Most "best expat health insurance" articles on the first page of Google are affiliate-ranked junk. They list the same five products in the same order, none of the writers have read a policy wording, and the recommendation rarely distinguishes between a 28-year-old nomad doing three months in Lisbon and a 52-year-old expat moving a family to Singapore. The right policy for those two readers differs by an order of magnitude in cost and coverage. This guide walks through the actual decision: what international expat health insurance is, who needs which product, what the leading plans cost and exclude, and where the residency-visa rules force your hand.

SafetyWing — Nomad insurance with recurring 364-day cookie

What "expat health insurance" actually means

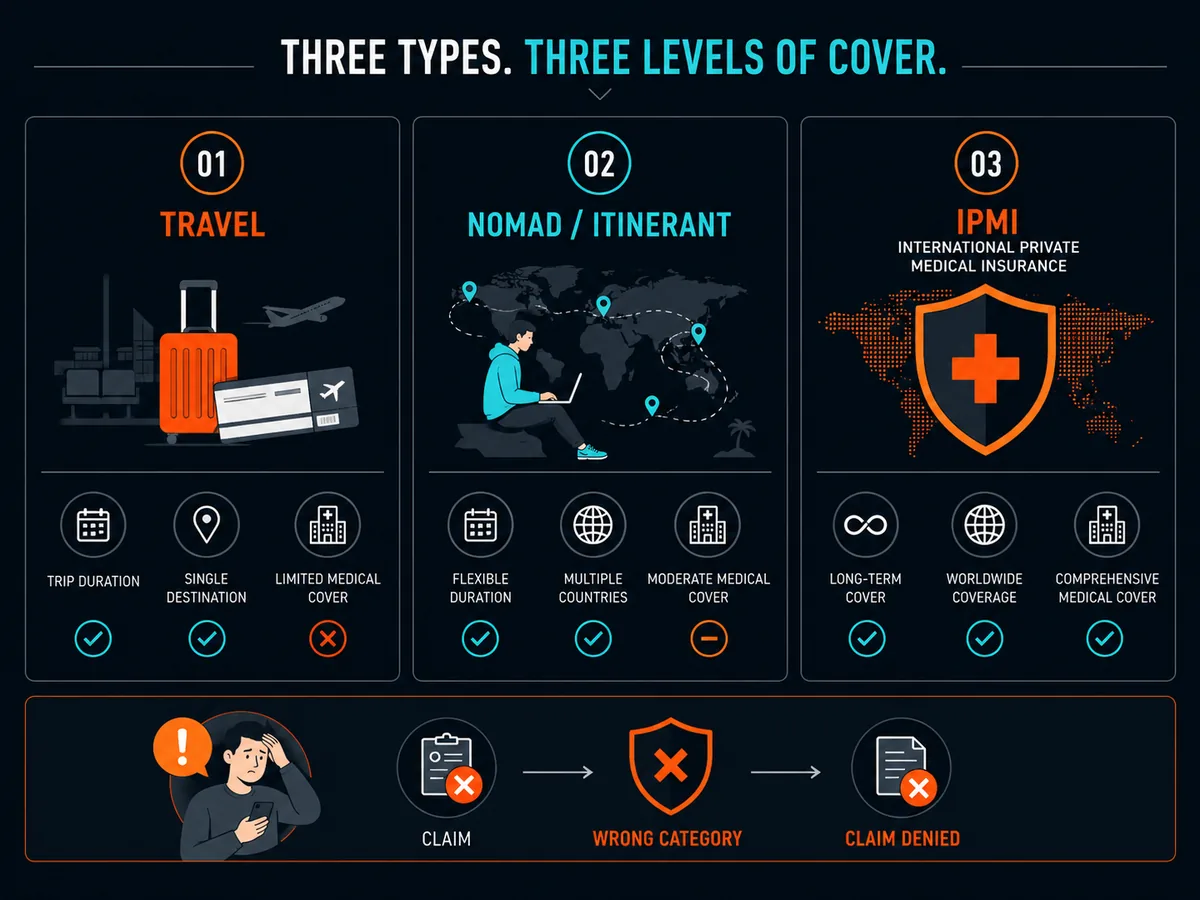

The phrase covers three different product categories that most blog posts merge into one. The differences matter because the wrong category will fail you at the moment you need to use it.

Travel insurance is a short, defined-trip product. World Nomads, Allianz Travel, AXA Schengen, Heymondo. It covers acute medical events and trip-related risks (cancellation, baggage, evacuation) for a fixed period and ends on the return date. It assumes you have a home you go back to and a primary health system there. It will not cover routine care, pre-existing chronic conditions, planned procedures or anything that looks like ongoing health management. It is the wrong product for living abroad.

Nomad and itinerant insurance is a hybrid. SafetyWing Nomad Insurance, Genki Explorer, Insured Nomads World Explorer. Sold as a monthly subscription, structured legally as travel-medical, but designed for people who do not have a fixed end date. It bridges short-trip cover and full health insurance, with the trade-off that medical limits are capped (typically USD 100,000–250,000 lifetime or per condition), pre-existing conditions are excluded, and home-country cover is limited.

International private medical insurance (IPMI) is the real expat health product. Cigna Global Health Options, SafetyWing Remote Health, Genki Native, Allianz Care, Aetna International, Bupa Global. Annual, renewable, guaranteed-renewable in most cases, with very high annual limits (USD 1.5m to unlimited depending on tier), modular cover (inpatient + outpatient + maternity + dental + vision), and pre-existing-condition handling via moratorium or medical underwriting. This is what satisfies residency visa requirements and what insures a family that is actually settling abroad.

Conflating the three is the single biggest error in this category. The rest of this article keeps them separate.

Who this applies to — read this first

US persons

US Medicare does not follow you abroad. The program's overseas coverage is narrow and intermittent, and there is no general benefit for US citizens or green-card holders living outside the United States (Medicare.gov: Travel). Medigap plans C, D, F, G, M and N include foreign emergency cover with an 80% reimbursement after a USD 250 deductible and a USD 50,000 lifetime cap — useful for emergencies on a short trip, useless for living abroad.

The Affordable Care Act individual mandate was reduced to a USD 0 federal penalty by the Tax Cuts and Jobs Act of 2017, but the statutory exemption for US citizens who are bona-fide residents of a foreign country or who meet the physical presence test under IRC §5000A(f)(4)(B) still exists and matters in states that maintain their own mandates (California, Massachusetts, New Jersey, Rhode Island, DC, Vermont). Our bona fide resident guide covers the test in detail.

The practical implication: as a US person abroad you need to buy international health insurance yourself. SafetyWing, Cigna Global, GeoBlue and Allianz Care all underwrite for US persons. Pricing is higher than for non-US residents because US-quality cover is expensive, but coverage anywhere outside the US is comparable.

EU residents

EU citizens who remain tax resident in their home country keep the European Health Insurance Card (EHIC), which covers state-provided medically necessary care in other EU/EEA states and Switzerland on the same terms as residents of the visited country (European Commission: EHIC). UK residents lost EHIC after Brexit and use the Global Health Insurance Card (GHIC), which provides similar EU/EEA cover (NHS: GHIC).

Both cards disappear when you deregister at home and become tax resident in a non-EU country, or in some configurations when you move to a different EU country and register there. At that point, private international health insurance becomes necessary — often legally, because the residency permit requires it. Most EU countries (Spain, Portugal, Italy, France, Germany) require new residents to enrol in either the public health system or a qualifying private plan within weeks of arrival.

For EU residents going outside the EU, expect monthly costs of EUR 100–300 for individual cover on SafetyWing or Genki, and EUR 300+ on Cigna Global for comparable IPMI tiers.

Non-US, non-EU readers

If you are not a US person and not an EU/UK resident, your situation depends entirely on bilateral health agreements between your home country and your host country. Most Commonwealth countries have reciprocal arrangements (Australia ↔ UK, NZ ↔ UK, parts of the GCC ↔ each other). Most do not extend beyond emergencies.

The practical reality is that you almost certainly need private international health insurance to obtain a residence visa in any country worth moving to. The four products discussed below all sell to non-US, non-EU residents. Pricing is generally cheaper than the US-inclusive version of the same plan.

SafetyWing Nomad Insurance

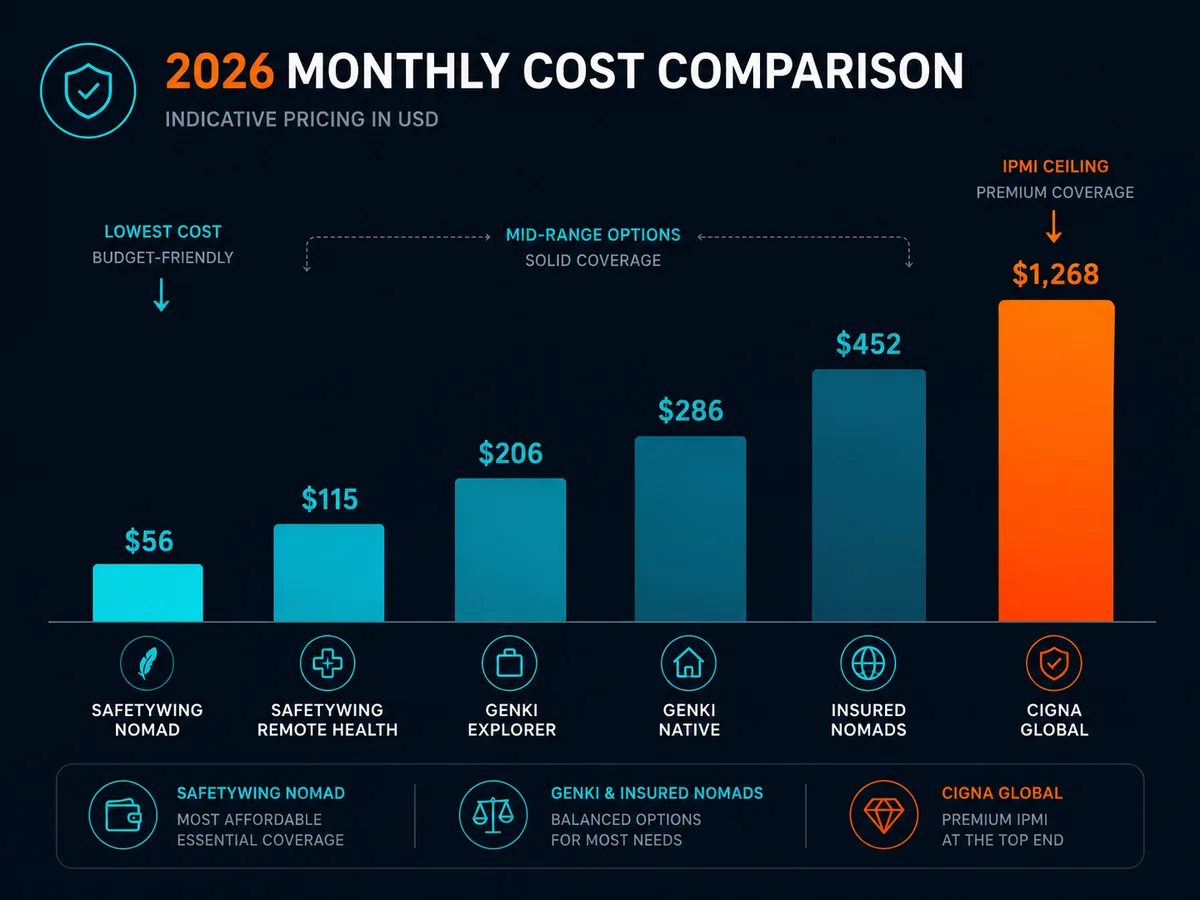

The cheapest and most-cited product in the category. SafetyWing Nomad Insurance is a travel-medical subscription that auto-renews every 28 days, underwritten by Tokio Marine HCC. Indicative 2026 pricing starts around USD 56 per 4 weeks for ages 10–39 on the worldwide-excluding-US plan, with higher rates for older travellers and for plans including US coverage (SafetyWing Nomad Insurance).

Strengths. Cheap, simple, no medical questionnaire, no pre-approval. Covers COVID treatment as a normal illness. Includes emergency dental, evacuation and a small trip-interruption benefit. Schengen-compliant certificate issued on request. Easy to start, easy to cancel.

Weaknesses. USD 250,000 lifetime medical maximum. Pre-existing conditions excluded outright. US cover restricted to 15 days per 90-day period for non-US residents, with stricter limits for US residents. Trip-interruption benefit capped at USD 5,000. Mental health under-covered. Maternity available only as a separate add-on after 10 months. Not a substitute for IPMI if you have any chronic condition, are over 40, or are settling somewhere that requires comprehensive insurance.

Best for. Healthy under-40s on the move with no chronic conditions, using insurance as accident-and-acute-illness cover. Not for anyone settling in one country long-term.

SafetyWing Remote Health

SafetyWing's full international health insurance — a different product from Nomad Insurance despite the shared brand. Remote Health is annual IPMI, renewable, with indicative 2026 pricing from about USD 147 per month for under-40s on a worldwide-excluding-US plan and considerably more with US cover (SafetyWing Remote Health).

Strengths. Comprehensive cover including inpatient, outpatient (on higher tier), maternity, mental health, dental and vision. Pre-existing conditions covered after a 12-month moratorium with no symptoms or treatment in between. Annual maximum of USD 1.5m or more depending on tier. Available globally including for US persons. Direct billing with major international hospital networks. Designed to satisfy residency visa requirements in most jurisdictions.

Weaknesses. Significantly more expensive than Nomad Insurance. Newer product with a shorter claims track record than Cigna or Bupa. Some markets show fewer in-network providers than the established IPMI brands.

Best for. Settled expats, nomads transitioning to one-country residency, families wanting a true health policy without paying Cigna prices, and anyone using a residency visa that demands comprehensive insurance.

Cigna Global Health Options

The default international private medical insurance for higher-net-worth expats, retirees and families. Cigna Global Health Options is a modular IPMI policy with three core tiers (Silver, Gold, Platinum) and optional modules for outpatient, medication, maternity, vision, dental and US cover (Cigna Global). Indicative 2026 pricing runs USD 250–600 per month for an individual depending on age, area of cover and modules; family and US-inclusive plans run much higher.

Strengths. The largest international hospital network in the category. Annual maximum from USD 1m up to unlimited depending on tier. Full US coverage available as a module — rare and valuable. Maternity, dental, vision and outpatient available as standalone modules so you only pay for what you need. Strong claims-handling reputation, direct billing globally, multilingual customer service. Genuine IPMI underwriting with medical underwriting available so declared pre-existing conditions can be covered (often with a surcharge or endorsement) rather than blanket-excluded.

Weaknesses. Expensive. Plans renew annually with age-band price increases that can be significant after 50 and again after 60. Some buyers report that the cheapest "Silver" tier is too thin to be useful — Gold is the realistic floor. US cover is the most expensive module and roughly doubles the premium.

Best for. Families settling abroad, expats over 40, anyone with declared pre-existing conditions, HNW readers wanting US-quality cover anywhere in the world, and people whose residency visa or employment contract specifies a high minimum coverage level.

Genki Native and Genki Explorer

Genki is the EU-flavoured alternative, underwritten in Germany by Hanse Merkur and administered by DR-WALTER (Genki). It sells two products that mirror the SafetyWing structure: Genki Explorer is travel-medical for itinerant readers; Genki Native is full IPMI for settled expats.

Indicative 2026 pricing for Genki Explorer starts around EUR 42 per month for under-40s on a worldwide plan with limited US cover. Genki Native starts around EUR 169 per month for under-40s on a worldwide-excluding-US plan and runs higher with US cover or comprehensive add-ons.

Strengths of Explorer. Cheap, euro-denominated, German underwriting (Hanse Merkur is a major established carrier), explicit support for European nomads with home-country re-entry cover, no exclusion for activities most adventure travellers would do.

Strengths of Native. Annual cover up to EUR 1m+ depending on tier, pre-existing conditions covered after 8–12 months on the plan, maternity available, Schengen and residency-visa compliant, single carrier with strong German consumer protection.

Weaknesses. Smaller English-language customer community than SafetyWing; fewer reviews and forum threads. Direct billing network is solid in Europe and South-East Asia, thinner in the Americas. US cover is limited even on Native — Cigna remains the better option if you need full US cover.

Best for. European nomads, EU residents moving outside the EU, anyone who prefers euro billing and German regulatory oversight, and readers who plan to retain some ties to the EU public system.

Insured Nomads World Explorer

Insured Nomads positions itself between SafetyWing and Cigna — premium travel-medical with added benefits. Indicative 2026 pricing starts around USD 89 per month for the World Explorer plan (Insured Nomads).

Strengths. Stronger COVID and mental-health cover than most travel-medical plans, telemedicine included, evacuation built in, cyber-security and identity-theft cover bundled, quarterly renewal structure that smooths cash flow. Underwritten by reputable carriers (Lloyd's syndicates and others depending on residence). Schengen-compliant certificates.

Weaknesses. Still travel-medical at heart — pre-existing conditions excluded, medical limits below true IPMI. Smaller brand recognition than SafetyWing or Cigna. Limited family-cover options compared to Cigna.

Best for. Nomads who want more than SafetyWing's bare-bones cover but do not yet need full IPMI; readers who value mental health and telemedicine inclusion.

Comparison table

Indicative 2026 monthly pricing for a healthy 35-year-old non-smoker, individual plan, worldwide-excluding-US area of cover. Prices change frequently — quote on each insurer's site with your real age and itinerary before buying.

| Product | Monthly cost | US cover | Pre-existing | Maternity | Maximum cover | Best for |

|---|---|---|---|---|---|---|

| SafetyWing Nomad Insurance | from USD 56 | 15 days / 90 days, capped | Excluded | Add-on after 10 months | USD 250k lifetime | Healthy nomads under 40 |

| SafetyWing Remote Health | from USD 147 | Module available | After 12-month moratorium | Included on higher tiers | USD 1.5m+ annual | Settled expats, families |

| Genki Explorer | from EUR 42 | Limited | Excluded | Excluded | Up to EUR 1m per case | EU-based nomads |

| Genki Native | from EUR 169 | Limited (add-on) | After 8–12 months | Included on higher tiers | EUR 1m+ annual | EU-residents moving abroad |

| Cigna Global Silver/Gold | USD 250–600 | Optional module | Underwritten, often covered | Optional module | USD 1m – unlimited | HNW, families, over-40 expats |

| Insured Nomads World Explorer | from USD 89 | Included | Excluded | Limited | USD 1m | Mid-tier nomads wanting more than SafetyWing |

Source: insurer plan pages cited above. [source: TODO — capture live 2026 quotes from each provider for footnote]

The visa-residency interaction

This is where the wrong choice of product costs you a visa application.

Schengen short-stay requires minimum EUR 30,000 medical and repatriation cover valid in all Schengen states (European Commission: Schengen visa). Most nomad and IPMI products meet this; some travel-medical products do not.

Portugal D7 and D8 visas require comprehensive health insurance with coverage in Portugal, typically minimum EUR 30,000 or proof of enrolment in the Serviço Nacional de Saúde. Consulates have rejected travel-medical-only plans; SafetyWing Remote Health, Genki Native, Cigna and Allianz Care are routinely accepted.

Spain Non-Lucrative Visa requires private health insurance with full coverage in Spain, no copayments, no waiting periods, and the carrier must have a Spanish operating licence. This rules out most travel-medical plans. Cigna Spain, Sanitas, DKV and Adeslas are the typical choices; international plans qualify if they meet the conditions.

Italy Elective Residence Visa requires private insurance with EUR 30,000+ medical cover valid in Italy. Many international plans qualify.

France Long-Stay Visiteur requires comprehensive private health insurance for the first year, after which you enrol in the PUMa public system. International plans typically accepted.

UAE Golden Visa, Singapore EP, US E-2, etc. all impose insurance requirements — sometimes via employer cover, sometimes private. Read the specific visa's terms; do not assume a nomad plan qualifies.

The general rule: if the visa requires "comprehensive private health insurance" without qualifying language, you need a real IPMI policy (Cigna, SafetyWing Remote Health, Genki Native, Allianz Care). If it requires "minimum EUR 30,000 medical cover," travel-medical plans are often accepted but read each consulate's published list.

The traps

Pre-existing conditions. Travel-medical plans exclude them outright. IPMI plans either exclude under moratorium (no cover for 12+ months, then covered if no symptoms in between) or accept under full medical underwriting (declared conditions may be covered with surcharge, endorsed out, or accepted). Disclose everything. An undeclared history found in your records at claim time is the most common reason claims fail across this entire category.

Maternity. Excluded on travel-medical plans. On IPMI, available only after a 10–12 month waiting period — you cannot buy cover when already pregnant. Plan the policy purchase well before trying to conceive.

US coverage is the most expensive surcharge. Adding US cover to any plan typically doubles or triples the premium. If you genuinely live outside the US, the calculus often favours a worldwide-excluding-US plan plus a separate domestic policy on US trips. If you split time, Cigna Global with US module is usually the cleanest answer.

Mental health. Under-covered on every travel-medical plan and on the lower tiers of most IPMI plans. If mental health matters to you, check the annual limit, the inpatient vs outpatient distinction, and the network of in-network providers in your host country specifically.

Evacuation and repatriation. Built in on SafetyWing, Genki and Insured Nomads. On Cigna and similar IPMI, often a separate module — buy it. The cost of a private medical evacuation from a remote location is six figures.

Direct billing networks. All these insurers will pay claims; not all of them have direct-billing arrangements with the specific hospital you want to use. Check the network in your host country before buying. The difference between handing over a card and paying USD 30,000 up front waiting for reimbursement is substantial.

Age-band increases. Premiums rise sharply at 40, 50, 60 and 65. A USD 250 plan at 35 can be USD 800 at 60 for identical cover. Lock in early; understand the renewal curve.

Data, privacy and the international medical record

One under-discussed dimension: when you buy international health insurance, your medical data crosses borders. HIPAA governs US-based health-data handling but does not extend to non-US insurers. GDPR governs EU-resident data and binds Genki, Cigna's EU entity and other European-underwritten plans. Most international insurers publish a privacy notice describing how data is shared between underwriters, reinsurers and direct-billing hospitals.

Two practical implications. First, declaring conditions in a country with weaker privacy protections may surface them later in unrelated contexts (other insurers, employer health screenings). Second, when you change insurer, you typically authorise the new insurer to obtain records from the old — this is how undeclared histories surface. The right strategy is to disclose at first purchase and stay with one insurer through the moratorium period, rather than switching plans hoping the new underwriter does not find out.

A note on the recommendations above

Soveraine has affiliate relationships with SafetyWing, Cigna, Genki and Insured Nomads. Commissions on these products vary; we have ranked them in this article by editorial fit for the typical reader, not by commission rate. For low-cost nomadic cover under 40 with no chronic conditions, SafetyWing Nomad Insurance is structurally the right product. For settled expats, families, or anyone with a residency visa requiring comprehensive cover, Cigna Global is usually the cleanest IPMI, with SafetyWing Remote Health and Genki Native as cheaper alternatives that meet most residency requirements. If a materially better policy exists for your specific situation, buy it. Our editorial policy and affiliate disclosure explain how we work and how we are funded.

For the related products in our coverage map, see our nomads travel insurance guide and, for US tax aspects of life abroad, our bona fide resident guide.## FAQ

What is the difference between travel insurance and expat health insurance

Travel insurance is a short-term, defined-trip product designed to cover sudden accidents and acute illness while you are away from home. It does not cover routine care, chronic conditions or anything resembling primary medical cover, and it ends on the return date. International expat health insurance — also called international private medical insurance or IPMI — is an annual, renewable health policy designed to be your primary medical cover while you live abroad. It includes inpatient and outpatient care, maternity, mental health and (depending on tier) dental and vision, and is structured to satisfy residency visas that require proof of comprehensive insurance. Cigna Global, SafetyWing Remote Health, Genki Native and Allianz Care are IPMI. SafetyWing Nomad Insurance and Insured Nomads World Explorer are travel-medical hybrids that sit between the two.

How much does international expat health insurance cost

For a healthy 35-year-old non-smoker in 2026, travel-medical nomad plans start around USD 56 per month (SafetyWing Nomad Insurance worldwide excluding the US) or EUR 42 per month (Genki Explorer). Full international health plans cost considerably more: SafetyWing Remote Health from about USD 147 per month, Genki Native around EUR 169 per month for global excluding US cover, and Cigna Global Health Options between USD 250 and USD 600 per month depending on age, area of cover and modules selected. Adding US coverage typically doubles or triples the premium on any plan. Family cover, maternity and pre-existing-condition riders increase prices further.

Cigna Global vs SafetyWing — which should I pick

They are different products for different readers. SafetyWing Nomad Insurance is a travel-medical subscription for people on the move with a USD 250,000 lifetime medical cap and limited US cover; it is cheap and flexible but not real health insurance. SafetyWing Remote Health is a true international health policy that competes more directly with Cigna. Cigna Global Health Options is the established IPMI choice for settled expats, families and higher-net-worth readers: modular plans, full US cover available, very high annual limits, and a global hospital network. If you are nomadic and under 40 with no chronic conditions, SafetyWing wins on price. If you are settling abroad with a family, need maternity or want US-quality cover anywhere, Cigna is the structural fit.

Genki vs SafetyWing — what is the real difference

Both offer a cheaper travel-medical product and a fuller international health product. Genki Explorer (EUR 42 per month upward for under-40s) is the closest equivalent to SafetyWing Nomad Insurance (USD 56 per month upward) and is popular with European nomads because it is priced in euros and underwritten in Germany by DR-WALTER and Hanse Merkur. Genki Native is the IPMI tier, roughly comparable to SafetyWing Remote Health but with German underwriting and EU-flavoured wording. Practical decision: if you bank in euros, file taxes in the EU, or want a policy with German consumer protection, Genki is the better fit. If you want the largest English-language nomad community, US-dollar billing and the longest-running nomad brand, SafetyWing leads.

Will my US Medicare or EU public health card cover me abroad

Largely no. US Medicare provides almost no cover outside the United States; the program's foreign-coverage exceptions are narrow and intermittent, and there is no general overseas benefit. Medigap supplemental plans C, D, F, G, M and N include limited foreign emergency cover up to a USD 50,000 lifetime cap, which is not adequate for ongoing expat life. EU residents who remain tax resident in their home country keep the European Health Insurance Card (EHIC), which covers state-provided necessary care in other EU/EEA states and Switzerland — useful for short trips, not for living abroad. UK residents have the Global Health Insurance Card (GHIC), which functions similarly within the EU. Both EHIC and GHIC are lost when you deregister at home and become tax resident elsewhere. After that, you need private international health insurance.

Do residency visas require expat health insurance

Most do, and the standards are getting stricter. Portugal's D7 and D8 visas, Spain's Non-Lucrative Visa, Italy's Elective Residence Visa, France's Visiteur visa and the EU Blue Card all require proof of private health insurance with coverage valid in the host country, usually with a minimum of EUR 30,000. Schengen short-stay visas require EUR 30,000 minimum medical and repatriation cover. Some consulates reject travel insurance and demand a true health policy — SafetyWing Remote Health, Genki Native, Cigna Global and Allianz Care all qualify. SafetyWing Nomad Insurance and other travel-medical products are accepted at some consulates and rejected at others. Always confirm with the specific consulate before applying.

Are pre-existing conditions ever covered

On most travel-medical plans, no — pre-existing conditions are excluded outright. On full international health plans, they are typically subject to a moratorium: SafetyWing Remote Health covers them after 12 continuous months on the plan with no symptoms or treatment in between. Cigna Global uses moratorium underwriting or full medical underwriting depending on plan choice — under full underwriting, declared conditions are either covered (often with a surcharge), excluded by named endorsement, or accepted at standard rates. Disclose everything at application. An undeclared history found in your medical records at claim time is the single most common reason claims are denied across every insurer in this category.

Is SafetyWing Nomad Insurance enough if I live abroad full-time

For most full-time expats, no — and SafetyWing is reasonably clear about this. Nomad Insurance is a travel-medical product capped at USD 250,000 in lifetime medical benefits, with limited US coverage (currently 15 days in the US per 90-day period for non-US residents, capped further for US residents), no real coverage of chronic conditions and only emergency-style dental and maternity add-ons. It is appropriate if you are healthy, under 40, on the move and using it as accident-and-acute-illness insurance rather than primary cover. If you are over 40, have any chronic condition, plan a pregnancy, or need a policy that will satisfy a residency visa requiring comprehensive cover, you need SafetyWing Remote Health, Genki Native, Cigna Global, Allianz Care or equivalent.

Ready to act on this?

SafetyWing — Nomad insurance with recurring 364-day cookie. Soveraine readers go to the front of the line through our partner link, and you fund independent editorial in the process.

Sources

- SafetyWing — Nomad Insurance. https://safetywing.com/nomad-insurance

- SafetyWing — Remote Health. https://safetywing.com/remote-health

- Cigna Global — Health Options. https://www.cignaglobal.com/

- Genki — World Health Insurance. https://genki.world/

- Insured Nomads — World Explorer. https://insurednomads.com/

- European Commission — European Health Insurance Card (EHIC). https://ec.europa.eu/social/main.jsp?catId=559

- NHS — Global Health Insurance Card (GHIC). https://www.nhs.uk/using-the-nhs/healthcare-abroad/apply-for-a-free-uk-global-health-insurance-card-ghic/

- Medicare.gov — Travel and Foreign Coverage. https://www.medicare.gov/coverage/travel

- US Code — IRC §5000A(f)(4)(B), bona-fide-resident exemption from individual mandate. https://www.law.cornell.edu/uscode/text/26/5000A

- World Health Organization — International Health Regulations (2005). https://www.who.int/publications/i/item/9789241580496

- European Commission — Schengen visa policy. https://home-affairs.ec.europa.eu/policies/schengen-borders-and-visa/visa-policy_en