The FATCA filing requirement is one of the most misunderstood obligations in international tax. Some readers arrive here because a box was checked on a Form 1099 and they want to know what it means. Others want to know whether their foreign brokerage account triggers a US filing. A third group are not US persons at all and want to understand why their European or Singaporean bank keeps asking about American ties.

Bright!Tax — US expat tax filings (FBAR + FATCA + FEIE specialists)

This article covers all three. It explains what FATCA actually requires, who has to file Form 8938, how thresholds work by filing status and residency, what is exempt, how FATCA differs from FBAR, and what the "FATCA filing requirement" box on a 1099 actually signals. It is written for individuals. It is not tax advice.

What the FATCA filing requirement is

The Foreign Account Tax Compliance Act (FATCA) was enacted in 2010 as part of the HIRE Act. It does two separate things, and conflating them is the source of most confusion.

First, FATCA requires foreign financial institutions (FFIs) — banks, brokers, certain insurers, certain funds — to identify accounts held by US persons and report them to the IRS, either directly or through their local tax authority under an intergovernmental agreement (IGA). This is the chapter 4 reporting regime.

Second, FATCA requires certain US taxpayers to report their specified foreign financial assets to the IRS on Form 8938, Statement of Specified Foreign Financial Assets, attached to their annual income-tax return. This is the individual filing requirement most people mean when they search "FATCA filing requirement."

The IRS Summary of FATCA Reporting for US Taxpayers sets out both sides. The statutory basis for Form 8938 is Internal Revenue Code §6038D.

Form 8938 is not a tax. It is an information return. It carries its own penalties — starting at $10,000 for failure to file, rising to $50,000 for continued failure after IRS notice, plus a 40% accuracy-related penalty on understatements attributable to undisclosed foreign assets (IRC §6038D(d); IRC §6662(j)).

Who this applies to — by nationality and residency

Before the thresholds, decide which reader you are. The rules diverge sharply.

US persons

US citizens, US resident aliens (green-card holders and those meeting the substantial presence test), and certain non-resident aliens who elect joint filing with a US-citizen spouse are specified individuals under Treas. Reg. §1.6038D-1. If you fall in this group and your specified foreign financial assets exceed the threshold for your filing status and tax home, you file Form 8938.

US citizenship is the trigger that travels. Moving to Lisbon does not switch this off. The thresholds get more generous when you live abroad — they do not disappear.

EU freelancers and digital nomads

If you are an EU citizen with no US passport, no green card, and you do not meet the US substantial presence test, you have no Form 8938 obligation. FATCA still affects you indirectly: your bank will ask you to confirm your US status on a self-certification form, often combined with the OECD Common Reporting Standard (CRS) form. The OECD CRS portal governs the parallel, broader exchange-of-information regime that covers EU and most non-US jurisdictions.

Your own reporting obligations live in your country of tax residence. Most EU states require disclosure of foreign accounts and assets — for example, Spain's Modelo 720 (note: the original penalty regime was struck down by the CJEU in Case C-788/19, and a softened version applies). France requires reporting on Form 3916.

Non-US, non-EU readers

If you are a tax resident of, say, the UAE, Singapore, or Paraguay, with no US ties, FATCA is something your bank deals with on your behalf via self-certification. You sign a W-8BEN or equivalent. You do not file Form 8938. Your home jurisdiction may impose its own reporting; many territorial-tax jurisdictions do not.

If you hold any US passport, any green card (even an expired one — green cards remain effective for tax purposes until formally surrendered with Form I-407 and, often, Form 8854), or you were born in the US, treat yourself as a US person until a cross-border tax adviser confirms otherwise.

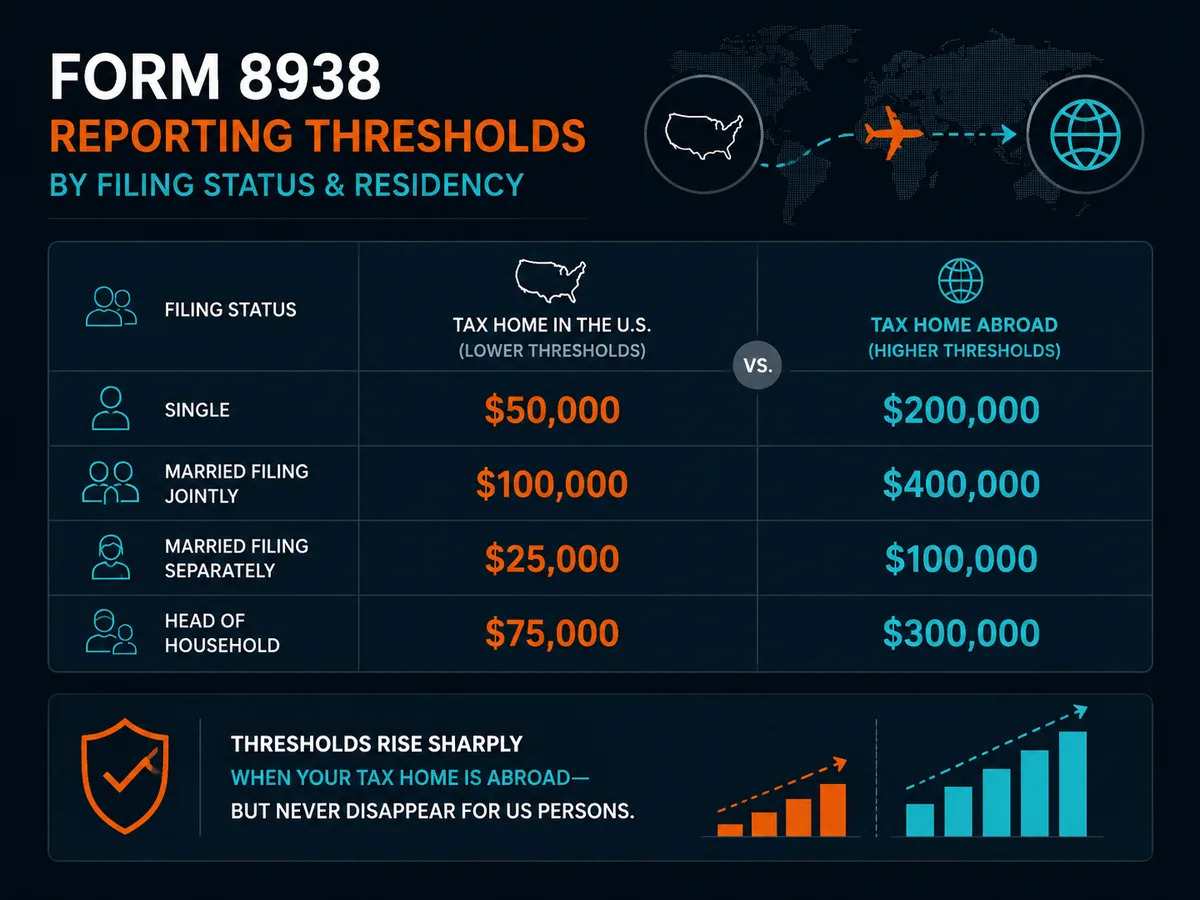

Reporting thresholds for Form 8938

Form 8938 thresholds depend on filing status and whether your tax home is inside or outside the United States. They are set out in Treas. Reg. §1.6038D-2 and the Form 8938 instructions.

| Filing status | Tax home in US — year-end | Tax home in US — any time in year | Tax home abroad — year-end | Tax home abroad — any time in year |

|---|---|---|---|---|

| Single / MFS | $50,000 | $75,000 | $200,000 | $300,000 |

| Married filing jointly | $100,000 | $150,000 | $400,000 | $600,000 |

You meet the threshold — and must file — if either the year-end value or the highest in-year value crosses the relevant number. Aggregate across all specified foreign financial assets; you cannot net losing positions against gainers.

"Tax home abroad" generally tracks the foreign earned income exclusion tests in IRC §911 — you are a bona fide resident of a foreign country for an uninterrupted period including the full tax year, or you are physically present in a foreign country for at least 330 full days during any consecutive 12 months.

What counts as a specified foreign financial asset

The defined term is broader than "foreign bank account." Per Treas. Reg. §1.6038D-3, it covers:

- Financial accounts maintained by a foreign financial institution (foreign banks, foreign brokerages, certain foreign mutual funds and insurance products with cash value).

- Stocks or securities issued by a non-US person, held outside a financial account.

- Any interest in a foreign entity (foreign corporations, partnerships, trusts).

- Any financial instrument or contract with a non-US issuer or counterparty, held for investment.

A US brokerage account that holds foreign stocks is not a specified foreign financial asset, because the account is at a US institution. Foreign stock held directly — in your name on the issuer's register — is reportable.

What is exempt from FATCA reporting

Form 8938 deliberately excludes several categories (IRS guidance on assets to report):

- Directly held real estate. A flat in Berlin you own personally is not reportable. An interest in a foreign company that owns the flat is.

- Directly held tangible personal property. Art, cars, gold bars in a personal safe.

- Foreign currency held directly (not in an account).

- US-payer financial accounts, including US brokerages holding foreign assets.

- Certain accounts held by US military banking facilities.

- Beneficial interests in foreign trusts and foreign estates you do not know about (the regulation specifically protects beneficiaries unaware of their interest).

If an asset is reported on Form 3520 (foreign trusts), 5471 (foreign corporations), 8621 (PFICs), or 8865 (foreign partnerships), you do not duplicate the detail on Form 8938, but you must still note its existence in Part IV.

Note that exemption from Form 8938 does not exempt you from FBAR, the income-tax treatment of the underlying income, or other information returns. PFIC rules (IRC §1291 et seq.) in particular can turn a foreign mutual fund into a tax disaster regardless of size.

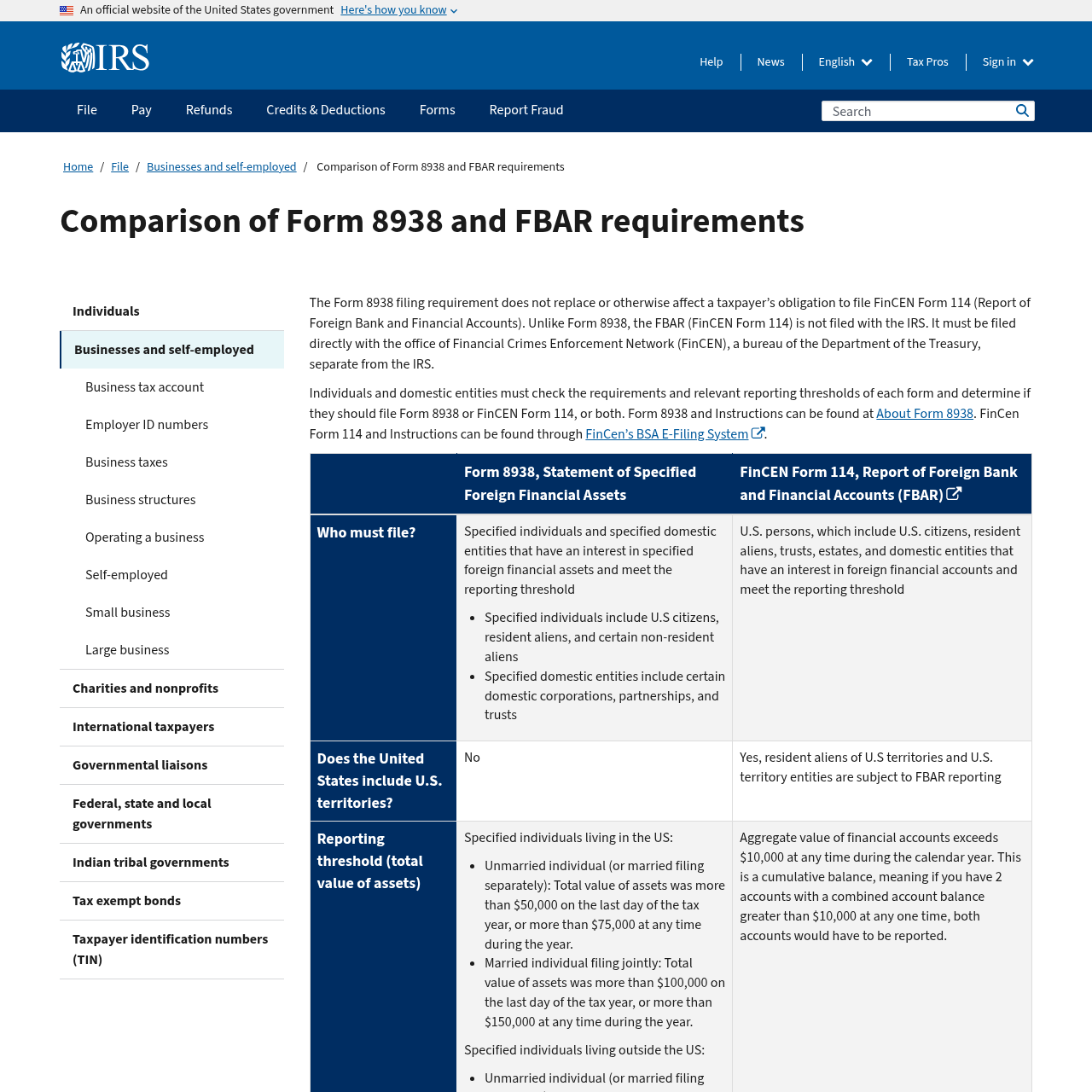

FATCA vs FBAR: two separate filings

Most US persons abroad file both. They are not interchangeable.

| Form 8938 (FATCA) | FBAR (FinCEN 114) | |

|---|---|---|

| Authority | IRS — IRC §6038D | FinCEN — 31 USC §5314 |

| Where filed | Attached to Form 1040 | Separate e-file via BSA E-Filing System |

| Threshold | $50,000+ depending on status | $10,000 aggregate any time in year |

| What's covered | Specified foreign financial assets (broader) | Foreign financial accounts (narrower) |

| Direct foreign stock | Reportable | Generally not — needs an account |

| Foreign real estate held directly | Not reportable | Not reportable |

| Failure penalty | $10,000 minimum; up to $50,000 + 40% accuracy | $10,000+ non-willful; greater of $100,000 or 50% of account for willful |

A side-by-side from the IRS comparison page is the authoritative reference.

The "FATCA filing requirement" box on a 1099

This is what brings most accidental readers here. Form 1099-B (Box 11), and the equivalent indicator on certain other 1099s, exists so that brokers can flag that they are reporting the account to satisfy their own chapter 4 obligations.

A checked box means: the payer thinks this account is within the FATCA reporting net at the institutional level.

It does not mean: you personally must file Form 8938. It does not mean: you have done anything wrong. It does not mean: the IRS expects a specific form from you because of the box.

If the box is checked, treat it as a prompt to do the Form 8938 threshold analysis yourself. If your specified foreign financial assets cross the relevant threshold, file. If they do not, you do not file Form 8938 based on the box alone. The IRS confirms this framing in the 1099-B instructions.

If the box is not checked and you hold significant foreign assets through that broker, that is also not the final word. The broker may be a US broker with no FATCA filing obligation of its own, or the account may sit below the institution's threshold. Apply your own §6038D analysis.

Costs, timeline, and what filing actually involves

There is no government fee to file Form 8938 or FBAR. The cost is professional preparation time, and it scales with how many accounts and assets you have.

| Item | Typical range | Notes |

|---|---|---|

| Self-prepared Form 8938 add-on in tax software | $0–$50 | Most consumer software supports it; complex assets often need overrides |

| Cross-border CPA — Form 8938 add-on | $150–$500 | Bundled with 1040; per-account complexity drives the upper end |

| Cross-border CPA — FBAR | $100–$300 | Often bundled |

| Streamlined Filing Compliance Procedures (catch-up) | $2,500–$10,000+ | Three years of returns + six years of FBARs; varies by firm and complexity [source: TODO — survey of US expat tax firm pricing pages] |

| Failure-to-file penalty (Form 8938) | $10,000 minimum | Up to $50,000 with continued non-filing after IRS notice |

| Non-willful FBAR penalty | $10,000+ per violation | Bittner v. United States (598 US 85, 2023) capped this at per-report, not per-account |

Form 8938 follows the Form 1040 deadline — 15 April, automatic two-month extension to 15 June for taxpayers abroad, further extension to 15 October by request. FBAR is due 15 April with an automatic extension to 15 October (FinCEN notice).

Common mistakes

Treating the 1099 box as the rule. As covered above, the box describes the payer's filing, not yours.

Filing FBAR but not Form 8938. They have different thresholds and different definitions. Aggregate foreign accounts of $60,000 with a tax home in the US triggers both. With a tax home abroad it triggers only FBAR.

Forgetting foreign pensions. Most foreign employer pensions and many foreign government-administered pensions are specified foreign financial assets. Australian superannuation, UK SIPPs, German Riester accounts — all generally reportable, regardless of whether you can currently access the funds.

Ignoring foreign mutual funds and ETFs. These are PFICs in nearly all cases. Form 8621 applies, with painful default tax treatment under IRC §1291. The Form 8938 reporting is the gentler of the two problems.

Assuming the green card no longer counts. A green card remains effective for US tax purposes until formally surrendered. Letting it lapse for immigration purposes does not end US tax residency. See IRS guidance on expatriation.

Assuming offshore structures help US persons. They do not, on the FATCA reporting axis. A US person owning a foreign corporation files Form 5471, often Form 8938, often FBAR for the corporation's accounts where the US person has signature authority, and faces GILTI and Subpart F on the entity's income. Offshore incorporation is a substance and timing tool for US persons — never an escape from reporting. The only way out of US worldwide taxation is formal renunciation, which carries its own exit-tax regime under IRC §877A.

Filing for the wrong year because of currency conversion. Use the Treasury year-end rates for Form 8938 valuations. Use the same for FBAR.

When to consult a qualified professional

The honest answer is: before you do anything that would change your filing posture, and certainly before you file a catch-up under the Streamlined Procedures. Specifically:

- You have just discovered you should have been filing Form 8938 or FBAR. Do not file ordinary back-returns without advice — the Streamlined process exists to handle this and is generally preferable to a quiet correction.

- You are considering a foreign company, foreign trust, or foreign pension contribution.

- You are an "accidental American" — born in the US but living abroad as another country's citizen — and your bank has flagged you.

- You are weighing renunciation, expatriation, or formally surrendering a green card.

- You are EU-resident and uncertain whether your home-state foreign-asset reporting overlaps with FATCA self-certifications.

Look for someone qualified in both jurisdictions — US-side, a CPA or enrolled agent with international experience; in your country of residence, a tax adviser familiar with that country's treatment of US-source income and the relevant treaty. Soveraine's editorial policy explains why we do not rank tax-prep firms here: the right adviser depends on your facts in a way no ranking can reflect.

Ready to act on this?

Bright!Tax — US expat tax filings (FBAR + FATCA + FEIE specialists). Soveraine readers go to the front of the line through our partner link, and you fund independent editorial in the process.

FAQ

Who is required to file FATCA?

FATCA filing on Form 8938 is required of specified persons — US citizens, US resident aliens, and certain non-resident aliens who elect to be treated as residents — whose specified foreign financial assets exceed the reporting threshold for their filing status and residency. Thresholds start at $50,000 on the last day of the year for single filers living in the US and rise to $400,000 for married filers living abroad. Certain domestic entities formed or used to hold specified foreign financial assets must also file. Non-US persons with no US tax filing obligation do not file Form 8938.

How do I know if my FATCA filing is required?

Add up the year-end and highest in-year values of all your specified foreign financial assets — foreign bank accounts, foreign brokerage accounts, foreign-issued stocks and bonds held outside a US custodian, interests in foreign entities, and certain foreign pensions. Compare those totals against the Form 8938 thresholds for your filing status and whether you live in or outside the US. If either the year-end or the in-year peak exceeds your threshold, you must attach Form 8938 to your Form 1040. FBAR (FinCEN Form 114) is a separate test at $10,000 aggregate.

What is exempt from FATCA reporting?

Form 8938 does not require you to report assets held in a US financial institution, including a US brokerage holding foreign stocks. Directly held real estate is not reportable, though an interest in a foreign entity that owns real estate is. Personal property — art, cars, jewellery — held directly is not reportable. Social Security-equivalent foreign government pensions you cannot control are generally reportable as foreign pensions, but US Social Security is not. Accounts reported on other forms (3520, 5471, 8621, 8865) avoid duplicate detail but must still be referenced on Form 8938.

What is the minimum amount to report to FATCA?

The lowest Form 8938 threshold is $50,000 in specified foreign financial assets on the last day of the tax year, or $75,000 at any point during the year, for a single filer or married-filing-separately filer living in the United States. Thresholds rise for joint filers and for taxpayers whose tax home is abroad — up to $400,000 year-end / $600,000 in-year for joint filers living abroad. FBAR is separate and stricter: any US person with foreign accounts aggregating over $10,000 at any moment during the year must file FinCEN Form 114.

What does the FATCA filing requirement box on a 1099 mean?

Box 11 on Form 1099-B and the equivalent box on certain other 1099s indicates that the payer — usually a broker — is reporting the account to the IRS