A "zero-tax company structure" is one of the most-searched phrases in international tax and one of the most misunderstood. The headline — a country where the corporate rate is 0% — is true in a handful of jurisdictions. The implication — that incorporating there means you pay no tax — is almost always false. The rate on the company and the rate on the owner are separate questions, and the owner's residency usually decides the outcome. This guide walks through twelve structures that can produce a 0% rate on the entity, what each costs, and why the same paperwork that saves one founder thousands costs another more than they would have paid at home.

Doola — US LLC + EIN + tax filings, built for non-residents

What "0% tax structure" actually means

A company is a separate legal person. Most countries tax it on its profits; some do not. A "0% tax structure" is a company formed in one of the jurisdictions that does not — or that exempts the kind of income the company earns, or defers the tax until profits are distributed.

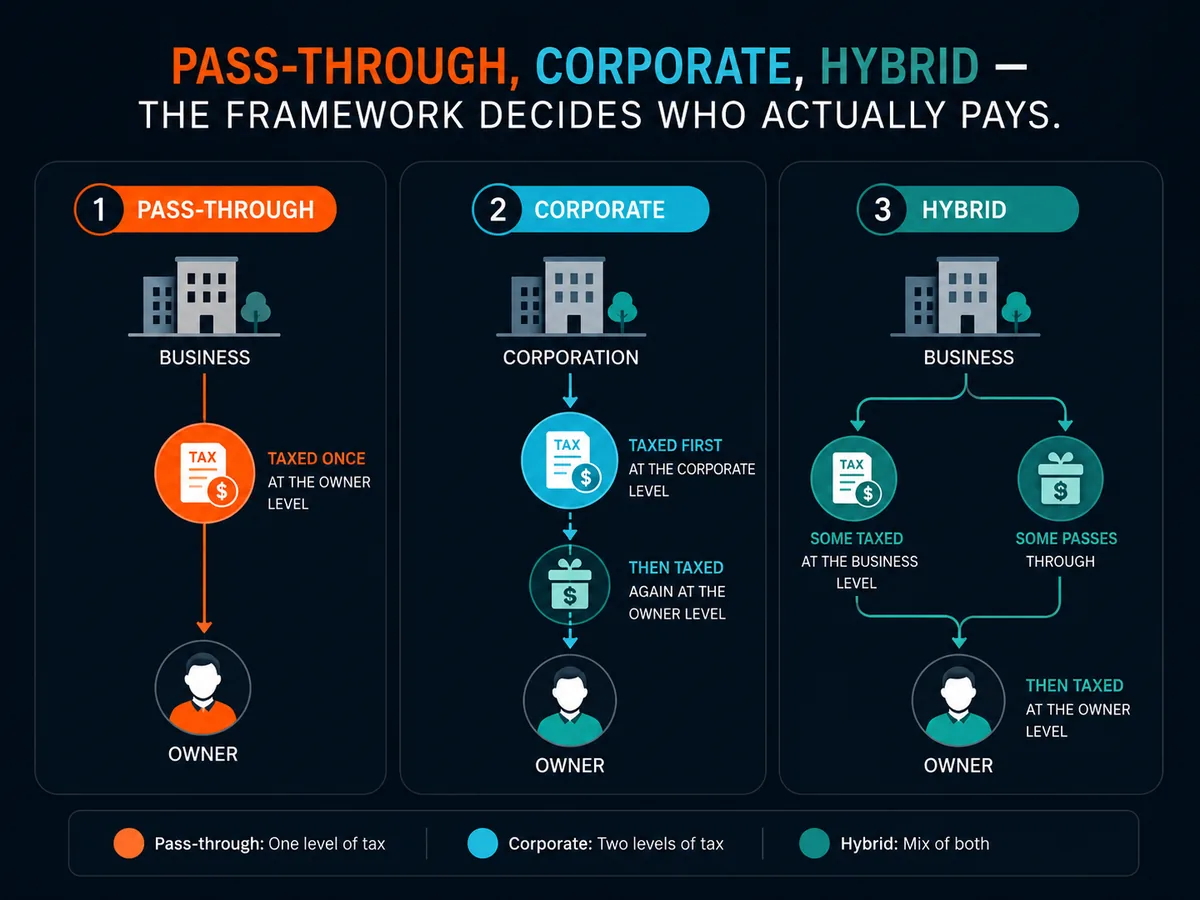

That part is straightforward. The complication starts with the owner. Three frameworks decide what happens to the profits.

Pass-through entities transfer the tax obligation directly to the owner. A US single-member LLC is the classic case: the IRS treats it as a "disregarded entity" and the profit is taxed in the owner's hands as if the company did not exist (IRS — disregarded entities). UK LLPs work similarly — the partnership pays no corporation tax, the partners do (HMRC Partnership Manual).

Corporate entities pay tax themselves and then distribute after-tax profits as dividends, which the owner may be taxed on again. A 0% corporate rate sounds appealing until the owner's country taxes the dividend at 30% or more.

Hybrid systems defer rather than eliminate. Estonia's OÜ pays no tax on retained earnings but a 22% rate on distributions in 2025 (Estonian Tax and Customs Board).

Layered on all three is the controlled foreign company rule set. Most developed economies attribute the undistributed profits of foreign companies back to resident owners who control them — the United States through Subpart F and GILTI (IRS — GILTI), the EU through the Anti-Tax Avoidance Directive (Directive (EU) 2016/1164).

The rule of thumb that survives every variation: incorporation does not change residency, and residency decides tax.

Who this applies to — read this first

The structures below are the same regardless of who you are. The tax outcomes are not. Read the section that matches your status before reading the catalogue.

US persons

If you are a US citizen or green-card holder, the marketing for offshore structures aims somewhere else. The US taxes citizens on worldwide income regardless of where they live (IRS — US Citizens Abroad). Owning more than 10% of a foreign corporation triggers Form 5471 reporting, with $10,000 minimum penalties for non-filing (Form 5471 instructions). A controlling stake activates Subpart F and GILTI, which pull foreign profits onto your US return whether you distribute them or not.

The three legitimate routes for a US person are: an entity fiscally transparent to the US (an LLC), Puerto Rico's Act 60 with genuine territory residency, or renunciation under IRC §877A with the associated exit tax. Everything else is paperwork that adds cost.

EU residents

The EU is a high-tax bloc with the world's most-developed anti-avoidance framework. The Anti-Tax Avoidance Directive (ATAD I and II) requires every member state to apply CFC rules, interest-deduction limits, exit taxation and a general anti-abuse rule. DAC6 requires reporting of cross-border tax arrangements. If you are tax resident in France, Germany, Spain or Italy and you incorporate in the UAE, your home tax authority can almost certainly attribute the profits back to you — and increasingly will.

The structures that work for EU residents are those operating inside the EU's own framework. An Estonian OÜ is a normal European company, taxable as Estonia chooses to tax it. A UK LLP for a non-UK partner sits outside UK corporation tax legitimately. Anything based on shifting profits to a zero-tax jurisdiction without changing residence first is, in 2026, the riskiest move on the menu.

Non-US, non-EU readers

This is where zero-tax structures can actually produce zero tax. If you are personally resident in a territorial-tax country (Hong Kong, Singapore, Panama, Costa Rica, Malaysia, Paraguay, Georgia) or a no-tax country (UAE, Cayman, BVI, Bermuda, Bahamas, Monaco), and your company's profits are foreign-source under your home country's rules, the combination genuinely works.

The constraint is real residency. A Caribbean CBI passport combined with a Dubai golden visa does not mean you are tax resident anywhere — and tax authorities increasingly treat statelessness for tax purposes as evidence you remain resident where you started. The OECD Model Convention's tie-breaker tests (Article 4) pull you toward the place where your home, family and economic life actually are.

The structures

Twelve structures that can produce a 0% rate on the entity. The order is rough — easier and cheaper toward the top, more specialised toward the bottom.

US LLC (single-member, non-resident-owned)

A single-member US LLC formed in Wyoming, Delaware or New Mexico, owned by a non-US person with no US-source income and no US trade or business, owes no US federal income tax. The IRS treats it as a "disregarded entity" — fiscally transparent, taxed in the owner's hands (IRS — Single Member LLCs). Setup runs $39 to $500 through providers like Northwest or Doola; annual cost stays under $500. Form 5472 with a pro-forma 1120 is mandatory if the LLC is foreign-owned, with $25,000 penalties for non-filing (Form 5472 instructions).

The catch: 0% at the entity, but the owner owes personal tax wherever they are resident. Banking is easier than most offshore options — Mercury and Relay open accounts for non-resident-owned LLCs.

Estonia OÜ

An Estonian private limited company (osaühing) pays no corporate income tax on retained earnings. The rate applies only on distribution — 22% for 2025 (Estonian Tax and Customs Board). For a founder reinvesting profits, the deferred system can mean genuine 0% during the retention period. The e-Residency programme allows non-residents to form and manage a company entirely online (e-Residency). Formation costs €265 plus state duty; accounting through Companio or Xolo runs €100 to €200 a month.

The catch: distributions are taxable in Estonia and again in the owner's country, with credit under most treaties. Suits founders compounding capital, not those needing monthly cash extraction.

UK LLP (non-resident partners)

A UK limited liability partnership is fiscally transparent — the LLP owes no UK corporation tax, and where all partners are non-UK residents with no UK-source income, no UK tax arises at the partnership level (HMRC Partnership Manual). Formation through Companies House costs £50; annual confirmation statement £34. Accounts file publicly.

The catch: privacy is minimal, and UK banking for non-resident LLPs remains difficult. Partners owe personal tax wherever they are resident.

UAE Free Zone Company

A free-zone company in the UAE can qualify for 0% corporate tax on "qualifying income" under the federal regime introduced in 2023 (UAE Federal Tax Authority). Personal income tax remains at 0%. Combined with UAE tax residency through the company, the structure produces a full-stack zero outcome for a resident owner. Setup through SPC, IFZA or Meydan costs AED 12,000 to 25,000 ($3,300 to $6,800), plus visa, Emirates ID and office. Annual maintenance runs $5,000 to $10,000.

The catch is substance. A free-zone company without real activity in the UAE risks losing the qualifying-income exemption. Plan to spend real time there — the 90-day informal benchmark, plus a tax residence certificate from the Federal Tax Authority.

Hong Kong Limited Company

Hong Kong operates a territorial tax system. Profits sourced outside Hong Kong are not taxed, even if the company is incorporated there; onshore profits are taxed at 8.25% on the first HK$2 million and 16.5% above (Inland Revenue Department). Setup costs $1,500 to $3,500; annual statutory audit runs $1,500 to $4,000.

The catch: offshore-source claims must survive an IRD audit, and the bar has tightened since the 2018 base-erosion reforms. Banking is notoriously difficult — HSBC, DBS and the major locals reject many small e-commerce applicants. Statrys and similar fintechs partially fill the gap.

Singapore Private Limited Company

Singapore's headline corporate rate is 17%, but partial exemptions reduce the effective rate to under 9% on the first S$200,000 of profit, and foreign-source income remitted under specific conditions can be exempt under section 13(8) (IRAS). Setup through Sleek runs S$700 to S$1,500; annual cost S$2,000 to S$5,000. A resident director is required.

The catch: not zero-tax but low-effective-rate, with world-class banking and credibility. Suits operating businesses with serious customers, not those chasing entity-level 0%.

BVI Business Company

A BVI Business Company pays no corporate income tax on foreign-source profits, no capital gains tax, no withholding tax on dividends, under the BVI Business Companies Act 2004 (BVI FSC). Formation runs $1,500 to $2,500; annual government fee $450. The Economic Substance Act 2018 requires "relevant activities" to demonstrate substance — pure holding companies comply more easily than operating ones.

The catch: banking. Few international banks open accounts for BVI companies without an underlying operating jurisdiction. Reputation has degraded since the Panama and Pandora Papers. Works as a holding vehicle in a multi-layer structure.

Cayman Islands Exempted Company / LLC

The Cayman Islands impose no corporate income tax, no capital gains tax, no withholding tax. The exempted company can obtain a tax-exemption certificate valid 20 years, renewable to 30 (Cayman General Registry). The Cayman LLC, introduced in 2016, mirrors a Delaware LLC and is widely used by hedge funds. Setup runs $4,000 to $10,000; annual government fee from $850. Economic-substance filings apply.

The catch: cost and reputation. Cayman is the benchmark for fund structures and serious holdings — overkill for a one-person consulting business, appropriate for assets measured in millions.

Nevis LLC

The Federation of Saint Kitts and Nevis levies no income tax on a Nevis LLC's foreign-source profits. Nevis is best known for asset protection — the Nevis LLC Ordinance creates one of the highest legal barriers in the world to creditor claims, including a $100,000 bond requirement for foreign creditors to bring suit (Nevis FSRC). Setup runs $1,500 to $3,500; annual fee $450 to $850.

The catch: payment processors and banks treat Nevis with suspicion. A defensive layer to hold equity in operating companies elsewhere, not an operating entity.

Panama Corporation (Sociedad Anónima)

Panama's territorial system exempts foreign-source income from corporate tax — a Panamanian corporation earning from clients outside Panama owes no Panamanian tax (Dirección General de Ingresos). Setup runs $1,000 to $1,500; annual tasa única is $300 plus registered agent $250 to $500.

The catch: Panamanian residency for the owner is the path to a clean outcome. The Friendly Nations Visa and pensionado programmes can produce real tax residency with a 183-day expectation. Without that, the corporation's position is sound but the owner's is determined elsewhere.

Georgia — Individual Entrepreneur, Small Business Status

Georgia (the country) offers a Small Business Status for registered individual entrepreneurs. Qualifying revenue is taxed at 1% up to 500,000 GEL (~$185,000) per year (Revenue Service of Georgia). Registration is free; bookkeeping costs $50 to $150 a month.

The catch: a personal regime, not corporate — and real residency in Georgia (180+ days, central place of life) is the legitimate way in.

Qatar Free Zone Entity

Qatar offers 0% personal income tax, and entities in the Qatar Free Zones Authority or Qatar Financial Centre can negotiate corporate-tax holidays for qualifying activities (Qatar Financial Centre). Standard corporate tax is 10% outside the free zones. Setup costs $5,000 to $15,000.

The catch: accessibility. Built for larger entrants and strategic sectors — for most online entrepreneurs the UAE remains the easier Middle East option.

Comparison table

| Structure | Setup cost (USD) | Annual cost (USD) | Tax on entity | Tax on owner | Who it suits |

|---|---|---|---|---|---|

| US LLC (Wyoming) | $39 – $500 | $200 – $500 | 0% (pass-through) | Owner's residency | Non-US online businesses |

| Estonia OÜ | $300 – $700 | $1,200 – $2,400 | 0% retained, 22% distributed | Plus owner's residency tax | EU-flavoured remote founders |

| UK LLP | $80 – $300 | $300 – $1,000 | 0% (pass-through) | Owner's residency | Small partnerships, agencies |

| UAE Free Zone | $3,300 – $6,800 | $5,000 – $10,000 | 0% on qualifying income | 0% if UAE resident | Founders relocating to Dubai |

| Hong Kong Ltd | $1,500 – $3,500 | $3,000 – $7,000 | 0% on foreign-source | Owner's residency | E-commerce, agencies with audit appetite |

| Singapore Pte Ltd | $700 – $1,500 | $2,000 – $5,000 | ~9% effective on first S$200k | Owner's residency | Scale-stage, banking-sensitive |

| BVI Business Company | $1,500 – $2,500 | $1,500 – $3,000 | 0% | Owner's residency + CFC | Holding companies |

| Cayman Exempted | $4,000 – $10,000 | $2,500 – $5,000 | 0% | Owner's residency + CFC | Funds, large holdings |

| Nevis LLC | $1,500 – $3,500 | $1,000 – $2,000 | 0% | Owner's residency + CFC | Asset protection layer |

| Panama Corp | $1,000 – $1,500 | $750 – $1,500 | 0% on foreign-source | Owner's residency | Territorial-system residents |

| Georgia IE | $0 | $600 – $1,800 | 1% on revenue | Personal regime | Solo freelancers in Georgia |

| Qatar Free Zone | $5,000 – $15,000 | $5,000 – $12,000 | 0% on qualifying | 0% if Qatar resident | Sectoral / regional fit |

CFC rules: the elephant in the room

Controlled foreign company rules are why a 0% structure does not produce a 0% outcome for most readers. Every developed country has them, and they share the same intuition: if a resident controls a foreign company in a low-tax jurisdiction, the home country attributes some or all of the company's undistributed profits back to the resident.

For US persons, the rules are Subpart F (in force since 1962) and GILTI (added by the 2017 Tax Cuts and Jobs Act). The effective US tax rate on GILTI for individual owners can exceed 35% without careful planning (IRS — GILTI). Form 5471 reports the company; penalties for non-filing start at $10,000 per form per year.

For EU residents, ATAD I (in force since 2019) requires every member state to adopt CFC rules (Directive (EU) 2016/1164). France's Article 209 B CGI catches subsidiaries in jurisdictions taxing at less than half the French rate; Germany's Außensteuergesetz attributes passive income from low-tax foreign entities. Incorporating in the UAE while living in Paris is, in 2026, a structure that triggers attribution rather than avoiding it.

For UK residents, CFC rules under TIOPA 2010 Part 9A operate on a chargeable-profits basis with exemptions for genuine commercial activity (HMRC CFC manual).

For non-US, non-EU readers whose home country has no CFC regime — much of Asia, Latin America, the Middle East and Africa — the rules below the company level often do not exist. This is why the same offshore company that triggers attribution for a Berlin freelancer produces a clean 0% for a Bangkok-resident entrepreneur.

OECD BEPS Pillar Two adds a 15% global minimum effective tax rate for multinationals with consolidated revenue ≥ €750 million (OECD — Pillar Two). Below that threshold the rule is irrelevant.

How to actually use these structures legally

Four principles separate legitimate structures from paperwork that creates risk.

Residency first, structure second. Decide where you will be tax resident before you incorporate anywhere. A clean residency in a territorial-tax or zero-tax country — UAE, Panama, Costa Rica, Georgia, Paraguay — does the heavy lifting. The reverse almost always fails CFC and treaty tie-breaker tests.

Substance is real and increasing. OECD BEPS Action 5 and the EU's economic-substance reviews pushed every traditional offshore jurisdiction to enact substance laws between 2018 and 2020. A shell with a mailing address fails; a company with real office, real bank account, real economic purpose passes.

Reporting is not optional. Common Reporting Standard exchange of financial-account data covers more than 110 jurisdictions (OECD — CRS). Beneficial-ownership registers in the EU, UK, Singapore and BVI disclose the real owner behind any nominee. FATCA does the same to US persons globally.

Banking is the silent killer. A legal structure that cannot open a bank account is useless. Test banking before you incorporate. Wise Business accepts most legitimate small-entity applications globally. Traditional banks remain difficult for BVI, Nevis and Cayman without serious assets behind them.

The honest summary: a 0% structure paired with a 0% residency produces a real outcome. A 0% structure paired with a normal residency is a compliance exercise that adds cost. The structure is the easy part; the residency is the rest of the iceberg.

Ready to act on this?

Doola handles US LLC formation, EIN, registered agent and annual filings for non-residents end to end — the cheapest legitimate entry point into a 0% structure. Soveraine readers fund independent editorial when they use our partner link.

Sources

- IRS — Single Member Limited Liability Companies. https://www.irs.gov/businesses/small-businesses-self-employed/single-member-limited-liability-companies

- IRS — Form 5472 instructions. https://www.irs.gov/forms-pubs/about-form-5472

- IRS — Global Intangible Low-Taxed Income (GILTI). https://www.irs.gov/businesses/corporations/global-intangible-low-taxed-income-gilti

- IRS — Form 5471 instructions. https://www.irs.gov/forms-pubs/about-form-5471

- HMRC — Partnership Manual on Limited Liability Partnerships. https://www.gov.uk/hmrc-internal-manuals/partnership-manual

- HMRC — International Manual: Controlled Foreign Companies. https://www.gov.uk/hmrc-internal-manuals/international-manual/intm190000

- Estonian Tax and Customs Board — Corporate income tax. https://www.emta.ee/en/business-client/taxes-and-payment/income-taxes/corporate-income-tax

- e-Residency Estonia — official site. https://www.e-resident.gov.ee/

- UAE Federal Tax Authority — Corporate Tax. https://tax.gov.ae/en/taxes/corporate.tax.aspx

- Hong Kong Inland Revenue Department — Profits Tax. https://www.ird.gov.hk/eng/tax/bus_pft.htm

- Inland Revenue Authority of Singapore — Foreign-Sourced Income. https://www.iras.gov.sg/taxes/corporate-income-tax/specific-topics/foreign-sourced-income

- BVI Financial Services Commission. https://www.bvifsc.vg/

- Cayman Islands General Registry. https://www.ciregistry.gov.ky/

- Nevis Financial Services Regulatory Commission. https://www.nevisfsrc.com/

- Dirección General de Ingresos — Panama. https://dgi.mef.gob.pa/

- Revenue Service of Georgia. https://rs.ge/en

- Qatar Financial Centre. https://www.qfc.qa/

- Directive (EU) 2016/1164 — Anti-Tax Avoidance Directive. https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32016L1164

- OECD — Pillar Two global minimum tax. https://www.oecd.org/tax/beps/pillar-two/

- OECD — Common Reporting Standard. https://www.oecd.org/tax/automatic-exchange/common-reporting-standard/

- OECD Model Tax Convention. https://www.oecd.org/tax/treaties/model-tax-convention-on-income-and-on-capital-condensed-version-20745419.htm

- IRC §877A — Expatriation tax. https://www.law.cornell.edu/uscode/text/26/877A