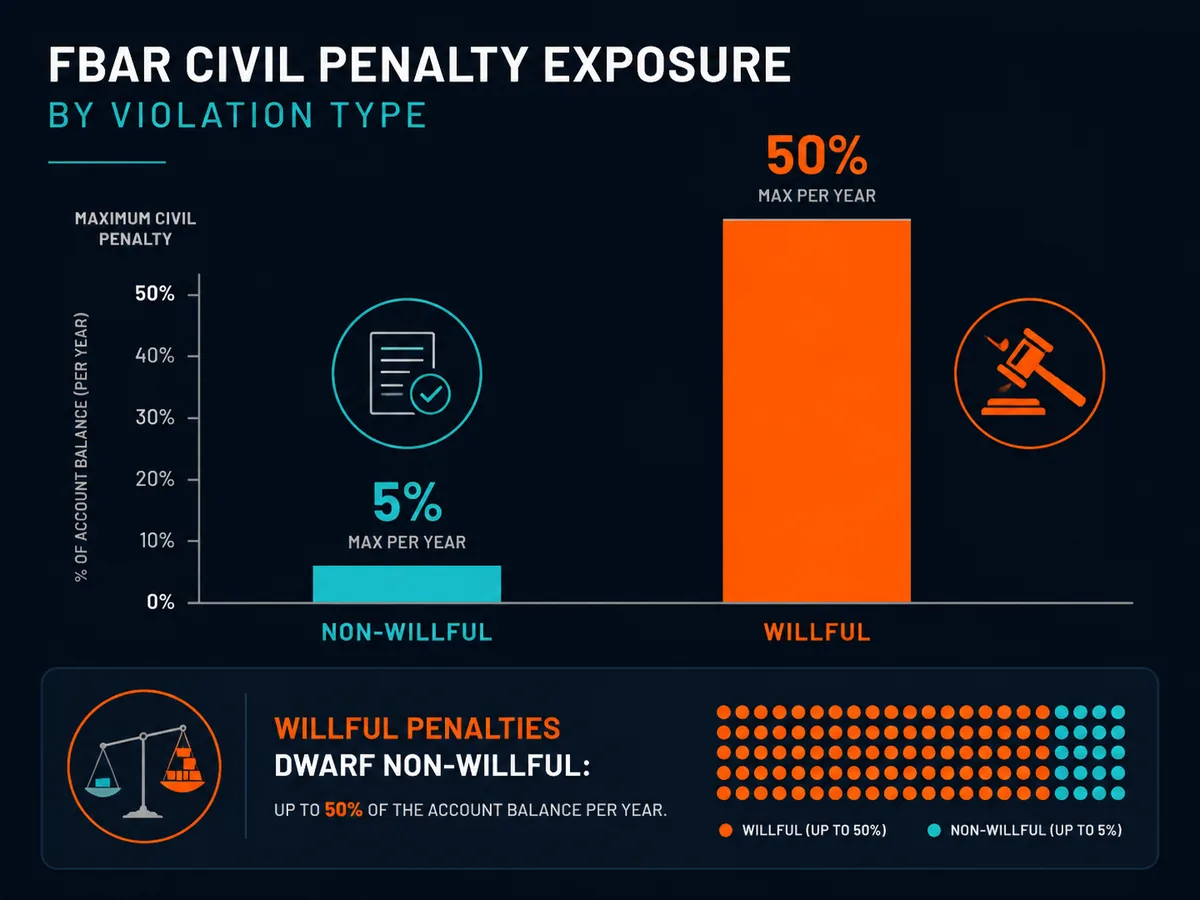

Penalty exposure depends entirely on whether your failure was non-willful or willful.

Non-willful failure — you did not know, or did not understand the obligation, and the omission was not reckless. Civil penalty: up to $16,536 per violation (2024 figure, adjusted annually for inflation per 31 CFR § 1010.821). The Supreme Court's 2023 decision in Bittner v. United States clarified that the non-willful penalty applies per form, not per account — a major reduction in exposure for filers with many small accounts.

Willful failure — you knew about the obligation and chose not to file, or you acted with reckless disregard. Civil penalty: the greater of $165,353 or 50% of the account balance at the time of the violation, per year. Criminal penalties under 31 U.S.C. § 5322: up to $250,000 in fines and 5 years' imprisonment, rising to $500,000 and 10 years if the violation occurred while violating another US law.

If you are behind on FBARs but have always reported the income from those accounts on your 1040, the Delinquent FBAR Submission Procedures let you file late with no penalty. If you are behind on both FBARs and income reporting and the failure was non-willful, the Streamlined Filing Compliance Procedures waive penalties on the FBARs and offshore information returns, though tax and interest on three years of amended returns is still owed.

Both programs require you to file before the IRS contacts you. Audit notice arrives first, the programs close.

How does the IRS know if you have a foreign bank account

Three answers, in order of importance.

FATCA. The Foreign Account Tax Compliance Act, enacted in 2010, requires every foreign financial institution to either (a) report accounts held by US persons directly to the IRS, or (b) suffer a 30% withholding tax on US-source payments. Over 110 jurisdictions have signed intergovernmental agreements implementing FATCA, per the Treasury IGA list. Your foreign bank already sent the IRS your name, address, account number, and year-end balance.

Common Reporting Standard (CRS). OECD's CRS is the international equivalent of FATCA — over 120 jurisdictions exchange account data automatically. The US is not a CRS signatory (it relies on FATCA bilaterally) but US authorities receive supplementary data through other channels.

Whistleblower and self-disclosure. The IRS Whistleblower Office pays 15–30% of recovered tax to informants. Ex-spouses, ex-business partners, and disgruntled employees of foreign banks have produced some of the largest offshore enforcement actions on record, including the Credit Suisse and UBS cases.

If your foreign account exists, the IRS likely already knows. The FBAR is your chance to declare it before the cross-reference flags the gap.

Realistic costs, fees and timeline

The FBAR itself is free to file. Professional fees vary widely. Indicative costs as of 2026:

| Service | Typical cost | What you get |

|---|---|---|

| Self-file via BSA E-Filing | $0 | Direct submission of FinCEN Form 114 |

| Bright!Tax, Greenback, Taxes for Expats — FBAR-only filing | $100–$200 per year | Preparation and filing for a single FBAR |

| FBAR included with full expat tax return | $400–$700 add-on | FBAR filed alongside Form 1040 and Form 8938 |

| Streamlined Filing Compliance Procedures (catch-up package) | $2,500–$6,000+ | 3 years amended returns + 6 years FBARs + non-willful certification |

| Cross-border tax attorney (willful or audit defence) | $500–$1,000/hour | Legal privilege, voluntary disclosure programs, litigation |

[source: TODO — confirm current published rates from Bright!Tax, Greenback Tax Services, and Taxes for Expats]

Timeline. Self-filing the FBAR takes 30–60 minutes once you have account numbers, institution addresses, and maximum balances. The BSA E-Filing System issues a submission ID immediately. Streamlined catch-up filings take 4–12 weeks with a preparer, longer if you need to reconstruct historical balances from closed accounts.

Soveraine has no affiliate relationship with any of the providers listed above; they are mentioned because they are the most-referenced names in the expat-tax category, not because they are necessarily the best fit for your situation. See our affiliate disclosure for our policy.

Common mistakes and how to avoid them

Treating Form 8938 and the FBAR as the same. They are not. The FBAR goes to FinCEN through BSA E-Filing; Form 8938 goes to the IRS with your 1040. Thresholds, definitions, and penalties differ. File both when both apply.

Forgetting accounts with signature authority. The corporate account at your foreign employer, the joint account with a non-US parent, the trust account where you are co-signatory — all reportable, even if no money belongs to you.

Using year-end balance instead of peak balance. The form asks for maximum value during the calendar year. Year-end is irrelevant to the test.

Omitting closed accounts. An account closed in March is still reportable if it held funds during the year. The form has a checkbox for accounts closed during the reporting period.

Single-member LLC filers missing the entity FBAR. If your US LLC holds a foreign account, the LLC files its own FBAR in addition to your personal one.

Assuming Wise, Revolut and Payoneer are US accounts. Wise's UK and Belgian entities issue accounts that are legally foreign. Revolut's licensed entity varies by region. Check the country your account is held in — not the app's logo.

Believing renouncing US citizenship eliminates back-filing. It does not. You owe FBARs for every year you were a US person, even after expatriation. Renunciation also triggers the exit tax under IRC § 877A for covered expatriates.

When to consult a qualified professional

You should engage a cross-border accountant or tax attorney if any of the following apply:

- You are behind by more than one year on FBAR filings.

- You have foreign accounts above $1 million in aggregate.

- You hold foreign mutual funds, ETFs or pension accounts (PFIC and Form 8621 issues).

- You are a US person with a controlled foreign corporation, foreign partnership or foreign trust.

- You are considering renunciation or have inherited foreign assets.

- You received a Letter 3949, Letter 6291, or any FinCEN/IRS contact mentioning foreign accounts.

For routine cases — one or two foreign accounts, income already reported, modest balances — self-filing through BSA E-Filing is straightforward. For anything else, the cost of professional advice is small relative to the penalty exposure. As with all tax matters, consult a qualified professional licensed in both your home and target jurisdictions before taking material action. See our editorial policy and disclaimer.

Ready to act on this?

Bright!Tax — US expat tax filings (FBAR + FATCA + FEIE specialists). Soveraine readers go to the front of the line through our partner link, and you fund independent editorial in the process.

FAQ

Who is required to file an FBAR?

Any United States person with a financial interest in, or signature authority over, one or more foreign financial accounts whose aggregate value exceeded $10,000 at any point during the calendar year. "US person" means US citizens, green-card holders, US resident aliens under the substantial presence test, and US-formed entities including LLCs, corporations, partnerships and most trusts. The threshold is aggregate, not per-account. Five accounts holding $3,000 each on the same day triggers a filing obligation. Non-US persons with no US tax nexus do not file an FBAR.

Do I need to file an FBAR if my accounts are under $10,000?

Only if the combined balance of all your foreign accounts stayed below $10,000 for every single day of the year. The test is the highest aggregate balance at any point during the calendar year, not the year-end balance. If you had $4,000 in a French account and $7,000 in a Singapore account on the same Tuesday, you crossed the threshold and must file. One transient peak is enough. Keep monthly statements for every foreign account so you can prove the highest balance if FinCEN later asks.

What happens if you don't file an FBAR?

Civil penalties for non-willful failure are up to $16,536 per violation for 2024 (adjusted annually for inflation). Willful failure carries the greater of $165,353 or 50% of the account balance, per year. Criminal penalties include up to $500,000 in fines and 10 years in prison when combined with other violations. The IRS runs the Streamlined Filing Compliance Procedures and the Delinquent FBAR Submission Procedures for taxpayers whose failure was non-willful — both can eliminate penalties if you qualify and file before the IRS contacts you.

How does the IRS know if you have a foreign bank account?

FATCA. The Foreign Account Tax Compliance Act, passed in 2010, requires foreign financial institutions to report accounts held by US persons directly to the IRS, or face a 30% withholding tax on US-source payments. Over 110 jurisdictions have signed intergovernmental agreements. Your Wise account, Revolut balance, Swiss bank, Singapore brokerage — all reported. The IRS cross-references those reports against filed FBARs. A foreign bank account that appears in FATCA data but not on an FBAR is a high-probability audit trigger.

When is the FBAR deadline?

April 15 of the year following the calendar year being reported, with an automatic extension to October 15. No form is required to claim the extension — it is granted automatically by FinCEN. The FBAR is filed electronically through the BSA E-Filing System, not with your federal tax return. Filing your Form 1040 does not file your FBAR; they are separate obligations submitted to different agencies (Treasury's Financial Crimes Enforc