A "bona fide resident" is a US tax concept. It is not a passport, not a visa, and not a status another country grants you. The IRS uses it as one of two tests — the other being the physical presence test — to decide whether a US citizen or resident alien living abroad can exclude foreign-earned income from US tax under Section 911 of the Internal Revenue Code. This guide explains what the test actually requires, who it applies to, how it differs from physical presence, and the territory-specific version used for Puerto Rico and the US Virgin Islands. It is written for US persons first, because the term is a US tax term — but we cover what readers from other countries should take from it.

Bright!Tax — US expat tax filings (FBAR + FATCA + FEIE specialists)

What "bona fide resident" means

A bona fide resident, in the IRS's words, is someone who "resides in a foreign country for an uninterrupted period that includes an entire tax year." For US filers that means January 1 to December 31 — a full calendar year, not a rolling twelve months (IRS: Foreign Earned Income Exclusion — Bona Fide Residence Test).

The word "resides" is doing real work. The IRS distinguishes a resident — someone with a settled life in a place — from a transient or sojourner who is there temporarily for a job, a contract, or pleasure. The statutory authority is IRC §911(d)(1)(A), and the test is borrowed from older case law on what it means to be domiciled somewhere.

There is no checklist. The IRS weighs the totality of your circumstances: the nature and length of your stay, the type of accommodation, whether your family is with you, your participation in local activities, whether you've filed a foreign tax return as a resident, and your stated intent. Pass the test and you can claim the foreign earned income exclusion — $130,000 for tax year 2025 (IRS Rev. Proc. 2024-40) — plus a foreign housing exclusion.

Who this applies to — read this first

The phrase "bona fide resident" appears across the SERP as if it were a universal residency concept. It is not. Here is what it means for each reader segment.

US persons (citizens and green-card holders)

This is your test. The US taxes its citizens and lawful permanent residents on worldwide income regardless of where they live. The bona fide residence test, alongside the physical presence test, is one of two ways to qualify for the foreign earned income exclusion under §911. It does not eliminate your filing obligation. You still file Form 1040, you still file FBAR (FinCEN 114) if you have foreign accounts over $10,000 in aggregate (FinCEN), and you still file Form 8938 under FATCA above the relevant thresholds (IRS Form 8938 instructions). What the test does is exclude up to the §911 cap of qualifying earned income from US tax.

It does not exclude: passive income, capital gains, US-source income, self-employment tax (you still owe SECA on net SE earnings), or anything above the cap.

EU freelancers and digital nomads

The bona fide resident test is irrelevant to your domestic tax position. EU member states determine residency under their own rules — typically a 183-day rule combined with a "centre of vital interests" test under the OECD Model Tax Convention (OECD MTC Article 4). Where you live, where your family is, where your economic interests lie. If you are a French tax resident, France will tax your worldwide income; passing or failing the IRS bona fide residence test has no effect on that.

The reason to read this section: if you work with US clients or hold a US green card, the US test applies to you in parallel. Many EU-based freelancers with US green cards forget this and accumulate years of unfiled returns.

Non-US, non-EU readers

If you are not a US person and not an EU tax resident, the IRS bona fide residence test does not apply to you at all. The concept you care about is your own country's residency definition and any territorial-taxation regime you can use. The relevance of this article for you is comparative: the IRS test is one of the strictest in the world at distinguishing real residency from paper residency. Many countries that advertise "easy residency" use looser definitions that look attractive until a treaty partner — or your home country — applies an OECD-style tie-breaker and pulls you back into their tax net.

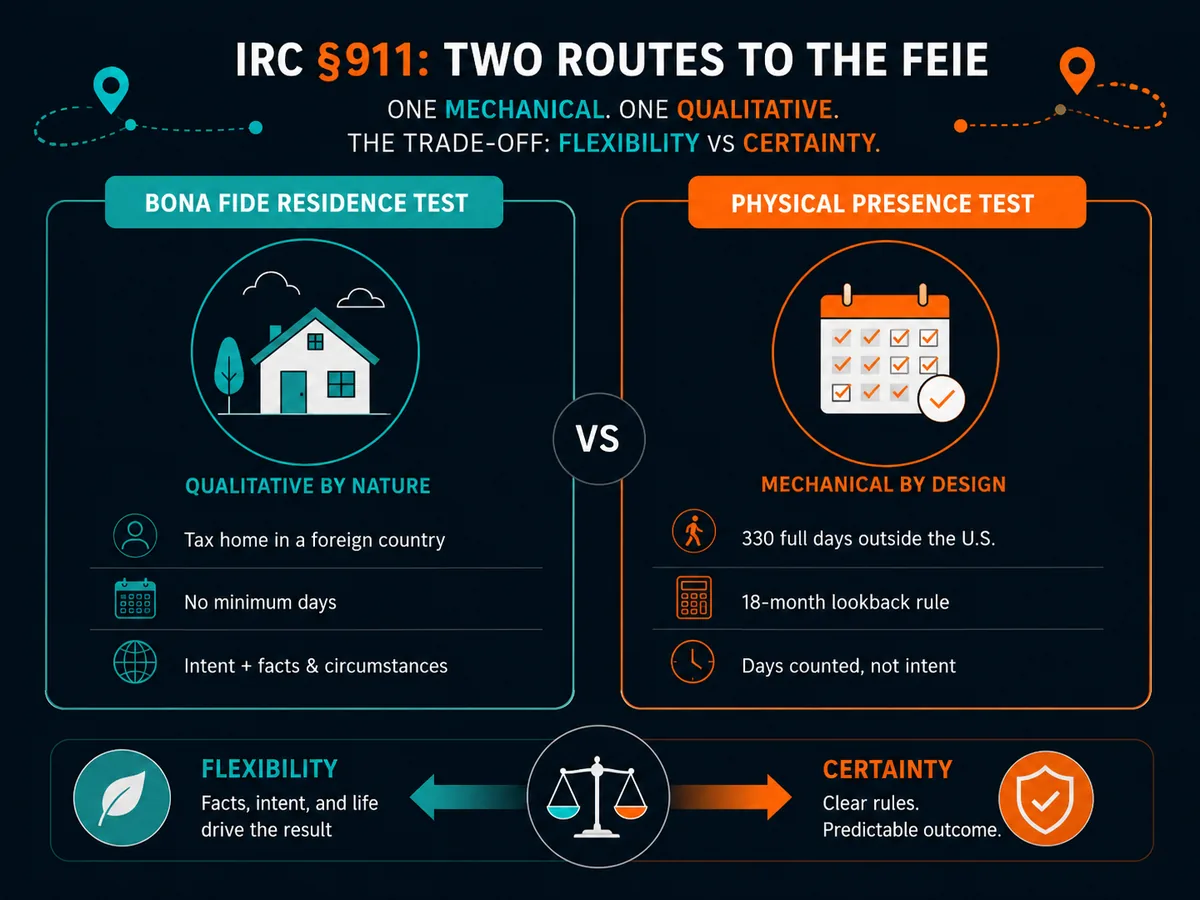

Bona fide residence vs the physical presence test

The two tests serve the same purpose — qualifying for the FEIE — but work very differently.

| Feature | Bona fide residence | Physical presence |

|---|---|---|

| Statutory basis | IRC §911(d)(1)(A) | IRC §911(d)(1)(B) |

| Period | Uninterrupted period including a full tax year | 330 full days in any 12 consecutive months |

| Counts | Intent, ties, integration | Days only |

| Who can use it | US citizens, plus resident aliens from treaty countries | Any US person |

| Trips back to US | Allowed if temporary, intent to return abroad | Each US day reduces your 330 count |

| Determined | After the fact by IRS, case by case | Mathematically |

| Best for | Long-term expats with settled lives abroad | Year-one movers, nomads, contract workers |

Source: IRS FEIE overview and IRS Publication 54.

The headline practical difference: physical presence is binary and provable. Bona fide residence is subjective and challengeable. The trade-off is flexibility. A bona fide resident can spend several weeks a year in the US for business or family without breaking the test. A taxpayer on physical presence cannot — every US day chips at the 330.

What qualifies — the four factors the IRS actually weighs

Form 2555 asks questions designed to surface the following:

1. Tax home in a foreign country. Your "tax home" is your regular place of business. If you have no regular place of business, it's your regular place of abode. You cannot be a bona fide resident if your tax home is the US — which usually means you cannot have a US home you treat as your primary residence (IRS: tax home).

2. Foreign tax treatment. Have you filed a tax return as a resident in the foreign country? Crucially, if you submitted a statement to the foreign authorities claiming non-resident status to avoid their tax, you are barred from claiming bona fide residence under IRC §911(d)(5). This trips up nomad-visa users in countries like Portugal, Malaysia and Thailand whose visa frameworks sometimes treat them as non-residents for tax.

3. Length and nature of stay. Indefinite is better than fixed. A two-year contract with a return date works against you. An open-ended move with a long lease works for you.

4. Ties. Family with you, household goods shipped, local driver's licence, foreign bank account used as primary, schooling for children locally — these all weigh in your favour. A US home left furnished, US cars, US schools for the family, US bank as your operating account — all weigh against.

The IRS reviews these in combination. No single factor is decisive. The famous illustrative case is Sochurek v. Commissioner (7th Cir. 1962), still cited in IRS guidance for its eleven-factor analysis.

Bona fide resident of a US territory — a different test

When people Google "bona fide resident," a large share are asking about Puerto Rico, the US Virgin Islands, Guam, American Samoa or the CNMI. The framework is different.

Under IRC §937, a bona fide resident of a US territory must meet three tests for the year:

- Presence test — generally 183 days in the territory, with several alternative ways to meet it (see IRS Publication 570).

- Tax home test — your tax home cannot be outside the territory.

- Closer connection test — you cannot have a closer connection to the US or a foreign country than to the territory.

This is the regime behind Puerto Rico's Act 60 (formerly Acts 20 and 22), which can reduce tax on Puerto Rico-source income for genuine residents. The headline rate is attractive — 4% on qualifying business income, 0% on qualifying capital gains accrued after the move — but the residency bar is real, and the IRS audits it actively (GAO report on PR Act 60 [source: TODO — confirm latest GAO/Treasury report on Act 60 compliance]).

Crucially, US-source income remains taxed by the US even for Act 60 residents. You cannot move to San Juan and shelter a Texas rental property or a New York consulting practice.

Bona fide resident in the Philippines and other non-US contexts

The phrase "bona fide resident" also appears in non-US legal contexts — most commonly Philippine election and residency law, where it refers to genuine residence in a barangay or municipality for purposes of voting or running for office. That is a domestic Philippine concept and has no connection to IRS rules. If you are a US person living in the Philippines, your US filing turns on the IRS test described above; your Philippine status turns on Philippine law (the Bureau of Internal Revenue's 180-day rule for resident aliens — BIR).

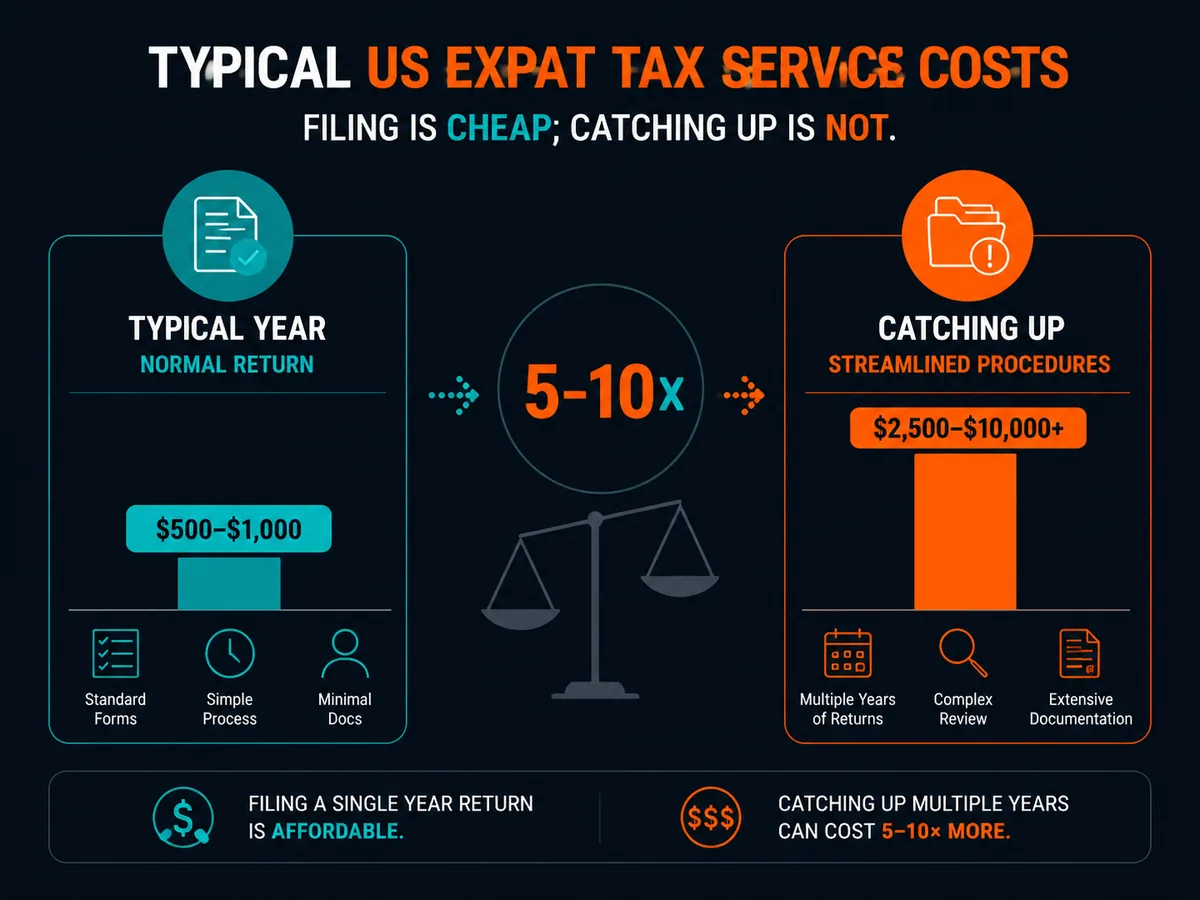

Realistic costs and timeline

Claiming bona fide resident status is procedurally cheap but substantively expensive — the cost is in the lifestyle commitment, not the filing fee.

| Item | Typical cost (US$) | Notes |

|---|---|---|

| Form 2555 prep by an expat CPA | $400 – $900 | Included in most expat tax packages |

| Full expat return (1040 + 2555 + FBAR + 8938) | $700 – $2,000 | Higher with foreign business interests |

| Foreign tax residency certificate (where issued) | $0 – $200 | Process varies by country |

| Streamlined Filing Procedure (if catching up) | $2,500 – $6,000 | Three years of returns + six years FBARs |

| Time to qualify (calendar) | 12 – 24 months | Must include one full Jan-Dec tax year |

| IRS review window after filing | 3 years statute, longer if substantial omission | IRC §6501 |

Sources: [source: TODO — survey of 3-5 expat CPA firms for current pricing]. Greenback, MyExpatTaxes, Bright!Tax and Taxes for Expats publish indicative pricing.

The timeline matters. You cannot qualify in the year you move unless you arrive early enough to also cover the next full tax year as a resident. Most movers use physical presence for year one (or a part-year approach) and switch to bona fide residence from year two onward.

Common mistakes

Filing a non-resident return in the host country. Doing this to avoid foreign tax automatically disqualifies you under §911(d)(5). The most expensive own goal in this area.

Keeping a US home as a "just in case." A US house you can return to at any time undermines the closer-connection argument. If you rent it out at arm's length to an unrelated tenant on a long lease, that helps. If it sits empty waiting for you, that hurts.

Treating nomad visas as residency. Many "digital nomad visas" are designed not to create tax residency in the host country. Estonia's e-Residency, Portugal's old D7 with the RNH structure, and several Caribbean nomad visas fall into this category in various ways. If the host country does not consider you a tax resident, the IRS may not either (IRS: tax home in foreign country).

Assuming FEIE eliminates US tax. It excludes earned income up to the cap. Above the cap, on passive income, on capital gains, on self-employment tax, you still owe. The FEIE is a useful tool, not an escape hatch.

Forgetting FBAR and 8938. The exclusion is on income tax. Reporting obligations are independent and the penalties for non-filing are severe — up to $10,000 per non-wilful FBAR violation, more for wilful (31 USC §5321).

Mixing the foreign country test with the territory test. They are different statutes (§911 vs §937), different forms, different requirements. Puerto Rico is not a "foreign country" for §911 purposes.

Bona fide residence does not solve the US persons problem

Worth saying plainly: passing the bona fide residence test does not make you a non-US taxpayer. The US taxes its citizens on worldwide income regardless of residence. The only ways out of that system are renunciation of citizenship (with an exit tax under IRC §877A if you are a covered expatriate) or, for green-card holders, formal abandonment of LPR status.

Everything else — bona fide residence, physical presence, foreign tax credits, treaty positions — operates inside the US tax system. It reduces what you owe. It does not let you stop filing. Any service or scheme that suggests otherwise is wrong, and in some configurations it is criminal.

When to consult a professional

In all of these situations, talk to a cross-border CPA or tax attorney before you act, not after:

- You are moving abroad mid-year and unsure which test fits year one.

- You are a US person planning to use Puerto Rico Act 60.

- You hold equity in a foreign company (PFIC and CFC rules — GILTI, Subpart F — may apply regardless of bona fide residence).

- You have unfiled US returns from prior expat years.

- You are considering renunciation.

- You hold a green card and live primarily outside the US.

Two professionals, not one: a US-side advisor and a host-country advisor. The most expensive errors happen when one side optimises in isolation.

For Soveraine's view on how we choose and disclose any service mentions, see our editorial policy and affiliate disclosure. We do not currently recommend a single expat tax provider — the right choice depends heavily on your country, business structure and complexity.

Ready to act on this?

Bright!Tax — US expat tax filings (FBAR + FATCA + FEIE specialists). Soveraine readers go to the front of the line through our partner link, and you fund independent editorial in the process.

FAQ

What is a bona fide resident?

Under US tax law, a bona fide resident is a US citizen — or in some cases a US resident alien from a treaty country — who has established genuine residence in a foreign country for an uninterrupted period that includes one full tax year (January 1 to December 31). The IRS looks at intent, ties to the host country, type of housing, family location and the length of stay. There is no single checklist; the determination is made case by case after you file Form 2555. Passing the test unlocks the foreign earned income exclusion and the foreign housing exclusion.

How is bona fide residence different from the physical presence test?

The physical presence test is mechanical: 330 full days outside the United States in any rolling 12-month period. It only counts days. The bona fide residence test is qualitative: it asks whether you actually live abroad, with all that implies — a home, a tax filing in the host country, integration into local life. You can leave a bona fide residence for short trips, including back to the US, without losing status. You cannot do that under physical presence without resetting the count.

Who qualifies as a bona fide resident of a US territory?

Different rules. For territories like Puerto Rico, the US Virgin Islands, Guam, American Samoa and the Northern Mariana Islands, the IRS uses a separate three-part test under IRC §937: a presence test (generally 183 days in the territory), a tax home test, and a closer connection test. This is the framework behind Puerto Rico's Act 60. It is not the same as the foreign country bona fide residence test under §911, and the two cannot be mixed.

How do I qualify for bona fide resident status?

You need to live in a foreign country for an uninterrupted period that covers a full tax year, file taxes there as a resident (not as a non-resident), and demonstrate intent to remain indefinitely. Practical evidence: a long-term lease or property purchase, local tax registration, family present with you, local bank accounts, local driver's licence, club memberships, and the absence of a US home you return to. You claim it by filing Form 2555 with your US return. The IRS reviews after the fact.

What documents prove bona fide residency?

There is no single certificate. The IRS expects a paper trail: a residence permit or visa for the host country, a long-term lease or property deed, foreign tax returns filed as a resident, utility bills in your name, local bank statements, employment contract with a local entity, school enrolment for children, and a statement of non-residence in the US (no homestead exemption, no state tax return as resident). The host country may issue a tax residency certificate — useful, but not by itself sufficient for US purposes.

What happens to IRS debt when someone dies?

IRS debt does not disappear at death. It becomes a liability of the estate, paid before heirs receive anything. The executor files a final Form 1040 for the year of death and, if the estate is large enough, Form 706. Unpaid tax becomes a federal claim against estate assets. Heirs are not personally liable unless they received property subject to a federal tax lien, or unless they signed a joint return. For expats, foreign assets are still part of the US estate of a US citizen or domiciliary.## Sources

- IRS — Foreign Earned Income Exclusion: Bona Fide Residence Test. https://www.irs.gov/individuals/international-taxpayers/foreign-earned-income-exclusion-bona-fide-residence-test

- IRS — Foreign Earned Income Exclusion (overview). https://www.irs.gov/individuals/international-taxpayers/foreign-earned-income-exclusion

- IRS — Exceptions to the Bona Fide Residence and Physical Presence Tests. https://www.irs.gov/individuals/international-taxpayers/exceptions-to-the-bona-fide-residence-and-the-physical-presence-tests

- IRS — Tax Home in Foreign Country. https://www.irs.gov/individuals/international-taxpayers/foreign-earned-income-exclusion-tax-home-in-foreign-country

- IRS Publication 54 — Tax Guide for US Citizens and Resident Aliens Abroad. https://www.irs.gov/forms-pubs/about-publication-54

- IRS Publication 570 — Tax Guide for Individuals with Income from US Territories. https://www.irs.gov/forms-pubs/about-publication-570

- IRS Rev. Proc. 2024-40 —