The D8 is Portugal's digital nomad visa, introduced in October 2022 to formalise what consulates had been awkwardly fitting into the D7 — remote workers earning active foreign income. It sits alongside two more familiar routes: the D7 (passive income), and the Golden Visa (now investment-only since the October 2023 reform closed the real-estate path). Most people Googling "Portugal nomad visa" end up confusing all three. This guide separates them, then walks through what the D8 actually requires in 2026 — income floors, documents, tax exposure under the post-NHR regime, and the real cost stack.

La Vida Golden Visas — UK-based specialist covering D7, D8 and the Golden Visa

This article is for prospective applicants doing diligence before they commit, not for people already at the consulate looking for paperwork shortcuts. It covers what the D8 grants, who it suits, the income and document floor, the post-NHR tax position, realistic costs, and the failure modes. It does not cover the Golden Visa fund route or the D2 entrepreneur visa — those are separate guides.

What the D8 actually is

The D8 is a national long-stay visa created under Article 61-B and 61-C of Lei 23/2007 as amended by Decreto-Lei 41/2023, which formalised the "remote workers and entrepreneurs" visa category. It permits a non-EU, non-EEA, non-Swiss national with active foreign-source income above the threshold to enter Portugal, then convert that visa into a renewable residence permit through AIMA — the Agency for Integration, Migration and Asylum that replaced SEF in October 2023.

The standard pathway:

- D8 visa issued by the consulate — valid four months for entry.

- AIMA residence-permit appointment — within those four months.

- Two-year residence permit — issued after the appointment.

- Renewal for three years — at the end of year two, on continued eligibility.

- Permanent residence or citizenship — after five years of legal residence.

The five-year citizenship clock under Article 6 of the Nationality Law is the same as for D7 and Golden Visa holders. What is different is the income type that qualifies, the threshold, and — under the rules in force at the time of writing — the absence of an NHR-style tax incentive specifically aimed at remote workers.

Two versions: temporary stay vs residence

The D8 is not one visa — it is two, with the same income floor but different durations and renewal profiles. Pick the wrong one and the consulate sends you back.

Temporary stay visa (≤ 1 year)

For remote workers who want to spend up to a year in Portugal without intending to settle. Issued for the duration of the contract or assignment, capped at one year, renewable in narrowly defined circumstances. Holders do not get a residence permit and generally do not become Portuguese tax residents unless they cross the 183-day threshold. Suitable for one-year sabbaticals, project assignments, or pre-residency trials.

Residence visa (long-term)

The route most applicants want. Four-month entry visa, AIMA appointment, two-year residence permit, three-year renewal, then permanent residence or citizenship at year five. This is the version that leads to EU residency rights and, eventually, a Portuguese passport. It also triggers the full tax-residency exposure once the holder spends 183 days or establishes a habitual home in Portugal.

Both versions require the same minimum income — four times the Portuguese minimum wage — and broadly the same supporting documents. The choice is intent: short stay vs life move.

Who this applies to — read this first

The application paperwork is roughly the same regardless of passport. The tax consequences are not. Read the segment that matches your situation before doing anything else.

US persons (citizens and green-card holders)

US citizenship-based taxation does not stop at the Portuguese border. You continue to file Form 1040 every year regardless of where you live, and you owe US tax on worldwide income. The Foreign Earned Income Exclusion shelters up to $130,000 of qualifying earned income in 2025 — if you pass either the bona fide residence test or the physical presence test. The D8's settled-residence profile makes the bona fide residence test the natural fit from year two onwards.

FBAR (FinCEN Form 114) and FATCA (Form 8938) reporting kicks in on Portuguese bank accounts above the thresholds — $10,000 aggregate for FBAR, higher for 8938. Several Portuguese banks refuse US-person accounts entirely because of FATCA compliance costs. Open with a bank that takes Americans — Millennium BCP and ActivoBank are the recurring names in 2026.

The PFIC trap is the bigger problem. Most Portuguese and EU mutual funds and ETFs are passive foreign investment companies under US rules. Buy one and you owe punitive PFIC tax (Form 8621) plus interest charges that can exceed the gain. Keep your investment portfolio US-domiciled.

The US–Portugal tax treaty provides foreign tax credit mechanics, so most D8 holders are not double-taxed. But you will likely owe additional US tax on Portuguese-source income each year, and the FEIE does not shield self-employment tax — freelancers still owe SECA on net SE earnings.

EU residents

If you hold an EU, EEA or Swiss passport, you do not need the D8. Free movement under Directive 2004/38/EC gives you the right to live and work in Portugal on a simple registration certificate from the local municipality, with no income floor. This article is not for you — the only piece worth reading is the tax section below, since Portuguese tax-residency rules apply to you the moment you cross the 183-day mark. For the broader non-dom landscape, see non-dom meaning explained.

If you are an EU resident on a non-EU passport (a UK national living in Germany, say, or a Brazilian permanent resident in Spain), the D8 is open to you and you face the same exit-tax considerations as other EU departures. Germany's exit tax under § 6 AStG and France's exit tax under Article 167 bis CGI catch unrealised gains on substantial shareholdings. Plan timing carefully.

Non-US, non-EU readers

This is the primary audience for the D8. Holders of UK, Canadian, Australian, South African, Brazilian, and most Asian passports have the cleanest path because their home tax systems are residence-based — leaving genuinely ends home-country tax exposure (UK split-year under SRT, Canada's departure-tax in T1243/T1244, Australia's residency tests).

CFC rules in your old country may still bite if you keep a foreign company, but for most remote workers a clean break is achievable. For this segment the D8 works closest to how marketing materials describe it — though even here, the post-NHR tax position is the headline change. The Portugal of the 2018-2023 era, with 10 years of capped or zero tax on foreign income, is gone.

Income threshold and documentation

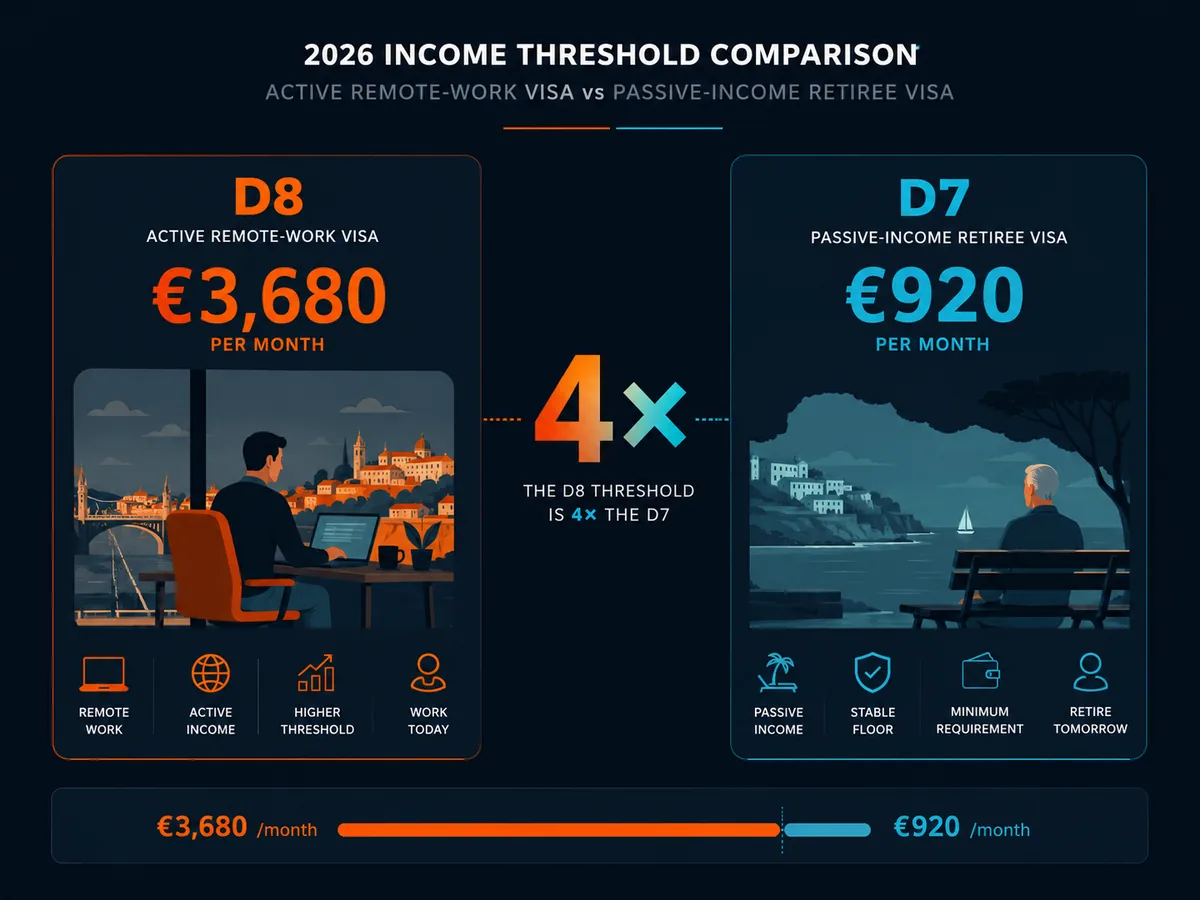

The D8 income floor is four times the Portuguese minimum wage (the retribuição mínima mensal garantida). The minimum wage rose to €870 per month for 2025 and to €920 per month for 2026 under the State Budget Law, putting the D8 floor at:

| Year | Minimum wage | D8 floor (monthly) | D8 floor (annual) |

|---|---|---|---|

| 2025 | €870 | €3,480 | €41,760 |

| 2026 | €920 | €3,680 | €44,160 |

This is the floor, not a target. Consulates approve applicants showing 1.25x to 1.5x the threshold comfortably; borderline cases get refused or sent back for further evidence. Family members scale on top — add 50% for a spouse and 30% per child, mirroring the D7 family formula under Article 98 of Lei 23/2007.

Acceptable proof of income:

- Three to six months of pay slips from a foreign employer, plus the employment contract

- One year of client invoices and matching bank deposits for freelancers

- Two years of business bank statements and tax returns for owner-operators

- Recent platform earnings statements (Upwork, Toptal, Stripe payouts) supported by client contracts

Savings buffer: consulates also expect roughly 12 months of the minimum wage as liquid funds in a Portuguese bank account opened before applying — around €11,040 for a single applicant in 2026, with the standard family scaling.

A common trap: consulates increasingly verify that the income source is genuinely foreign. If you invoice a Portuguese client, that income does not count toward the D8 threshold — it counts as Portuguese-source income that triggers domestic tax and social-security obligations on day one, which is not what the D8 is for. Keep client and employer relationships outside Portugal until residency is settled.

Tax — the post-NHR reality

The single most outdated thing on the English-language internet about Portugal is the "zero-tax remote worker" pitch. That regime closed.

The non-habitual resident (NHR) tax regime, which capped foreign-source professional income at 20% and exempted most foreign passive income for ten years, closed to new applicants on 31 December 2023 under the 2024 State Budget Law (Lei n.º 82/2023). Anyone who became Portuguese tax resident from 1 January 2024 onward cannot apply for NHR.

The replacement, the IFICI scheme — Incentivo Fiscal à Investigação Científica e Inovação — was created under Article 58-A of the Tax Benefits Code (EBF) by Lei n.º 82/2023 and operationalised by Portaria 352/2024. IFICI offers a flat 20% IRS rate on Portuguese-source employment and self-employment income, plus exemption on most foreign-source income, for ten years — but only to a narrow population:

- Tenured researchers in higher-education and scientific institutions

- Qualified technical staff at companies certified as eligible by IAPMEI or AICEP

- Highly qualified roles in companies investing in R&D or in projects benefiting from the contractual tax-benefit regime

- Specific roles in start-ups and innovation centres meeting criteria set by the Agência para a Investigação Clínica e Inovação Biomédica

For a typical D8 holder — a freelance designer working with US clients, a remote engineer at a foreign tech company, a consultant invoicing through a UK Ltd — IFICI does not apply. The default position is ordinary Portuguese personal income tax (IRS) with these 2026 progressive bands:

| Taxable income (€) | Marginal IRS rate |

|---|---|

| Up to 8,059 | 13.0% |

| 8,059 – 12,160 | 16.5% |

| 12,160 – 17,233 | 22.0% |

| 17,233 – 22,306 | 25.0% |

| 22,306 – 28,400 | 32.0% |

| 28,400 – 41,629 | 35.5% |

| 41,629 – 44,987 | 43.5% |

| 44,987 – 83,696 | 45.0% |

| Above 83,696 | 48.0% |

Source: Portuguese 2026 State Budget bands published by Autoridade Tributária e Aduaneira. A solidarity surcharge of 2.5% applies between €80,000 and €250,000, and 5% above €250,000.

On top of IRS, social security contributions apply. Self-employed D8 holders fall under the trabalhador independente regime: 21.4% on a notional contribution base derived from 70% of relevant income, recalculated quarterly. Employed D8 holders working for a foreign employer with no Portuguese presence usually owe contributions personally unless an A1/CoC certificate from a totalisation-agreement country covers them — check the Social Security portal for the current list.

The honest summary: a D8 holder earning €60,000 per year as a freelancer should plan for combined IRS plus social security of roughly 35–45% on Portuguese-residency income, similar to any mid-tier EU member state. The 0% pitch is dead.

Application steps and timeline

The D8 sequence in 2026:

- Gather documents at home (4-8 weeks). Passport, two photos, criminal-record certificates from every country lived in for over a year since age 16 (apostilled, translated), proof of income (12 months minimum), proof of accommodation in Portugal (12-month lease or property deed), Portuguese NIF, Portuguese bank account with buffer funds, private health insurance valid in Portugal, AIMA criminal-record authorisation form, and a cover letter explaining the move.

- Submit at the Portuguese consulate covering your jurisdiction. VFS Global processes intake in many countries; the consulate adjudicates. Service standard is 60-90 days; several consulates run longer.

- Receive D8 visa valid for four months for entry.

- Enter Portugal and attend AIMA appointment within the four-month window. AIMA scheduling has been the main bottleneck since the SEF transition in October 2023, with appointment dates pushed six to eighteen months out in some districts. Show up with originals of everything you submitted at the consulate plus your atestado de residência from the local junta de freguesia.

- Receive two-year residence permit. This is the document that proves you are legally resident. It is the start of the five-year citizenship clock.

Realistic total elapsed time, start to residence card in hand: four to nine months, occasionally longer where AIMA appointments slip.

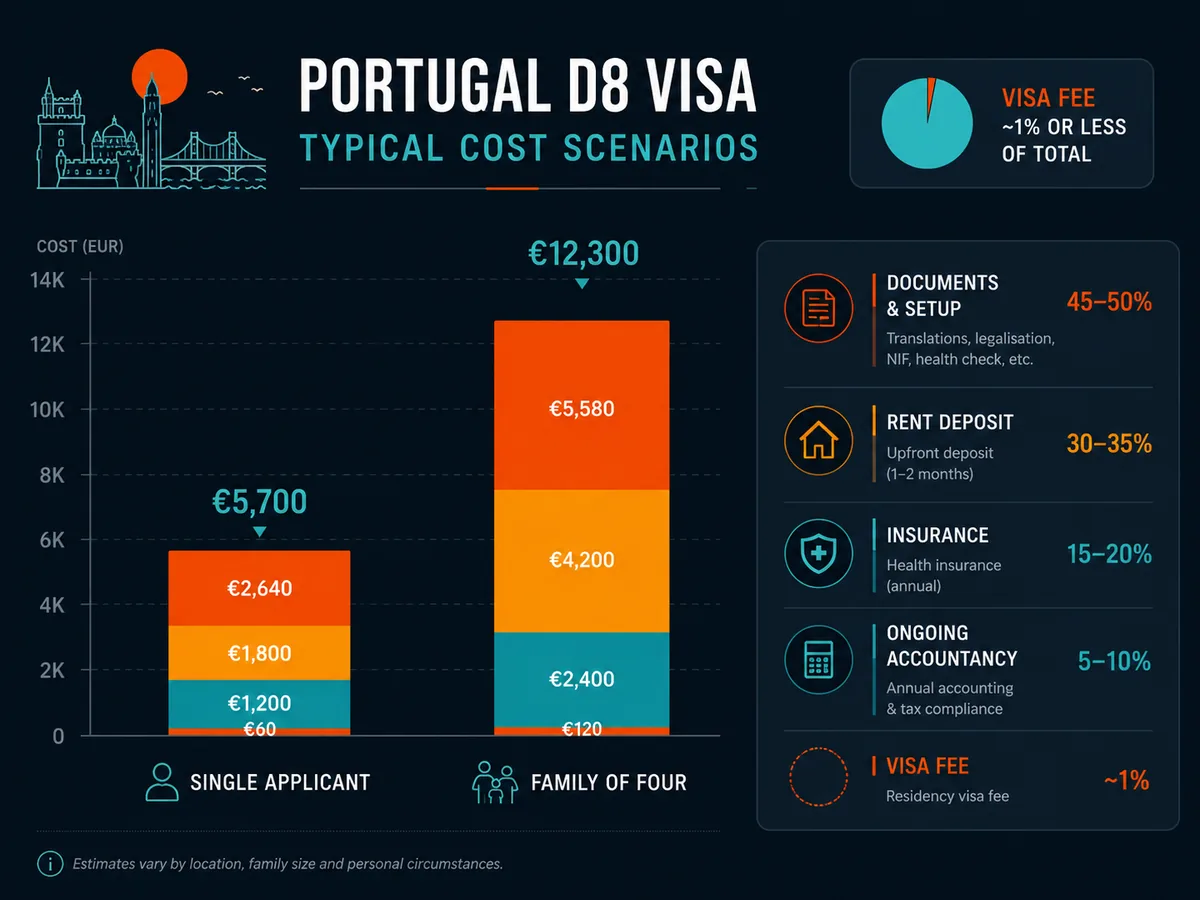

Real costs

Government fees are modest. The real bill is the supporting cost stack.

| Item | Cost (€) | Notes |

|---|---|---|

| Consular visa fee | ~90 | Per applicant |

| AIMA residence-permit fee | ~170 | Per applicant, at the appointment |

| Document apostilles & sworn translations | 300-900 | Varies by country of origin |

| Criminal-record certificates | 50-200 | Per jurisdiction lived in |

| NIF via fiscal representative | 100-250 | Annual fee while non-resident |

| Portuguese bank account opening | 0-300 | Some banks charge non-residents |

| Health insurance (12 months, private) | 500-1,200 | Per applicant; SNS access comes later |

| Rental deposit + first month | 2,500-6,000 | Lisbon/Porto significantly higher |

| Notarised lease (if required) | 50-150 | Some consulates require this |

| Legal / immigration support (optional) | 2,000-5,000 | Per family, full service |

| Annual Portuguese accountancy | 600-1,500 | Self-employed pays more |

| Single applicant DIY | ~4,000-9,000 | Excluding flight, moving, deposits beyond rent |

| Family of three with lawyer | ~10,000-18,000 | Excluding moving costs |

A DIY application is genuinely possible if you can read Portuguese reasonably well and travel to the consulate. A lawyer earns their fee if you have a US passport (FATCA banking issues), unusual income (crypto, multi-jurisdictional freelance), or dependants with complex documentation.

For the practical infrastructure side — international payments, multi-currency accounts, transferring deposit money to Portugal — most D8 applicants set up a Wise account before they move. For travel and gap-period health coverage before the SNS, SafetyWing is the nomad-aware option; pairing it with a longer-term Portuguese private policy is common.

D7 vs D8 vs Golden Visa — which is which

The single most common Soveraine reader question is "which Portugal visa is right for me?" The table below is the short answer. The longer answer is in the dedicated pillars: Portugal D7 visa and Portuguese Golden Visa.

| Feature | D7 | D8 | Golden Visa |

|---|---|---|---|

| Income / investment type | Passive (pensions, dividends, rent, royalties) | Active remote-work / freelance from foreign sources | Capital (fund subscription €500k, R&D €500k, donation €250k) |

| Minimum monthly income (2026) | €920 (1× min wage) | €3,680 (4× min wage) | n/a — capital threshold |

| Minimum capital | ~€11k buffer | ~€11k buffer | €250k–€500k investment |

| Real-estate route | n/a | n/a | Closed since October 2023 |

| Initial residence permit | 2 years | 2 years | 2 years |

| Renewal cycle | 3 years | 3 years | 3 years |

| Minimum stay in Portugal | 6 consecutive / 8 total months per 2yr period | 6 consecutive / 8 total months per 2yr period | 7 days per year |

| Tax residency triggered? | Yes, if 183+ days | Yes, if 183+ days | Optional — most GV holders stay non-resident |

| Tax regime now | Standard IRS (NHR closed) | Standard IRS (NHR closed) | Standard IRS if resident |

| Years to citizenship | 5 | 5 | 5 |

| Best for | Retirees, passive-income holders | Remote employees and freelancers above the floor | High-net-worth investors wanting EU optionality without moving |

The wrong-visa rejections cluster at the D7/D8 boundary. Consulates have wised up to remote-work salary disguised as "dividend income" routed through a one-person company. If your income is active foreign employment or freelance work, apply for the D8 and stop trying to game the D7.

The traps

The AIMA backlog. This is the single biggest source of pain. Since the agency took over from SEF in October 2023, residence-permit appointments have slipped from weeks to months and in some districts more than a year. The visa is valid four months; legally you remain in status as long as the AIMA appointment is scheduled in time, but the practical reality is a long limbo without the residence card needed for banking, healthcare and travel. Apply for the AIMA appointment the day you land. Use the official AIMA portal.

Treating NHR as still available. It is not for anyone who became tax resident on or after 1 January 2024. Marketing pages, immigration-firm blog posts and YouTube videos that still pitch "10 years of 0% tax in Portugal" are either out of date or wrong. The IFICI replacement is narrowly scoped and almost no ordinary D8 holder qualifies. Plan your tax position on standard Portuguese rates.

Portuguese-source income trap. Income from Portuguese clients does not count toward the D8 threshold and triggers Portuguese tax and social security from day one, before residency questions are settled. If you want to keep things simple in year one, keep client work foreign.

US person + PFIC. US D8 holders who buy Portuguese or EU mutual funds, ETFs, or "smart" investment accounts on the assumption that European products are diversified and tax-efficient are walking into the PFIC regime. Form 8621, mark-to-market or QEF elections, and punitive default tax. Keep your investment portfolio US-domiciled and use Portuguese banks only for current-account purposes. A US expat CPA is non-optional — see Bright!Tax or the broader market for options.

Showing only platform earnings. Stripe, Upwork or Toptal payout statements alone are usually not enough. Consulates want to see the underlying contracts, the recurrence of payments, and the relationship to a real client base. Build a 12-month evidence pack before applying.

Booking accommodation via Airbnb for the proof-of-address document. A registered 12-month lease with the landlord's NIF is what the consulate wants. Airbnb screenshots get returned.

Missing the citizenship language requirement late. A2-level Portuguese sounds easy until year four. Start CIPLE-aligned classes within the first year of residency. Free options exist through Português Língua de Acolhimento (PLA) at IEFP centres.

For broader nomad-visa comparison context — Spain's nomad visa, Greece's, Estonia's e-Residency — see digital nomad visas. For the broader question of where to actually become tax resident, see zero-percent tax residencies.

When to consult a professional

The D8 application itself is administrative — most people can run it themselves if they read carefully. The places where professional advice pays for itself:

- Tax planning before becoming Portuguese resident. Realising capital gains, restructuring company holdings, timing dividend distributions, or considering an IFICI angle for genuinely qualifying roles — all decisions best made before the 183-day clock starts.

- US persons on FATCA, FBAR, GILTI and PFIC. A US expat CPA is non-optional. PFIC exposure alone justifies the fee.

- Exit tax in your departing country. EU departures in particular need a tax lawyer in the old jurisdiction.

- Multi-jurisdictional freelance income. If you invoice clients across the US, EU, UK and Asia, the source-of-income analysis is not a DIY job.

A Portuguese immigration lawyer charges €2,000-€5,000 for a full family D8 service. A US expat CPA runs $1,500-$3,500 per year for the ongoing return. For the second passport conversation that some D8 holders eventually have at year five, see Henley & Partners for the citizenship-by-investment route as a parallel option, and our renouncing American citizenship pillar for the exit-tax side. For travel-document tracking during the residency years, iVisa handles the visa-on-arrival paperwork most D8 holders need for non-EU travel.

See our editorial policy on professional advice and our affiliate disclosure for how we handle service recommendations.

Ready to act on this?

La Vida Golden Visas — UK-based specialist that handles D7, D8 and Golden Visa applications end-to-end. Soveraine readers go to the front of the line through our partner link, and you fund independent editorial in the process.

FAQ

What is the digital nomad visa for Portugal?

Portugal's digital nomad visa is the D8, a national long-stay visa introduced in October 2022 under Decreto-Lei 41/2023 and the broader foreigners' law (Lei 23/2007). It is open to non-EU nationals who earn active income from employment or freelance work performed for clients or employers outside Portugal, at or above four times the Portuguese minimum wage — roughly €3,680 per month gross in 2026. It comes in two forms: a temporary stay visa up to one year, and a residence visa that leads to a renewable two-year residence permit and, after five years, eligibility for permanent residence or citizenship.

How much income do I need for the Portugal D8 visa?

The threshold is pegged to four times the Portuguese national minimum wage (the retribuição mínima mensal garantida). For 2025 the minimum wage was €870 per month, so the D8 floor was €3,480. For 2026 the minimum wage rises to €920 per month, putting the D8 income floor at approximately €3,680 per month gross — about €44,160 per year. Consulates also expect a savings buffer of roughly 12 months of the minimum wage (around €11,040 in 2026) and proof of the income via three to six months of pay slips, client contracts, or business bank statements.

What is the difference between the D7 and D8 visa in Portugal?

The D7 is for passive income — pensions, dividends, rental yield, royalties — at a threshold of roughly one times the Portuguese minimum wage. The D8 is for active remote-work income — salary from a foreign employer, freelance fees from foreign clients, business income earned outside Portugal — at four times the minimum wage. Both lead to a two-year residence permit, then renewals, then five-year citizenship. The wrong choice gets rejected. Consulates have started refusing D7 applications where the income source is clearly remote employment, and routing those applicants to the D8.

Do D8 visa holders pay tax in Portugal?

Yes, once they become Portuguese tax residents — generally after 183 days in country or by establishing a habitual home there. The old non-habitual resident (NHR) regime closed to new applicants on 31 December 2023 and was replaced by the much narrower IFICI scheme (Incentivo Fiscal à Investigação Científica e Inovação), aimed mostly at scientific researchers and certain qualified technical workers. Ordinary D8 remote workers generally fall under the standard progressive personal income tax (IRS), with rates from 14.5% to 48% plus solidarity surcharges. Social security contributions of 21.4% on self-employment income may also apply.

How long does the Portugal D8 visa take?

Plan for four to nine months from start to residence card. Document gathering and apostilles take six to eight weeks. The consulate processes the D8 visa in roughly 60 to 90 days under the published service standard, though several consulates run longer. The visa itself is valid for four months from issue, during which you must enter Portugal and attend an AIMA appointment to convert it into a two-year residence permit. AIMA backlogs since taking over from SEF in October 2023 have pushed appointment scheduling out to six to eighteen months in some districts.

Can D8 visa holders bring family members?

Yes. Family reunification under Article 98 of Lei 23/2007 allows the main D8 holder to bring a spouse or registered partner, minor children, dependent adult children under 26 in full-time education, dependent parents (typically over 65), and minor siblings under legal guardianship. Each dependant files their own application. Filing together with the main applicant is usually cheaper and faster than reunifying after arrival. Income requirements scale: add 50% for the spouse and 30% per child on top of the main applicant's threshold.

Does the D8 visa lead to Portuguese citizenship?

Yes, on the same timeline as other residence routes. After five years of legal residence under the D8, you can apply for permanent residence or Portuguese citizenship under Article 6 of the Nationality Law. Citizenship requires A2-level Portuguese (the CIPLE language exam), a clean criminal record in Portugal and any country where you lived after age 16, and proof of genuine community connection. Portugal allows dual citizenship, so most applicants do not need to renounce their original nationality. The five-year clock starts from the date the residence permit is issued, not the date you arrive on the visa.

Is the Portugal D8 visa worth it in 2026?

For genuinely remote workers earning above the threshold who want a real EU residence — yes. The path to permanent residence and citizenship is intact, the cost is moderate compared to investment routes, and the income floor is achievable for mid-career engineers, designers and consultants. What it is no longer is a zero-tax move. With NHR closed and IFICI narrowly scoped, most D8 holders will pay ordinary Portuguese tax on worldwide income from year one of residency. Run the numbers against the D7, Spain's nomad visa, Greece's, and Italy's impatriate regime before committing.

Sources

- Lei 23/2007 (Portuguese foreigners' law), consolidated text — https://dre.pt/dre/legislacao-consolidada/lei/2007-34536475

- Decreto-Lei 41/2023 (D8 and related visa-category amendments) — https://dre.pt/

- AIMA — Agência para a Integração, Migrações e Asilo — https://aima.gov.pt/

- Portuguese national visas — official MNE portal — https://vistos.mne.gov.pt/en/national-visas/general-information

- Autoridade Tributária e Aduaneira (AT) — https://www.portaldasfinancas.gov.pt/

- Segurança Social — self-employed contributions — https://www.seg-social.pt/

- Article 6, Portuguese Nationality Law — https://dre.pt/dre/legislacao-consolidada/lei/1981-34530775

- IRS Publication 54 (Tax Guide for US Citizens and Residents Abroad) — https://www.irs.gov/publications/p54

- FinCEN BSA E-Filing (FBAR / Form 114) — https://bsaefiling.fincen.treas.gov/main.html

- IRS FATCA summary (Form 8938) — https://www.irs.gov/businesses/corporations/summary-of-fatca-reporting-for-us-taxpayers

- Directive 2004/38/EC (EU citizens' free movement) — https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=celex%3A32004L0038

- UK Statutory Residence Test (RDR3) — https://www.gov.uk/government/publications/rdr3-statutory-residence-test-srt

- France exit tax — Article 167 bis CGI — https://www.legifrance.gouv.fr/codes/article_lc/LEGIARTI000041464977