Spain's digital nomad visa — officially the visado para teletrabajo de carácter internacional — has been live since January 2023 under Law 28/2022. It lets non-EU remote workers reside legally in Spain, brings spouses and children along, and unlocks the Beckham Law tax regime. This article covers who qualifies, what it actually costs, how the tax treatment differs by passport, and where the paperwork tends to break. It is written for three readers: US citizens and green-card holders, EU freelancers considering relocating within the bloc, and non-US/non-EU applicants. If you hold an EU passport, you do not need this visa at all.

La Vida Golden Visas — UK-based golden-visa specialist

What the Spain digital nomad visa is

The digital nomad visa is a residence authorisation for non-EU nationals who work remotely for companies or clients based outside Spain. The legal basis is Law 28/2022 on the Startups Ecosystem, which amended Spain's immigration framework to create a new "international teleworker" category.

You can apply two ways: as a visa at a Spanish consulate in your home country (one-year initial validity, then convert to a three-year residence permit on arrival), or as a residence permit from inside Spain if you are already there legally — for example on a tourist stamp (source: Ministry of Foreign Affairs). The in-country route is processed by the UGE (Unidad de Grandes Empresas) and is typically faster.

Maximum stay is five years (one-year visa + one three-year renewal + one two-year renewal, depending on route). After five years of legal residence you can apply for long-term EU residence.

Who this applies to — by passport

EU, EEA and Swiss citizens

You do not need this visa. Under TFEU Article 21, you have the right to move and reside freely in Spain. Register with the Central Register of Foreigners and obtain a NIE. Tax residency still applies if you spend more than 183 days in Spain in a calendar year.

US persons (citizens and green-card holders)

You can apply. You should also understand that the United States taxes citizens and permanent residents on worldwide income regardless of residence (IRS Publication 54). Moving to Spain does not change your US filing obligations: Form 1040, FBAR if your foreign accounts exceed $10,000 at any point in the year (FinCEN), and Form 8938 above the FATCA thresholds. The US–Spain tax treaty and foreign tax credits prevent most double taxation, but they do not exempt you from filing.

Non-US, non-EU readers

This is the cleanest case. If you are tax-resident in a territorial-tax country (Singapore, Hong Kong, UAE, Panama) or a country without strong CFC enforcement, moving to Spain triggers a clear residency switch on day 183. The Beckham Law, covered below, becomes genuinely valuable here.

Requirements and proof of income

The core conditions, set out in Article 71 of Law 14/2013 as amended:

- Non-EU/EEA/Swiss nationality.

- Three years of relevant work experience OR a university degree from a recognised institution.

- Existing employment or client relationship of at least three months with non-Spanish entities. Your employer must have existed for at least one year.

- Remote work clause in your contract, or evidence the work can be done remotely.

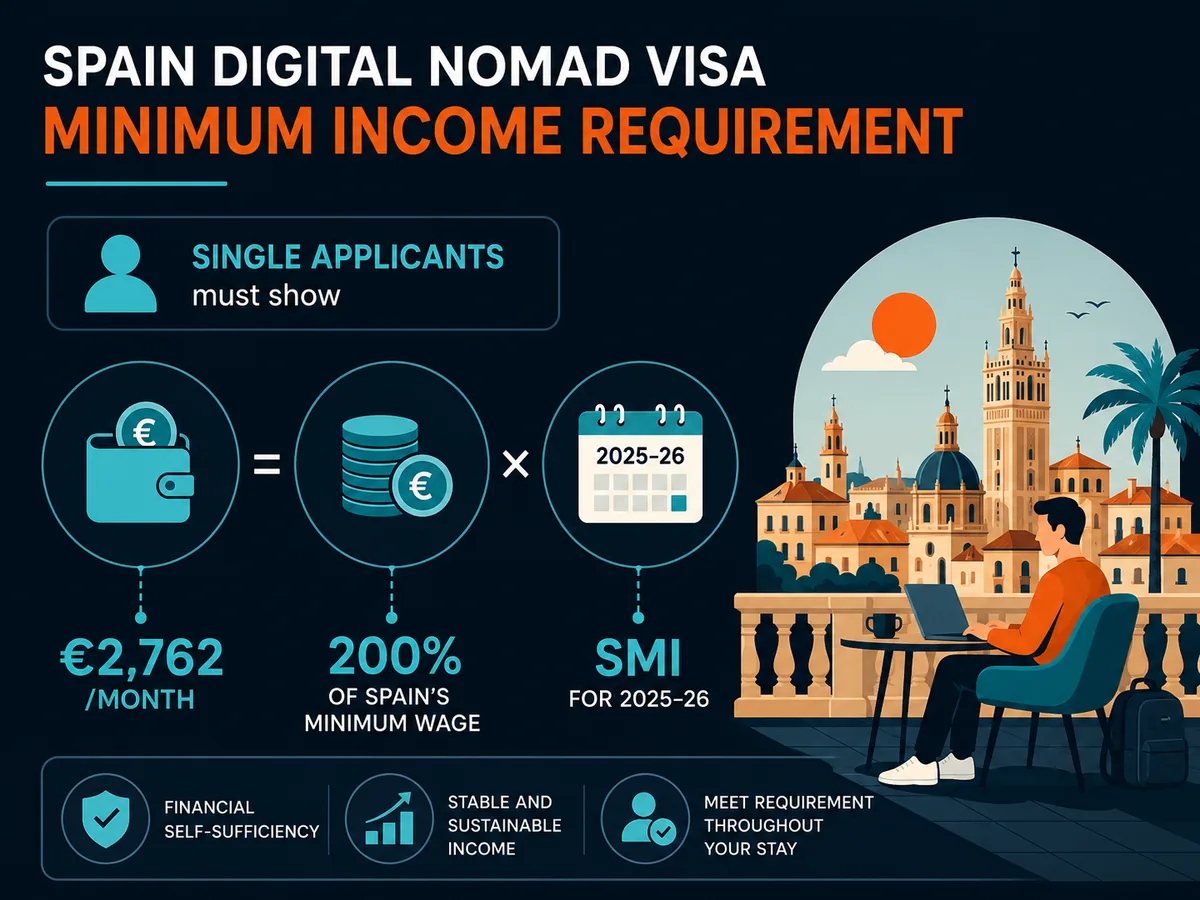

- Income of at least 200% of Spain's SMI — approximately €2,762/month or €33,144/year for 2025–26 (Ministry of Labour SMI reference).

- Add ~75% SMI for a spouse, 25% per child.

- Spanish-source income capped at 20% of total professional income (freelancers only).

- Private health insurance with full coverage in Spain, no co-pays, from an authorised insurer.

- Clean criminal record for the last five years, certified and apostilled from every country of residence.

- Form 790-038 fee paid (currently around €83 for the residence permit; consular visa fees vary by nationality, typically €60–€80).

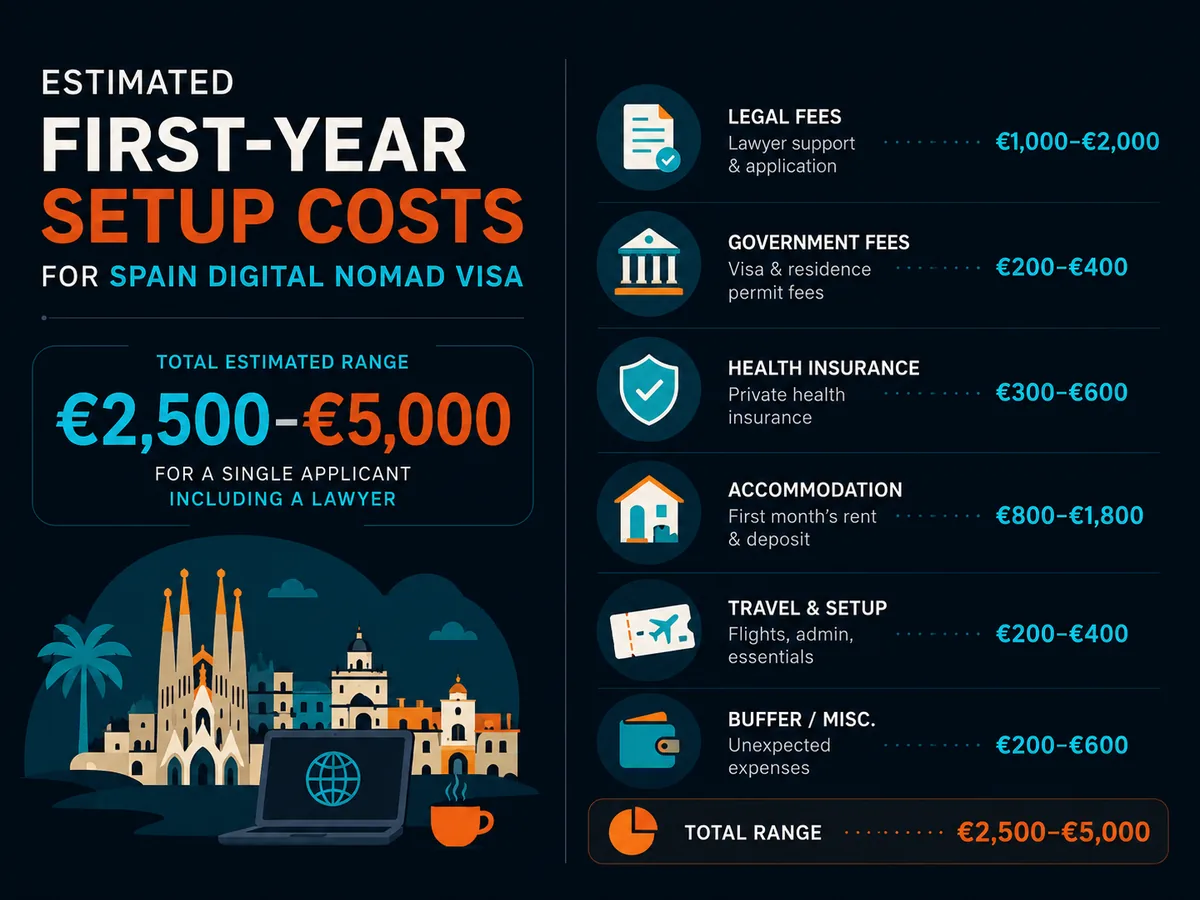

Costs and timeline

| Item | Approximate cost (EUR) | Notes |

|---|---|---|

| Consular visa fee | €60–€80 | Varies by nationality and reciprocity |

| In-country residence permit (Form 790-038) | €83 | UGE route |

| Apostille of documents (home country) | €10–€50 per document | US: state Secretary of State |

| Sworn Spanish translations | €30–€60 per page | Required for non-Spanish documents |

| Private health insurance | €50–€200/month | Sanitas, Adeslas, Cigna Global commonly accepted |

| Immigration lawyer (optional) | €1,500–€3,500 | First-application success rate materially higher |

| Total realistic first-year setup | €2,500–€5,000 | Single applicant, lawyer included |

Processing times: consular route typically 15–45 working days; UGE in-country route averages 20 working days by statute, often faster in practice (source: TODO — link to UGE current SLA page on inclusion.gob.es).

The tax question — Beckham Law and the catches

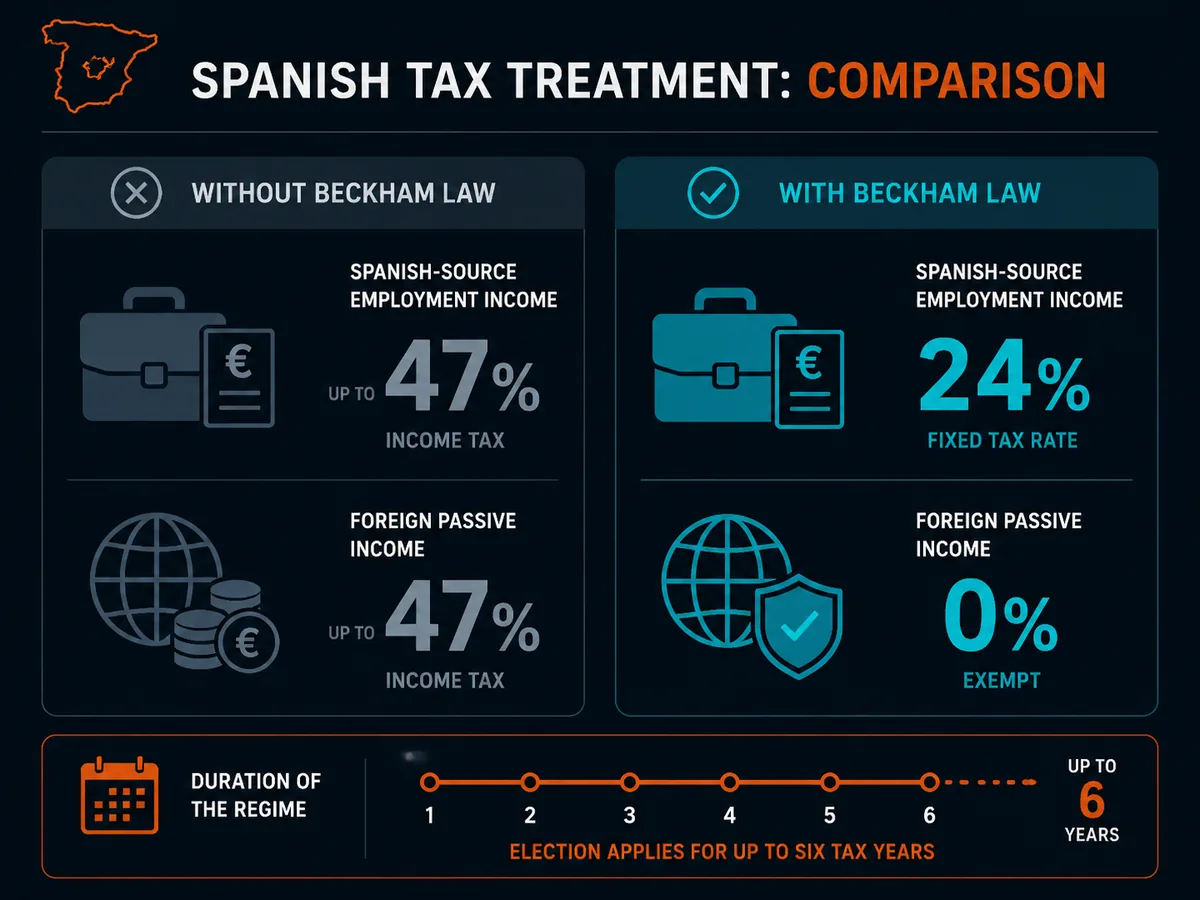

This is where the visa earns its reputation. Law 28/2022 extended Spain's special expat tax regime (commonly called the Beckham Law, codified in Article 93 of the Personal Income Tax Law, LIRPF) to digital nomad visa holders.

If you elect it by filing Form 149 within six months of registering with Spanish social security, you are taxed as a non-resident for up to six years:

- 24% flat rate on Spanish-source employment income up to €600,000; 47% above.

- No Spanish tax on most foreign-source passive income (dividends, interest, capital gains generated outside Spain).

- Exempt from wealth tax on assets located outside Spain.

- No Modelo 720 foreign-asset reporting obligation during the regime.

Without the election, you are a full tax resident: progressive rates from ~19% to 47% on worldwide income, plus wealth tax in most regions on net assets above €700,000 (with a primary-residence exemption up to €300,000), plus the temporary solidarity tax on fortunes above €3 million.

What this means by passport

US persons: the Beckham election reduces your Spanish bill, but you still file in the US. The US does not recognise the Beckham regime for treaty purposes in the way you might hope; coordination is through foreign tax credits on Form 1116, not exemption. You cannot use Spanish non-resident status to escape US worldwide taxation. Renunciation is the only legal route out of US worldwide tax — everything else is reporting.

EU freelancers: if you are leaving another EU country, watch for exit taxes (Germany, France, Netherlands all apply variants under ATAD Article 5) and ensure you genuinely break tax residency in the departure state — 183-day rule, centre of vital interests, permanent home test.

Non-US/non-EU readers: the Beckham Law works largely as advertised. Six years of low Spanish tax on foreign passive income is a genuine planning opportunity.

How hard is it, really

The visa is approvable but document-heavy. The common failure modes:

- Employer letters that do not specify remote work is permitted.

- Apostilles missing on criminal record certificates or degree diplomas.

- Translations not done by a sworn translator (traductor jurado) accredited in Spain.

- Health insurance with co-payments or hospital exclusions — Spanish consulates reject these routinely.

- Freelancers whose income mix shows more than 20% Spanish clients.

DIY applications succeed; they just succeed less often on the first try. Budget for one round of requerimiento (request for additional documents) if going alone.

Common mistakes

- Assuming the Beckham Law is automatic. It is not. File Form 149 within six months or you default to full worldwide taxation.

- Booking a long-term rental before getting NIE and empadronamiento. Many landlords require both.

- Closing your home-country tax residency cleanly. US persons cannot; EU readers must.

- Using a generic travel insurance policy. It will be rejected. You need a Spain-specific health policy meeting consular standards.

- Forgetting that the visa is tied to the work relationship you applied with. If you lose the contract, you must notify authorities and potentially re-qualify.

When to consult a professional

Before applying, talk to:

- A Spanish immigration lawyer if your case has any complication: prior Schengen overstays, family members on different passports, freelance income from multiple jurisdictions.

- A tax adviser in your home country to model exit-tax exposure, treaty interaction and timing.

- A Spanish asesor fiscal to file the Beckham election correctly and on time.

For US persons, the tax adviser should be a US CPA or EA familiar with expat returns, not a Spanish gestoría alone. The two sides of the file are independent and both must be right.

Soveraine is an independent editorial publication. We do not provide legal or tax advice. See our editorial policy, affiliate disclosure and disclaimer.

Ready to act on this?

La Vida Golden Visas — UK-based golden-visa specialist. Soveraine readers go to the front of the line through our partner link, and you fund independent editorial in the process.

FAQ

How hard is it to get a digital nomad visa in Spain?

Procedurally it is one of the more demanding EU nomad visas. You need a clean criminal record, private health insurance with full Spanish coverage, proof of at least three months working remotely for non-Spanish clients or employers, and income roughly double Spain's minimum wage. Most refusals come from incomplete paperwork — missing apostilles, untranslated documents, or contracts that do not clearly show the work is remote. Applicants who use a Spanish immigration lawyer typically succeed on the first attempt; DIY applicants more often face requirements to supply additional documents.

Who is eligible for the Spain digital nomad visa?

Non-EU/EEA/Swiss nationals who work remotely for companies based outside Spain, or freelancers whose Spanish-sourced income is no more than 20% of their total. You must show at least three months of prior relationship with your employer or main clients, a university degree or three years of relevant professional experience, monthly income around €2,762 (200% of Spain's SMI), and no criminal record gaps in the last five years. EU nationals do not need this visa — they have free movement rights under TFEU Article 21.

What are the disadvantages of Spain's nomad visa?

Three main ones. First, tax: without the Beckham Law election, you become a Spanish tax resident on worldwide income at progressive rates up to 47%. Second, Spain has wealth tax and, in some regions, a solidarity tax on net assets above €3 million. Third, the paperwork burden — apostilled documents, sworn translations, criminal record checks from every country you have lived in during the last five years. The visa also does not give you Schengen-wide work rights; you are authorised to reside in Spain specifically.

How much money do I need for a digital nomad visa in Spain?

The income threshold is tied to Spain's Minimum Interprofessional Wage. For 2025–26 it is approximately €2,762 per month, or €33,144 per year, for a single applicant. Add roughly 75% of the SMI for a spouse (~€1,036/month) and 25% per dependent child. You prove this through payslips, freelance contracts, or company financial statements covering at least the last three months. Most consulates also want to see savings, though there is no statutory bank balance requirement separate from the income test.

Does the Beckham Law apply to digital nomad visa holders?

Yes — and this is the visa's main tax draw. Law 28/2022 extended the special expat regime to digital nomad visa holders. If you elect it within six months of registering with Spanish social security, you are taxed as a non-resident: a flat 24% on Spanish-source employment income up to €600,000 (47% above), and generally no Spanish tax on foreign passive income. The election lasts up to six years. It is not automatic — you must file Form 149. US persons should note this does not reduce their US tax filing obligations.

Can US citizens use the Spain digital nomad visa to lower their taxes?

Partly. The Beckham Law can cut your Spanish tax bill significantly, but US citizens remain liable for US federal tax on worldwide income regardless of where they live. You can use the Foreign Earned Income Exclusion (about $130,000 for 2025) and foreign tax credits to avoid double taxation, but you must still file Form 1040, FBAR (FinCEN 114) for foreign accounts over $10,000, and potentially Form 8938. The US–Spain tax treaty helps coordinate the two systems but does not exempt you from US filing.## Sources

- Ministry of Foreign Affairs of Spain, Digital Nomad Visa — https://www.exteriores.gob.es/Consulados/londres/en/ServiciosConsulares/Paginas/Consular/Digital-Nomad-Visa.aspx

- Law 28/2022 on the Startups Ecosystem (BOE) — https://www.boe.es/eli/es/l/2022/12/21/28/con

- Law 14/2013 (entrepreneurs and internationalisation), as amended — https://www.boe.es/eli/es/l/2013/09/27/14/con

- Personal Income Tax Law (LIRPF), Article 93 — https://www.boe.es/eli/es/l/2006/11/28/35/con

- Treaty on the Functioning of the European Union, Article 21 — https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:12012E021

- EU Anti-Tax Avoidance Directive (ATAD), Article 5 (exit tax) — https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32016L1164

- IRS Publication 54, Tax Guide for US Citizens and Resident Aliens Abroad — https://www.irs.gov/publications/p54

- US–Spain Income Tax Treaty documents — https://www.irs.gov/businesses/international-businesses/spain-tax-treaty-documents

- FinCEN BSA E-Filing (FBAR / FinCEN 114) — https://bsaefiling.fincen.treas.gov/main.html

- Ministry of Labour of Spain — SMI normative reference — https://www.mites.gob.es/es/portada/serviciohogar/normativa/index.htm