The Malta Global Residence Programme (GRP) is a special tax-status scheme that lets non-EU, non-EEA and non-Swiss nationals become Maltese tax residents and pay a flat 15% on foreign income they bring into Malta. It is not a passport scheme, not a path to citizenship, and not a way out of US tax filing. This guide explains what the GRP actually does, what it costs in 2026, and how it lands differently depending on whether you hold a US, EU or other passport. We cite the Maltese statute and tax-authority pages throughout — competing summaries online often paraphrase the rules loosely, and the details matter.

La Vida Golden Visas — UK-based golden-visa specialist

What the Malta Global Residence Programme actually is

The GRP was introduced by Legal Notice 167 of 2013 and is codified in Subsidiary Legislation 123.148 of the Income Tax Act (legislation.mt). It grants successful applicants a special tax status — not a residence permit on its own. You still need a separate residence document, which the GRP application bundles together.

Two things make it interesting:

- Flat 15% on remitted foreign income. Income arising outside Malta is taxed at 15% only when remitted to Malta. Income kept abroad is not taxed by Malta at all. Foreign capital can be remitted tax-free (Malta Tax & Customs Administration).

- No minimum stay. Unlike most residence programmes, you are not required to spend a set number of days in Malta. You must not, however, spend more than 183 days in any other single country.

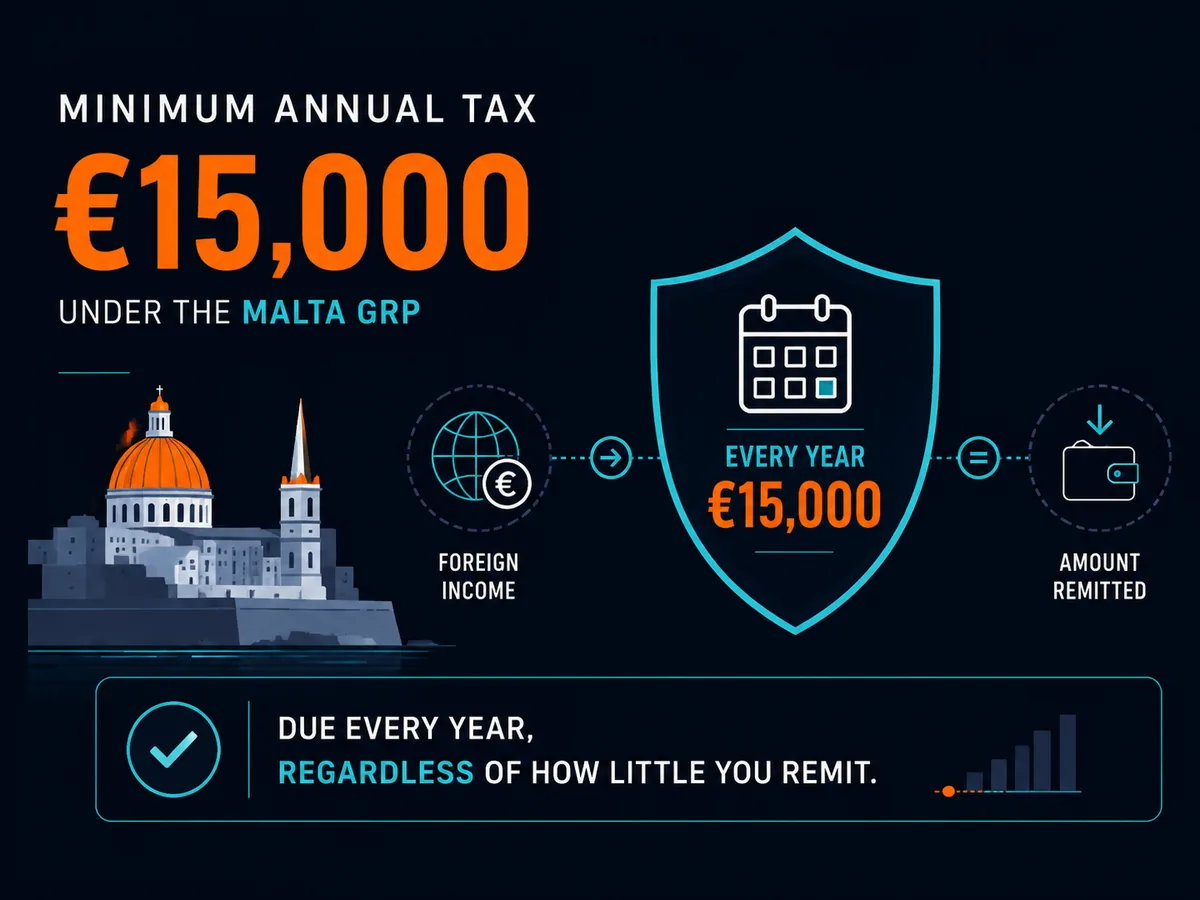

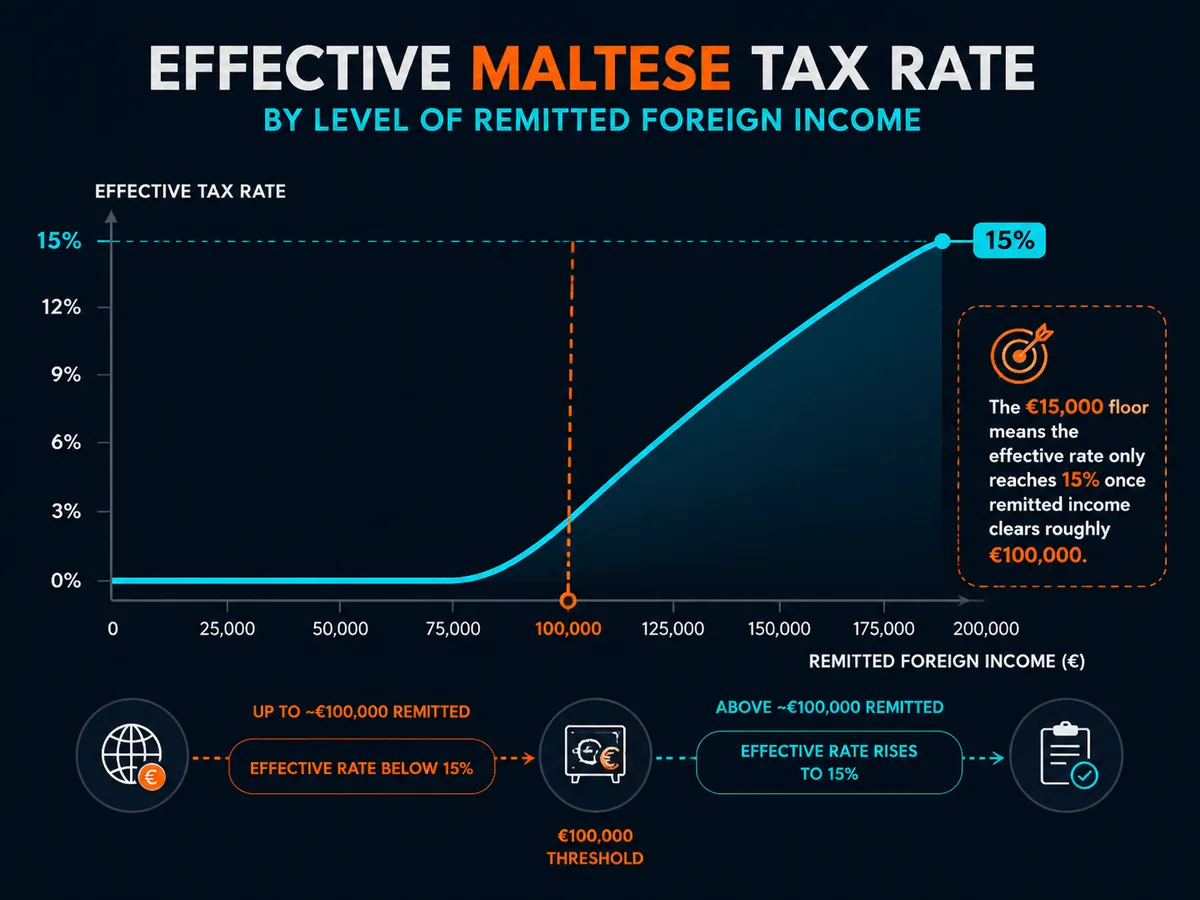

The price of the status is a minimum annual tax of €15,000, payable whether or not you remit that much. Malta-source income is taxed separately at standard rates up to 35%.

Who this applies to — by nationality

The GRP's value depends almost entirely on your passport and your prior tax residence. Be honest about which bucket you are in before you read further.

US persons

US citizens and green-card holders are taxed on worldwide income regardless of where they live. The IRS makes this explicit (IRS — International Taxpayers). Moving to Malta does not change that. You will still file Form 1040, still file FBARs for foreign accounts over $10,000 aggregate (FinCEN Form 114), and still report under FATCA on Form 8938 where thresholds apply.

What the GRP can do for a US person:

- Provide an EU base with predictable tax treatment on the non-US side.

- Let you use foreign tax credits against the Maltese 15% to reduce double taxation.

- Reduce exposure to the higher rates of your previous residence country, if that country had any.

What it cannot do: lower your US tax bill in any meaningful way for most income types. Only renunciation does that, and renunciation carries its own exit-tax consequences under IRC §877A. Anyone selling you a Malta structure as a US tax shelter is misleading you.

EU freelancers and digital nomads

EU, EEA and Swiss nationals are not eligible for the GRP. The parallel scheme for EU/EEA/Swiss applicants is the Residence Programme (TRP), which mirrors the GRP's 15% remittance treatment and €15,000 minimum tax (MTCA — Residence Programme Rules).

If you are an EU freelancer leaving a high-tax country (Germany, France, Spain, Netherlands), you need to handle three things before Malta will save you money:

- Break tax residence cleanly in your departure country. The 183-day rule is the floor; the real test is your centre of vital interests under each bilateral double-tax treaty.

- Check exit taxes. France, Germany and Spain levy exit taxes on unrealised gains for significant shareholdings (OECD — Exit Tax overview).

- Watch CFC rules. EU member states implement the Anti-Tax Avoidance Directive (ATAD), which can attribute the income of low-taxed foreign companies back to controlling EU residents (EU Council Directive 2016/1164).

Non-US, non-EU readers

This is the segment for whom the GRP works closest to the brochure. If your home country uses territorial taxation or has weak enforcement of CFC and exit rules, you can use Malta as a low-friction EU base with the 15% flat rate doing real work. You still need to verify your home country does not consider you tax resident after departure — many countries retain a "domicile" or "ordinarily resident" test that survives a passport stamp.

Realistic costs, fees and timeline

Numbers below are 2026 figures from the Maltese statute and the Authorised Registered Mandatories who file these applications. Property prices are statutory minima, not market reality — actual rental and purchase prices in desirable parts of Malta run well above the floor.

| Item | Cost | Notes |

|---|---|---|

| Government application fee | €6,000 (€5,500 if property in Gozo/south) | One-off, non-refundable (SL 123.148) |

| Minimum property purchase | €275,000 Malta / €220,000 Gozo & south | Or rent: €9,600 / €8,750 per year |

| Minimum annual tax | €15,000 | Payable every year, whether or not income reaches that level |

| Health insurance | ~€500–€2,000/year | Must cover all EU risks |

| ARM (advisor) fees | €5,000–€15,000 | Required intermediary; shop around |

| Due-diligence checks | ~€500 per applicant | Plus dependants |

| Timeline | 3–6 months | From filed application to certificate |

The minimum tax is the line most readers miss. If you earn €40,000 of remitted foreign income, your effective rate is 37.5%, not 15%. The programme makes financial sense above roughly €100,000 of remitted income, where the flat 15% starts to bite below the minimum.

What the law says vs. what providers commonly do

Several providers market the GRP with claims that drift from the statute. A few worth flagging:

- "You don't need to spend any time in Malta." Technically true — no minimum-day rule. But you must hold the property as your principal residence worldwide. Spending zero nights there while telling your home tax authority you live in Malta is a fact pattern that does not survive a residency audit. Treaty tie-breaker rules look at where your home, family and economic interests actually sit (OECD Model Tax Convention, Article 4).

- "Foreign income is tax-free if not remitted." True under Maltese law. False as a global statement if your home country still taxes you on worldwide income, which is the case for US persons and for anyone who has not properly broken residence elsewhere.

- "€15,000 buys you EU residence." The €15,000 is the minimum tax, not the total cost. Add property, ARM fees, insurance and government fees. First-year all-in for a renter is typically €30,000–€40,000.

Common mistakes and how to avoid them

- Treating the GRP as a citizenship route. It is not. Maltese citizenship by naturalisation for exceptional services (Identità Malta) is a separate, far more expensive programme that has faced repeated EU Commission challenges.

- Forgetting the remittance trap. Money remitted to Malta is taxed. Many GRP holders run their living costs through a Maltese account without realising every transfer creates a taxable event for income (not capital).

- Skipping the source-of-funds file. Maltese due diligence is genuine. Build a clean paper trail before you file: bank statements, payslips or business accounts, tax returns from your prior jurisdiction.

- Ignoring the home-country exit. The single biggest failure point is not Malta's process — it is the fact that France, Germany or the IRS still considers you resident. Get a tax-residency certificate from Malta and use it to formally exit your prior jurisdiction.

When to consult a qualified professional

Before signing any ARM engagement letter, get independent advice from:

- A tax advisor in your current country of residence, who can confirm how and when you stop being taxable there.

- A tax advisor in Malta (the ARM doubles as this, but a second opinion is cheap insurance).

- For US persons: a US-licensed CPA or tax attorney with international experience. The interaction between GRP status, GILTI, Subpart F and PFIC rules is technical and unforgiving.

Soveraine is editorial — we publish guides, not advice. See our editorial policy and disclaimer for what that means in practice.

FAQ

Who qualifies for the Malta Global Residence Programme?

The GRP is open to nationals of non-EU, non-EEA and non-Swiss countries who are not already long-term residents of Malta. Applicants must hold or rent qualifying property in Malta, prove a stable income, hold health insurance covering all EU risks, and pass a fit-and-proper test. EU, EEA and Swiss nationals are excluded from the GRP but can apply under the parallel Residence Programme (TRP), which carries the same 15% tax treatment on remitted foreign income.

How is income taxed under the GRP?

Beneficiaries are taxed on a source-and-remittance basis. Foreign-source income remitted to Malta is taxed at a flat 15%, subject to a minimum annual tax of €15,000. Malta-source income is taxed at the standard progressive rates, up to 35%. Foreign-source income that stays outside Malta is not taxed by Malta, and foreign capital is not taxed even if remitted. Double-tax relief is available against the 15% rate.

What property must I buy or rent?

You must hold qualifying immovable property. Minimum purchase prices are €275,000 in Malta or €220,000 in Gozo and the south of Malta. Minimum annual rents are €9,600 in Malta or €8,750 in Gozo and the south. The property must be your principal residence worldwide and cannot be let or sublet. The minimum-value tests apply at acquisition.

Does the GRP work for US citizens?

Only partially. Maltese tax residence does not release US persons from US worldwide taxation or from FATCA and FBAR reporting. A US citizen on the GRP still files a 1040, still reports foreign accounts, and still owes US tax on global income with foreign tax credits applied. The GRP can reduce non-US tax exposure and provide an EU base, but it does not lower the US tax bill in most cases. Speak to a US-licensed tax advisor before relying on it.

How long does the application take?

Filed through an Authorised Registered Mandatory (ARM), the process typically runs three to four months from submission to certificate. Property acquisition, due diligence and apostilled document gathering add lead time. Plan on six months end-to-end. Initial paperwork includes police clearance, proof of income, health insurance, source-of-funds documentation and the property deed or lease.

Do I need to live in Malta full-time?

No. There is no minimum physical-presence requirement. But you cannot spend more than 183 days in any other single jurisdiction, and Malta must be your principal place of residence worldwide. The GRP certificate is reviewed annually, and you must file a Maltese tax return and pay the €15,000 minimum tax each year. Spending too little time in Malta while claiming it as your base invites scrutiny from your previous home country's tax authority.

Ready to act on this?

La Vida Golden Visas — UK-based golden-visa specialist. Soveraine readers go to the front of the line through our partner link, and you fund independent editorial in the process.

Sources

- Malta Tax & Customs Administration — Global Residence Programme Rules: https://mtca.gov.mt/personal-tax/individual/special-schemes/global-residence-programme-rules

- Subsidiary Legislation 123.148 — Global Residence Programme Rules: https://legislation.mt/eli/sl/123.148/eng

- Malta Tax & Customs Administration — Residence Programme Rules (EU/EEA/Swiss equivalent): https://mtca.gov.mt/personal-tax/individual/special-schemes/residence-programme-rules

- IRS — US Citizens and Resident Aliens Abroad: https://www.irs.gov/individuals/international-taxpayers/us-citizens-and-resident-aliens-abroad

- FinCEN — Report of Foreign Bank and Financial Accounts (FBAR): https://bsaefiling.fincen.treas.gov/main.html

- EU Council Directive 2016/1164 (Anti-Tax Avoidance Directive): https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32016L1164

- OECD Model Tax Convention on Income and on Capital: https://www.oecd.org/tax/treaties/model-tax-convention-on-income-and-on-capital-condensed-version-20745419.htm

- Identità Malta — Citizenship services: https://identita.gov.mt/