Opening a company bank account in 2026 is no longer the formality it was a decade ago. Banks are the front line of anti-money-laundering enforcement, and onboarding now involves identity checks, beneficial-ownership disclosure, source-of-funds questions and, increasingly, tax-residency verification. This article covers what the process actually looks like, what documents you need, what it costs, and how the rules differ depending on whether you are a US person, an EU tax resident, or based outside both blocs. It does not cover personal accounts, nor does it recommend any structure designed to obscure ownership — that path closed years ago.

Wise Business — Multi-currency business banking with lifetime affiliate cookie

What "opening a company bank account" actually means

A company bank account is a deposit account held in the legal name of an incorporated entity — an LLC, Ltd, GmbH, SAS, or equivalent — separate from any personal account of its owners. The account exists so the company can receive revenue, pay expenses, and produce auditable financial records distinct from the founders' personal finances.

Two things have changed since 2020. First, beneficial ownership reporting is now mandatory in most major jurisdictions: the US Corporate Transparency Act (FinCEN BOI reporting), the EU's 5th and 6th Anti-Money Laundering Directives, and the UK's Persons of Significant Control register all require the bank to identify every human who owns 25% or more. Second, tax-residency disclosure under the OECD's Common Reporting Standard means the bank will report your account to the tax authority of every country where you or the company is resident (OECD CRS).

Who this applies to

The mechanics of opening an account are similar everywhere. The tax consequences are not.

US persons (citizens and green-card holders)

US citizenship-based taxation means a US person pays US tax on worldwide income regardless of where they live or where the company is incorporated (IRS — US Citizens and Resident Aliens Abroad). Opening a company account abroad does not change that. If you own 10% or more of a foreign corporation, you likely have a Form 5471 filing obligation. If the foreign account balance exceeds $10,000 at any point in the year, you owe an FBAR (FinCEN Form 114). GILTI and Subpart F rules can pull foreign company income into your US return immediately, even if you never distribute it. Incorporating offshore does not remove US tax — it usually adds compliance cost.

EU freelancers and digital nomads

EU tax residents are taxed where they have their centre of vital interests or spend more than 183 days, not where their company is registered. Most EU countries have CFC rules that attribute the profits of a low-tax foreign subsidiary back to the controlling resident (EU Anti-Tax Avoidance Directive). Exit taxes apply in Germany, France, the Netherlands and others when you move residency while holding company shares. A bank in Estonia or Cyprus will open your account, but your home tax authority will still receive the CRS report.

Non-US, non-EU readers

Residents of territorial-tax jurisdictions (UAE, Singapore, Malaysia, Panama, Hong Kong, Georgia, Paraguay and others) have the widest legal latitude. Foreign-source income is generally untaxed at home, CFC enforcement is weak or absent, and CRS reporting still happens but has fewer domestic tax consequences. This is the segment for whom international structuring tends to work as advertised — provided the residency is real, not a paper exercise.

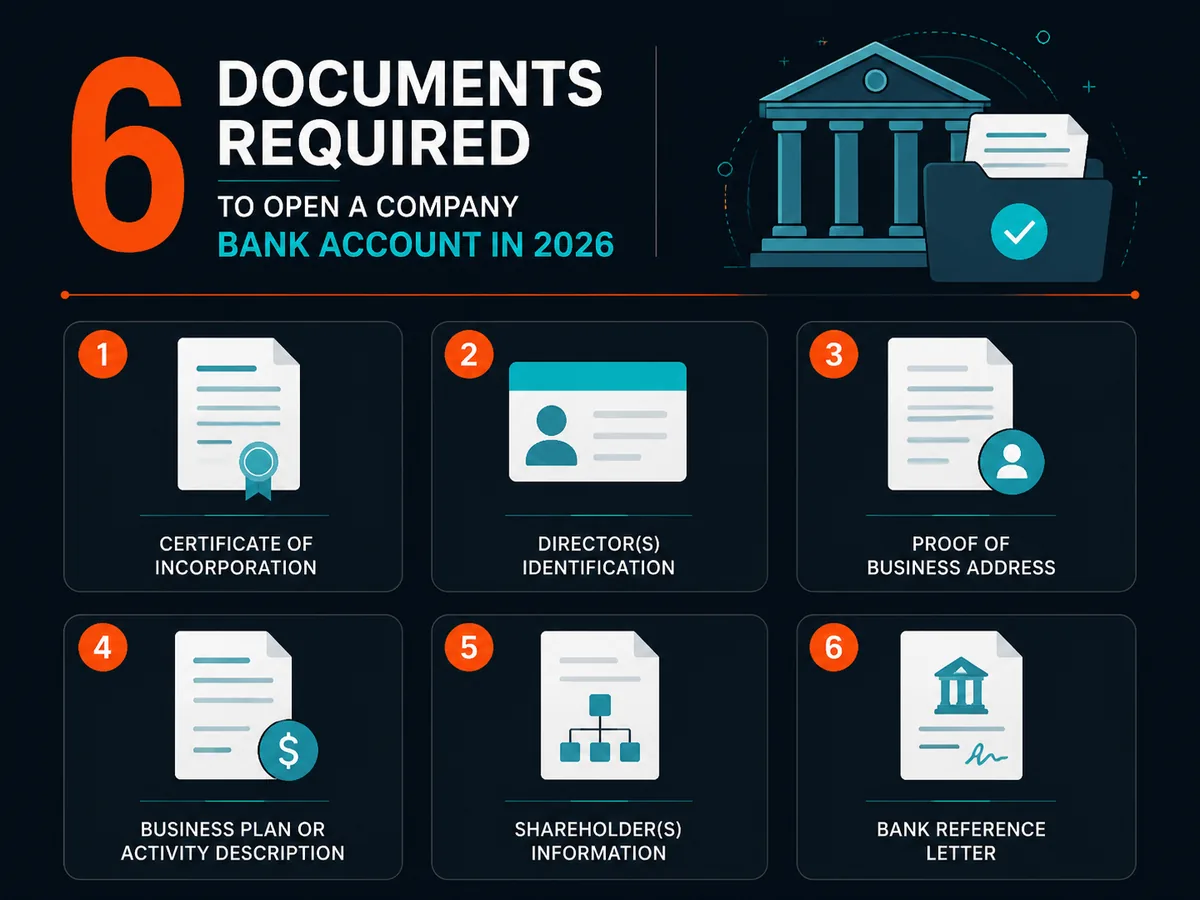

What documents you need

Every bank, in every jurisdiction, asks for variations of the same six items:

- Certificate of incorporation or formation (articles of association, operating agreement)

- Tax identification number — EIN (IRS EIN application) for US LLCs, VAT number for EU companies, equivalent local ID elsewhere

- Government photo ID for every beneficial owner ≥25% and every signatory

- Proof of business and residential address (utility bill, lease, registry extract — usually under 90 days old)

- Description of business activity — what the company sells, to whom, in which countries, expected monthly turnover

- Source-of-funds evidence — payslips, prior business accounts, sale contracts, investment statements

Banks dealing with non-resident-owned entities will also ask for a tax residency certificate from the country where the beneficial owner files taxes.

Why open one at all

Two reasons, both unglamorous. Legal separation: commingling personal and business funds is the fastest way to lose limited-liability protection if the company is sued — courts call this piercing the corporate veil. Tax substance: a company that uses the owner's personal account looks like a sham to tax authorities applying substance-over-form analysis, particularly under the EU's ATAD and the OECD's BEPS framework.

Realistic costs, fees and timeline

| Provider type | Setup time | Monthly fee | Notes |

|---|---|---|---|

| US high-street (Chase, BofA) | 1 day in branch | $0–$30 | Requires SSN/ITIN and US address |

| Mercury, Relay (US fintech) | 3–10 days online | $0 | Open to non-resident US LLC owners |

| Wise Business | 2–7 days online | £0 + per-transaction | Multi-currency, no overdraft |

| EU incumbent (BNP, Deutsche) | 2–6 weeks | €10–€30 | Strong SEPA, slow onboarding |

| Revolut Business / Qonto | 1–5 days | €10–€45 | Faster but more rejections for cross-border owners |

| UAE / Singapore local bank | 4–12 weeks | $25–$100 | In-person meeting usually required |

Figures based on published 2026 pricing pages [source: TODO — link each provider's current pricing page at publish time].

The PAA questions, briefly

The $10,000 rule, the $3,000 rule and the "will they get suspicious" question are answered in the FAQ below. The short version: these are reporting thresholds under the US Bank Secrecy Act (FinCEN — BSA), not limits on what you can legally move. Document your source of funds and the reports are administrative noise. Try to dodge them and you commit a separate crime called structuring.

Common mistakes

- Using a personal account "just for now." It contaminates your bookkeeping and exposes you to veil-piercing.

- Opening in a jurisdiction with no business nexus. A Latvian bank account for a Wyoming LLC with a Dubai resident owner and no customers in any of those places will get frozen at the first compliance review.

- Understating expected turnover at onboarding. Banks set internal thresholds based on what you tell them. Exceeding them by 10x in month two triggers a review.

- Treating fintech accounts as banks. Mercury, Wise and Revolut Business are not chartered banks in most jurisdictions — your deposits are held at partner banks, and protection varies. Read the terms.

When to consult a professional

Before incorporating across borders, before changing tax residency, and before any transaction that crosses a CRS or FATCA reporting threshold, get advice from a qualified tax adviser in both your country of residence and the country where the company is registered. Cross-border structuring is one of the few areas where the cost of getting it wrong — back taxes, penalties, criminal exposure — vastly exceeds the cost of an hour with a competent professional.

Soveraine does not provide legal or tax advice. See our editorial policy and disclaimer for how we cover these topics.

Ready to act on this?

Wise Business — Multi-currency business banking with lifetime affiliate cookie. Soveraine readers go to the front of the line through our partner link, and you fund independent editorial in the process.

FAQ

What is the $10,000 bank rule?

US banks must file a Currency Transaction Report with FinCEN for any cash deposit, withdrawal or exchange over $10,000 in a single business day. This is a reporting threshold under the Bank Secrecy Act, not a legal limit. Splitting deposits to stay below it is structuring, a separate federal crime under 31 U.S.C. § 5324, regardless of whether the underlying money is legal. The rule applies to cash only; wires and cheques are tracked through other systems.

What is needed to open a company bank account?

Incorporation documents, a tax ID (EIN, VAT number or local equivalent), government photo ID for every beneficial owner above 25%, proof of business address, and a description of the activity and expected transaction volumes. Most banks now also ask for source-of-funds evidence and, for non-resident owners, proof of tax residency. Online providers ask for the same documents — they just process them faster.

What bank is best to open a business account?

There is no universal answer. For US-resident LLC owners, Chase, Bank of America and Mercury cover most needs. For non-resident US LLC owners, Mercury, Relay and Wise Business are realistic. For EU companies, local incumbents give the cleanest SEPA access; Revolut and Qonto are faster but stricter on cross-border ownership. Choose by jurisdiction, residency and payment corridors.

Will the bank get suspicious if I deposit $150,000 cash into my account?

Yes. The deposit triggers an automatic Currency Transaction Report and will likely prompt a Suspicious Activity Report review. The bank cannot tell you a SAR was filed. Expect questions about source of funds and possibly a temporary hold. The deposit is not illegal if the money is legal and documented — but bring paperwork, not explanations.

What is the $3,000 rule for banks?

Under FinCEN's recordkeeping rules (31 CFR 1010.410), banks must log detailed information for cash purchases of monetary instruments — cashier's cheques, money orders, traveller's cheques — between $3,000 and $10,000. The rule targets the use of monetary instruments to move cash without triggering a CTR. It applies to the bank's recordkeeping, not to ordinary deposits or wires.

Can I open a business bank account with an EIN only?

Yes, with a narrow set of fintech providers. Mercury, Relay and Wise Business onboard non-resident-owned US LLCs using the EIN, formation documents and a foreign passport. Traditional banks almost always require an SSN or ITIN and a US address for at least one signatory. The EIN proves the company exists for tax purposes; it does not satisfy KYC on the humans behind it.## Sources

- FinCEN — Beneficial Ownership Information Reporting: https://www.fincen.gov/boi

- FinCEN — Bank Secrecy Act: https://www.fincen.gov/resources/statutes-and-regulations/bank-secrecy-act

- IRS — US Citizens and Resident Aliens Abroad: https://www.irs.gov/individuals/international-taxpayers/us-citizens-and-resident-aliens-abroad

- IRS — Apply for an Employer Identification Number (EIN): https://www.irs.gov/businesses/small-businesses-self-employed/apply-for-an-employer-identification-number-ein-online

- OECD — Common Reporting Standard: https://www.oecd.org/tax/automatic-exchange/common-reporting-standard/

- European Commission — Anti-Tax Avoidance Directive: https://taxation-customs.ec.europa.eu/taxation/business-taxation/anti-tax-avoidance-directive_en

- 31 U.S.C. § 5324 (Structuring): https://www.law.cornell.edu/uscode/text/31/5324

- 31 CFR 1010.410 (Recordkeeping for monetary instruments): https://www.ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1010