Georgia advertises a 1% tax for small entrepreneurs and the headline is accurate as far as it goes. The Small Business Status regime taxes gross turnover at 1% up to GEL 500,000 per calendar year — roughly USD 180,000 — for sole proprietors registered as Individual Entrepreneurs with the Revenue Service. The catch is in the qualifiers. The rate applies to turnover not profit; several activities are excluded; you need 183 days in the country to benefit as a tax resident; and your home country may pull most of the income back regardless. This review covers what the 1% actually is, who it works for, how to qualify, costs, and failure modes — written for US persons, EU residents, and readers tax-resident outside both blocs.

Bright!Tax — US expat tax filings for citizens abroad (FBAR, FATCA, FEIE specialists)

What Georgia's 1% tax actually is

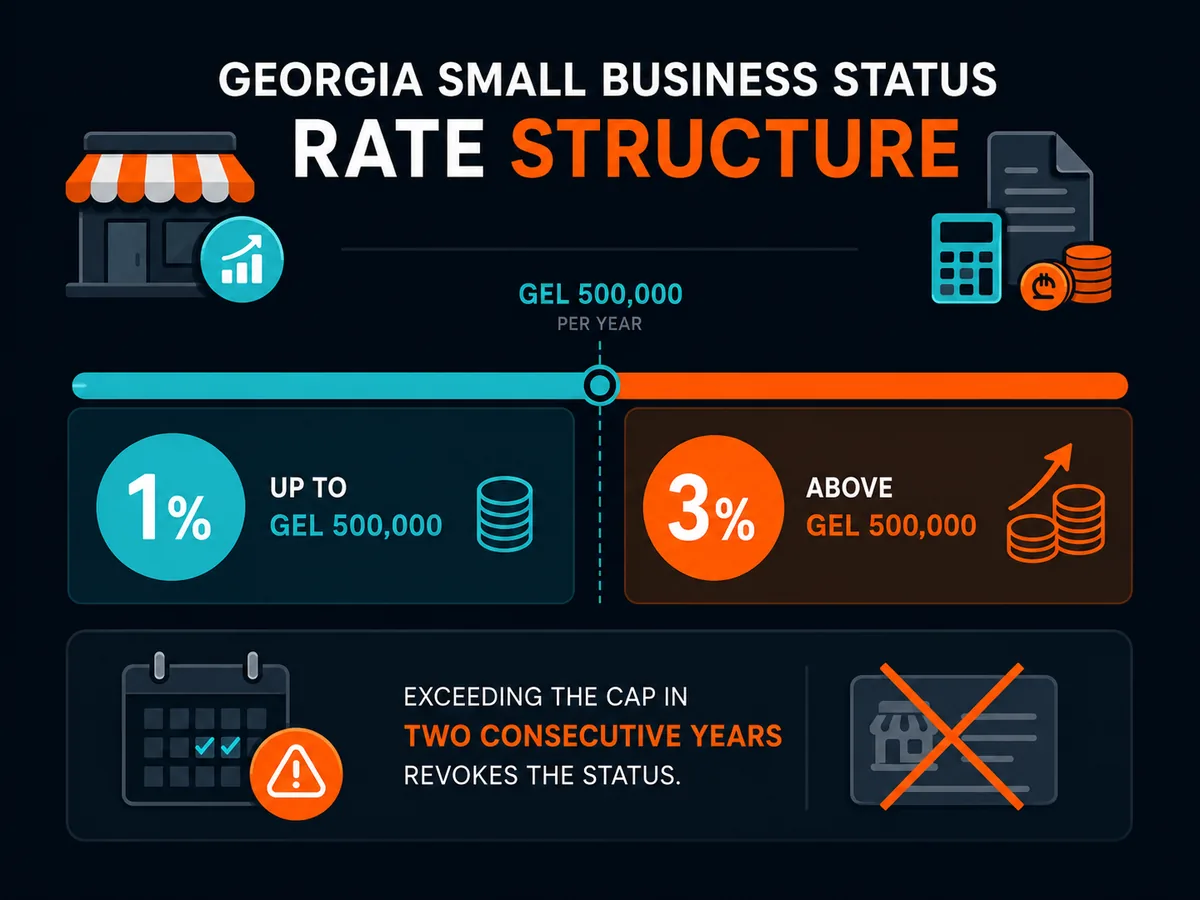

Small Business Status is a special regime for Individual Entrepreneurs governed by Article 90 of the Georgian Tax Code. Eligible Individual Entrepreneurs pay 1% of gross turnover instead of the standard 20%, provided turnover stays below the statutory threshold.

The threshold is GEL 500,000 per calendar year. Turnover above the cap is taxed at 3% for that year. If the cap is breached in two consecutive years, the Georgian Revenue Service revokes the status and the entrepreneur reverts to 20%. The regime suits low-six-figure freelancers and consultants; it is not designed for businesses scaling past USD 180,000.

Two structural points matter. First, this is a turnover tax not a profit tax. A consultant with USD 100,000 turnover and USD 10,000 costs pays USD 1,000 on the full USD 100,000. A dropshipper with USD 100,000 turnover and USD 90,000 ad spend also pays USD 1,000 — a 10% effective rate on the USD 10,000 of profit. The regime favours high-margin service work.

Second, Small Business Status applies to Individual Entrepreneurs (sole proprietors), not Georgian limited liability companies. A Georgian LLC pays 15% corporate income tax on distributed profits under the Estonian-style model adopted in 2017. The 1% headline does not apply to companies.

The Tax Code and decrees from the Ministry of Finance bar Small Business Status for banking, currency exchange, gambling, medical and dental services, notarial work, architectural and legal consulting, audit, and any licensed activity. Invoicing for a single excluded service can disqualify the status retroactively.

Who this applies to — read this first

The Georgian regime is the same for everyone who qualifies. What changes by audience is the home-country tax that runs on top of it.

US persons

US citizens and green-card holders are taxed on worldwide income under 26 U.S. Code Section 61 regardless of where they live. Paying 1% in Tbilisi does not reduce the US filing burden — it changes the calculation, not the obligation.

Two reliefs partially offset this. The Foreign Earned Income Exclusion under IRC Section 911 excludes up to USD 130,000 of earned income for 2025 if the physical presence or bona fide residence test is met. The Foreign Tax Credit allows Georgian tax paid to offset US tax due on the same income. There is no US-Georgia income tax treaty in force, which limits some planning and complicates Social Security totalisation.

US persons also face FBAR (FinCEN Form 114) reporting for Georgian accounts exceeding USD 10,000 in aggregate, and potentially Form 8938 under FATCA. A US person who forms a Georgian LLC instead of registering as an Individual Entrepreneur triggers Form 5471 and potentially GILTI on retained earnings.

EU residents

The 183-day Georgian residency rule interacts with each EU member state's own tests. A French or German resident spending 183 days in Georgia can become Georgian tax resident — but France and Germany apply additional tests (centre of vital interests, habitual abode, family ties) that can override day-counting. The result is dual residency, resolved by treaty tiebreaker rules.

Georgia has bilateral tax treaties with most EU member states (full list at the Georgian Revenue Service). The tiebreaker usually resolves to where the taxpayer has a permanent home or centre of vital interests. Keep an apartment, family, or business operations in your prior EU country and the treaty is unlikely to land in Georgia's favour.

CFC rules under Articles 7-8 of the EU Anti-Tax Avoidance Directive attribute the income of low-taxed foreign entities back to the resident shareholder in most member states. An EU resident who genuinely severs ties can use the regime; one who keeps a foot in the EU usually cannot.

Non-US, non-EU readers

Readers tax-resident in jurisdictions without CFC enforcement or worldwide taxation have the cleanest path. A South African, British, Australian, Singaporean, or Hong Kong resident who genuinely relocates and meets the 183-day test can benefit with few home-country complications. UK residents should check the Statutory Residence Test under FA 2013 Schedule 45 before assuming UK residence has ceased. Australian residents face the "ordinarily resident" test and need to formally break residence to escape Australian tax. Georgia became a Common Reporting Standard jurisdiction in 2023 and shares account information with partner countries.

How to qualify

The mechanical steps are straightforward. The compliance work around them is where most setups go wrong.

Step 1: Enter Georgia. Citizens of approximately 95 countries — including the US, UK, EU member states, Canada, Australia, and Japan — can enter visa-free for up to one year per entry under Ordinance N255. This is the structural feature that makes the regime accessible.

Step 2: Register as an Individual Entrepreneur. Visit the Public Service Hall in Tbilisi or Batumi with your passport. Standard processing is one business day. You receive a Tax Identification Number and registration certificate. A local address is required — service providers offer registered-address services for USD 100 to USD 300 per year.

Step 3: Apply for Small Business Status. Submit Form 100 to the Georgian Revenue Service declaring the activities you will undertake. Status takes effect from approval, not retroactively. Until approval, turnover is taxed at 20%.

Step 4: Establish tax residency. Physical presence of 183 days in any 12-month period creates Georgian tax residency under Article 34. The High Net Worth Individual programme offers an alternative for applicants meeting wealth or income criteria. Without tax residency your home country still taxes the same income, usually eliminating the benefit.

Step 5: Open a Georgian bank account. Bank of Georgia and TBC Bank are the main institutions, both offering multi-currency accounts in GEL, USD, and EUR. Onboarding has tightened since 2022 — applications now sometimes take one to three weeks rather than same-day. Having your Individual Entrepreneur registration in hand improves approval odds. Wise multi-currency accounts are commonly used as a bridge during onboarding.

Real costs and timeline

Setup costs are among the lowest of any low-tax jurisdiction. The structure rewards small operators rather than wealthy ones.

| Item | Cost (USD) | Notes |

|---|---|---|

| IE registration (Public Service Hall) | ~20 | Same-day or next-day issuance |

| Small Business Status application | 0 | Filed at Revenue Service |

| Registered address (year 1) | 100-300 | Service-provider fees |

| Initial accountant setup | 100-300 | Including translations |

| Bank account opening | 0-50 | Bank of Georgia or TBC |

| Ongoing accounting (monthly) | 50-150 | Depends on volume |

| Annual tax filing (year-end) | 100-200 | Included by some accountants |

Timeline. Steps 1 through 3 — entry, IE registration, Small Business Status — can be completed in three business days. Bank account opening currently takes one to three weeks. Tax residency requires 183 days of physical presence, so the full benefit lands in year two for new arrivals unless the HNWI route applies.

Monthly compliance. Individual Entrepreneurs file a turnover declaration via the Revenue Service portal by the 15th of each month for the prior month, paying 1% (or 3% above the cap). An annual return is due by 1 April. Most setups use a local accountant; the portal is primarily in Georgian.

The gotchas

Substance and source. Georgia operates a territorial system in principle, but income earned while physically present is Georgian-source. If you own a foreign company (US LLC, UK Ltd) and do all the work from Tbilisi, the Revenue Service can argue a Georgian permanent establishment exists and tax the income locally. Operating directly through the Individual Entrepreneur is cleaner than layering a foreign company on top.

Home-country CFC and exit tax. Most EU member states, the UK, Australia, and Canada apply CFC rules that attribute income of low-taxed foreign entities to resident shareholders. Several apply exit taxes when residency ceases. Speak to a tax advisor in your departure country — Henley & Partners handles cross-border residency planning for complex cases.

US filings continue. US citizens registering a Georgian LLC trigger Form 5471 and potentially GILTI. Individual Entrepreneur registration creates FBAR obligations once accounts exceed USD 10,000 aggregate. Failure carries civil penalties of USD 10,000 per non-wilful violation. Bright!Tax is worth the fee for US persons setting up abroad.

Banking risk. The same de-risking that complicates onboarding can also lead to account closures with limited notice. Keep a backup account elsewhere.

Political and operational context. Domestic politics are contested, with periodic protests in Tbilisi. Traffic and air quality are real lifestyle considerations. None of this affects the legal status of the regime — but a relocation rests on more than the tax rate. Healthcare is inexpensive but the public system is limited; most expats carry private cover via SafetyWing or similar.

Comparison table

Each low-tax jurisdiction carries a different trade-off between rate, presence requirement, and setup cost.

| Jurisdiction | Headline rate | Presence required | Setup cost (USD) | Source |

|---|---|---|---|---|

| Georgia Small Business Status | 1% turnover to GEL 500k | 183 days | 200-500 | Article 90 Tax Code |

| Estonia e-Residency company | 0% retained / 20% distributed | None (residency separate) | 500-1,500 | e-Resident.gov.ee |

| UAE Free Zone | 0% personal / 9% corp above AED 375k | 90 days for residency | 5,000-15,000 | UAE Federal Decree-Law 47/2022 |

| Cyprus non-dom | 0% on dividends / 12.5% corp | 60 days | 2,000-5,000 | Cyprus Tax Department |

Different operators win different rounds. Georgia leads on absolute cost and entry friction for a six-month-presence freelancer earning under USD 180,000. The UAE leads on flexibility and presence minimum but costs an order of magnitude more. Estonia is the cleanest pure structure for entrepreneurs who do not want to relocate — but it does nothing to solve personal tax residency.

When the 1% is real and when it isn't

The 1% rate is genuine for its target operator: a low-six-figure freelancer from a jurisdiction without aggressive worldwide taxation, willing to spend 183 days a year in Georgia, doing high-margin service work, not in an excluded activity. Combined with Tbilisi or Batumi cost of living, the regime compounds into meaningful capital accumulation over two to three years.

It is largely fictional for US citizens (who still owe US tax on worldwide income), partially fictional for EU residents who do not genuinely sever ties, and irrelevant for thin-margin businesses where 1% of revenue exceeds normal tax on profit. If residency, substance, and home-country rules stack up cleanly, Georgia is among the most accessible low-tax setups in the world. If any piece wobbles, the headline rate is a distraction from the bill that lands elsewhere.

This review is editorial. Soveraine may earn commissions on links to tax-prep and banking partners. See our affiliate disclosure and editorial policy. Nothing here is tax or legal advice — see our disclaimer.

Planning a Georgian setup?

If you are a US citizen, the Georgian 1% rate sits on top of US worldwide-income filing — Bright!Tax specialises in FBAR, FATCA and Foreign Earned Income Exclusion filings for Americans abroad and is the right starting point before any relocation.

Sources

- Georgian Tax Code: https://matsne.gov.ge/en/document/view/1043717

- Georgian Revenue Service: https://rs.ge/

- Ministry of Finance of Georgia: https://www.mof.ge/en

- Public Service Hall: https://psh.gov.ge/en

- Bank of Georgia: https://bankofgeorgia.ge/en

- TBC Bank: https://www.tbcbank.ge/web/en/

- Ordinance N255 (visa-free entry): https://matsne.gov.ge/en/document/view/2278806

- Georgian Revenue Service — tax treaties: https://rs.ge/CommonInformation/14/9d34f3d7-e2b6-4ee1-a83b-2b96e5d76b1a

- 26 U.S. Code Section 61: https://www.law.cornell.edu/uscode/text/26/61

- IRS — FEIE: https://www.irs.gov/individuals/international-taxpayers/foreign-earned-income-exclusion

- IRS — FBAR: https://www.irs.gov/businesses/small-businesses-self-employed/report-of-foreign-bank-and-financial-accounts-fbar

- IRS — Form 5471: https://www.irs.gov/forms-pubs/about-form-5471

- EU Anti-Tax Avoidance Directive: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32016L1164

- OECD Common Reporting Standard: https://www.oecd.org/tax/automatic-exchange/common-reporting-standard/

- UK Statutory Residence Test: https://www.legislation.gov.uk/ukpga/2013/29/schedule/45

- UAE Corporate Tax: https://mof.gov.ae/corporate-tax/

- Estonia e-Residency: https://www.e-resident.gov.ee/

- Cyprus Tax Department: https://www.mof.gov.cy/mof/tax/taxdep.nsf/index_en/index_en?OpenDocument