e-Residency is the most-marketed and most-misunderstood product the Estonian government sells. It is a digital ID issued by the Police and Border Guard that lets non-residents form and run an Estonian company online. It is not residency, not a visa, not a tax-residency shortcut, and not a banking solution. This guide covers what e-Residency actually does, what it costs, where the tax traps sit by nationality, and when it is the wrong tool. We will be specific about US persons, EU tax residents, and the rest of the world — because the same product produces very different outcomes depending on the passport you hold.

Companio — Estonia e-Residency formation + accounting

What e-Residency is

e-Residency is a government-issued digital identity launched by Estonia in December 2014. The card and PIN codes let you authenticate, sign documents with a legally binding qualified electronic signature under EU eIDAS regulation, and access Estonian e-government services from anywhere.

What it lets you do, in practice:

- Register an Estonian private limited company (osaühing, or OÜ) fully online.

- Sign contracts and board resolutions with an EU-recognised digital signature.

- File Estonian tax returns and annual reports remotely.

- Open accounts with most EU fintechs (Wise, Revolut Business, Payoneer) using the Estonian company.

What it does not do:

- Grant any right to enter, live, or work in Estonia or the Schengen area.

- Confer Estonian tax residency on you personally.

- Open the door to traditional Estonian high-street bank accounts in most cases.

- Shield you from your home country's tax rules.

If you only remember one line: e-Residency is a key to Estonia's digital public services, not a passport, not a visa, not a tax structure.

Who this applies to — by nationality

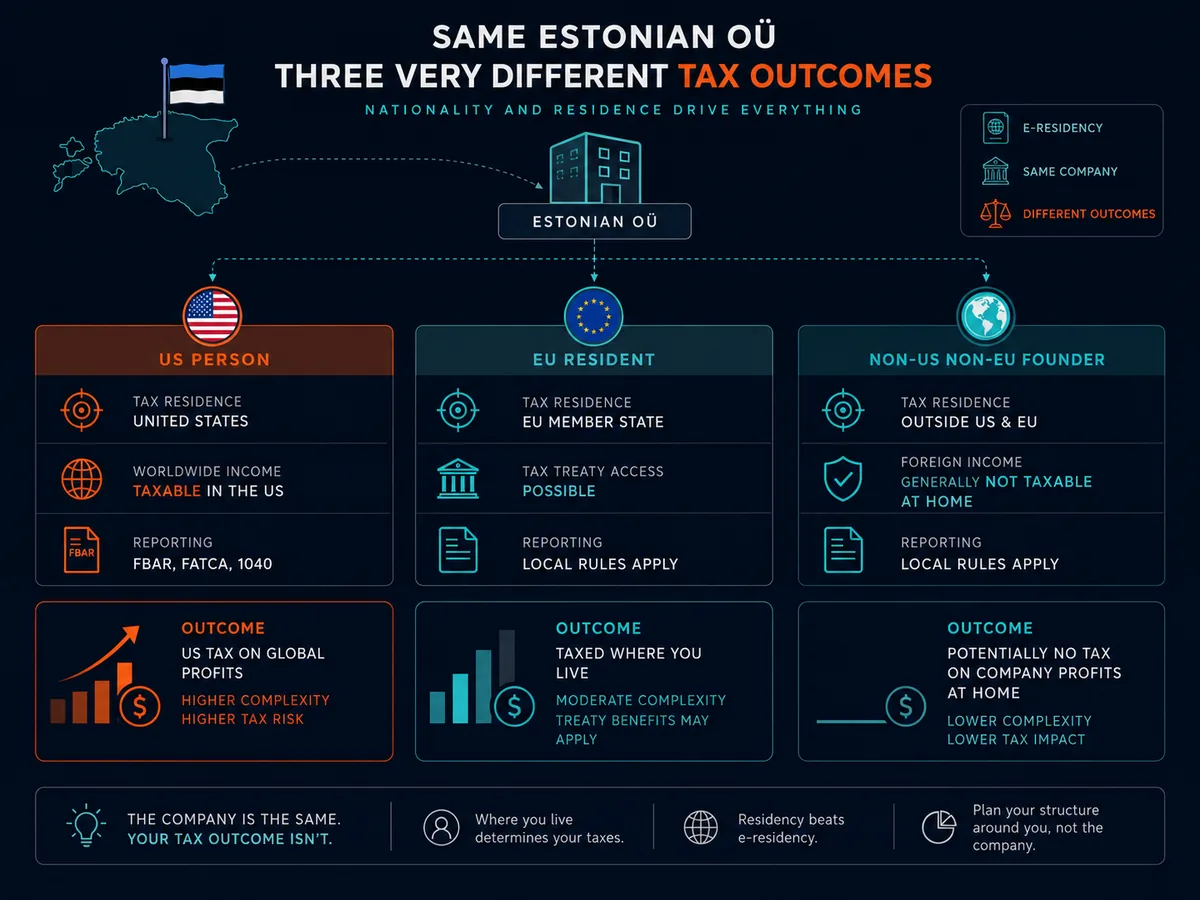

The same Estonian OÜ produces wildly different outcomes depending on where you are tax resident. Three segments matter.

US persons (citizens and green-card holders)

US persons are taxed on worldwide income regardless of where they live or where their company is registered (IRS, Taxation of U.S. Citizens Abroad). An Estonian OÜ owned by a US person is, in nearly all cases, a Controlled Foreign Corporation (CFC) under Subpart F and the GILTI rules in IRC §951A. That means active business income earned by the OÜ is generally taxed currently on the US shareholder's personal return, regardless of whether profits are distributed.

You also owe Form 5471, FBAR (FinCEN 114) for any foreign account over $10,000 aggregate, and FATCA Form 8938 above the relevant threshold (source: FinCEN BSA E-Filing). Forming an Estonian OÜ does not reduce US tax — it adds reporting. The Foreign Earned Income Exclusion (IRS Publication 54) applies to your salary, not the company's profits.

Honest summary for US persons: e-Residency is useful only if you have a genuine business reason to invoice European clients through an EU entity. It is not a tax-optimisation tool for you.

EU freelancers and digital nomads

If you are tax resident in an EU member state, the OECD Model Tax Convention and most national laws will treat your Estonian OÜ as tax resident where it is effectively managed — usually where you, the director, sit. A Spanish-resident founder running an Estonian OÜ from Valencia is operating a Spanish-tax-resident company in the eyes of the Spanish AEAT, with all the corporate tax and social security consequences that brings.

EU CFC rules under ATAD (Directive 2016/1164) can also attribute the OÜ's passive income to you personally if Estonia's effective tax on it is below half your home rate. Several EU states (France, Germany, Spain, the Netherlands) operate exit taxes on unrealised gains if you move abroad with substantial holdings.

Honest summary for EU readers: e-Residency simplifies admin if you live in Estonia or genuinely operate from there. If you stay in your home country, the OÜ is most likely taxed at home, and you have just added an extra layer of accounting.

Non-US, non-EU readers

This is the segment for whom the marketing comes closest to reality. If you live in a territorial-tax jurisdiction (Hong Kong, Singapore for foreign-sourced active income, Malaysia, Georgia, Panama, Paraguay, UAE) or a country with weak CFC enforcement, an Estonian OÜ can sit cleanly above your personal residence and the 0%-on-retained-earnings system works as advertised — provided the company genuinely operates from somewhere outside your home jurisdiction or your home jurisdiction simply does not tax foreign corporate income.

You still need real substance somewhere. A letterbox in Tallinn run from your apartment in Tbilisi will not survive a serious tax challenge.

How to become an e-resident in Estonia

The mechanical process is straightforward. The judgement calls come earlier.

- Decide whether you actually need it. Read the section above. If you are a US person looking for tax savings, stop here.

- Prepare documents. A passport scan, a recent digital photo to passport-photo specifications, a CV or LinkedIn URL, a Visa or Mastercard for the fee, and a motivation statement (one to three paragraphs explaining what you intend to do).

- Apply online at eresident.politsei.ee. The form takes 30–45 minutes if your documents are ready. Choose a pickup location — an Estonian embassy, consulate, or one of the dedicated pickup points in Tallinn, Tokyo, Seoul, San Francisco, Singapore, and a handful of other cities.

- Pay the state fee. €100 if you collect in Estonia, €120 if you collect at an embassy, plus a €30 service fee if collecting outside Estonia (source: e-Resident.gov.ee fees page).

- Wait for background checks. Estonia's Police and Border Guard run the screening. Published guidance says up to 3–8 weeks; in practice many applicants report 6–10 weeks.

- Collect in person. You must appear in person, present your passport, and give fingerprints. The card, PIN1, PIN2, and PUK envelopes are handed over together.

- Install the software. Download the Estonian ID-card software, set up DigiDoc4, and test signing a document before you rely on it.

Approval rates sit around 95% of completed applications based on programme-level disclosures, but Estonia does not publish a current monthly figure. Refusals cluster around sanctioned jurisdictions, criminal records, and unclear motivation statements.

What it actually costs

The €100 application fee is the marketing number. The total annual cost of running an Estonian OÜ as a non-resident is materially higher. Here is a realistic breakdown for a sole-founder service business.

| Item | Cost | Frequency |

|---|---|---|

| e-Residency state fee | €100–€120 | One-off |

| Service fee (collection outside Estonia) | €30 | One-off |

| Company registration (OÜ) state fee | €265 | One-off |

| Share capital (can be deferred since 2023) | €0.01 minimum | One-off |

| Legal/virtual address in Estonia | €100–€300 | Annual |

| Contact person (required for non-resident boards) | €200–€400 | Annual |

| Accounting (basic, sole founder) | €600–€1,500 | Annual |

| Annual report filing | Included with accountant or €50–€150 separately | Annual |

| VAT registration and filings (if applicable) | €300–€800 | Annual |

| Banking — fintech (Wise Business, Revolut Business) | €0–€150 setup, ~€10/month | Ongoing |

[source: e-Resident.gov.ee start-a-company pages, Xolo, Companio pricing — verify against current published rates before relying]

Realistic first-year cash outlay for a non-resident solo founder using a service provider: €1,200–€2,400. Year two onwards: €900–€1,800. Add corporate income tax of 22% on any distributed profit from 2025 (source: Estonian Tax and Customs Board), and personal tax wherever you actually live.

Tax: the part the marketing skips

Estonia's headline tax feature is real: a private limited company pays 0% corporate income tax on retained and reinvested profits, and tax only crystallises on distribution. From 1 January 2025 the distribution rate is 22% (up from 20%) on gross distributions (source: Estonian Tax and Customs Board, corporate income tax).

This is genuinely useful for founders who reinvest. It is genuinely useless if:

- You live in a country that taxes your worldwide income or applies CFC rules.

- You take the money out as salary, dividends, or owner draws to live on.

- Your home country treats the OÜ as locally tax resident because it is managed from there.

The single most common mistake we see: people form an Estonian OÜ, continue living and working from Lisbon, Berlin, or San Francisco, and assume the OÜ's 0% retained-earnings treatment is theirs. It is not. Place of effective management determines corporate tax residence under most treaties (OECD Model Convention, Article 4).

Benefits of e-Residency

For the right reader, the benefits are concrete:

- Legitimate EU legal entity without needing a director or office in Estonia (a contact person is required, not a director).

- Fully online administration — signing, filing, banking via fintechs, board resolutions.

- 0% corporate tax on retained earnings, which compounds across years for reinvesting founders.

- Access to EU payment infrastructure — Stripe, Wise, Payoneer, EU marketplaces.

- Credible jurisdiction — Estonia is an OECD and EU member, not an offshore blacklist name.

- Low minimum share capital — €0.01 per shareholder since the 2023 Commercial Code amendments (source: Estonian Centre of Registers and Information Systems).

Drawbacks of e-Residency

The honest list:

- Banking is the bottleneck. Estonian high-street banks (LHV, SEB, Swedbank) routinely refuse non-resident applicants. Most e-residents use Wise Business or Revolut Business, which are payment institutions, not banks — no deposit insurance up to €100,000 on those balances.

- Tax residency confusion. The OÜ is taxed where it is managed, which is rarely Estonia for non-resident founders.

- Annual costs add up. €900–€2,000/year is typical once accounting, address, and contact person are included.

- No Schengen, no visa, no relocation right. This trips up applicants every month on Reddit and forums.

- Compliance overhead grows with revenue. VAT, EU OSS, payroll if you hire — all real obligations.

- Reputation risk where overused for substance-less structures. Some banks and payment processors now ask more questions when they see Estonian OÜs with non-resident sole owners.

Common mistakes

Avoid these:

- Treating e-Residency as a tax structure. It is not. The OÜ is a tax structure; e-Residency is just how you access it.

- Ignoring place of effective management. If you are the only director and you live in Munich, your OÜ is at material risk of being treated as German tax resident.

- Assuming you can bank in Estonia. Plan for fintech banking from day one.

- Skipping the accountant. Estonian filings are in Estonian. You need a service provider — Xolo, Companio, 1Office, Enty, or similar.

- Forgetting US tax obligations. If you hold a US passport or green card, the OÜ does not reduce your US tax. It adds reporting (Form 5471, FBAR, FATCA).

- Using a residential address without permission. A virtual address service is cheap (€100–€300/year). Using a friend's flat without proper agreement creates substance and contractual problems.

Comparing service providers

You can register the OÜ yourself, but most e-residents use a service provider that bundles legal address, contact person, accounting, and bookkeeping. The main players, by editorial assessment:

- Xolo — strongest for solo freelancers; flat-rate "Xolo Leap" includes everything bundled. Best documentation. Higher monthly cost than à-la-carte providers.

- Companio — competitive pricing, English-language support, transparent.

- 1Office — older incumbent, more formal, better for higher-revenue companies needing real accounting.

- Enty — newer, modern interface, useful if you want lighter-touch admin.

We have no current affiliate arrangement with any of these as of publication; pricing and feature claims should be verified on each provider's site. The right choice depends on revenue, complexity, and whether you need VAT and EU OSS handling.

When to consult a qualified professional

Talk to a tax adviser in your country of tax residence before you incorporate, not after. Specifically:

- A US person should speak to a CPA with international experience — Subpart F, GILTI, and Form 5471 are not optional.

- An EU resident should ask their domestic tax authority or a local adviser about place of effective management and domestic CFC rules.

- Anyone considering relocating to Estonia or another jurisdiction to give the structure real substance should take advice in both the origin and destination countries before moving.

If a provider tells you e-Residency lets you escape your home country's tax with no relocation, no substance, and no professional advice, walk away. They are selling a problem, not a solution. See our editorial policy and disclaimer for how we approach this.

FAQ

How do I become an e-resident in Estonia?

Apply online through the Estonian Police and Border Guard portal at eresident.politsei.ee. You submit a passport scan, a motivation statement, a digital photo, and pay the €100–€120 state fee plus a €30 service charge if you collect the card outside Estonia. The application takes about 30 minutes to complete. Background checks run 6–8 weeks. Once approved, you collect the digital ID card in person at an Estonian embassy, consulate, or designated pickup point — biometric verification on collection is mandatory.

What are the drawbacks of e-Residency?

e-Residency is not residency. It gives you no right to live, work, or pay tax in Estonia, and no Schengen access. Banking is the hardest part: traditional Estonian banks rarely open accounts for non-resident e-residents, so most people use fintechs like Wise or Payoneer. The bigger trap is tax: your Estonian company is usually taxed where you actually live and manage it, not in Estonia. US persons remain fully liable for US tax and FATCA reporting. Annual accounting and reporting costs run €600–€2,000.

What are the benefits of e-Residency in Estonia?

You get a government-issued digital identity that lets you form and run an EU company entirely online. Estonia's corporate tax is 0% on retained earnings and 22% on distributed profits from 2025, which suits founders who reinvest. Administration is genuinely digital: signing contracts, filing taxes, banking, and notarising documents all work remotely. For non-EU founders, it offers a credible EU legal entity for invoicing European clients and accessing Stripe, payment processors, and EU marketplaces.

What is the approval rate for e-Residency in Estonia?

Estonia does not publish a single official approval rate, but reported figures from the e-Residency programme sit around 95–97% of completed applications. Refusals usually involve incomplete documentation, sanctioned jurisdictions, criminal records, or unclear motivation statements. Note that e-Residency is not a visa — it carries no immigration rights — so it is not assessed like a residence permit. If you are refused, the Police and Border Guard rarely give detailed reasons, and reapplying without addressing the underlying issue tends to produce the same outcome.

Can US citizens move to Estonia?

Yes, but not via e-Residency. e-Residency is purely digital and grants no right to live in Estonia. US citizens can visit Estonia visa-free for 90 days in any 180-day period under Schengen rules. To relocate, you apply for a residence permit — work, study, family, or the Digital Nomad Visa, which requires proof of €4,500/month gross income from foreign sources. US citizens remain liable for US worldwide tax filing regardless of where they live, which is a separate problem from immigration.

Do I pay tax in Estonia if I have e-Residency?

Only if Estonia is where you actually live or where your company is genuinely managed from. e-Residency itself creates no tax residency. Under most double tax treaties and the OECD model, a company is taxed where its place of effective management sits — usually where the director makes decisions. If you live in Germany and run an Estonian OÜ from your Berlin flat, German tax authorities will likely treat the company as German tax resident. Estonia's 0%-on-retained-earnings system only helps if you genuinely operate from Estonia or another low-tax jurisdiction.

Ready to act on this?

Companio — Estonia e-Residency formation + accounting. Soveraine readers go to the front of the line through our partner link, and you fund independent editorial in the process.

Sources

- e-Residency of Estonia, official programme site — https://www.e-resident.gov.ee/

- Application portal, Estonian Police and Border Guard — https://eresident.politsei.ee/

- Estonian Tax and Customs Board, corporate income tax — https://www.emta.ee/en/business-client/taxes-and-payment/income-tax-companies

- Estonian Centre of Registers and Information Systems (RIK) — https://www.rik.ee/en

- EU Regulation (EU) No 910/2014, eIDAS — https://digital-strategy.ec.europa.eu/en/policies/eidas-regulation

- Council Directive (EU) 2016/1164, Anti-Tax Avoidance Directive (ATAD) — https://eur-lex.europa.eu/legal-content/EN/T